The company will be meeting institutional investors 23-28 March 23 in Mumbai. With FII/DII money inflow coming in, it may see PE rerating. I can foresee Shivalik Bimetal trading at par with valuations of Schneider/Siemens in near future when it will transition from small cap to mid cap space.

The latest investor presentation link is shared below

5 Likes

thanks for sharing it, ive summarized it in the stock story thread:

2 Likes

Valuation at Par with OEM, not possible unless this technology commands at a huge premium and highly patented. Because mkt know, they don’t have pricing power with the OEMs

Also has it reached it’s peak margin already ? Now it will be only Top line growth ?

Just a few thoughts

1 Like

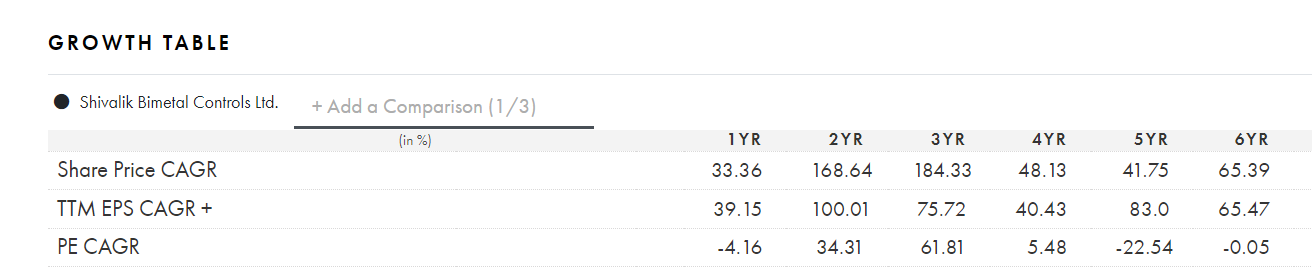

As Sageone’s Samir Vartak says, the Price Growth = PE rerating + Earnings Growth, from the below table of Tijori, we need to see , how much PE rating is possible ?

Vishay presenting at APEC expo. Seems like there are exciting growth prospects for Vishay and thus also for SBCL as a supplier.

Disc- invested

3 Likes

Few queries in mind:

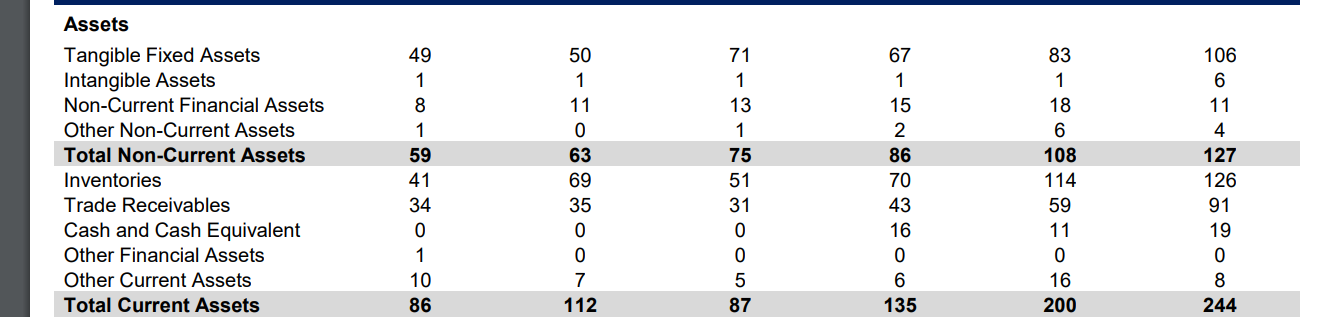

- Inventories and Trade Receivables has been increasing over the quarters

- Why is the company paying dividends although it has quite a lot borrowings?

1 Like

You supposed to look at receivables growth in relationship to sales. Receivables and Inventories as an absolute number is meaningless

As for debt dont look at the absolute number. Look at D/E or Net debt/ equity.

4 Likes

As per monthly charts the life time high of SBCL is at 506 levels .A strong move above that level especially a weekly close above that level can lift the prices to 653 in the very short term.

8 Likes

3 Likes

Notes from the meeting done in Mumbai. Pardon any typos, sharing running notes as is.

Addressable market for shunt resistors is 230million$ (Shunts and resistors): this is size only of the products we do. 230 million$ mkt size: 60% BMS 40% Smart meter.

We are doing only 250 crores (30million$ i.e 12% market share). Isabellehe (German) is competitor. We are not facing direct challenge from anyone else who is across.

Welding and resistor making are 2 separate things.

