Business

-

SJS Enterprises Limited is one of the leading players in the Indian decorative aesthetics industry in terms of revenue in Fiscal 2020 and as at March 31, 2021, offered the widest range of aesthetics products in India, It is a “design-to-delivery” aesthetics solutions provider with the ability to design, develop and manufacture a diverse product portfolio for a wide range of customers primarily in the automotive and consumer appliance industries. The Company supplied over 115 million parts with more than 6,000 SKUs in Fiscal 2021 to around 170 customers in approximately 90 cities across 20 countries. it differentiates itself on the basis of the wide range of its product portfolio, quality of its product offerings, product design and development capabilities and the strength of its relationships with customers located across various industries globally.

-

SJS also manufacture a wide range of aesthetics products that cater to the requirements of the commercial vehicles, medical devices, farm equipment and sanitary ware industries. Its product offerings include decals and body graphics, 2D appliques and dials, 3D appliques and dials, 3D lux badges, domes, overlays, aluminium badges, “In-mould” label or decoration parts (“IML/IMD(s)”), lens mask assembly and chrome-plated, printed and painted injection moulded plastic parts. It also offers a variety of accessories for the two-wheelers’ and passenger vehicles’ aftermarket under its “Transform” brand.

-

Key customer base

-

original equipment manufacturers (“OEMs”) such as Suzuki, Mahindra & Mahindra, John Deere, Volkswagen, Ashok Leyland, Honda Motorcycle, Bajaj Auto, Royal Enfield and TVS Motors;

-

Tier-1 automotive component suppliers such as Marelli, Visteon, Brembo and Mindarika;

-

Consumer durables/appliances manufacturers such as Whirlpool, Panasonic, Samsung, Eureka Forbes, Godrej and Liebherr;

-

Medical devices manufacturers such as Sensa Core; and

-

Sanitary ware manufacturers such as Geberit.

-

-

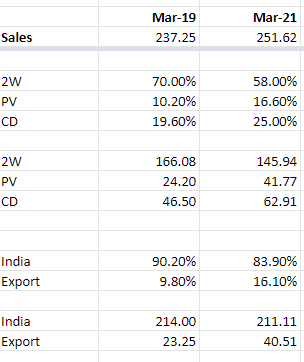

75% revenues comes from automotive and 25% from consumer durables in FY21.

-

As at June 30, 2021, SJS had a team of 44 personnel for NPD, representing approximately 8.64% of its total on-roll manpower as at that date. This included a dedicated design and development team of six personnel, which primarily works on the design, development and prototypes of new products and certain product upgrades.

-

Principal raw materials used in manufacturing SJS aesthetic products are plastics, aluminium, plastic polymers such as PVC, inks, chemicals and adhesives. Raw material costs formed ~38.4% of revenues from operations in FY21. Raw material costs are higher for Exotech (~54.5% in FY21) with key raw materials being polymer granules, chemicals, paints, copper, nickel, tapes and packing materials. The company procured ~33.7% of raw materials from outside India in FY21.

-

IPO: Company did IPO in November 2021, issue size was Rs. 800 cr at Rs. 542 per share. Entire issue was Offer for Sale and post issue promoter holding has come down from 98.9% to 50.4%.

Manufacturing facilities

-

Company has 2 state of the art facilities at Bangalore and Pune. Both plants are IATF and ISO certified.

-

Bangalore plant is LEED gold certified which is leadership in energy, efficiency, and design by the US Green Building Council. They generate almost 2 MW of solar power at Bangalore facility and more importantly this Bangalore facility is fungible allowing them to interchange capacity and product mix based on changing customer requirements and optimizing machine productivity and operational efficiency.

-

As at June 30, 2021, the annual production capacity of the Bengaluru and Pune facilities was 209.70 million and 29.50 million products, respectively.

-

manufacturing facilities located in Bengaluru and Pune in India spread across an area of approximately 235,000 and 68,350 square feet, respectively.

