Few Questions with respect to business model

- Do OEM have only one vendor with respect to the model or there are multiple vendors?

- Are there are any lower priced substitute for chrome plating which is being considered?

- Any impact of China opening up?

Few Questions with respect to business model

most oems has 1 or 2 vendors.

chrome plating is premium product in trend. why would anyone want a cheap substitute.

No idea about china+ 1 theme. This is not a chemical company. so I don’t think it’s relevant.

Generally OEM have more than one vendor in order to remove the last minute fear of order fulfillment so it’s not any sign of worry even if they have more than one vendor for aesthetic components.

SJS comes across as an interesting company. The underlying sector of aesthetics is a growing sector . Today I read an IDBI cap initiating report on the company which provides some insights into the company and its key customers and triggers. Part of it ties up with what management articulates in its concall.

In a sector which is likely to grow at 20% CAGR for next few years, because of the theme of premiumisation in auto and consumer goods, SJS can aim to grow by atleast 25%. Of course there are a lot of assumptions here, but one has to take educated guesses and see on the ground how things are panning out.

Key customers of the company in auto OEM are Honda, Suzuki, M&M, VW, Bajaj Auto, TVS Motors, Royal Enfield, auto comp suppliers like Visteon, Marelli, consumer durables players like Whirlpool (a key customer in terms of exports too) Samsung, Eureka Forbes, Panasonic.

Exports growth can be a meaningful growth driver for SJS. Overall seems to be a company placed in a sector which is expected to show strong growth, along with tailwinds for the main customer segment, i.e auto sector.

On the charts, the stock price was stuck in a broad trading range of 350-450 and recently broke out of this range to post a high of 510 and now retesting upper end of trading range at around 450-460. If and when stock price crosses the hurdle of 500-510, strong move can be expected.

disc: invested as a techno funda bet.

The growth in last 5/3/1 years is 8% / 4% /6%.

looks like they don’t grow fast in absence of overall auto industry growth. A bet on sjs is essentially a bet on auto industry.

Another issue i faced in doing analysis of sjs was whh we think sjs would gain market share versus peers could not understand competitive positioning.

A bet on sjs is essentially a bet on auto industry.

Hmm, IMO it is more of a bet on the premiumisation trend in auto industry(the most direct way to play the trend as they are purely into aesthetics), which is less cyclical in nature. Also the industry seems to be turning up atleast based on surface short term no’s, so seeing it as a bet in auto might not be a negative.

The growth in last 5/3/1 years is 8% / 4% /6%.

Yes the past performance is a bit lacking and management seems to give aggressive guidance, but

Disc - don’t own, have also been following its chart for a techno bet.

Compare the consolidated revenue. They acquired exotech recently. It deals in chrome plating, which is replacing some old products of exotech. So the acquisition was a good decision. Revenue due to sale of those old products reduced which makes SJS standalone revenue to look like stagnant. What SJS did was they sold exotech products to their existing clients, thus gained wallet share. so for growth figures it’s better to compare consolidated figure.

They have 45% revenue from PV for which the up cycle is already visible. 45% is from 2W for which upcycle is yet to come. rest is consumer durables which gives optionality. Plus there is premiumization trend which is clearly visible due to which in spite of industry downturn sjs has grow over past few years.

They are the most efficient player in the industry. The whole industry size is 3000 cr.

plus there is long standing relationship with the OEMs.

So small market size+good relationship with the oems+ being the most efficient player gives some protection from exisiting competitors or new player who wants to enter.

Disclosure: Invested recently. Waiting for a break down or break out for allocating more.

Screener data will show poor growth because they show the CAGR numbers. But you have to take numbers in two lots. Those before 2018 and those after 2020. Auto industry went into a big slump from 2018-2020, and post Covid cycle seems to have turned, though its still marred by chip shortage.

In you look at numbers for 2016-17-18, sales were 153 cr-184 cr - 226 cr. Nearly 20 % CAGR. And OP was 42-59-74 cr. Again more than 20% CAGR.

