It’s 30 crores.

6 Likes

my take on sjs

SJS ENTERPRISES

Business

- Operates in the high value-add aesthetics market across multiple consumer-oriented end industries.

- One of the leading players in the Indian decorative aesthetic industry, designs products according to the customer’s needs.

- Leading edge technologies and a wide product suite including decals, appliques/dials, overlays, logos/3D lux, aluminium badges, in-mould decoratives (IMD), optical plastics and lens mask covers for diverse applications

-

Top 5 customers contributed 63% and top 10 contributed 87% of the total revenues in 2022 (recent data is not provided by the company), although this is reducing with addition of the new clients of Walter Pack and Exotech.

-

All their clientele are blue chips and have been with the company for decades.

-

The Bangalore facility is fungible, allowing them to interchange product mix based on customer requirements.

-

The succession planning of the company is secure with the current managing director Mr. K.A. Joseph’s son Mr. Kevin K. Joseph being active in the business

-

SJS has never lost a single customer till date. This indicates some kind of switching costs with their products, also proves the quality and delivery of its products and trust of all its customers in them.

-

Bengaluru has additional land available for future capex.

-

As the volume of orders increases, customers demand higher discounts.

-

None of the peers are in all the aesthetic segments except SJS.

-

In Q1 FY23, Exotech won its first export contract with whirlpool.

-

The company is trying to get HERO on board as a customer.

-

One of the key benefits is that the products are light and easy to ship. This brings down the freight cost as a percentage of sales.

-

Open to inorganic acquisitions, but very selective.

-

Very interactive products and services, have a whole floor where they do creative work and trials in front of customers and make it as customised as possible.

-

On a standalone basis SJS has had the lowest margins since the last 7 quarters, this was due to lower 2 wheeler sales, lower export sales and wage rate hike by approximately 2%.

-

The products supplied by Walter are in a near monopoly situation, with them having close to 100% market share.

-

The technologies acquired by SJS through the Walter acquisition compared to the current SJS and Exotech technologies.

Financials

- The margins of the company on a standalone basis have been consistent over the years at greater than 25%, indicating some kind of pricing power which prevented the margins crashing in downcycles.

Management

- The management is very experienced and are technocrats.

- The company is run by a professional management, with the promoter guiding and directioning the team.

Guidance

- SJS expects over 50% YoY revenue growth on account of expected positive outlook for 2W, PV and Consumer Durables, , while ebitda and pat growth will be a bit lower at around 40% for FY24. As they plan to balance high growth with margins.

Premiumisation + New Customer Wins + Exports + WPI Acquisition = Higher than industry sales growth for SJS

- SJS has a very high visibility of the with the current order book being over 85% for the FY24 forecasted revenue.

- Organic growth expected at ~20-25% CAGR, with best-in-class margins

- SJS will continue to outperform the industry despite the continuing macroeconomic headwinds in export markets and gradual recovery in domestic 2W market

Entry barriers

- In this industry, the companies need to maintain a large number of SKU’s as clients prefer to choose from a larger collection with many options, SJS has 6000+ SKU’s.

- SJS has Long standing relationships with customers, due to this a newly developed product can be quickly taken into the market and can reach scale comparatively faster than the firm which has recently entered the industry.

Risks

- Client concentration risk, a significant part of their revenues is derived from the top 10 clients.

- As the company deals in aesthetic products and not necessary or critical products, there is a huge risk of changes in trends and tastes of different customers. Right now the company is doing good but maybe tomorrow the trends change and maybe SJS will not be able to adapt or develop these products.

- Heavily dependent on two wheeler sales growth as majority of customers are two wheeler oem’s (although this will reduce as Walter Pack serves the four wheeler industry).

- PE firm Evergraph holds 34.83% of the total equity of SJS. Any change in their long term commitment is a risk.

- Highly competitive industry, with some products being commoditized. Although this isn’t impacting SJS as they seem to be able to maintain their margins even in downcycles.

- No long term contracts with any of their suppliers, this may lead to raw material availability and price volatility in future.

Triggers

- The acquisition of Exotech helped the company gain not only its products, technologies, management team but also its customers. This will provide SJS with various cross-selling opportunities, by selling SJS’s product to Exotech customers and also vice versa.

- Exports is a higher margin business. Currently the exports are in low double digits (less than 20% when reported last), the management wants to focus and grow the exports business. It’s already increasing Q-o-Q except this quarter as there were some demand issues.

