it’s good to find some discussion on worth peripheral (normally you don’t see it anywhere easily)

I am holding since IPO and added more during our dip last year.

Reason for Holding:

Migrated to NSE.

Value Buy (Good Dividend Player, Fundamentally Good, Good Management, Evergreen Industry, Industry expected to grow)

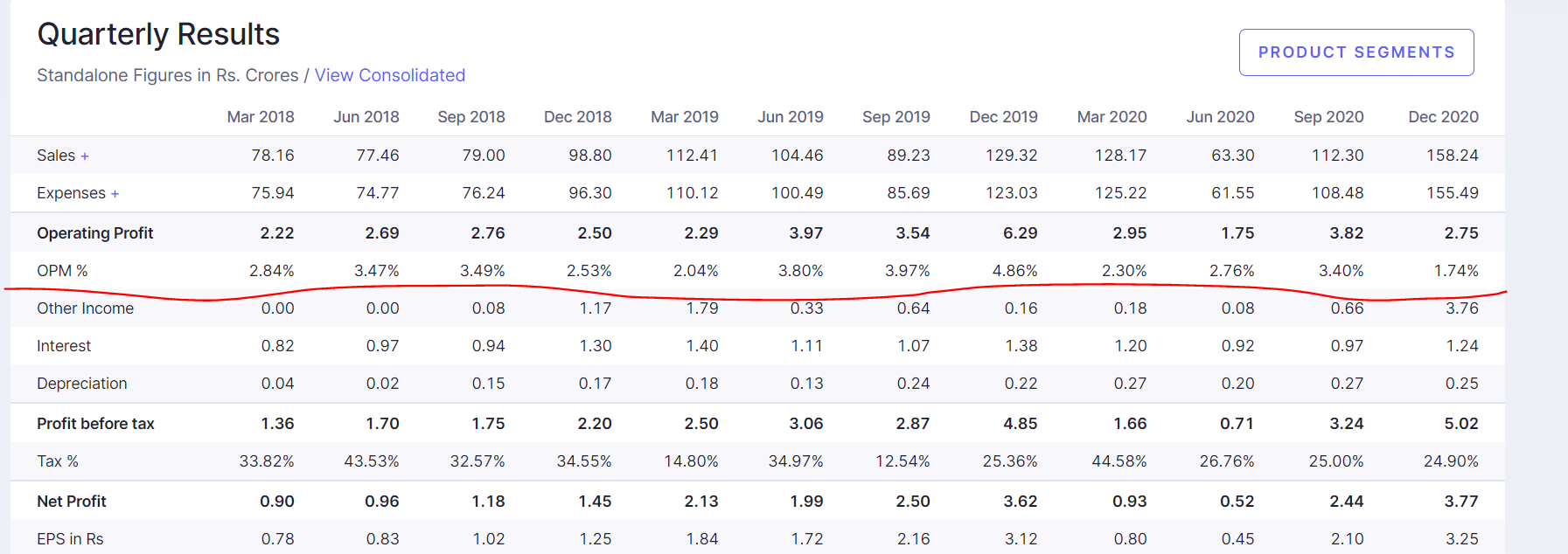

Raw Material prices have gone up for last 1 year, many players have already shut down. Worth is surviving tough phase now.

