It’s answered above by @kalpesh4430

Also their shareholding hasn’t changed much over time.

Disc.: invested

It’s answered above by @kalpesh4430

Also their shareholding hasn’t changed much over time.

Disc.: invested

Hi Sandesh

Which one is the Financial Magazine? Can I subscribe to this magazine.

warm regards

Navneet Agarwal

No, Think it is because the company has a limit on how much info it can divulge. Then Got busy with my job…Hence could not afford the time to follow up, I have reduced my position to a much much lower level. Once I follow it back, Shall let you know if I have something of value

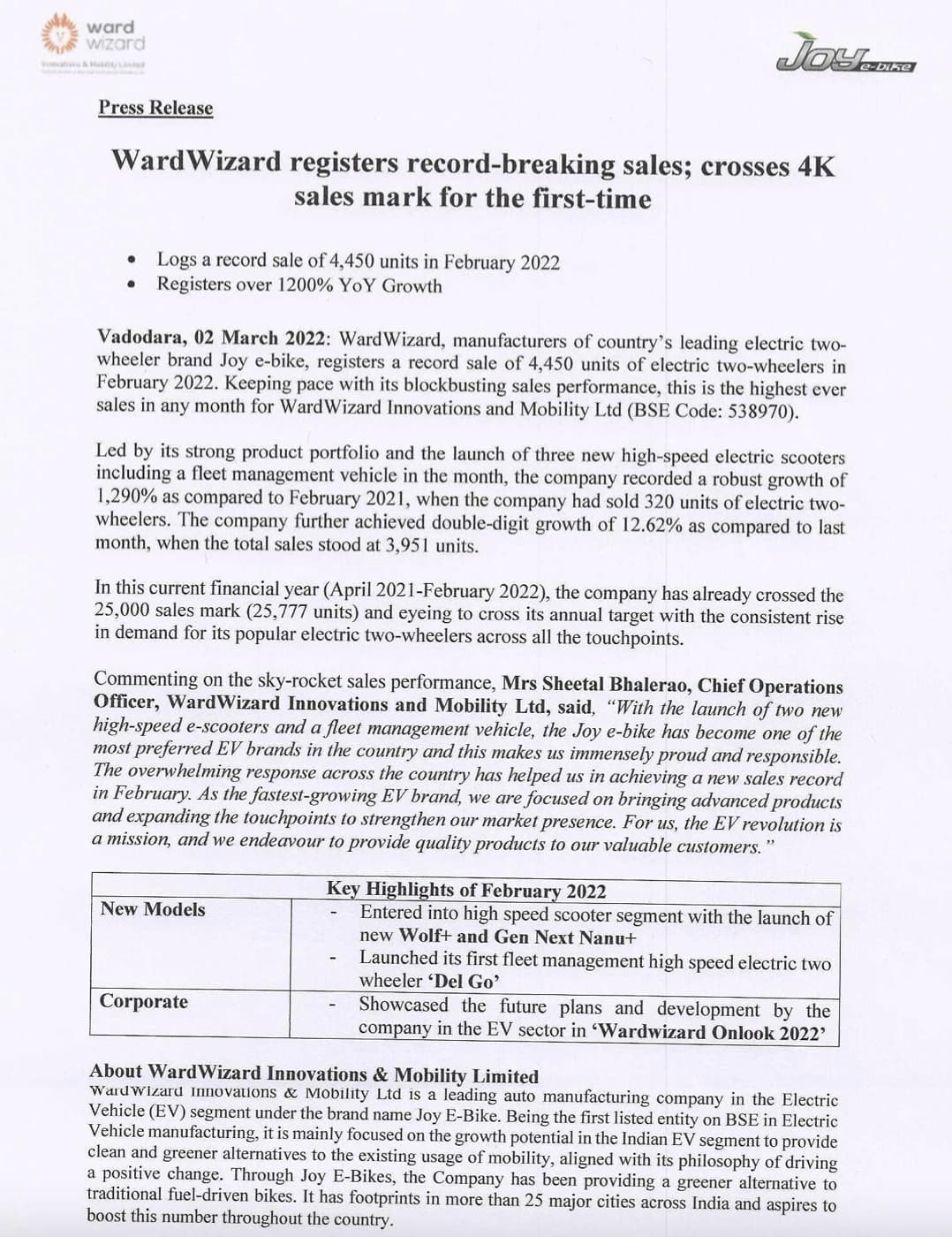

WardWizard Consistently delivering superior sales growth in their Electronic 2 Wheeler segment, worth tracking it

I regularly read all the online magazine from Moneylife.