- The capacity utilisation at Exotech is close to 100%, but for SJS and Walter Pack is at close to 60-65%. Thus as the utilisation increases the operating leverage will kick in and increase margins.

- Expanding chrome plating capacity to meet higher demand pipeline.

Double the chrome plating capacity to support revenues of Rs 300 crores from the current Rs 130 crores capacity.

Higher capacity will also enable entry into global markets.

- The company is focusing on new product development.

- Chrome plating market in India is currently greater than 1000 crores, Exotech is currently at only 140 crores.

- SJS also serves consumer durable durable manufacturers. As we are currently seeing the real estate demand increasing, also now with the interest rates expected to cut down due to the inflationary period ending. The demand for real estate is expected to increase further thus increasing demand for the consumer durables, in turn benefitting SJS.

- Shift towards premium, more aesthetically pleasing and more technologically superior products, like optical plastics (touch screens) and chrome plated parts. Shift towards higher costing products (analogue to digital speedometer).

- The Walter Pack acquisition will help in diversifying the end industry revenue split as it majorly serves the passenger vehicle segment. It will also provide various cross selling opportunities.

- The Walter Pack acquisition will lead to margin expansion for SJS on a consolidated basis, as EBITDA margins of Walter are at 30% (significantly higher than SJS). Although one thing to note is that just this year the margins touched 30%, previously they were below 20%. Walter also has a ROCE of 50%.

- Speedy integration of Walter into SJS as the SJS management decided to retain the founder of Walter to help with faster integration and better results.

13 Likes

Answering based on my work experience in Indian OEMS.

Decals are low value products when compared to the overall BOM Cost of the final vehicle. There are models where the only change done is on decals and are released in market as an all new model variant. So basically the number of new Decal part numbers developed at any point of time is comparatively higher than any other part family. So obviously no. of production part numbers to be managed and NPD Part numbers to be managed are very high in case of decals. Lead time usually given for development is also low , somewhat 4-8 weeks. So it doesn’t make sense to go for Chinese suppliers because of following reasons

1)Decimal cost weightage

2)Short lead time

3)Avoid import/duty/logistics cost. As OEMs prefer suppliers nearby to their plant

4)Huge number of part numbers to be managed and any communication gap/understanding problem will lead to loss of production delivery

Not having exposure to TFTs. So no idea.

4 Likes

SJS definitely looks like a promising stock with strong financials, unmatched number of SKUs and very strong client relationships. One thing I am failing to understand here is what exactly is the reasons why SJS is able to earn this much margins in a field that is easy to enter and has a lot of private and unorganized players as well, leading to high competition among the players.

The number of new tech products that do command high margins are still a small part of the topline and I am not sure if strong client relations help on the margin front. Possibly, the years of experience could have led to operational efficiencies but am not able to verify given the limited info the stock has (recently listed only with no listed peers). Anyone who can throw some light on it?

1 Like

There are two possible reason for these global companies to source 3D domes from India.

These are global companies with Strategic sourcing unit in India which are solely aimed at Localisation of parts to India as a part of Cost reduction and derisking. SJS seems to be a minor beneficiary of this strategy along with other Vendors. 3D domes are costlier than decals (By a factor of minimum 2-3 times per unit of surface area and lesser number of variants (part numbers) for a model. For eg. Imagine the number decals used in a bike vs 3d dome used. 3D domes are used for brand symbols, over steering and for safety symbols. And mostly these domes are commonized across models. It only makes sense economically if these parts are imported in higher volumes and with lesser variants (More volume per part numbers leads to lesser complications for customers and better operation leverage for vendors since their machines don’t suffer downtime due to setting time of machines for different part numbers).

My answer involves speculation so please consider with a pinch of salt.

6 Likes

Good results from SJS. sales and profit growth QoQ as well as YoY

https://www.bseindia.com/xml-data/corpfiling/AttachLive/657b9482-5c28-4a48-bbc9-7fc735664054.pdf

Only one spoiler - Management remuneration gone up from 11% to 15% of the net profit. Market is clearly not enthused by this and punishing the stock price in spite of good results.

1 Like

YoY Revenue and PAT growth is <15% and management keep guiding for 25% growth. And management goes for higher remuneration. Doesn’t seem walking the talk at all.

