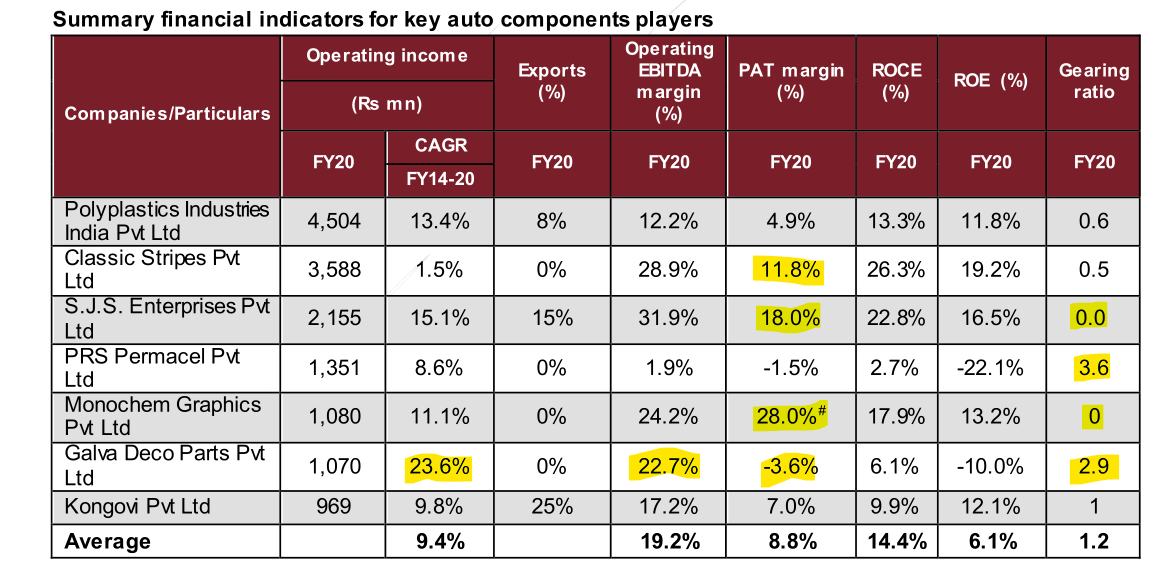

You can checkout Credit rating of Care and ICRA it has result upto 2016 Though it’s only rough Figure covering Sales,Margins,ROCE and credit rating ratios but it’s useful.

Some interesting facts about competitors. Looking at the table shared in the title post:

First thoughts:

- SJS, Classic Stripes and Monochem Graphics are the three most interesting players from this list.

- Polyplastics and PRS Permacel do not look very efficient.

- Galva Deco manages 22.7% EBITDA margins, but has negative PAT. Looking at the gearing ratio of 2.9, a reasonable assumption is that they are being wrecked by interest payments/depreciation. They have also grown the fastest since FY14.

- Monochem makes 24% EBITDA margins, but 28% PAT margins, which means they have other income, and no debt eating away at the cash.

Digging deeper:

Classic Stripes report from Icra: https://www.icra.in/Rationale/ShowRationaleReport?Id=110061

- They’ve invested 200 Cr. into group companies as of FY21, which represents 66% of FY20’s PAT as comparison.

- Is an exclusive supplier for Hero Moto. 70% of revenue comes from top client in two wheelers.

Kongovi report from Icra: https://www.icra.in/Rationale/ShowRationaleReport/?Id=110213

- Is the smallest company in the list, however the focus on exports has paid off, improving margins significantly.

Polyplastics report from Icra: https://www.icra.in/Rationale/ShowRationaleReport?Id=102199

17 Likes

In case of a shift from 2D/3D dials and appliques, automotive overlays to fuy digital screens that almost all EVs are equipped with - would the company be able to add any value?

Isn’t design work likely to be handed to others? SJS would be left solely with optical glass in that case?

1 Like

Design part can be assigned some USP but the decorative aesthetic parts over a period of time will have competition from 3D printing.

1 Like

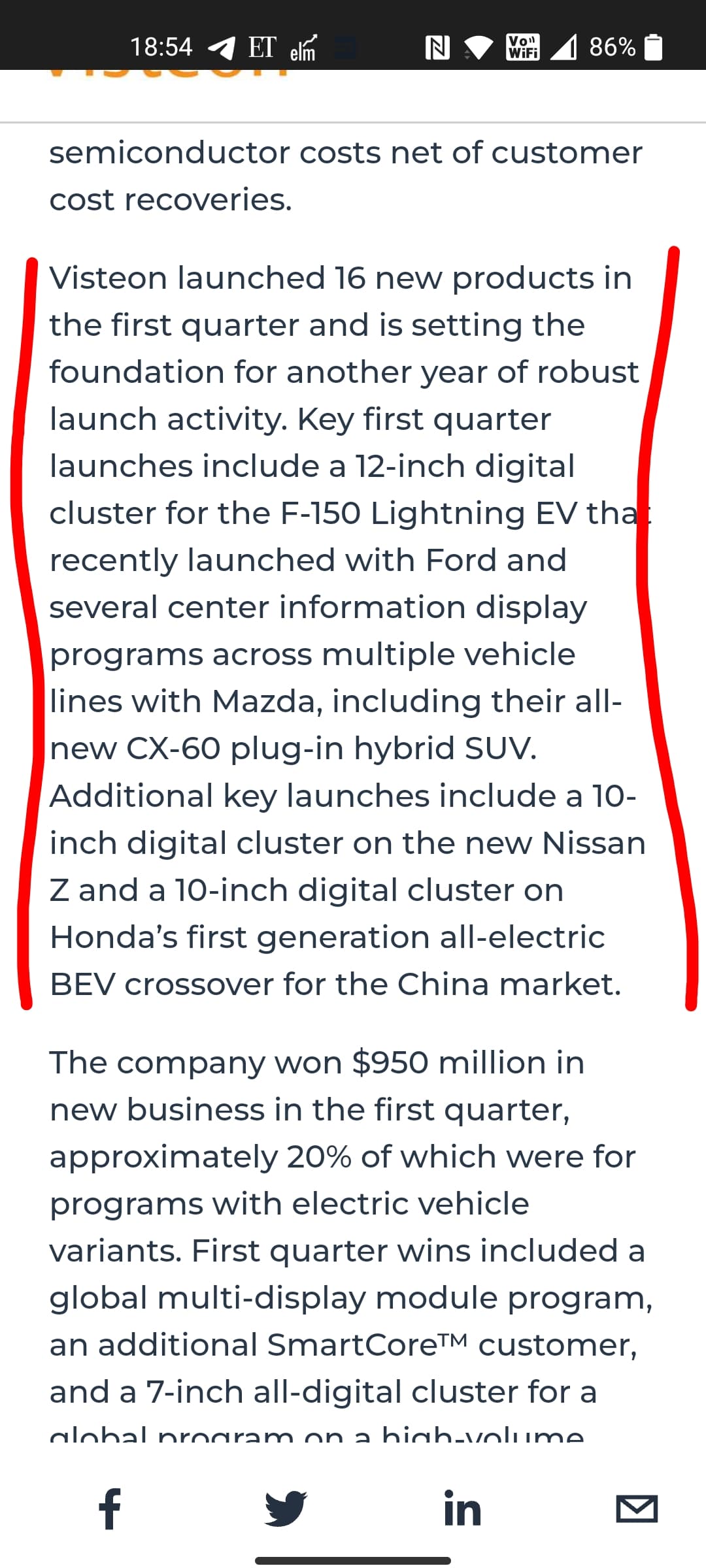

Visteon had reported great earning Visteon reported net sales of $818 million, representing a year-over-year increase of 11% excluding the impact of currency. Total industry production decreased 4% while vehicle production at Visteon’s top customers decreased 11%1 in the same period, reflecting supply chain constraints and the worldwide semiconductor shortage. Despite these constraints, the company’s sales performance represents 22%1 growth-over-market compared to the production volumes of its customers

Company is launching more products including digital cluster need to see if SJS is sole supplier of it then it’s huge boost if they don’t dilute their business due to Russia Ukraine issue.

7 Likes

My study on SJS

19 Likes

Good results in current environment

3 Likes

Snippet Press Release -

The Company’s revenue from Exports doubled from FY19 to FY22

to ~Rs 470 Mn. Contribution to revenues from new-age products has grown to 16% in FY22 from

<3% in FY19. Overall the Company is debt free and generating a strong free cash flow of Rs 500.3

Mn. SJS plans to grow at a CAGR of ~25% organically for FY23-25 period and inorganic growth

would boost the growth further up.

Management Commentry

“We are confident of achieving ~25% revenue CAGR over the next 3 years FY23-25 organically,

while maintaining our best-in-class margins. This organic growth would be on back of positive

outlook of automobile industry and our strategy of enhancing our chrome plating capacity,

increasing presence in exports market and developing new age products and technologies while

strengthening relations with existing customers and building mega accounts. Simultaneously

we would also like to explore more business accretive M&A opportunities that would help us

grow over and above the organic growth of 25%,” added Mr. Sanjay Thapar, Executive Director &

CEO, SJS Enterprises Limited.

4 Likes

8 Likes

After reading their investor presentation and press release, sharing few observations.Need fellow VPeers to provide their inputs

-

Management is bit overdoing in communicating future growth guidance. The press release- CEO commentary starts with the line confident of 25% growth…(it could be just my personal feedback)

-

The crisil doc indicated aesthetics industry to recover around 17% in fy22 whereas they had a flattish standalone rev growth (SJS only)

-

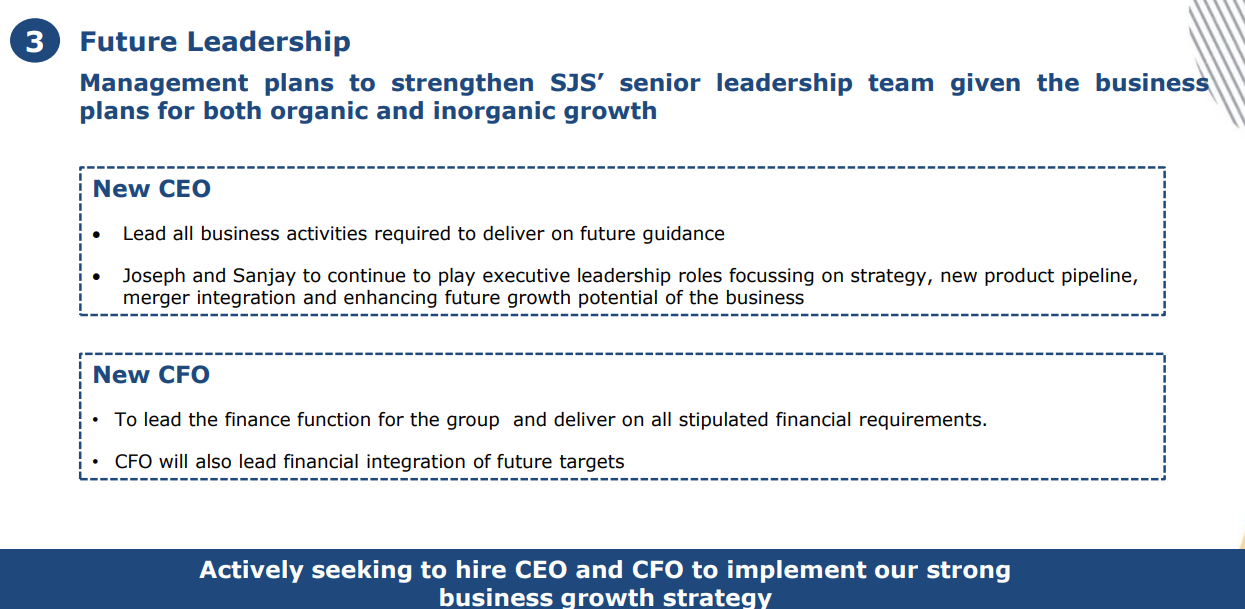

CFO name is missing from the presentation. Did they silently remove him? I know they mentioned ,they want to hire a new one but until then who is the current CFO?

