About supply side, there is already massive consolidation that has already taken place. One of the very nice research pieces on this was published by Gera (@bheeshma, link, valuePickr post) who showed that consolidation has already taken place in micromarkets like Pune. I am citing this from their 2019 annual report (wordings are not exact though).

In 2017 it took 40 projects to cumulatively sell 10’000 homes in Pune which by 2019 came down to 17 projects to sell 10’000 homes. This implies that average sale of homes in a given project increased from 250 in 2017 to 588 in 2019.

I think the situation is very similar for other micromarkets, every reasonably large listed developer has sold more apartments in FY2020 compared to the previous 3 years.

About availability to credit, this is again super skewed to reputed developers and has nothing to do with size of developer. Godrej (who is the largest guy) has a borrowing cost of 7.75% (this is super low for any developer). Other smaller players like Sobha currently borrow at ~9.6%. Kolte now has a project platform where they get money from private equity who fund projects on an IRR basis. Even smaller players like Ashiana have credit lines with international organizations like IFC whose returns are directly related to project specific IRRs. Domestic mutual funds like ICICI are also super active in this space and fund specific projects. So availability of money is not a problem for reputed developers who have delivered in the past.

About oversupply of inventory, this is a market narrative and has nothing to do with reality. There are two micromarkets that are oversupplied (MMR, Delhi NCR). However, demand supply matches perfectly for markets such as Pune, Hyderabad and Bangalore. Frank Knight reports clearly state the inventory situation. Even within a city, there are multiple micromarkets which can be oversupplied. So its super region specific.

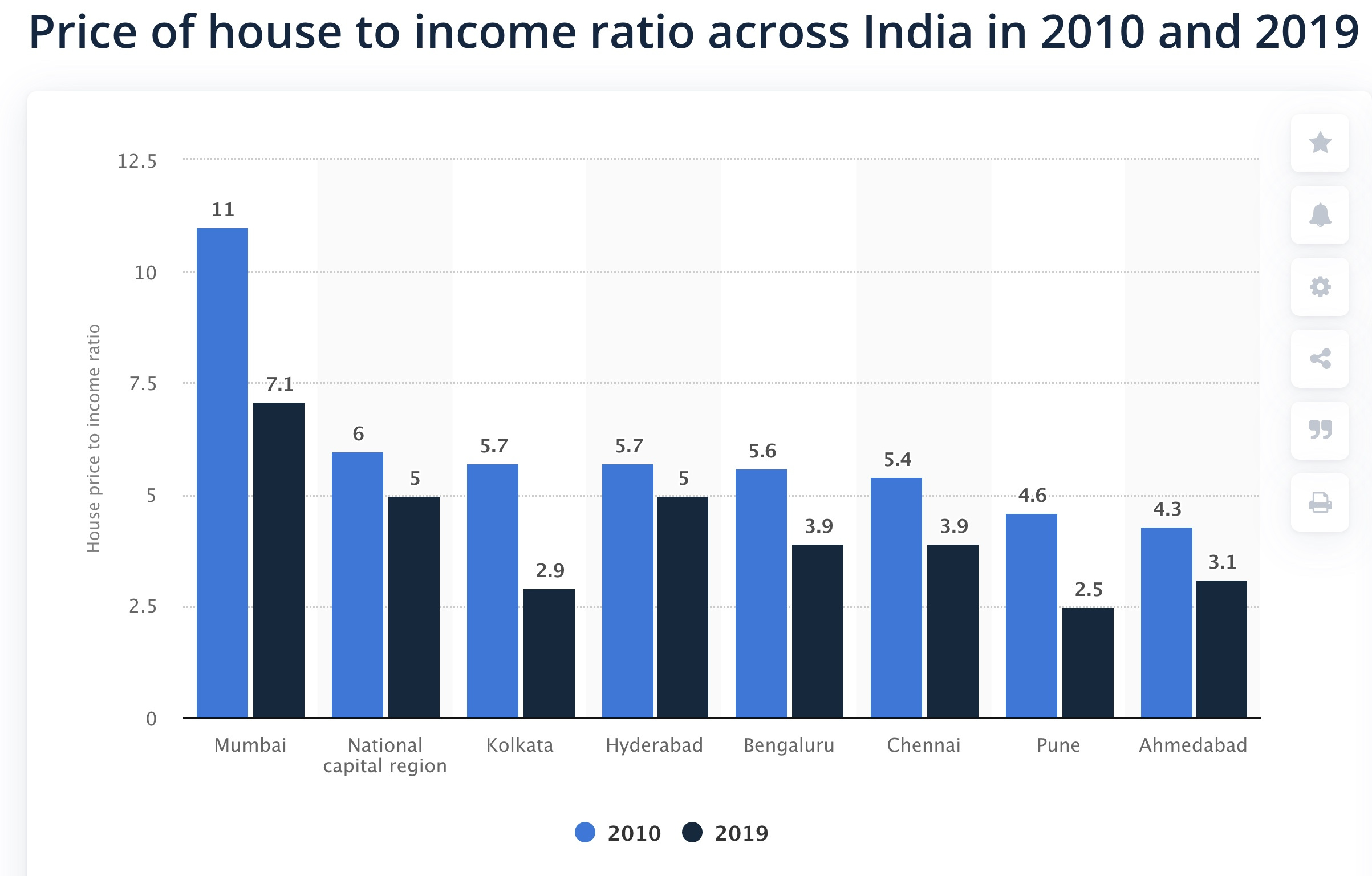

About pricing, real-estate prices are now much more affordable than what the case was a few years ago. I am attaching the price to income ratio graph below for major markets. Low interest rates and government SOPs make pricing further attractive. My family also has a real-estate broking business and we were able to broker the sale of a super luxury flat (priced at ~1.5cr.) in Ranchi during the lockdown. If people come with a reasonable price tag, there are buyers available.

About WFH and ruralization, this is again a market narrative and has nothing to do with reality. If this were true, it was not possible for Godrej to sell flats worth 1485 cr. in Q1FY21 (the lockdown quarter). And where did this sale come from? Bangalore (478 cr.), Pune (358 cr.), NCR (413 cr.) and MMR (236 cr.). And where did the demand come from? Premium housing as affordable housing is oversupplied now because of the large number of project launches in the past couple of years and very few launches in premium space. And how is buying? NRIs and people with a stable job. Savings have actually gone up for people who have a stable job and can continue working from home, because they cannot go out and spend money.