Disc: Invested

2 Likes

Walter Pack acquisition is not part of this qtr results. It will come from next qtr. Adding that would change things. Check Walter’s last year nos and you can see the change,

3 Likes

This is typical problem with PE owned businesses. They have ‘Exit’ mindset, rather than a Ownership. It is a ‘Risk’ we need evaluate while owning these bizes.

Thanks.

3 Likes

Sanjay Thapar is the key person, if he exit early then the co may be in trouble as it’s into niche level of transformation & private equity’s will definitely buy lower than mkt price that’s not the issue , also looking into India’s prospect more block deal is going happen in small caps

2 Likes

1 Like

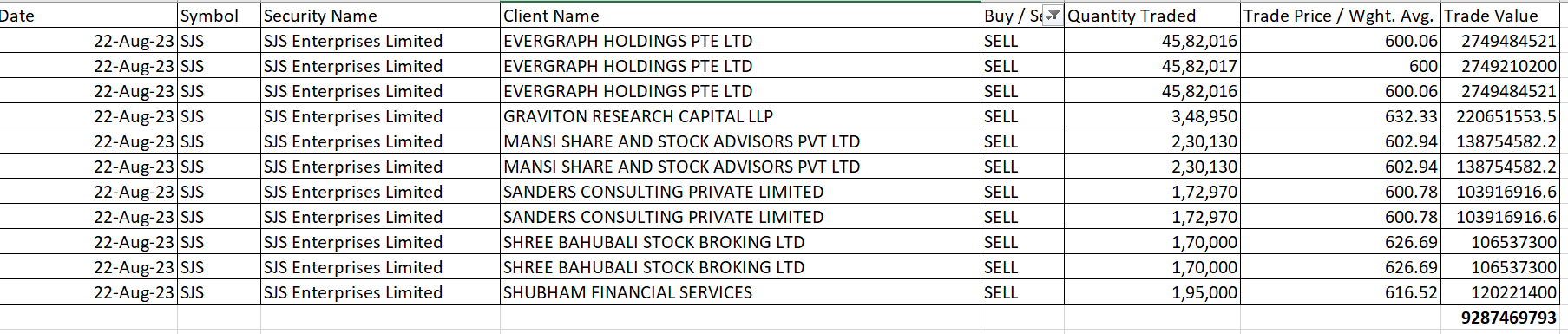

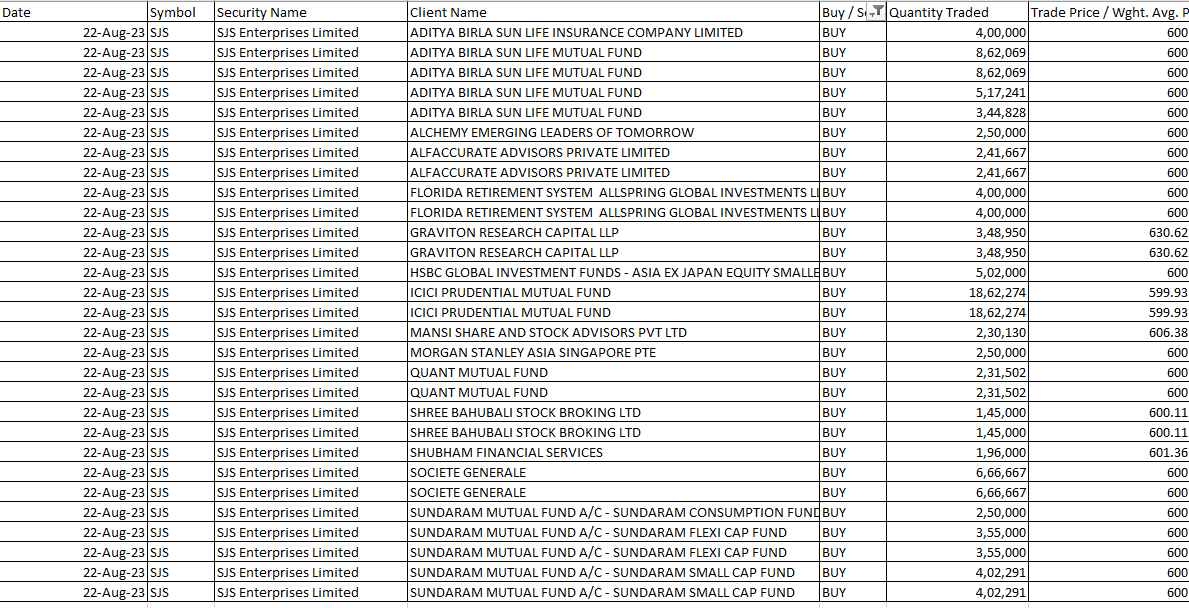

Curios to know who is the buyer and the open offer price if 26% has been acquired by single buyer as per SEBI SAST Regulations.