D: Invested

8 Likes

About overdoing the communication on future growth, in corporate world, our bosses push us to make big fuss even about small things to get the visibility ![]() . Its natural that this sort of communication becomes a part of a culture. They probably anticipate that this may help the market cap. Is it bad, personally I think the results should speak for itself. But to a degree it helps retail investor who can not always get to hear from the management

. Its natural that this sort of communication becomes a part of a culture. They probably anticipate that this may help the market cap. Is it bad, personally I think the results should speak for itself. But to a degree it helps retail investor who can not always get to hear from the management

4 Likes

The way world is heading towards premiumisation & fast life style change the need for aesthetic product will rise for sure, but nature of the product is basically commodity based on crude so less margin & capacity to price pass on is less, But SJS seems to be different it has the capacity to pass on, even in down cycle it has maintained it’s margin, Management gimmick will be there as it’s a small cap, every one aspire to be big nothing wrong in it, as India’s culture & life style has changed & will change more in near future ppl will spend more on premium, which will make lot of small / midcap to large cap, Auto cycle is going through head wind but a huge demand is pending for auto in that case at least apart from export we can see a huge domestic demand spike that will sustain for a certain period , also closely monitor management walk on talk or not , expecting few more M&A as Technology changes very fast, not invested yet but tracking

4 Likes

Actually these technology shifts and premiumization is helping SJS

Exotech revenue increased from 68 cr to 102 cr with increase in profit msrgin. You should give that credit to sjs. Exotech revenue is not flat. It seems like exotech products are substituting their products bcz they acquired exotech to reduce risk of product substitution. Crisil document was published in June 2021. Lot of things changed after that. So industry recovery might not happened. Crisil also predicted increase in 2w sales but it didn’t happen.

One thing I agree is they should not boast about revenue increase without increasing profit or profit margin. Revenue can increase if you simply pass on the rm price rise.

Disclosure: Not invested. Studying presently.

6 Likes

Hi,

A couple of key questions on the corporate governance front?

- One of the executive directors on the board is Kevin Joseph, who happens to be K.A. Joseph’s son. What are his credentials? Is it a cause of concern?

- The CFO Amit Kumar Garg seems to have resigned.There has been no mention of this is any company communication, they merely communicated in Q4 investor presentation that they are looking for a new CFO. Shouldnt there be more transparency and clarity from the company on this?

Would appreciate insights on the above from anyone who may know.

Disclosure: Not invested.

4 Likes

Actually the horizon for aesthetic is big & getting bigger , Every electronic device that has a human interface requires aesthetic product, anything like Mobile, Consumer goods like TV,WM, Fridge, Chimney, Mixer, Iron, Power Bank, has a good amount of aesthetic product in it, every one wants their Car/CD more shinier than neighbor , So looks comes first, in that case this industry definitely has potential but it’s commodity in nature as based on Crude based product, How much SJS will reap benefit of China +1 that the main focus, still they have bigger domestic opportunity as GDP per capita will grow in India, life style shift is evident,

5 Likes

It’s not comodity. Not everyone one who sets up a plant can sell to the oems. It takes time to get order from the oems. on the other hand approved vendors can easily increase wallet share of the oems. plus longstanding relationship with the oems also matter. Plus the market is not huge. presently some 2000-3000 cr. so it’s not that everyone will try to start a new business. Then the balance sheet strength also matters. oems will simply not give order to someone who doesn’t have strong financials so that tommorow they are unable to supply. Their margins are steady even with rise in crude prices. that tells about their pricing power.

So I don’t think it’s a commodity play. The real competition they can face is from the existing players. but sjs is way ahead of them in terms of product portfolio, return ratios, debt, balance sheet strength etc

6 Likes

Hi, can you pl share the source. Shall help to understand better

Read the DRHP. Not the whole 300 page drhp, just the “industry and our business portion”. It’s about 50 pages. Take the growth guidance with a pinch of salt. You can also watch scientific investing video on sjs. link already posted above.

2 Likes

Insights by @suru27

7 Likes