Besides this, margins have been maintained at around 30%. They have not screwed the balance sheet. Dividend payout at 20-25% has been decent.

And the bet of course is on the auto industry growth aided by a strong trend of premiumisation. Look at all the hot selling cars. Most of them are in the 15-20 lacs bracket, most of them crossovers like Creta, Taigun, Kushaq, Seltos, Venue, etc. All these contains lots of premiumisation features and again a lot of them have loads of chrome plating. I tend to view the reviews of various cars on you tube and the first thing the presenter talks about is the chrome plating stuff and premium features. So I guess the theme of premiumisation is well and truly on and is going to stay. I think in previous years, the premiumisation theme was not so prominent. A car usually meant a car. No frills. Only a few cars provided premium features. Plus preference was for the budget cars. Nowadays, there is a huge preference for the higher end cars.

In my analysis the company ticks the boxes of management quality, business quality. Now need to see what kind of growth they can show. Million dollar question is can they walk the talk? If they do, at current juncture it seems attractive to me.

My strategy is to allocate a little lower than normal percentage now and then scale up if it crosses 500-510 in terms of price action. That will only happen if market participants feel company is on to something, or if numbers start coming through.

In the peer analysis provided in the IDBI initiating coverage report, only Galva Deco Parts has higher growth rate than SJS, but it is into losses. Data provided shows growth rate between 2014-2020 at 15%. Plus it has one of the best return ratios, and margin, and growth combinations in the comparative universe.

But the proof of the pudding will be in the eating. Hence now that we are seeing some sectoral tailwinds, esp in the PV segment with waiting periods stretching months in some instances, we need to see growth in next few quarters and how it pans out. Near term, I think the Exotech and export segment should help.

The chart is the most interesting part of the whole equation. We have here a double bottom at around 350 levels. (rounded off). Stock price went down from around 450 in Jan 22 and went down to post another bottom at 350. Subsequent rally took it well over 450 mark and since June 22, it has formed a daily flag sort of formation with flag pole extending from 377 to 498. Breakout point would be closing above 480-485 with volumes and if that flag breakout pattern is successful, target can be close to 600 .

Hitesh sir, on weekly chart this looks like forming a symmetrical triangle pattern and since it’s already above 30 WMA don’t you think it’s more like a break out candidate?

Technical seems to be very weak, chances are less , down side is possible , lets see

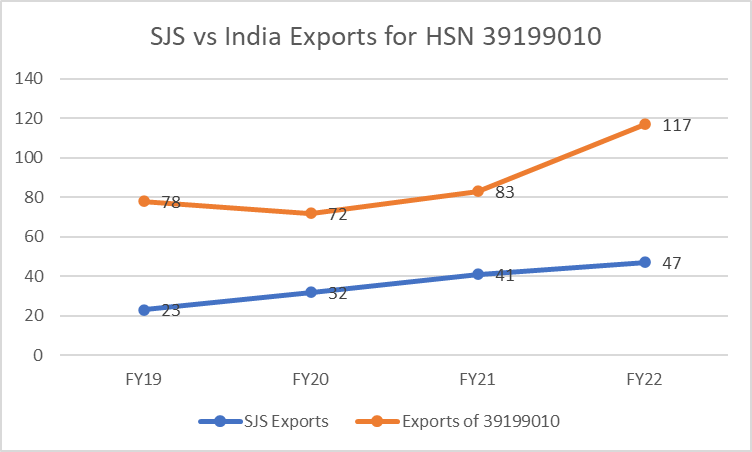

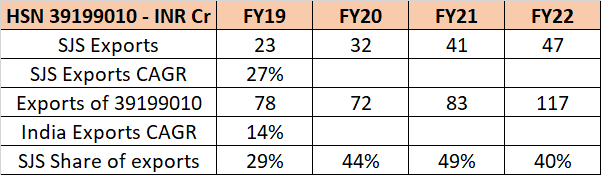

Some Google searching will reveal that the HSN code for a bulk of SJS’s exports is 39199010 ( PLASTIC STICKERS, WHETHER OR NOT PRINTED, EMBOSSED, OR IMPREGNATED)

Here’s a comparison of SJS’s annual exports (taken from DRHP & Investor presentation) vs India’s total exports for HSN 39199010

While India exports have grown at a CAGR of 14% since FY19, SJS has grown at almost double the rate. However, in FY22, the trend has reversed with SJS growing only at 15-17% where India exports has grown by a whopping 40% Y-o-Y. Escalation of exports by an existing player?