There are very few do entire thing : welding and resistor making, we do it. Welding is backward integration.

Out of 250 crores sales (Shunts) : 42% energy meters. 70% Indian customers.

We see it growing as a result of smart meters, lot of relay manufacturers started manufacturing in India (shunts used in this), which were earlier imported so we are now getting good opportunity. Permanent Magnet does it, One German does. We work with meter manufacturer.

Meters smart : growing consistently from long time. 14-15Rs we supply in 1 meter, 1 shunt.

Electrical contacts : relatively new business, actively ramping up capacities. Against 1 15 Rs shunt goes in relay we get 10 times value for this business, so added opportunity with same customer. Relay in India is giving us volumes for shunts and electrical contacts.

It is a unique businesses, high value added part(of energy meters portfolio) we are in, we are not in the generic category

What is a contact : switch turns off due to overheating (some point closing and opening , made of conductive material, silver alloy, that point is electrical contact).

SEEPL JV >> now WOS, contact plant is geared up for US market. Our partners were American, suited for American market. Earlier it was partner control, partner sold business. This market solely ours now.

We are struggling with capacity in contact, take 1 year for new plant (10kms from existing location), building is ready, take 1 year by the time functional.

50 crores of contact: 85% is domestic.

JV was doing the Export market now this ratio will change. How is Lead generation in contact ? The customer base is small, few. Somebody manufacturing switchgear, they have to go to 3-4 suppliers in world, supplier base in not big. Indian switchgear : they switch suppliers so they are familiar, reference business, word of mouth.

Bonding mill : highly customised rolling mill. Cost is high. Custom made. Our equipment came from Sweden company, German mill, after installation, took 1.5 year of trial to get tolerance and dimension right despite us being in 35 years. So takes time to rampup.

Focus on RD :

Our research team has been consistently growing. There are 6 people dedicated. NS Ghumman sir solely working on it passionately on it. Infect automotive shunt is his contribution. Kabir ghumman carbon copy of NS ghumman. Shaping up to do that. He has 2 people under him.

3 vertical : GM 49-50% in bimetal and resistor similar, contact GPM lower than that at 27%.

Capacity after expansion and guidance.

Next 2 years capex : 25-30 crores(in shunt resistors only). Resistors : 20 crores done, 25-30 in next 2 years, mainly efficient finishing methods of resistors high precisions.

3x of bimetals plant (600 crores, 2 shift basis and some processes (nailing) 3 shift basis),

Contacts : 100% 3 shift basis. As soon plant is ready, 10 crores in 1 year ramped up to 3x capacity.

So Potential Revenues post expansion (basically after 2 years).

200cr in Bimetal currently – 600 cr revenues at full. It is in place.

225cr in shunt resistor – 600 cr revenues at full. Will take 2 years.

50-60cr in contract business – 300-400cr revenues. Will be fuctional in 1 year.

We have visibility from customer requirements. These numbers are not aggressive, and more conservative keeping in view the economic conditions.

Contribution from Vishay 20%. It has come down from 35%.

We will grow 20% YoY 5 years. We are at 470 crores. 5-6th year, 1600 crores (all 3 plants fully utilised). Whatever projecting is basis customer study.

Barriers :

Customer switching : approval process, not easy to switch only basis of cost.

New Competitor will need to invest – 400cr capex and be willing to do trial and error for 4-5 years (Don’t see a competitor at the moment, does not rule out than competition will not try It).

Shivalik’s Value add comes from stamping – technical aspect. Customer pays for tooling and dyes initially which costs 2-3L for Shivalik. 30k USD if same tooling is made by competitor – so customer does save cost, also subsequent tool costs are borne by Shovalik since it gives them business for crores and hence bear couple of costs

Schneider and ABB : They know its our core business, secured supply whereas other supplier (not core businesses, giving lead times 8-12 months and some are downsizing). Competitor’s not core business, they don’t add capacities. Our competitors (Aperam, key competitor brought down bimetals from 1200 to 500 MT, some came to us, some gone EMS, some Fepac in china).

Switchgear – Schneider 100% supplier, secondary source is backup for them.

Capacities ramp up takes time for testing, few qualities, 2-3 years, validation in region, so business takes time over 5 years.

Quantitative of Vishay has grown. We are sole supplier to them. Welding shunt we are only suppliers. We also supply bimetals strip to them.

Shunt and bimetal price : price is increasing, keeping in view energy or labor.

Main RM : bimetal nickel alloy, Shunt it is copper. 80% plus RM is imported

Policy of pass through: back to back pass on with customer to avoid commodity volatility.