Post this block deal, promoters will be left out with 21.8%. Any chance of hostile takeover by any big group?

Also would appreciate the view of fellow VP members, CNBC TV 18 has reported on August 11 that block deal will happen in SJS very soon (Watch from 1:45 )

https://twitter.com/i/status/1689936636812091392

Is this a price sensitive information which company has to disclose to stock exchanges. Company has also neither denied or accepted this statement of CNBC TV-18. How come such large block deals are getting leaked to media before it comes to public. Is there any CG issue over here?

1 Like

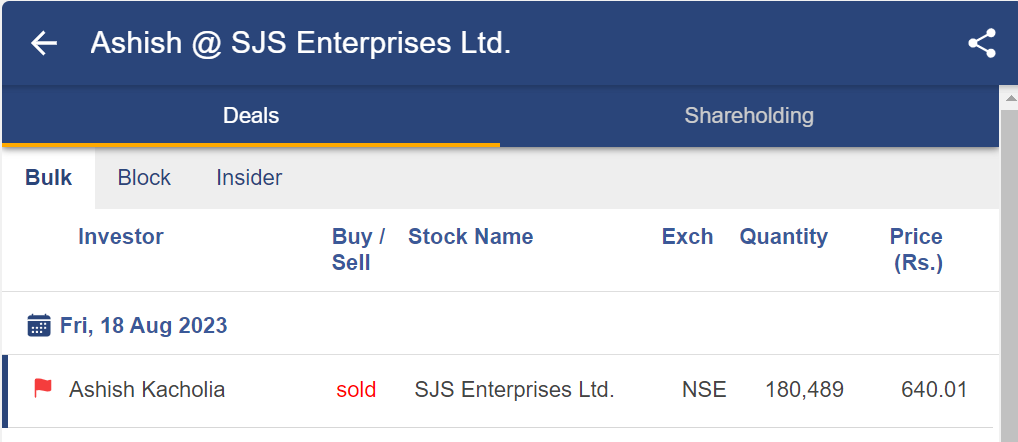

All time high trade volume and value. 824 worth of shares sold by Evergraph

Good to see majority of MF absorbed all sellers

Exciting times ahead for SJS.

3 Likes

Just a question here, is the dilution by promoter to many fund houses will weaken the promoter structure?

Absence of a stronger promoter and mis-aligned interest of too many fund houses will only create chaos…

1 Like

I think this is a negative on SJS. Promoter selling as also Mr Ashish Kacholia. I would not give much to institution interest as they are more investors than promoters who run the core.

Safir Anand

1 Like

Brother, where can we find this everyday data.

Can you please guide ?

**Invested in SJS

yes, and this acts as a switching costs for oems, there is no substantial savings for them in changing suppliers.

hence unless there is inferiority in quality of product, suppliers aren’t changed.

high customer stickiness

1 Like

Look for promoters who are managing the actual business. Here, the stake is sold by Evergraph Holdings which is a PE Fund. PE Fund by virtue invests at bad/turnaround/very high growth phases and exits a decent chunk at their good times. Here, Evergraph has invested pre-IPO and took an exit in IPO and post-IPO.

KA Joseph, Sanjay Thapar, and its team are intact with their interest in the business. It’s just a change in the shareholding of those who were sitting for returns and not for long-run business. I think nothing material has changed in the business.

Regards,

Invested as a techno-funda bet.

7 Likes

I have been following SJS only recently but generally, mgmt seems to be over promising and under-delivering so far. They guided for 20-25% organic growth in F23 and missed it (blaming weak exports) and have once again guided for 20-25% organic growth in F24 (delivered 10% growth in H1 F24) while maintaining it despite weak H1.

Commentary continues to be strong though and WPI numbers should start improving from Dec-23 quarter. Based on my numbers, company can deliver peak revenue of 1000 Cr (assuming Exotech’s capacity expansion to 300 Cr topline goes through in C24) over the next 3 years with potential PAT of 145-150 Cr. Will have to wait and see.

3 Likes