Since a large part of the outperformance thesis seems to be based on export growth, Management needs to be queried on this in the quarterly concall. Also, investors should ask them to start providing quarterly export figures.

Also, in the Q4 presentation, Management has explicitly mentioned that Exotech had no export contributions. Is that a matter of scaling up or is that indicative of @Chins concern around hexavalent Chromium? if the latter is true, then export growth will be led only by the standalone entity.

Countries like India and China continue to use hexavalent chromium, and I’ve not found a definitive answer on Exotech on the process it uses for producing the chrome plated parts. One hopes that it isn’t using hexavalent chromium, and that management has cracked the problems trivalent chromium brings with it, but I’d like to know more definitive details.

PS: Since I can’t be 100% sure about the HSN code, take this analysis with appropriate amounts of salt.

Agreed stock looks very decent trading at 25.0x FY22 P/E with outlook for 25% Sales and 30% EPS CAGR organically over the next 3 years and higher growth if there are inorganic acquisitions

Disclosure: Invested

Hi all, I have an update to the questions asked below:

Got a chance to interact with management. Have some insightful answers:

Exotech before our acquisition did not do exports. All plastics plating suppliers worldwide are currently using Hexavalent Chromium for the initial etching phase of the process due to the lack of fully proven alternate solutions. We will be targeting both existing clients and new deal wins.

Should trivalent chromium etching become a viable option in the future, we will be using it as and when it becomes so. In fact for the new plant for Exotech, which is under design stage, we are planning to have the option of hexavalent chrome free etching so that once this solution is proven, Exotech can offer this option to the customer as well.

Disclosure: invested, biased.

• Revenue at ₹ 1,032 Mn, growth of 39% YoY

• EBITDA grew 50% YoY to ₹ 278 Mn; Margin at 26.4%, expanded 170 bps YoY

• Net Profit jumps 71% YoY to ₹ 162 Mn, margins improved 280 bps to 15.4%

• Forayed into new country, Argentina and expanded footprint in North America (Ohio)

• Added new customers – Alladio, a Mabe Group company (leading manufacturer of consumer appliances in Latin America). Also added EV manufacturers - Benling India, Gravton Motors and Navbharat Edison Motor

• Won several key projects from Whirlpool, Mahindra & Mahindra, Bajaj Auto, TVS, Maruti Suzuki and Samsung among others

• Exotech won its first business in the exports market by cross selling chrome plated parts to Whirlpool

Looks like domestic revenue was good. But export revenue growth hasn’t happened. Export revenue is missing in presentation.

Detailed Blog on the company

https://soic.in/blog-description/SJS

My observations from all the concalls.

Revenue Concentration -

(So our largest customer does not constitute more than 20% of our sale on an average roughly that is the number, now top five customers across the group about 55% to 60% roughly.)

If they can bring down the revenue concentration in the coming years, it will give an investor more comfort.

Contract longevity

No, so it is awarded per model so let say there is a new model that a customer launches and there is a life-time of that order so let say that model go to run for six years or seven years we are nominated as a supplier so there are categories of products like dials for example which run like that. If you talk of decal so fundamentally these are the items that are refreshed every year at an average so the color change the shape of the decal changes but the model that is awarded to you normally continues unless a supplier does not perform upto the expectation of the OEM.