Automobile sector : We are getting more and more geared up different world. Approval from : continental and Hela(couldn’t get this name) shows our capabilities.

Current revenues: 45% resistor revenues (55% BMS(auto), 40% meter).

GPM variability : We started supplying components in 2021 which is value added and hence GPM improved.

We are making strip and component out of strip. FY23 (more than 70% in component form and 30% in strip from.)

Product approval from OEM : For next 5 years, similar level growth, after 5 years, explosive growth from automotive after that.

We get a year’s forecast, 1 year forecast gives us visibility of 20% growth.

BMS : We work with OEMs in designing stage, Mahindra through their BMS manufacturer (auto guys involved in approval). OEM tests and approves it.

5years : equal product mix in shunts. We target shunts where welding needed that is our core competence. What gives needs to weld : it is more application driven thing, depends on accuracy.

Component we supply to Vishay is different from what Vishay does in house. Vishay doesn’t weld. Cost is huge, technical investment need to made hence Vishay will focus on much bigger opportunities.

Resistor we supply to Vishay he wont to continental.

Margin and WC guidance :

5 months WC will reduce to 4 months, but still is a WC heavy business.

WC days : We have been reducing cycle. WC intensive, RM is tailor made and not off the shelf RM. Not easily available. We have been importing, inventory cycle 4 months. If material started from Japan it takes 45-50 days to reach. Receivable : as we grow all our customer international pay upfront using some instrument, reduce WC cycle. Talks with vendors : more credit terms from them. We are hopeful coming years cycle 150 days to 120 days in 3-5 years.

Peak EBITDA of 26% possible, currently 22%

PAT margin is 16% currently, improve up to 18%

Fund needed ?

No as of now, Capex done.

61 Likes

I have got an opportunity to attend the analyst meet the company planned in Mumbai during Last week of March 2023. Find enclosed my notes from interaction with management.

Shunt Business

The shunt resistor market size estimate of USD 230 mn in FY22 is for relevant segment for the company. Total sales of company from this vertical for company is Rs 230-250 cr (~USD 50 mn, giving approximate market share of 12% in relevant segment). There many types of shunts which are used in Automobile. The company focus is on electric beam welded shunts which are relatively difficult to manufacture.

Smart meter business is currently focused in India and account for 40-45% Shunt business (Note sure on the numbers), while Automobile account for balance shunt business. In Automobile segment, the company has also now got approval from Hella and Continental.

Cost of shunts is around Rs 14-15 in one Smart meter. Previously, Relay in smart meters were imported In India. Requirement for Relay manufacturing need Shunt. However, now few Indian players have started manufacturing Relay in India which would drive shunt demand for Shivalik in Smart Meter. The company is involved from design stage with the meter manufacture, Hence, in case Meter manufacturer wants to change the shunt, one has to go through full approval cycle again and given small cost, unless company provide inferior quality shunt or not able to supply, the chances of being replaced by competitor is very low. Same also affect gaining market share from other players for the company. So despite competitive advantage, the company cannot just gain market share by cost competitiveness in most business.

Vishay account of 40% of shunts business and 20% of total sales of the company.

Bimetal Business:

Ability of develop various type of Bimetal with unique usage is key competitive strength of the company. Bimetal is key raw material which is used in Shunts. Company like Vishay initially started sourcing Bimetal from the company, however from 2021, the company started to supply Component (i.e., Shunt and other value-added products). Having backward integration in bimetal is key strength of the company and provide unique competitive advantage.

Electric Contact business

This business was previously in JV with the partner. The global partner exited this business and sold India equity holding in JV to the company. Silver alloy used in open and close of comer is key area of operations. Previously, JV partner allowed the company only to market in India. However, the plant was equipped with latest technology. With the JV partner constraints being out and the company is scaling up capacity, it expects significant growth in this business. Margin in the business is relatively lower than Bimetal and Shunt but the growth potential is high with long pathway for addressing both local and global (specifically US market) demand. The company in process to add new plant at 10 km from existing facility. That facility shall commence production within 12-15 months. The current sales from this business are Rs 50 Cr (with 85% being Indian market and balance is export). However, with increased focus of US market, over medium term, export growth is expected to higher than domestic business in this segment.

R&D Team:

The company has currently 4 members dedicated team in R&D. Mr. Ghumman and his son Mr. Kabir are leading R&D efforts of the company. While the cash expenditure on R&D is not high, most of key learning from manufacturing and process improvements are kind of skill based competitive advantage which provide edge to the company along with backward integration and scale of operations.

Competition

In Bimetal and Shunts, while there are multiple players in manufacturing various type of shunts and specific Bimetal, the share of Shunts and Bimetal in total revenue for most of global players is small. As a results, many players like Sandvik are looking at exiting business despite higher margin due to relatively small size. That is working additional advantage for Shivalik in global market. The volume it supplies every year in export market are increasing, first due to higher demand and second due to reduced competition.

Capex and finance

The company expect to spent Rs 20-25 cr during FY23 and FY24 for capex. The completed capacity with 2 shifts (some processes assumed 3 shifts) can provide sales of Rs 1,600 cr at full capacity. Over 3-5 year, the company also intend to reduce working capital days by 10-15 days. Currently, there are no plan to raise new equity capital as capex can be funded easily from internal accruals.

Disclosure: Among my Top 2 holding. My view may be positively biased. Not a SEBI registered advisor. Not suggesting any investment action. I may change my investment decision in the company without informing forum

72 Likes

Thanks @nikhil_chowdhary @dd1474 for sharing detailed notes.

Request @Anirudh_Shetty to share your Notes that adds more granularity/perspectives to above.

While I am sure a few more like @Malhar_Manek and others would pitch in with more granular details, I am doing a different take. Based on what we heard from SBCL Management in Mumbai meet, let’s try and capture what we have added to our understanding of SBCL strengths/opportunity mapping since Sep 2022 AGM.

-

Only Company globally to have these 3 verticals under one roof (factory) - Bimetals, Precision Shunts, Contacts

-

Largest EBW Capacity in world - 7 existing machines with 8th being commissioned. The next largest EBW capacity is in China (probably 3 machines)

-

The first EBW machine was bought by Shivalik from Germany (?) at off-the-shelf prices. Post that they started assembling the machine(s) buying from all the sub vendors, including 3rd party software. Incredibly, SBCL cost now comes to one-fourth or lower of what a new set up costs

-

SBCL has another impeccable measure of deeper customer penetration. If SBCL customer count is say 10, for 6 out of this 10, SBCL is the Exclusive Supplier

-

SBCL is a preferred global supplier based on cost leadership, customer responsiveness leadership, and Delivery Lead Time leadership

-

100% of RM volatility is pass-through on way up/down; 100% of SBCL products are Customised; 100% of RM is Customised (true for all 3 verticals)

-

Because of this, SBCL needs to maintain for every month of production - 4 months of additional Inventory.

1 month inventory in warehouse

1 month inventory in custom clearance

1 month inventory in High seas

1 month inventory in dispatches -

Unlike say a Vishay, or a Marquardt or a Rohm who define themselves as Shunt Resistor Suppliers, SBCL defines itself (and it’s addressable market narrowly) as Edge, EBW Shunts Supplier. Applications are primarily Automotive BMS and Smart Meters. Conservatively they peg this global market at $230 Mn today.

-

Thus defined, SBCL sees itself as #4 player globally after Vishay, Continental, Hella. Hyundai Mobis is the other one in Top 5. SBCL claims to have taken away 90% market share of Isabellenhutte in its India market segment. According to SBCL Isabellenhutte is more a special alloys player than Shunts

-

When quizzed why not do other EV (non BMS) Shunts, SBCL mentioned that these are pure resistor shunts mostly where Shivalik will not have the Bimetal-EBW-Bonding edge and hence prefers to stick to its core strengths. If you want to be a player in pure resistor shunts, then you cant just choose a or b product, you need to have a much wider basket of products (that might mean Shivalik moving off their protected turf)

-

Very interestingly, SBCL has thus positioned itself as a win-win ally and NOT as a Competitor to bigger players in this market. Hella and Continental relationships are on solid ground. This is new EV product development for them. Should eventually scale comparable to Vishay, if not more. Significantly Vishay is positioning itself for substantially higher growth [Q4FY22 Transcript]. investing $400 Mn per year for next 3 years (vs $160 Mn annual spend earlier)

-

Even as SBCL started off with ICE BMS Shunts, today 90% plus share is for EV BMS shunts. Unlike our previous understanding SBCL does not claim to produce other Shunts used in EVs such as DC-DC Motors, or others. They want to only play the shunts market - that builds on their strengths - Edge, EBW and Bonding - where they are (and will remain) unshakeable!

-

Most Customers share annualised forecasts. SBCL expanded capacity (1600 Cr) is based on 6-7 year growth forecasts (non-contractual) shared by some of the majors. 65% Visibility from Customer shared forecasts (35% they will need to find new customers). Fully utilised by next 6 years is a conservative estimate as per SBCL Management

-

SBCL Management Team breadth is bolstered by addition of Neville Fernandez. Neville is an investment banker with a rich profile in Corporate M&A & Structured Finance. When asked on his role at Shivalik he mentioned structured finance advisory. He seemed very well-versed with Shivalik strengths/opportunities/challenges and was invited by Chairman to add to CFO comments/answers to some queries, which he handled with aplomb.

-

My sense is (for whatever it is worth), since Management has clarified multiple times in unambiguous terms SBCL doesn’t need to raise funds, there is probably a stake sale down the line (maybe someone within promoter family a 5%-10% stake). But that is NOT something that someone like Neville’s expertise is expressly called for. It’s probably the start of a process for a structured base - that allows/enables possibilities down the line. E.g. for M&A (distressed assets in developed markets are more common now), structured JVs with marquee customers (+1 strategies), and/or value-creating spinoffs

PS: Please Note My Take above is based on interactions in the larger late-afternoon group. Please be aware there are nuances (first-exposure ![]() ) which might NOT have been accurately captured by me. Please allow us a couple of days to get these vetted and verified.

) which might NOT have been accurately captured by me. Please allow us a couple of days to get these vetted and verified.

Disc: Invested from 2018 levels. My views are highly biased.

There is significant valuation risk embedded at current levels, even as Industry Tailwinds are strong (become stronger for bimetal side) and SBCL competitive position has become stronger. No significant Business/Industry Risks I foresee in near/medium term

79 Likes

Discussion with Shivalik management 29-03-2023

Market opportunity/ growth

Shunts

TAM of 650 Mn$ by FY30

This TAM is specifically for what Shivalik caters to today. This is the basis of current technology. Conservative estimate.

Key applications

Electric vehicles -BMS

Energy Meters

Solar (Nascent stage)

Not sure how this TAM will unfold as no of BMS/Shunts required is evolving

The estimated value as of today for 4W/4 BMS is 10-12$.

Per BMS 4 shunts are used. Therefore for 4BMS 16 shunts will be required.

The estimated value of total shunts required in 2W is 3-4$/2W

2W has a lower shunt requirement

2W opportunity is more than a 4W opportunity

More BMS might come into use, as this space evolves. Range could be 4-8 BMS in 4W

Solar – can this become a large opportunity? Shunts X value per shunt?

Any renewable source will contribute to energy storage. All these applications will require Shunts. Growth can be exponential but a industry today is at a nascent stage.

How do Shivalik Shunts differ from other Shunts?

For Any equipment where current sensing technology is required, Shivalik will play the role.

However where value addition is less, Shivalik does not want to enter. They get such offers from customers but choose to say no.

Shivalik edge?

EBW Technology sets Shivalik apart. This is 1 out of 10 process that needs to be done. Although the other 9 can be done by anyone, the EBW process is key edge.

EBW welding was started by Shivalik because of the existing segments which Shivalik was catering to.

Opportunity is not limited to only EBW welding , but Shivalik specialises in joining of 2 metals , so will find value add opportunities here.

Any new entrant has to first buy critical components, understand the technical know-how of this process which will take 3-4 years and later has to take customer validation which will again take ~2 years. In total it has to spend around 5-6 years. Given gestation period, need to invest ~100crs, small industry size- they will prefer to enter in another vertical where they can cater.

Shivalik Cost is 4-5 times lower

This EBW can be used to cater to other areas too. Like Defence e.g Tanks etc. However, don’t want to enter where demand is uncertain.

Will prefer exploring opportunities in electronics.

Bimetals

Q-Bimetals – historically growth has been in the low double digits here. but we are expanding significantly with 600crs of capacity being set up, so what exactly is the opportunity here? Is there a China + 1? From a cost perspective, how competitive are we versus China?

Is there a China+1?

Yes, the recent validation speed was unexpected.

Companies are actively looking to de-risk from China supplier

Shivalik is competitively placed on cost versus China.

Don’t see China as a competition given that Chinese suppliers are catering more to China itself (Need to understand China + 1 tailwinds better)

Will gain share from Europe and USA suppliers as these players are giants and the bimetals division is too small and not a focus area.

The Sandwick group shut their bimetals division overnight which resulted in supply chain problems for customers- Therefore customers want someone now who will specifically focus on this category like Shivalik caters to.

Bimetals:

Bimetals cost 1-2% of switchgear.

Export growth will largely come from Bimetal.

Already in the advanced Sampling stage with customers in Bimetals.

Shivalik is considered a benchmark globally for Bimetals. that positioning in Shunts is still being developed.

Electrical Contacts:

This is a cross sell opportunity with bimetals

This is a lower margin but higher ROCE Business.

Electrical contacts require precious metal material, lower GM and lower value add components compared to Shunts.

Financials:

Bimetals and Shunts have the same margins. (Why did company level GP margins expand over last few years then?)

10-12% EBITDA margin for electrical components. However, higher ROCE business.

Margins can improve with operating leverage.

Believes ROIC as per expected Margin/asset turns are sustainable. Their products are low cost for customer, they have cost edge, industry structure- not many competitors.

Q -All our 3 plants are in Solan, which is seismic zone IV, so how does one think about supply chain risk from a natural disaster tail risk event? Will the future expansion be done in a different location?

Don’t see risk from this. The only way they manage it is by building robust infra

Delhi is categorized as higher seismic zone

The Plant is on a flat surface. Therefore the risk is less. risk in Dharamshala is higher.

No earthquake has happened near the plant to date.

What explains high GFA turns?

Shivalik’s cost of machinery is 1/4 th less than peers because of their technical know-how expertise. Source machinery parts from different sources and fabricate machinery in house

55 Likes

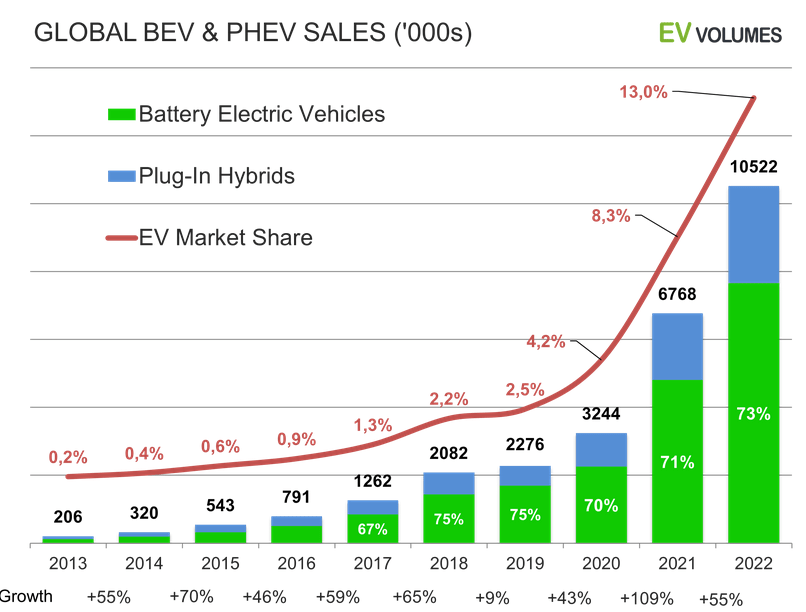

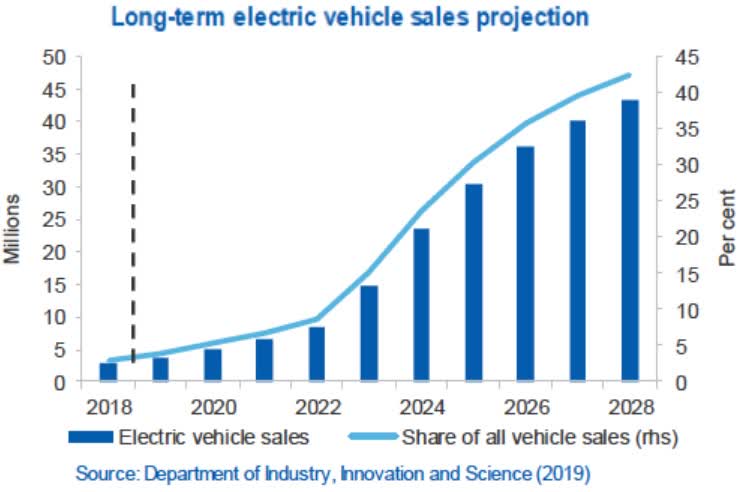

Although not exactly on the company performance, but would give an extract of the report I was reading on a website on the EV sales trend, as the sentiment affects Shivalik Bimetal.

The global sales estimates definitely paint a rosy picture for the company.