Acquisition of Exotech

-

In April 2021, SJS acquired Exotech Plastics Private Limited and Exotech will be a 100% subsidiary of SJSPL. The total amount of investment for acquisition was around Rs. 64.00 crore and the same was done through internal accruals. With this acquisition, SJSPL diversified into chrome plating business and acquiring new customers as well. Exotech had a revenue of Rs. 74.3 crore and PAT of Rs. 4.1 crore in FY2020.

-

Exotech Acquisition has enhanced its product portfolio, increased its manufacturing capabilities and increased its customer base. While chrome-plated parts constituted the second largest product segment within the overall aesthetics market in India in Fiscal 2021, it is expected to be the largest product segment within the overall aesthetics market in India in Fiscal 2026.

-

The demand for chrome plated parts comprised 23.00% to 25.00% of the total demand in India for decorative aesthetics in Fiscal 2021, which is expected to increase to 26.00% to 28.00% of the total demand in India for decorative aesthetics by Fiscal 2026.

-

SJS expects to leverage its existing capabilities, product offerings and customer base to capitalize on this market opportunity. It has started offering products that use chrome-plated, printed and painted injection moulded plastic parts, such as wheel covers, radiator grills and door handles, following the acquisition of its Subsidiary.

-

there has been a margin enhancement in Exotech post acquisition. Exotech business was operating at 10.5% margin. Now it’s in the range of 14% driven by revenue plus operational efficiencies that SJS have brought in the material management and the synergies that their procurements with SJS capabilities and from the process discipline that has been introduced in Exotech.

Management

-

K.A. Joseph, its Managing Director and one of its Promoters, has been instrumental in the establishment and growth of the business. He has been associated with the Company for the last 34 years. Leads the manufacturing operations for the Company and has spearheaded technological and product innovation over the years

-

Sanjay Thapar is the Executive Director and CEO. He has over 30 years of experience in the auto industry. Previously he was Group Chief Strategy Officer with Ashok Minda Group; MD of Minda Valeo Security Systems.

Financials & Valuations

-

At cmp Rs. 360 company has mcap of Rs. 1080 cr and Enterprise Value of Rs. 1000 cr.

-

Company’s consolidated numbers for Q3FY22

Sales: Rs. 92 cr

EBITDA: Rs. 26 cr (28% margin)

PAT: Rs. 14.90 cr

EPS: 4.85 (quarterly) -

Based on recent numbers company is available at decent valuations

EV/Sales: 2.71

EV/EBITDA: 10

Price to Earnings: 18.5 -

Company has consistently given high operating margins over the years. Consistent focus on increasing share of exports and increasing share of Consmer Durables and 4 wheelers in overall mix will help them in maintaining these margins and bring incremental growth. Company has better sales growth and margin profile than the competitors.

-

Company did big capex in FY19. Full effect of this is yet to be seen as company is operating at low capacity utilisation.

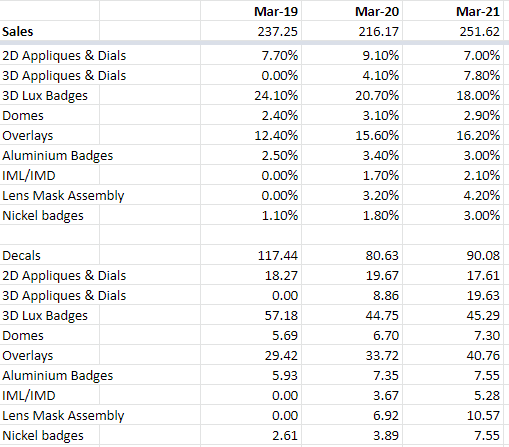

SJS Product Wise Sale

Strength/Opportunities

-

High Industry growth rate. It is estimated by CRISIL that in 2019, the size of the aesthetic market in North America and Europe was $2.7 bn plus another Rs.19.9 bn in India and growing at a CAGR of 20% and likely to do so for the next five to six years. The Indian market then by itself would be close to about Rs 5000 Crores by the year 2026. This 20% growth in aesthetic market is one and half times the growth of the underlying industries like two wheelers, passenger vehicles and consumer durables estimated to grow at 10 to 12% during the same period.

