Transcript of 17th AGM proceedings. Lot of info on company and its future growth.

2 Likes

Some notes from August’22 ICRA report:

- Acquired Exotech Plastics for chrome plating business.

- It derives around 41% of its revenues from the 2W segment, 30% from PVs and the remaining from the white goods and farm equipment segments.

- The vendor switch-over cost for OEMs in SJSEL’s product segment remains low.

- Tier -1 OEMs: TVS, Bajaj, Honda motorcycles. Further, it serves reputed brands such as Whirlpool, Samsung, and Electrolux, among others, in the white goods segments. With the acquisition of EPPL, SJSEL also added four-wheeler (4W) brands such as Mahindra & Mahindra and John Deere India to its customer base.

- Operating margins to remain stable in the near term ~26%

- Top 3 products contributed to 69% of revenue. This share will go down with Exotech business and company diversifying to new products.

- The company is planning to set up a new plant for its chrome plating business at a total

cost of ~Rs. 100.0 crore. Of the total capex, the company is expected to incur ~Rs. 40.0 crore in FY2023, funded by internal accrual and cash reserves

4 Likes

Is their any entry barrier to competitors or switching cost involved for OEM??

There is no switching cost. The whole thing is based on past relationships. Their relationship with most of their clients is 9-10 years old. There is no barriers to entry but the marker is small…So it doesn’t make sense for big players to enter.

1 Like

The barrier to entry in a sense is that there are thousands of SKUs and the market is limited enough for too many players to come in and deal with that kind of complexity. There is no real incentive for an OEM to switch suppliers, so long as theybare being serviced well and the relationship is strong.

4 Likes

Contract longevity

No, so it is awarded per model so let say there is a new model that a customer launches and there is a life-time of that order so let say that model go to run for six years or seven years we are nominated as a supplier so there are categories of products like dials for example which run like that. If you talk of decal so fundamentally these are the items that are refreshed every year at an average so the color change the shape of the decal changes but the model that is awarded to you normally continues unless a supplier does not perform upto the expectation of the OEM.

There may not be a barrier to entry however that wouldn’t mean a lot of people want to enter that business. Switching Costs are always there, for an OEM finding a new and reliable partner is not that easy, plus they can’t be sure if the New Vendor will deliver the products on time and maintain the desired quality. "There has to be a serious error in the quality of the products delivered or the financial status of the vendor has gone bad/worsening " or if a similar product is available at a significantly lower cost and same quality. only then the OEM will switch. These things don’t happen so often. Taking SJS case in point, there are no such eventualities.

3 Likes

1 qoq big earnings growth will absorb all the sellers. Company has sectorial tail wind. All it needs is some good sequential growth which is missing.

Disclosure: Invested

1 Like

To be honest, all of us have invested in the narrative of growth and operating leverage. We haven’t seen the growth play out yet. And with an upcoming global recession / slow down, who knows how demand for SJS auto and consumer durable aesthetics will pan out.

Lets hope there is some growth soon and we get some more margin of safety. On present metrics and economic outlook, the stock is not cheap.

Disclosure: Small 2.5% position at about 410. Will scale up once numbers start matching narrative.

8 Likes

As demand is shaping up & recession is probably already been discounted, this interview will clear the air little bit

1 Like

I don’t see any exchange announcement related to Dividend for this company. Is there any restriction to announce Dividend post listing(1 or 2 year) or They have not declared any Dividend for FY22 performance yet?

Even Screener data also misleading. In header, it was displaying 0% Dividend. But in Profit & Loss Statement, there is 21% of Dividend for FY22. Did anyone received Dividend having some exposure to this counter?

Management seems to be still on track for 25% growth for FY23:

Disclosure: I am not having any position in this counter. I was interested to see 30% growth even during recession time that too from auto sector. It will be red flag for me if Dividend are not declared as per the performance of the company.

Happy Investing,

Karthik

2 Likes

Brokerage coverage on SJS

638107308329590119_SJS Enterprises Ltd - Initiating Coverage - SMIFS Institutional Research.pdf (1.7 MB)

2 Likes

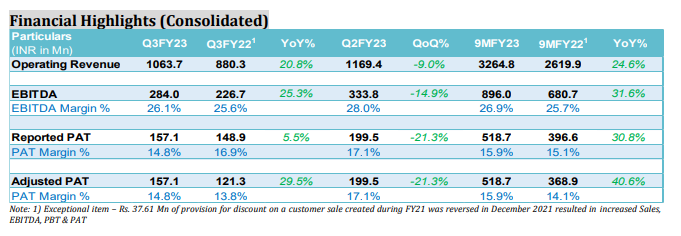

Q3FY23 (Consolidated)