My recent findings

KITEX GARMENT LIMITED

About the Company

Established in 1992, Kitex Garments Ltd (KGL) is into exports of cotton and organic cotton garments especially infants wear located in Kizhakkambalam, Kerala.

World 2nd largest infants wear manufacturer

Per day production 4.5 Lakhs units with 4600 employees in payroll

Kitex also supplies to Jockey International. Most of their sales are export to US market.

Recorded highest turnover of 730 crore in March 2020.

Touched Market capitalisation of 5000 crore in 2015

Company enjoys EBITA margin of around 20% in past several years.

Infant wear is a specialised product.

Figures (based on 18/01/2022)

Market capitalization 1732 crore

Debt-free company

P/E – 22

Future Plan (Based on MD comment, report, MOU, Director’s discussion)

Kitex have a CAPEX plan of 2406 Crore and on the political issue, they have decided to move out from Kerala (Not an investor-friendly state) and invest in Telangana State(Number 1 state for ease of doing business in India).

MOU with Telangana Government has signed by the company for Capex plan of 2406 Crore. Kitex will be investing in 2 textile parks in Telangana state.

• Kakatiya Mega Textile Park, Warangal – 1113 Crore

• Sitarampur – 1293 Crore

Kitex has formed a subsidiary company in Telangana called Kitex Apparel Parks

On completion of the above to project company expects target sales of 4,000 crores. (Current sales of the company is 700 crore). Which is 4 to 5 time upside growth

Kitex will become world largest kids wear manufacturer. Current production is 4.5 Lakh units per day (largest player is from china having 5.5 Lakh units’ capacity per day).

Kitex capacity will become 18 Lakh units post expansion of above mentioned 2 units.

Capex has already stated in Kakatiya Mega Textile Park, Warangal project and expected to commission from December 2022. Project in Sitarampur will kick start from December 2023. So expecting full capacity from the company in 2024 onwards.

Telangana state is 3rd largest cotton manufacturing state in the country. So kitex can easily get these cotton which is the principal raw material for the company.

Offer from Telangana

The government will give an interest subsidy of 8%. So, the company can run the business with 1% or less interest for 5 to 10 years.

Income tax exemption

PF/ESI Exemption

Income Tax 8% Saving u/s 115 and 1% save 80JJA

Easy procurement of cotton from the state because Telangana is the 3rd largest cotton producer in the country.

Cheap labor, water, land cost etc.

Top of that Company will benefit from Central Government PLI scheme of 10,000 Crore.

MD says over 6 to 7 years company is going to get 70 to 80% return from the government in the form of various subsidies.

Management

The success of every business lies in the hands of its management.

No wealth will be made if operator is not capable enough. In other words, a good management can make wealth even if they run bad business.

Kitex group has made nationally recognized brands over last 2 decades that too from not an investor friendly state in India. Their major brands Chakson pressure cooker, Sara’s curry powder (Sister concern of kitex run by MD’s brother) and kitex infant wear.

Many companies failed to manufacture When NASA needs some special dress which will adjust based on climate change including Aravind mill and later the same has manufactured by kitex group for jockey who supply said items to NASA in USA.

My bet on Kitex (Why I invested)

Proven management

• 3 well-recognized brands created by the group.

• Run the textile business for the last 2 decades with above industry average EBITA margin.

• Moving out from Kerala to the best investor-friendly state.

• Infant wear manufacturing is not easy to start so many are not involved.

Business perspective

• Expansion is 4 to 5 times more of the existing plant (Expecting to hit 18 lakh units per day against current capacity of 4.5 Lakh units).

• Incentives from the Telangana government. (Tax exemption under income tax and interest subsidy of 6 to 7% which will result in 75% of investment of 2500 crore over a period of time).

Some calculation corners

My entry was when share was trading at 170/-

Share price - 170

Share Capital – 7 Crore Shares

Market capitalization (170*7=1190 Crore).