-

Large scale and High Volumes. What makes SJS unique and very tough for competitors is the fact that they manufacture 11 different types of products, catering to more than 7 end customer segments, have over 6000 SKUs in their portfolio. Annually produce 115 mn parts that they ship to 160 customer location in 20 countries.

-

Continuous focus on new product development. Company has dedicated New Product Development team. In last four years company has developed five completely new products, have in house design, development, engineering capabilities. They collaborate with customers to design their products as per their needs and today have a best in class new product development infrastructure. Recently acquired a chrome plating business. Chrome plating is Rs 1000 Crores business in India and this expands their total market quite massively.

-

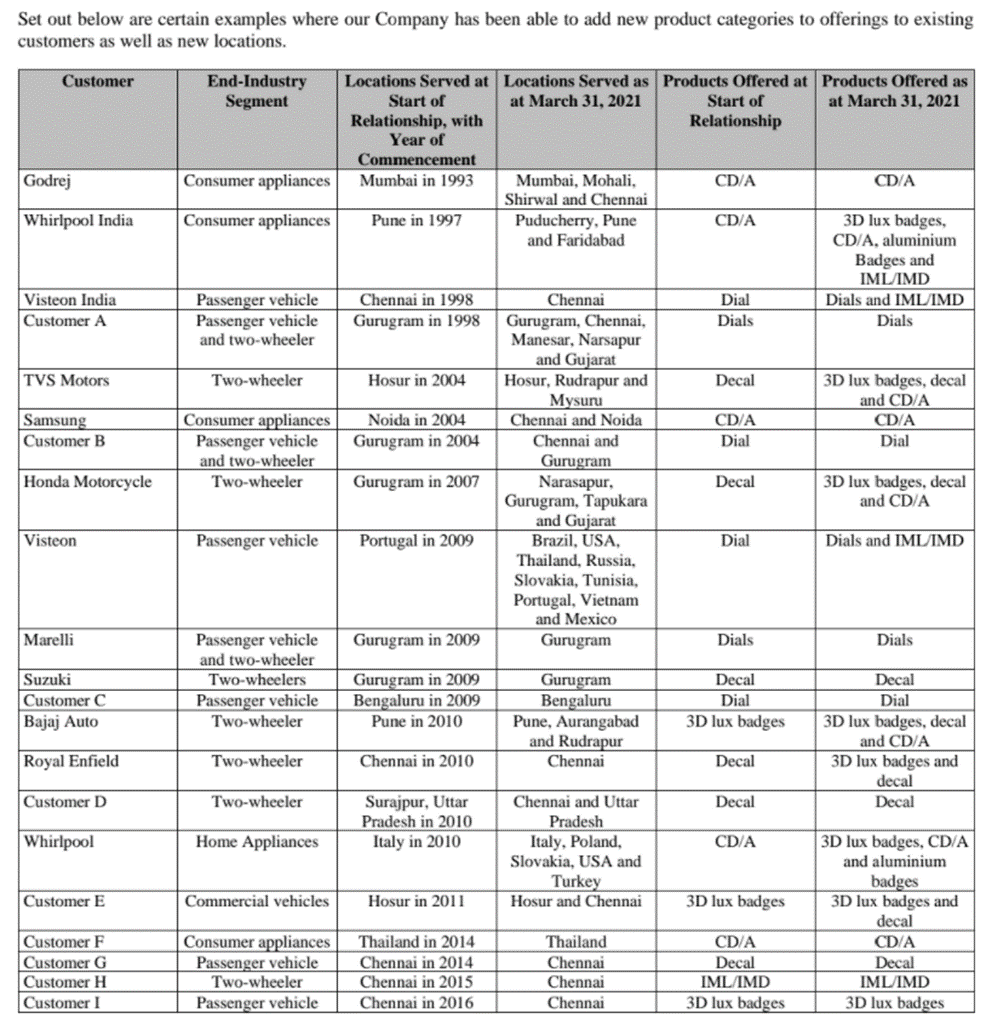

Longstanding relationship with customers. So average relationship with the top 10 customers that they have is close to 15 years. This longstanding relationship provides them with an opportunity to cross sell products. Any new product that they develop can very quickly take it to market with our customers and we have not lost a single customer as on date. It has demonstrated the ability to grow, adapt and integrate its products in response to its customers’ needs. The Company’s robust account management processes resulted in an increase in the number of customers with whom it had over Rs.100.00 million in yearly annual sales from five in Fiscal 2016 to eight in the three-month period ended June 30, 2021 and, as a result, deepening their relationship with the Company and it becoming an integral part of their supply chain.