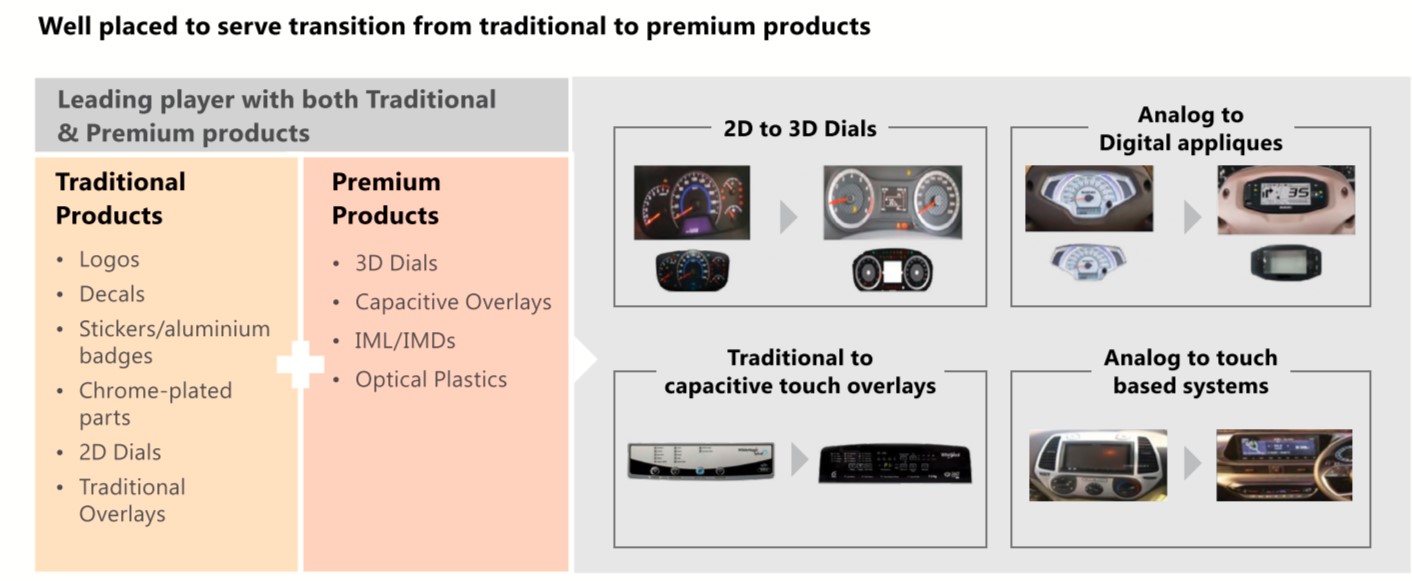

Premium Product revenue share

so in FY2019 it was about 3% of our sales and today premium products last there they were 16% of our sales, moving forward, especially in the Indian market and the export market we see that the premiumization trend will continue. Since the bet on SJS is largely on Premuimization, it’s imperative to track the contribution from this segment to the revenues.

Competitive Advantage

So as you see, as I mentioned in my earlier calls the people we compete with in export markets are manufacturers in Europe, North America. This is a batch mode operation business where it is very difficult for those guys to compete with us and we are further improving our competitive edge by constantly looking at ways to reduce cost and improve margins.

Basically they have a low cost of production advantage

Inventory Management

No, the OEMs maintain some stock, they ask us to maintain some stock in some cases where the OEM has a constraint, they would like to have just in time supplies, we do that also, but most of them is through stocks. So there is a little variation as I said and you rightly understood that one should look at a larger frame, so year-on-year is the better number to look at than to look at immediate quarterly inwarding because sometimes the OEM have some stock for a particular model which they do not want to lift the material at the moment so depending on the situation in the supply chain, so absolutely, to look at it quarterly may not give the right picture completely

New Product –

There are huge opportunities that exist in medical devices. We have already started the supplies to this sector. As you can understand the volumes are very large. We are also supplying to industrial applications and gaming applications, so anything that requires displays, anything that requires human-machine interface.

Order to Delivery timeline (lead time)

So, as I said to the previous question, our lead time, so we can actually deliver parts within two weeks, so dependents on the product category, so we have 11 product categories that we manufacture, so the lead time varies for each.

AR 2022 Notes

Premium Products

Total Employees – 1257

6000+ sku

175 customers

New Product Development We are building new capabilities to introduce in-mould electronics (IME) solutions, which allow integration of electronic chips and circuit boards within a plastic injection moulded part. This breakthrough technology finds increased application in two-wheelers, passenger vehicles, consumer appliances, and electric vehicles (EVs).

Capex & Growth Projections

we are firmly focused on building our chrome-plating capacity from the current level of 1,300 million revenue per year to generate almost 3,000 million of revenue at full capacity. This would entail a capex of approximately ` 1,000 million over a span of 18 to 24 months and generate an ROCE of 20% at full capacity. Higher capacity will also enable us to pursue exports and acquire new customers in India and abroad for chrome-plating business. We have appointed sales representatives in international markets including Turkey, Brazil, and Argentina, and intend to explore similar opportunities in other countries too.

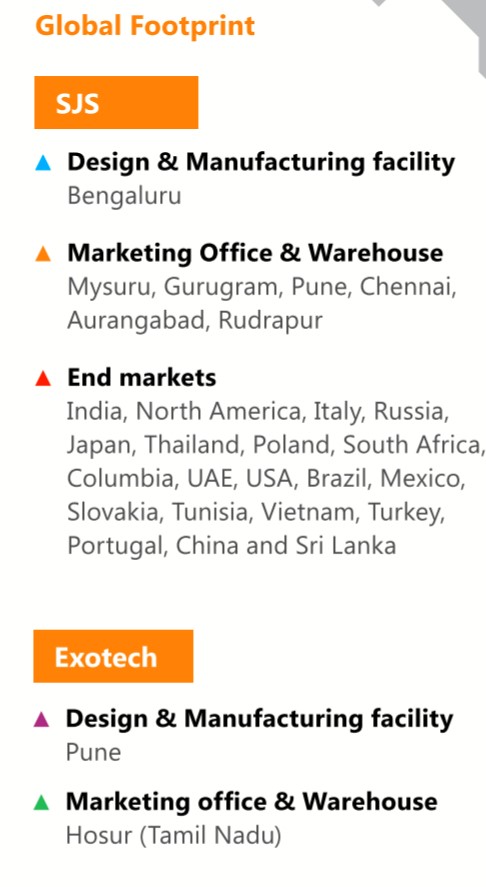

Plants

1000 million as cash & Bank Balance

Operation Highlights

Added marquee customers like Kia India, Ola Electric, Minda Industries, MG Motors, Stellantis, Ultraviolette Automotive

Won key business projects from Continental, Morris Garage, Honda & Hyundai, etc

Bagged prestigious order for HMSI’s maiden motorcycle entry in the huge 100cc bike segment

Developed Products for EV segment and started supplies to Ola Electric and TVS iQube

ESOP Policy

SJS has a unique ESOP policy, which was distributed to around 250+ employees in FY 2021-22, and will have a vesting period of 3-5 years to motivate employees

Statutory Auditors:

M /s. BSR & Co. LLP, Chartered Accountants

Subsidiary

Exotech Plastics Private Limited

Short Term Borrowing – 126 million

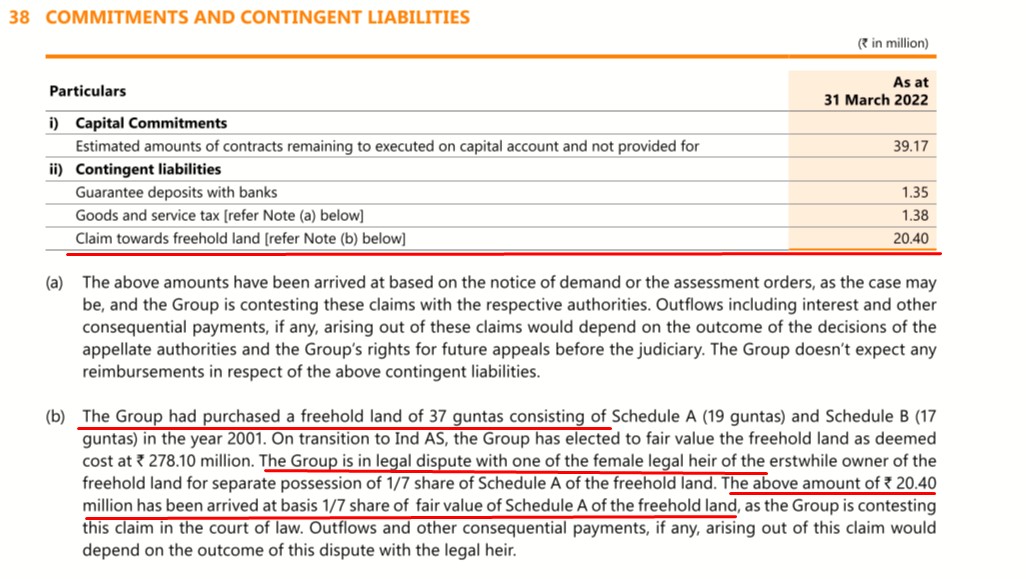

Dispute with respect to the land purchased recently – Im not sure if this the same land for capex plans, this needs to get sorted quickly

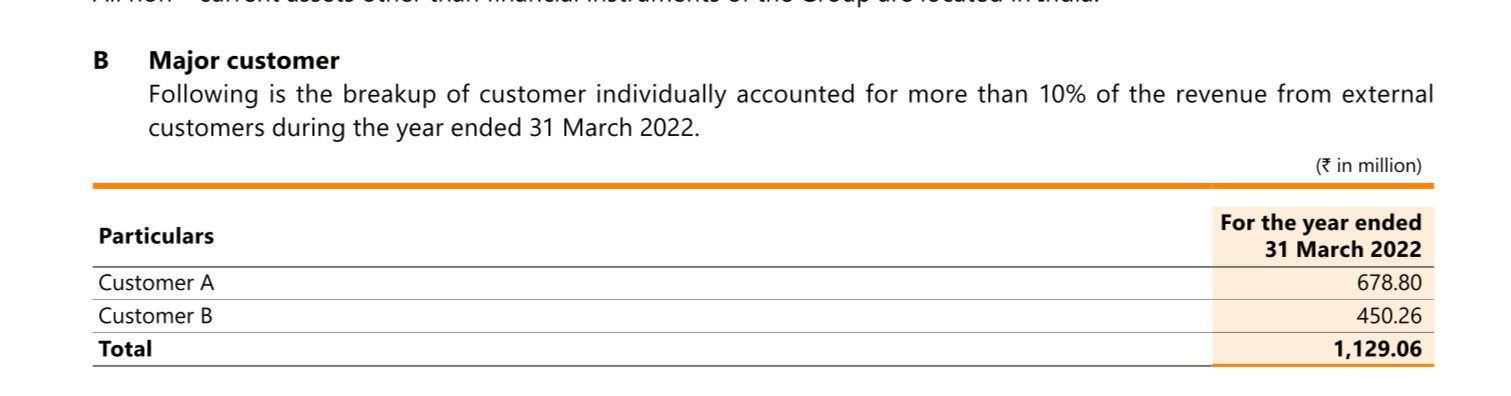

Revenue Concentration

Customer individually accounted for more than 10% of revenue

Customer A – 679

Customer B – 450

A total of roughly 30% of the revenue comes from two customers

Small Acquisition of 10 cr

Civil disputes are long drawn and subject to appeal in higher courts by the loosing parties. The land was purchased in 2001 and it is not known when the dispute was raised and at what stage the dispute is currently pending at the court ( at the lower court or at the appeal stage). Management should think of alternate site for Capex if they want to fast track the Capex plans.

they recently purchased land as mentioned in one of their concall, probably this land parcel maybe an old one. i will try and find out. probably send out an email to the management