• Outperformed Auto industry with 25.3% YoY growth in auto segment compared to 3.9%

YoY production volumes in 2W + PV segment

• Revenue at ₹ 1,063.7 Mn, robust growth of 20.8% YoY

• EBITDA grew 25.3% YoY to ₹ 284.0 Mn, Strong margin at 26.1%

• Adjusted Net Profit jumped 29.5% YoY to ₹ 157.1 Mn, with margins at 14.8%

• Strong Cash & cash equivalents position of ~Rs 1,431 Mn; Debt free company

• Added new customers – Foxconn in 2W EV segment and IFB Industries in Consumer

Appliances

• Continued growing business with mega accounts by winning new orders from M&M,

Tata Motors, Toyota, Whirlpool, Electrolux and Royal Enfield

• Added sales representative in Columbia, thereby covering key markets of Latin America

9MFY23 (Consolidated)

• Consistently maintaining ~25% growth, outpacing the industry

• Revenue at ₹3,264.8 Mn, robust growth of 24.6% YoY

• EBITDA at ₹ 896.0 Mn, a sturdy growth of 31.6% YoY, strong margin at 26.9%,

• Adjusted Net Profit rises to ₹518.7 Mn, strong jump of 40.6% YoY, with a margin of

15.9%

16 Likes

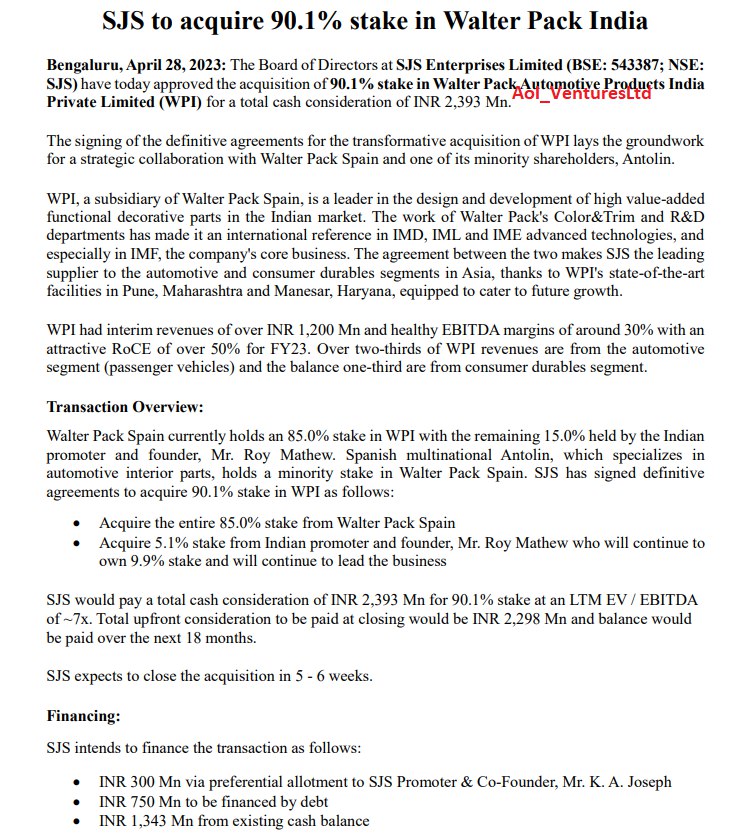

SJS to acquire 90.1% stake in Walter Pack India

First look - Seems like a good acquisition.

Acquired entity has margins of close to 30%.

Business is complementary to SJS existing products.

Acquired entity is stronger in PV and consumer durables where SJS was relatively weaker.

Valuations seem very reasonable at EV/EBITDA of ~7x.

Plant locations in Pune and Manesar.

Deal structuring - Looks good. 30cr preferential allotment to promoter.

2 Likes

Preferential issue of equity shares upto Rs 30 crs to Mr. K. A. Joseph, SJS Promoter & Co-Founder

It would be interesting to understand the price at which promoter is getting preferential shares. If it is fair market value or minor discount to FMV, stock can get rerated. If not, it would be treated as bad corp governance. Lets wait and watch

It seems promoter is confident about business performance. Price for preferential shares has been decided as 500/-

6 Likes

This is very BIG news as promoter is bringing in Rs 30 Crores at valuation of Rs 500 per share (premium to CMP) whereas price calculated as per SEBI guidelines is Rs 445. That shows his confidence in his company as well as a great corporate governance example.

3 Likes

operating leverage is yet to play, crude heading towards $50-60, M&A almost following Minda strategy which is applicable , huge marketing & warehousing spreading plan, export opportunity is huge, Management is top notch, as soon as economic situations eased Mobility will out perform,

2 Likes