-

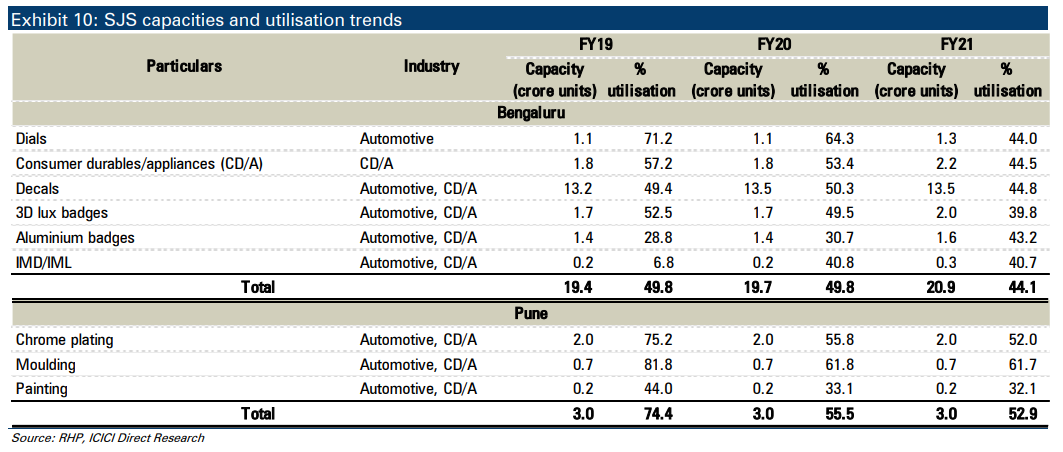

Low capacity utilisation offers an opportunity to pursue growth with minimum capex. Capacity utilization rates were of 44.07% in Bangalore and 52.88% in Pune, in Fiscal 2021, and its revenue from operations during Fiscal 2021 were Rs. 2,516.16 million and Rs.685.26 million, respectively. Also, its Bengaluru facility has additional land to undertake further expansion, if required, to capitalize on the growth of the industry.

Risk

-

75% of SJS sales in FY21 came from Automotive customers. Growth rate of auto industry will directly impact SJS. Low auto growth in past was the reason for their low organic growth from 2018 to 2021. Company has heavy 2W exposure with 58% of sales in FY21.

-

Client concentration: . The company’s client exposure is fairly concentrated, opening it up to the risk of significant impact on revenues in case of reduction in demand or loss of any key customer. Sales to the top customer formed ~21.5% of FY21 sales. Further, the company’s top five and top 10 customers accounted for ~62.7% and 87.3% of FY21 sales, respectively.

-

SJS does not have firm long term commitment agreements with all its customers.

-

Private Equity firm Evergraph Holding Pts Ltd. (part of Everstone) holds 34.83% and are promoters in the company since 2015. They have helped the company a lot in growing in past 6 years by bringing in professional management. Any change in their long term commitment to the company is a key monitorable.

Disclosure: Invested

Sources: