Thank you for asking great questions over conf - call …

1 Like

Sigachi moved so much today and can’t find any news in google. Volume is 6 times more than 20 day average. Some Big investors or DII/FII entered this stock?

1 Like

There are new perspectives that have made me skeptical about Sigachi. I never thought that way.

No new information.

We have to track how they scale up their OTC business along with MCC

No clarity on the profit share based on Revenue by the promoter.

3 Likes

My question at 44:00

5 Likes

Q2 Results

CONS NET PROFIT UP 38 % AT 13.5 CR (YOY), UP 6 % (QOQ)

REVENUE UP 44 % AT 82 CR (YOY) ,UP 5.5 % (QOQ)

MARGINS AT 19.7 % V 23.6 % (YOY), 20.6 % (QOQ)

1 Like

In March - Large increase in Receivables/ debtor days

In September - large increase in debt - indicating again increase in debtors.

Implying sales increase not translating into cash flows. Even worse is that increasing sales is not easy and huge increase in capacity.

I think thats why they went for IPO inspite of Nil term debt for many years.

Better to wait and watch…

1 Like

The big hangover is promoter is taking cut from the sales as Royalty, no changes on this front, this is very big negative in my view

5 Likes

Good point. Where is royalty mentioned - in annual report? is there a reason for giving this royalty.

Few doubts on this entity while reading their conference call and financial statements from stock edge,

Good things,

- Margins are great, sales increasing with same margins,

- Company expanding and moving up in value chain

- Customers are essentials, so demand for customers products is not an issue.

Observation, Doubts,

- Tax paid is only 11% and conf call notes mentioned that SeZ period of 15 years is going to expire and from next year there will be a tax increase of 5%. This will affect the EPS and the price.

- Entity has diluted it’s equity twice, first time in 2020 and 2022.

- They have diluted equity without having long term debt is more scary because any owner wants to retain the ownership and first will take debt to expand. That too in low interest scenario, they have not taken any long term debt.

- The equity percentile of the promoter is less than 50%, why?? Red flag for me.

- Debtor days is tremendously increasing and short term borrowings is increasing. More and over the short term borrowings, the 2022 pat is fully consumed by debtors increase. This is happening after IPO. Either the sales can be fake or the customer is beating the MCC market down. High margins become worthless with worst working capital.

- They are venturing into too many things at the same time, Nutraceuticals, OTC, O&M, capacity expansion, Dubai office. All this is okay, but when we look at this along with cash flow worsening is a worry. Need to get clarity from business

- The MF invested 5% of the company and next quarter they exited?? Why?

- At this market where liquidity is high why did the price falll from the roof. Why the price went to so high and why it fell.

- The retail investors are more than promoter or DII,FII.

11 Likes

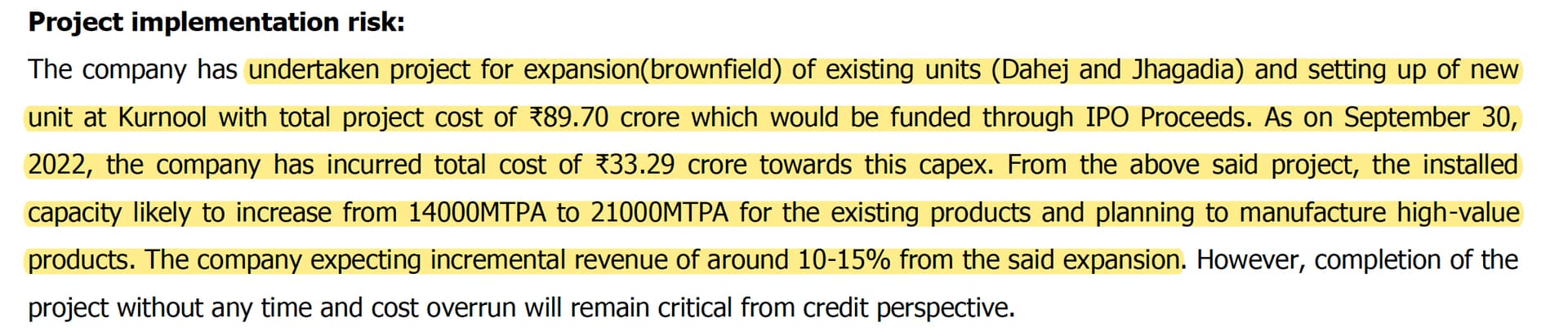

The recent credit rating report mentions that the expansion will increase capacity from 14k to 21k MTPA, but only add 10-15% to revenues. I dont understand how this is possible, as management has guided higher growth. Does anyone have insights into this?

2 Likes

Hi.

Entering new segments is good as long as the profit margins are maintained in line with the sales.

The concalls show management also guided for sales growth but profit growth would be lower as gaining market share for new products and building the brand for OTC products.

Not a Buy/ Sell recommendation.

I prefer to stay away and read on the con calls and annual reports.

3 Likes

Could you please help me understand the derivation of figure of 3000Cr market size for MCC in Pharma? Any reference will be highly appreciated.

Is the new 7K MT capacity coming live from this quarter or next fiscal ?*

The only thing I can speculate is that CRISIL referred to FY24 revenue and not on permanent basis. If that is the case, this could be to do with their capacity utilization rate which could take a couple of quarters to ramp up…

![]() Concal (Conference Call) “Sigachi Industries Ltd” - Q4 FY23

Concal (Conference Call) “Sigachi Industries Ltd” - Q4 FY23

Major Guidance :-

https://twitter.com/AnirbanManna10/status/1663075750029983745

1 Like

Hi, everyone i have a question.

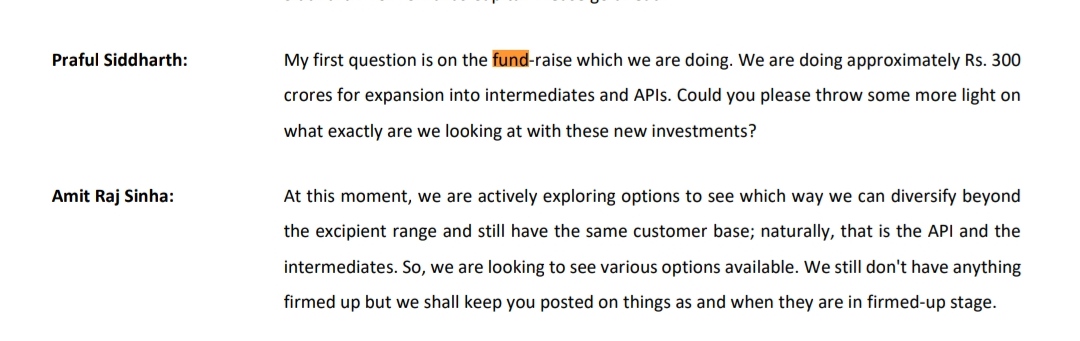

In Q3FY23 there is discussion on 300cr fund raising. I can’t find any disclosure on BSE. Can some one explain?

Here you go…