Hi, dhaval

I have seen this disclosure what i am taking about is in concall they talk about 300 cr capital raising and who are this two firm which is taking participation in preference allotment?

Sigachi industries is going to issue 1,10,00,000 convertible warrants at 261₹ to promoter and non-promoters, effectively raising 287 cr

621ba522-71ce-4a0b-9073-449ef8672cd0.pdf (286.4 KB)

Sigachi is proposed to issue not exceeding 52,00,000 convertible warrants to the Promoters and

58,00,000 convertible warrants to the Non-promoters aggregating to 1,10,00,000 convertible

warrants at an issue price of Rs. 261/- each.

At discount to market price !!! this company has always been low on Corp Governance. In most cases it is done at mkt price.

1 Like

Sigachi industries fund utilisation program of 287.1cr

1)Sigachi industries is going to acquire API manufacturing facility by paying 160 cr.

2) Expansion of existing

Manufacturing facilities at Dahej and

Jhagadia by using 50 cr.

3) Expansion of existing

Manufacturing facility at Hyderabad by using 22.10 cr.

4) Working Capital requirements 30 cr.

5) General coperate purpose 25 cr.

1 Like

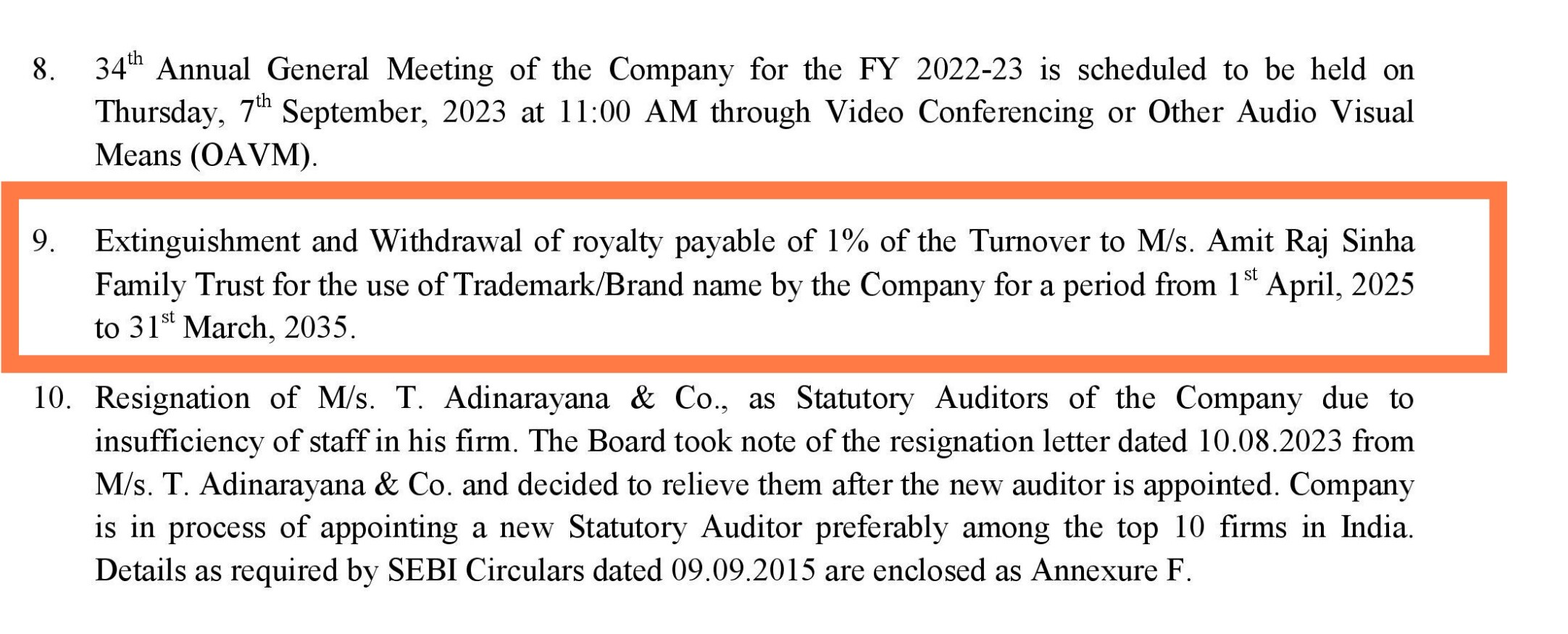

Yeah. Also Sigachi Industries will start paying a royalty of 1% of its sales to its promoters starting from 2025 . Someone had asked to tie the royalty to Net Profit instead of Sales and the Official on concall said they will consider. Any new updates on that front?

1 Like

In recent concall cfo gave positive indication. But who knows what they are going to do.

1 Like

Auditor resigned

Changing face value of the share

looks like these guys lost the track

1 Like

Investors have concern that auditor are some how related to promoter group( see the concall ). They( promoter ) explain that auditor are not related to promoter in any such way. But Investors seeing as corporate governance issue.

So that why,

I think they want to change the auditor, so investor don’t see corporate governance issue and get higher multiple.

See they removed they 1% royalty to promoter. They are working on corporate governance issue that investors raised in past one year.

Company is becoming more investor friendly. (Not the best corporate governance practices) but they are evolving.

3 Likes

On changing face value i am confused.

But i think they have large HNIs who want to exit and there is low liquidity so for that they might be doing this share split.

1 Like

Could you please share the update on this 1% royalty paid on sales is no longer paid ?

Bse filing

https://www.bseindia.com/xml-data/corpfiling/AttachLive/2b784931-6f8d-49ec-b5b4-e7b79ffd1609.pdf

5 Likes

I have 2 questions on Sigachi Industries for the experts on this thread:

- Why did the company go for a preferential issue at a discount to current market price and not go for a Rights issue?

- What will they use the 261 Cr+ amount raised through preferential issue?

Would be grateful for your views on this.

3 Likes

Accent Microcell - Indian Competitor for Sigachi is listing this month.

3 Likes

Industry Overview

FY2020 and FY2027, the pharmaceutical industry is projected to grow by a net cumulative USD 500 billion1 and the worldwide market growth is expected to return to prepandemic levels by 2024.

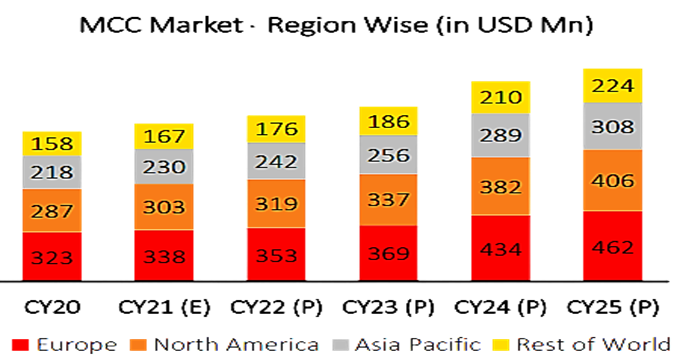

Microcrystalline Cellulose Market size was valued USD 1.14 Bn in 2022 and expected to reach at forecast to reach USD 2.05 Bn by CY 2031, growing at a CAGR of 6.7% during CY 23-31.

The global MCC market is expanding due in large part to the growing application of MCC across various industries. To stabilise and prevent caking in beverages, for example, MCC is utilised. Additionally, it is used in frozen food as a hot and cold stabiliser to extend the product’s shelf life.

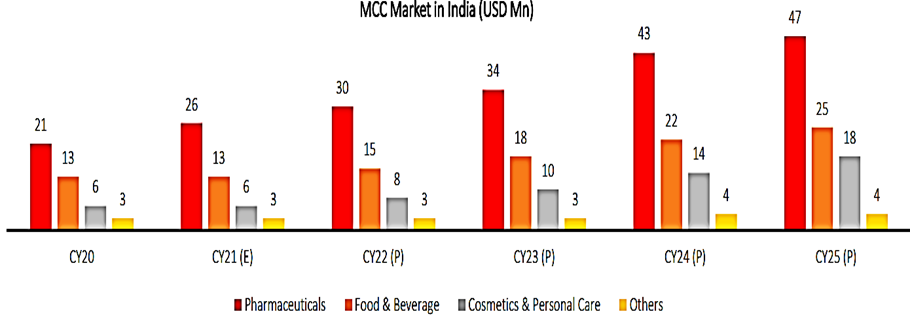

The domestic pharmaceutical industry in India was estimated to be valued at USD 41 billion in FY2021 and is likely to be valued at USD 65 billion by FY2024 before reaching USD 130 billion by FY2030.5.

Company Overview

Sigachi Industries Ltd, a Telangana-based company, was first established in 1989 under the name “Sigachi Chloro-chemicals Private Limited” with the intention of producing chlorinated paraffin. The company made the decision to expand its line of business and start producing microcrystalline cellulose (MCC) in the 1990s.

The company’s name was subsequently changed to “Sigachi Industries Private Limited” in March 2012. To meet the growing industry demand for MCC, the promoters established “Sigachi Plasticisers Private Limited” in 2009 and “Sigachi Cellulos Private Limited” in 2011, respectively.

But in 2014, the previously mentioned businesses merged with Sigachi. Additionally, the company changed its name to “Sigachi Industries Limited” in December 2019 after it was converted from a private limited company to a public limited company (equity is listed on BSE).

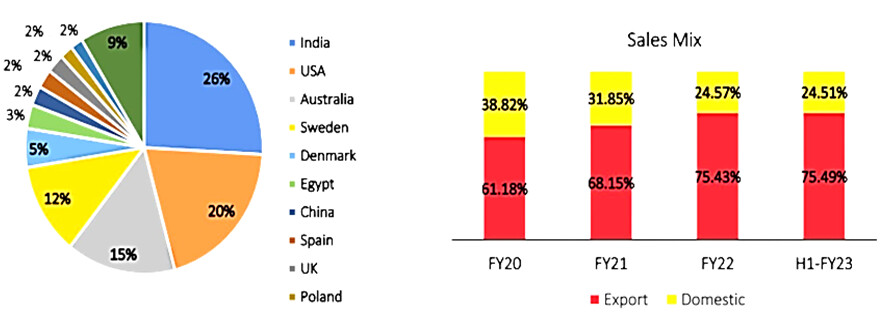

The company exports its goods to over 50 nations, such as Australia, the US, South America, the UK, Poland, Italy, Denmark, China, Colombia, Bangladesh, etc.

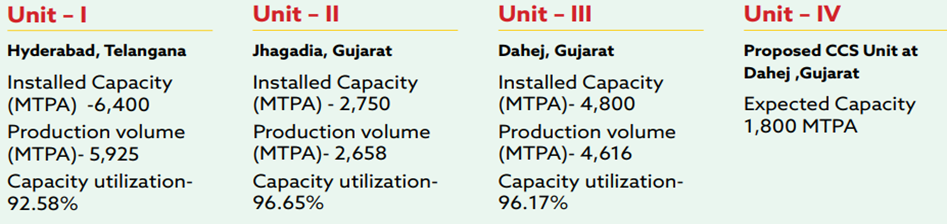

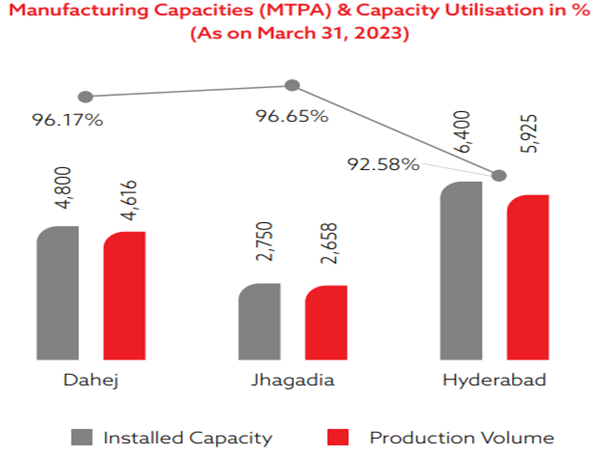

The company operates three MCC manufacturing facilities in Dahej, Jhagadia, and Hyderabad. The plants’ installed capacity and capacity utilisation are as follows: 6,400 MTPA in Hyderabad; 92%, 2,600 MTPA - 93% - Jhagadia, 96% of Dahej’s MTPA is 4,800.

Business Model

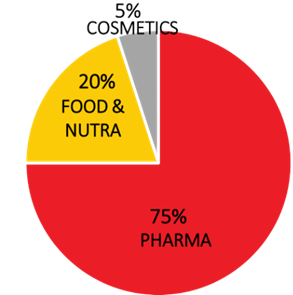

Microcrystalline cellulose (MCC) and other cellulose-based excipients are the foundation of Sigachi Industries Ltd.'s business strategy. MCC is a tasteless, odorless, white powder that flows freely and is insoluble in most organic solvents and water. It is utilized in many different products, such as food and drink, cosmetics, pharmaceuticals, and various industrial uses.

Company manufactures MCC of 60 different grades ranging from 15 microns to 250 microns having varied applications in the pharmaceutical, food, nutraceutical and cosmetic industry.

Brands Portfolio

Sigachi sells its cellulose based products under the following brands: HiCelTM, AceCelR, CoatCelR, GloCelR, BARETabR.

The company additionally manufactures different product grades in combination with different chemicals such as mannitol, carboxy cellulose sodium, and colloidal silicon dioxide to meet the expanding demand for co-processed excipients.

Application Segment or End-user

Pharma Portfolio consists of :

Antiulcerative API’s & their intermediates, Pre-Formulated Excipients

High Functionality Excipients, Thickeners/Stabilizers, Binders, Superdisintegrants

Lubricants, Functional Fillers/Carriers, Spheres.

Food Ingredients are Primarily Used as:

Stabilizer & Emulsifier • Dietary Fibre • Bulking Agent

• Texturizer • Anticaking Agent • Flow Improver

Cosmetic Ingredients are primarily used as:

• Sensory Agent • Texturizer • Filler • Humectant

• Flow Enhancer • Anti-Caking Agents.

Chemical applications:

- Cellulose products are utilised in the chemical industry as filter aids and electrodes. These goods are both reasonably priced and eco-friendly.

- Deep penetrating welding can benefit from MCC since it produces less slag, provides a nice texture, and keeps welding rods from cracking.

Key Clientele

Some of the important clients are Wockhardt, Ipca, Cipla, Lupin, Himalaya, and Herballife Nutrition.

Revenue Break Up

Segment Wise

Competitive Strength

- Sigachi appears to be a fantastic business. It boasts a sizable customer base focused on exports, newly operational capacity, strong product demand, an excellent margin profile, and a rapidly expanding top line.

- In order to maintain a strong market presence in both domestic and international markets, SIL has established three multi-locational manufacturing units in Jhagadia, Dahej, and Hyderabad. These locations enable SIL to deliver products in a timely, effective, and customised manner, catering to the unique needs of various demographic segments.

- Because MCC is a low-value product, producers find it easier to pass on price increases and inflationary pressures associated with raw material costs. Because of this, the margins typically stay the same for all parties along the value chain.

- MCC is manufactured by the Company in 60 distinct grades ranging from 15 microns to 250 microns, with various uses in the pharmaceutical, food, nutraceutical, and cosmetic sectors.

- The company has 126 Vendors & 337 customers through which company runs its business

Future Outlook

-

In addition to contract manufacturing sodium chlorate, stable bleaching powder, and poly aluminium chloride, the Company has an agreement with Gujarat Alkalies and Chemicals Limited (GACL) for the operation and management of GACL’s manufacturing facilities.

-

The announcement that the acquisition of 80% stake in Trimax Bio Sciences Private limited for a consideration of ₹100 crore. Furthermore, SIL’s board has approved allotment of convertible warrants (through which the company is expected to raise around ₹286 crore)

-

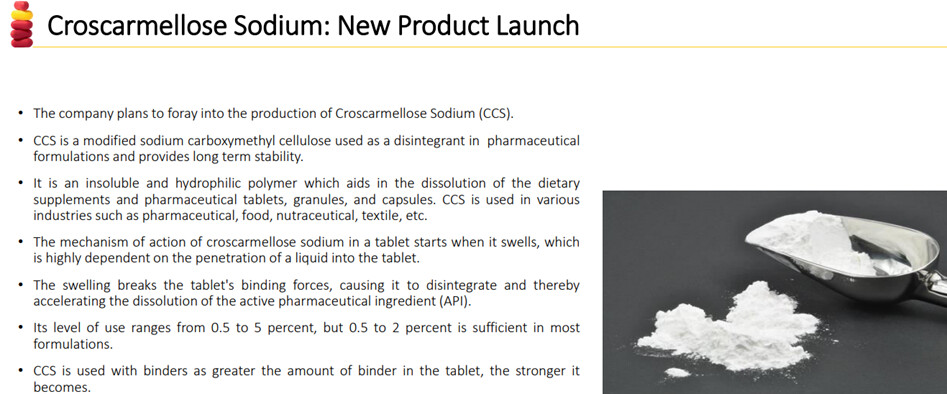

Introduction of a novel product called croscarmellose sodium, or CCS, Pharma companies have a strong demand for CCS, a high-value, high-margin product. It serves as a disintegrant in medications to guarantee that the active pharmaceutical ingredient (API) is absorbed by the body at the appropriate time.

-

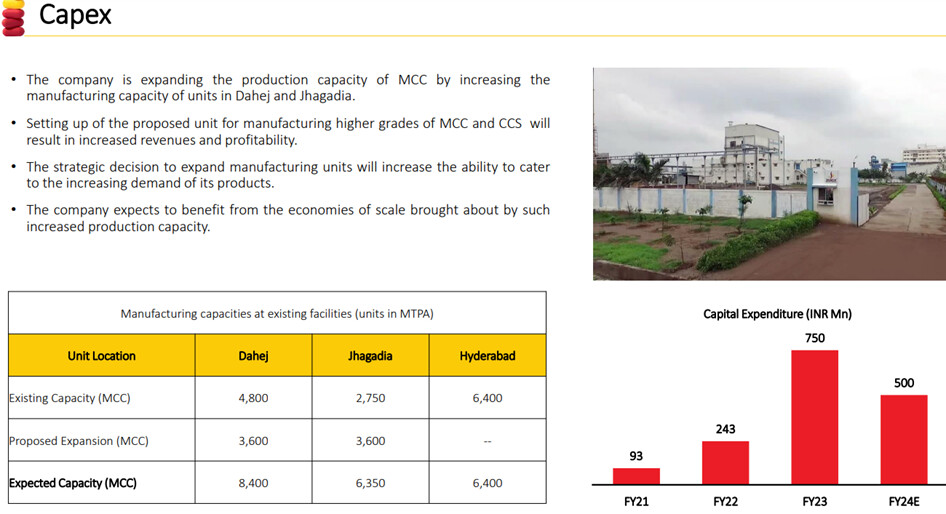

Capex amounting to arounf ₹32 Crore w.r.t the project to manufacture CCS, however, is yet to begin. The company is expecting an incremental revenue of around 10-15% from the said expansion

-

The company plans to enter the human nutrition sector, concentrating primarily on business-to-business (B2B) markets in India and other countries.The product line will consist of premixes of micronutrients, spray-dried ingredients, and other related goods.

-

At Dahej and Jhagadia to focus on the growing demand of MCC, setting up a new unit at Dahej to

-

manufacture CCS.

Risk

- The pharmaceutical industry, which currently accounts for roughly 70% of demand, is the main application for MCC as a product any down trend in the Industry may impact the company performance.

- Regional firms control a combined market share in their specific regions. For instance, Sigachi, an outside company, only works with generic pharmaceutical companies, while DuPont supplies the majority of innovative pharmaceutical companies in North America.

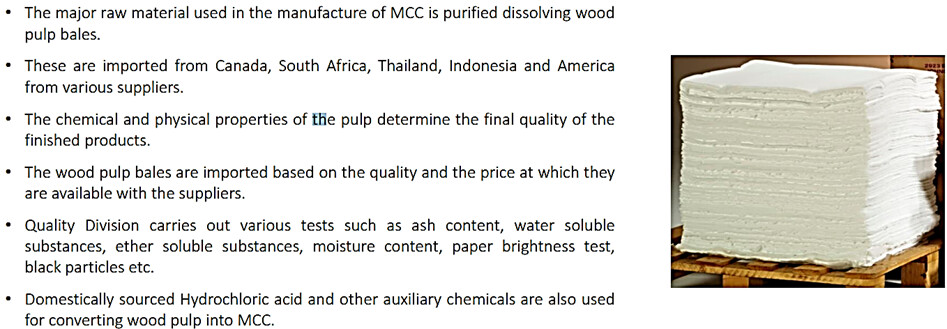

- Due to the scarcity of standard refined wood pulp and eucalyptus in the domestic market, the company deals with a concentration of suppliers and obtains nearly all of its raw materials from abroad. The company imports wood pulp from countries such as Canada, Germany, Switzerland, USA, and Hong Kong. The remaining 30% would be purchased based on pricing opportunities. The company purchases 70% of its raw materials through annual contract pricing with set delivery schedules.

Notes For Understanding

Excipients -

Excipients are substances that are added to pharmaceutical formulations to improve their stability, performance, or appearance. They can also be used to improve the patient experience, such as by making medications easier to swallow or taste better.

Excipients are typically inert, meaning that they do not have any pharmacological activity. However, they can play an important role in ensuring the safety and efficacy of medications.

Some common examples of excipients include:

- Fillers: Fillers are used to bulk up medications and make them easier to produce and handle. Common fillers include lactose, starch, and microcrystalline cellulose.

- Binders: Binders hold medications together and help them to retain their shape. Common binders include acacia, povidone, and gelatin.

- Disintegrants: Disintegrants help medications to break apart in the stomach so that they can be absorbed into the bloodstream. Common disintegrants include sodium starch glycolate, croscarmellose sodium, and povidone.

- Lubricants: Lubricants help medications to slide smoothly through manufacturing and packaging equipment. Common lubricants include magnesium stearate, stearic acid, and talc.

- Preservatives: Preservatives are used to prevent the growth of bacteria and other microorganisms in medications. Common preservatives include methylparaben, propylparaben, and benzoic acid.

- Flavorings and colorants: Flavorings and colorants are used to improve the taste and appearance of medications.

Dis: Invested At Lowest Price No Buy Sell Rico**

2 Likes

OVERVIEW OF CONCALL Q3 FY2024 :

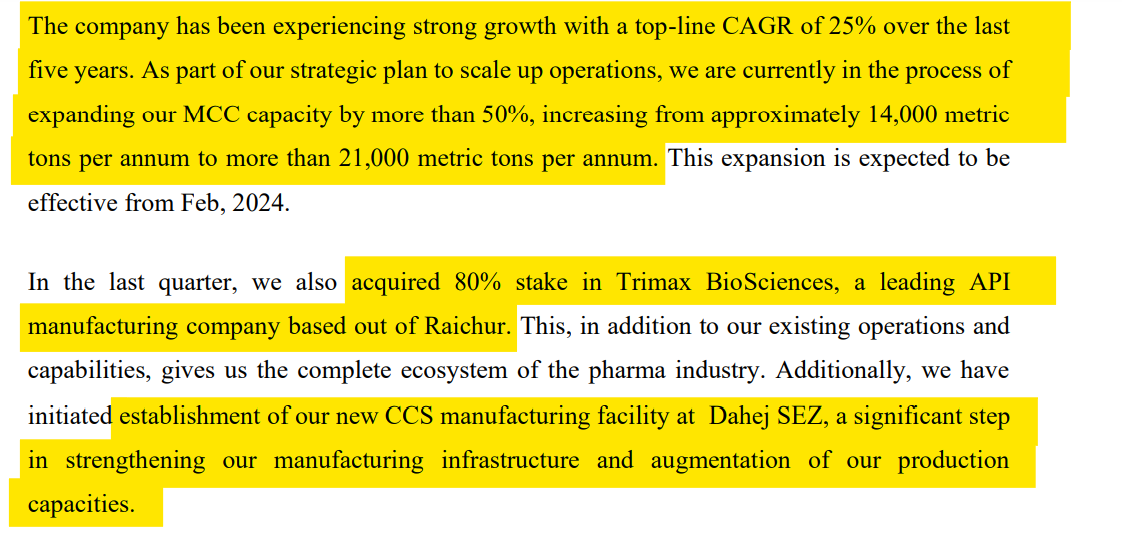

The company has been experiencing strong growth with a top-line CAGR of 25% over the last

five yearsWe are currently in the process of expanding our MCC capacity by more than 50%, increasing from approximately 14,000 metric tons per annum to more than 21,000 metric tons per annum.

Acquired 80% stake in Trimax BioSciences, a leading API manufacturing company

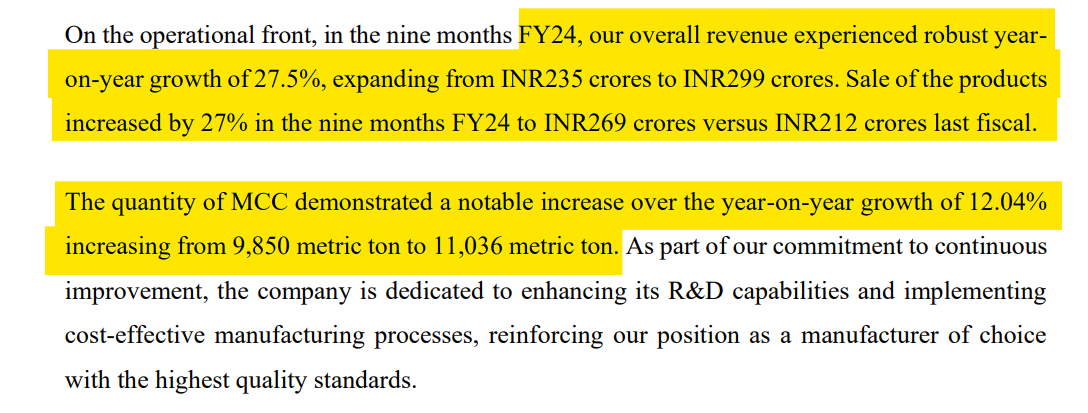

The quantity of MCC demonstrated a notable increase over the year-on-year growth of 12.04%

increasing from 9,850 metric tons to 11,036 metric tons

3 Likes

Is it due to preferential

ED freezes ₹1,100cr shares in demat a/cs linked to Mahadev app partner

They manipulated the share price of the below-listed companies.

GENSOL

TFCI

CUPID

BCL IND

SIGACHI

PARACABLES

APOLLO MICRO

MUFIN

SALASAR

SERVOTECH POWER

3 Likes