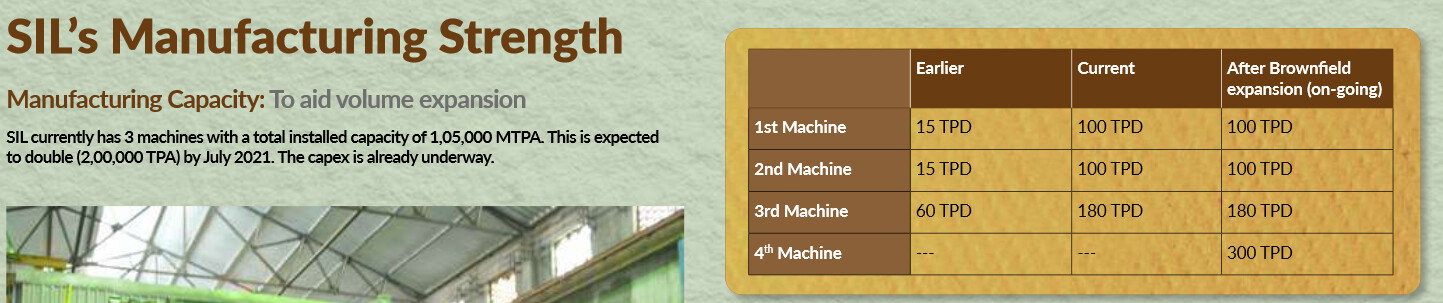

Increased capacity in 2019 (10 MT i guess after IPO with borrowing)

Applied land to manufacture of diapers (surprise to me) worth wellness private limited

Applied land to manufacture of corrugated boxes (expansion) - worth pack india private limited.

Incentives from MP Govt.

Market Cap - Almost 100 CR… lot of investors will find companies only if they are above 100 CR. hope things will change once we sustain 100 CR

Risk:

Highly fragmented industry - (though post covid, it may be different)

Raw Material Impact

Growth - Slow (suddenly things may change if we get approval and if all goes well)

I tried to get inputs from management but no response (concall / investors meet will be good).

They should focus to add more clients

Same here too

I did buy around 3k shares in hopes that the management will be co operative in letting us know what is actually happening. If you see the industry as a whole, There is excellent opportunity to grow. But on account of the stiff competition and similarity in products, One has to either innovate in products to attract more customers or innovate in the production process in order to keep their margin intact. However worth seems to manufacture only corrugated sheets which is the most basic material which would keep their margins low. As of now there is no unique selling point with the company which leaves it with no pricing power. The company has expanded capacity but there is very high concentration on both its buyers and suppliers. As far as i have read, I cannot relate it’s foray into diaper industry with anything they’ve done earlier. I had shot off a similar questionnaire to their cs team and am yet to get a reply due to COVID. With the limited information available we can only hope anything not actually know things.

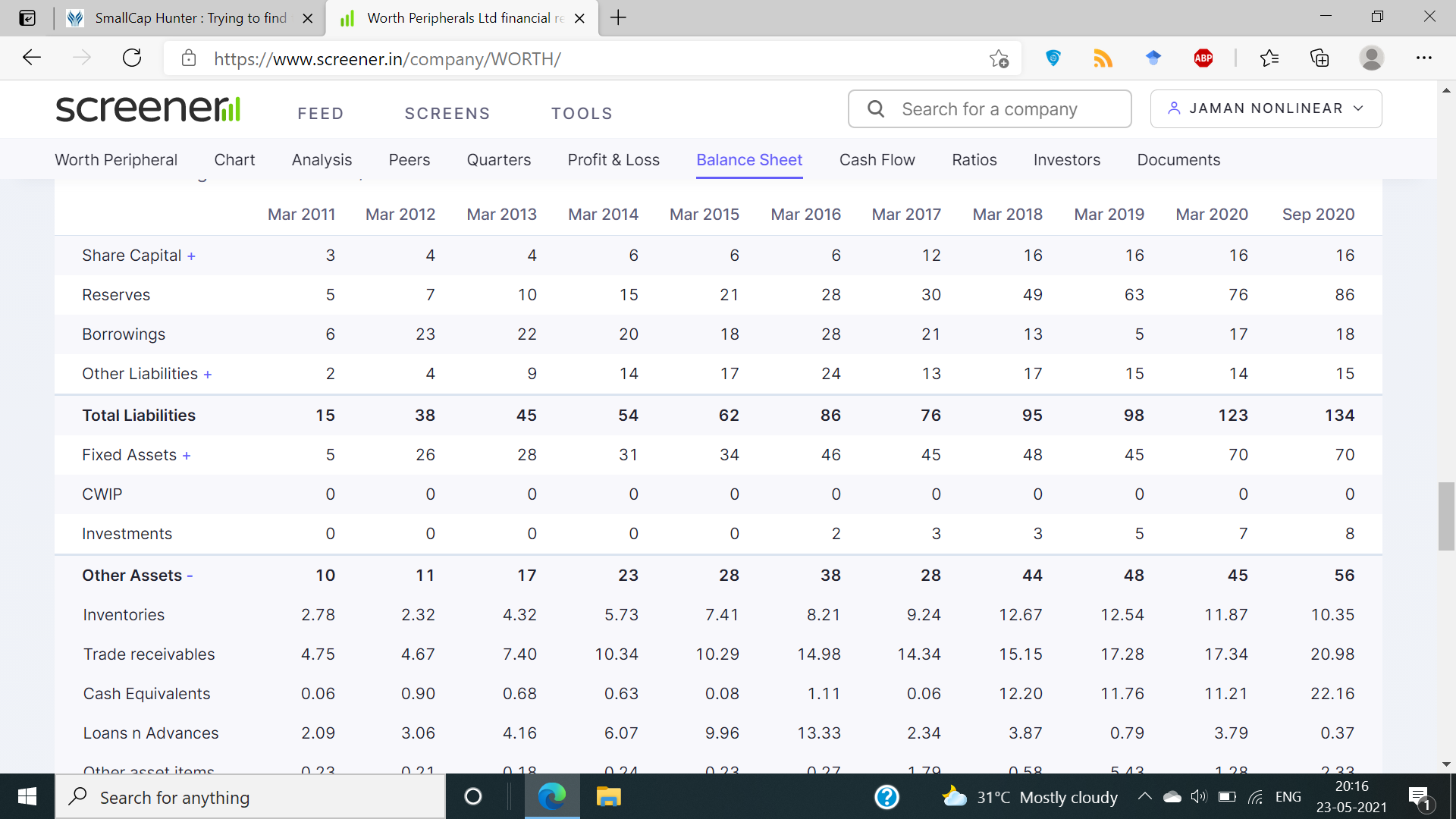

They seem to have around 35 lakhs in cash as on 31 march 2020 and around 24.18 crores in debt. Does anyone know how much of this debt was accrued on the recent expansion>?

Disc. Sold 99% holdings, Still have a tracking position

Any views from anyone on Creative Peripherals? They have started with b2b marketplace last year and it looks like scalable business similar to indiamart

They seem to be dealing with the best of the brands and are able to scale up but my concern is wafer thin margins with decreasing trend…Any reason why so low margins

Came across this company - Ginni filaments. Two things seem to be working in favor of the company - Debt reduction and margin expansion. Sales growth is a concern. Does anyone have more information about this company?

Worth Peripherals

In response to my mail to the CS of the company, I received the following.

The company passes on the adverse changes in the raw material prices to the customers and the expected timeline for the same is said to be about 1.5 months

Their entire sale is covered by weekly orders from customers and they are trying to get more customers into their fold

They expect to invest around 50 crores in their new plant (Boxes) and are expecting an initial production of around 1500 tons. I have further asked them how they wish to fund the same i.e accruals or debt

“We believe we stand out from the competition primarily due to our R&D, Quality, Services, Long-standing relationships with our customers and suppliers, technical knowhow, company-owned vehicles for on-time delivery of boxes, and our capabilities in terms of multicolor high graphic printing in a completely automated line leading to savings to customers and increased strength” was their reply when i asked them about how they differentiated themselves from not being a pure commodity play.

I have asked them a few more questions about their foray into diaper making, Margins, and so on. I have also asked them how they are planning to de-risk their supplier / client portfolio which is very concentrated as per their DHRP. Will update this thread as it goes.

I think the company is trying to leverage what it knows and does the best on a much higher scale, I still have no clarity on what their diaper fiasco is all about. As far as I understand multicolor high graphic printing is just printing boxes with images or something of that sort. Also, I don’t know how an expertise in that will be beneficial to the company, Seniors pls share your thoughts.

Hold a tracking position

Pls delete if it does not add value

Thank you for sharing this. Has been in public discourse earlier. Have you come across or done a later analysis? I would like to post a deep dive into IST if anyone is interested…

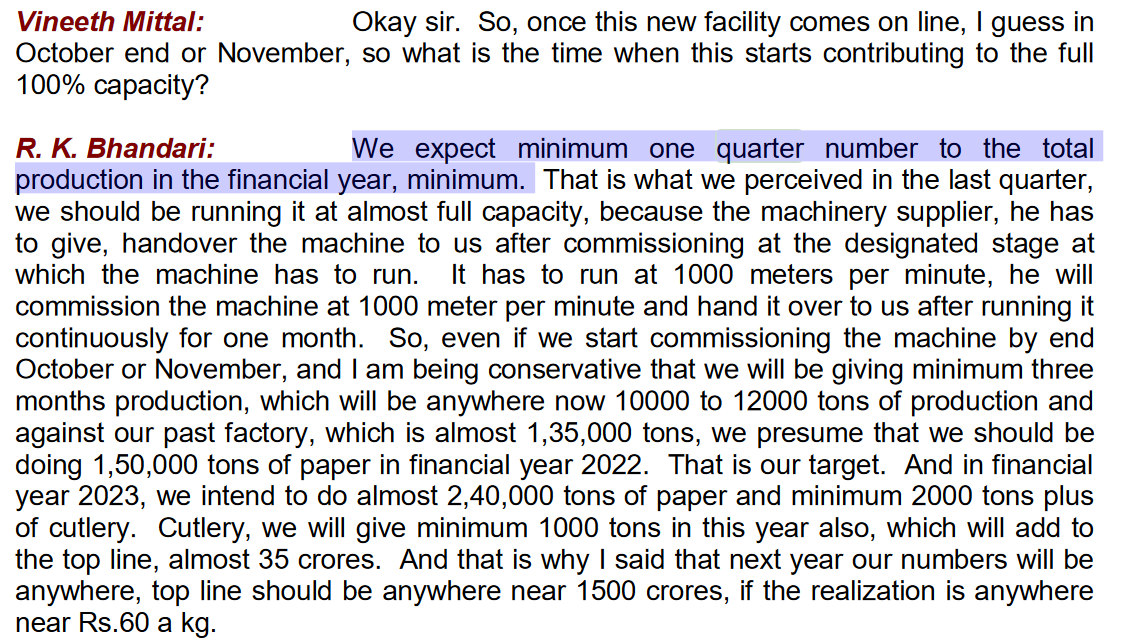

Production capacity will be 2x soon. In the latest conf. call the MD said that FY22 will have at least one quarter with 2x capacity coming online [1] [2]

Margins are lower in creative peripherals because of lack of Pricing power historically. But management has provided guidance for better margins going forward due to economies of scale. They have started international operations with distribution of Honeywell products. Margins will also increase with induction of more customers on ckart due to reduction of traditional selling costs.

Previously creative was only in distribution business whereas now it’s in three businesses… I.e distribution, contract manufacturing for Honeywell ane Ckart which is b2b market place like India mart and jdmart.

Another interesting development is that the company changed it’s name recently from creative peripherals and distribution to Creative Newtech limited to reflect the fact that it’s not solely in distribution business anymore

If anyone tracking Sterling Tools – I am trying to assess the potency of the following triggers but not able to find good information sources:

Trigger 1: JV with Jiangsu Gtake Electric Company Limited. The two companies agreed to join hands to provide the Indian Electric Vehicle OEM’s with best in class MCUs. MCUs are a very core component of EVs.

Trigger 2: addition of Hyundai to its new customer list that will lead to incremental revenues from FY22.

Trigger 3: Bangalore facility capex leading to additional capacity.

Please DM if you’d like to collaborate on this research.

In Advait case, Sales has gone up but the operating profit has remained more or less the same in the last two years. And, operating margin has gone down. I think this should also be considered.