P/E – 15/-

IN 2016 Company’s market cap touched 5,000 crores with a turnover of 700 crore. Management says 2022 will have the highest turnover in the company)

On future (perspective)

When they complete plants in Telangana top-line touch 4000 crore

Keeping same profit margin – 10% = PAT = 400 Crore against current year 100 crore PAT)

Multiplying with current P/E = 400+100 = 50015 = 7500 crore market cap

If market is crazy about valuation in 2016 when p/e was 40 then valuation will be 50040 = 20,000 crore.

So share price may hit = 20,000/7 = 2875/- (Oh my god). Forget even if it touches 1000 great return (fingers are crossed. Time will tell).

Assume when they get 8% tax exemption and 8% interest subsidiary the profit can double or triple. No, I don’t want that calculation.

Summary “Heads I win; Tails I don’t lose much” borrowed from Mohnish Pabrai whose thoughts have influenced me a lot

Concern

Management runs a non-listed sister concern of similar business

No idea about company funding plan for new CAPEX of 2400 crore.

The market is all-time high and any correction can have an impact of all shares irrespective of the performance of the company

Highly labour and CAPEX intensive industry. Scaling up with such huge labor can be a concern

All figures are based on comments from management. Need to wait and see how demands pick up

Highly dependant on 3 to 4 suppliers.

Vietnam and Bangladesh are more competing companies in the sector when china plus move starts.

These return will be expecting 4 to 5-year time frame.

My entry was at 170 range and now share trade at 265 Range (30/01/2022) Seems bit priced based on current earnings.

My view can change and I will exit based on future developments so keep it as only a discussion for education purposes.

Will it be possible for you to share the entire data of stocks which can be extracted from screener in excel format with all columns, that would be really helpful to everyone.

The corporate governance is a major issue in this company.

Can you elaborate… If you ask me in 2017 they had focused to promote a political party called 20-20. In fact, that was a huge success in the panchayat election. they had swept all 4 panchayath elections like what AAP does in Delhi. Seems they had a plan to enter state polities and contexted in the 2020 election but failed all the candidates… Recent, interview of MD seems they started politics to help people and if the verdict of the general public is against us then we accept. Now, he is behind the Telangana project which 4 times higher than the current business of Kitex.

Has any one done any work on shah alloy, came up with 80+cr PAT last year. However, has been marred by debt in the past and in 2017 did one time settlement with lenders, Are things turned around for good or still some issues pending or is it just the commodity cycle that they are benefitting from?

Management losing focus on business is big no no for me!

Kitex MD is more interested in fighting the ruling communist pary and congress. To show kerala government is not investers friendly he went to thelugana. Everyday he is in news fighting the left.

Last one year he comes up with some aligations against all political parties so no party is supporting him. His main interest is politics now.

True post Legislative assembly election seems he is focused more on the new project. seems share also went from 80 to 270 range

Can any company sustain a PE of 350? I would be very uncomfortable unless a PE expansion happens quickly. I understand the PE earlier had been even higher, but these levels too make me uncomfortable to enter.

Corporate governance should be first filter rather than last imho.

Rating of Tinna Rubber upgraded by ICRA

CMS infosystem…

New listed stock.

Small cap ~4000 cr market cap.

Zero debt

Increasing revenue n profit

Cash rich

IT company with cash management service

24% share of ATM

Clientage like axis, hdfc bank, ICICI bank.

Hidden gem with high growth potential.

High promoter holding.

Disclosure: invested.

Ward wizard continues to deliver.

Crosses 5K monthly sales mark for the first time and logs a record sale of 30,761 units in FY’22. Company is new in e-bike segment and i am not sure on their bike quality either. Does any body track it?

Actually I started the thread for Wardwizard - Wardwizard Innovations & Mobility Ltd – Joy e-bikes

But I unable to gather much information about the business, and also I think its too risky, as I doubt promoter integrity.

But I still closely track the Joy e-bikes, though quality is not as par with peers, I think it is doing well, because of the huge tailwinds in the sectors, as far as deliveries of bikes are concerned, they just started to deliver on time, last quarter there was at least 1 months delay for deliveries, which now seems to be gone.

ATM is already a sunset industry; high growth potential here is dobtful.

It looks more like an Infrastructure company, capital-intensive business.