Source-

11 Likes

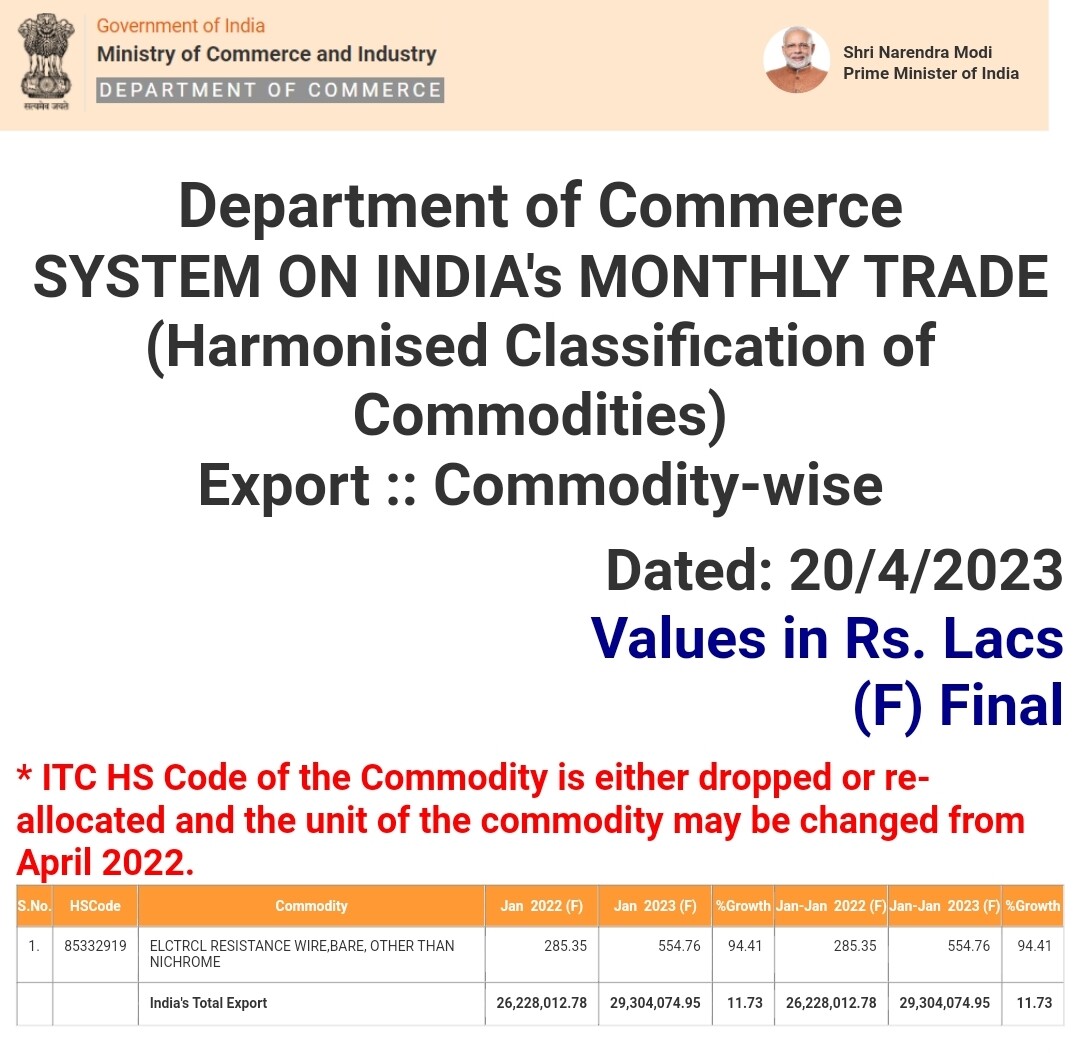

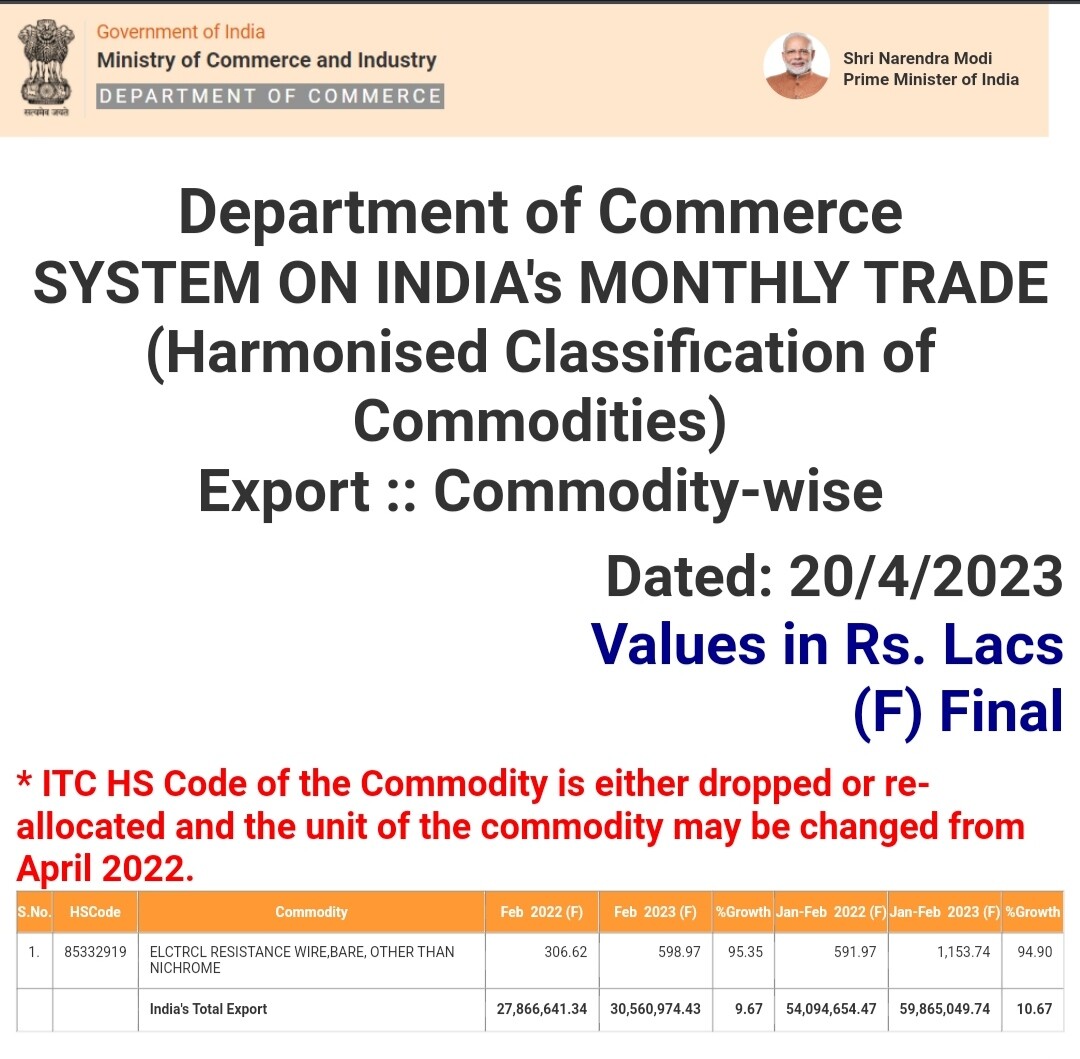

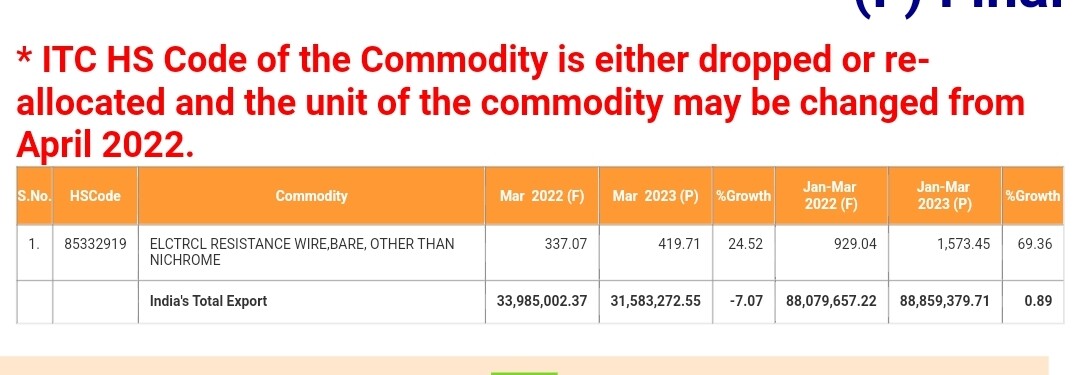

YOY trade Data for Jan and Feb is very positive. However, it’s 10% below the peak achieved in the months of Sept & Oct 22.

For Mar 23 it’s quite mediocre.

6 Likes

Exports to the US have been good. They have achieved 50% of last year exports in just 3.5 months of this calendar year.

16 Likes

I was just going through the earnings call transcript of VSH accessible here Vishay Intertechnology, Inc. (VSH) Q1 2023 Earnings Call Transcript | Seeking Alpha.

Earnings presentation attached here.

VSH-2023-1Q-Presentation-Investor-1Q-Deck.pdf (1.3 MB)

Positive commentary from the management on future prospects in automotive, defence and medical verticals.

Shivalik Bimetal as a preferred supplier will continue to benefit from the growth of VSH.

Looking forward to positive Q4 results from Shivalik Bimetal and some positive management commentary.

26 Likes

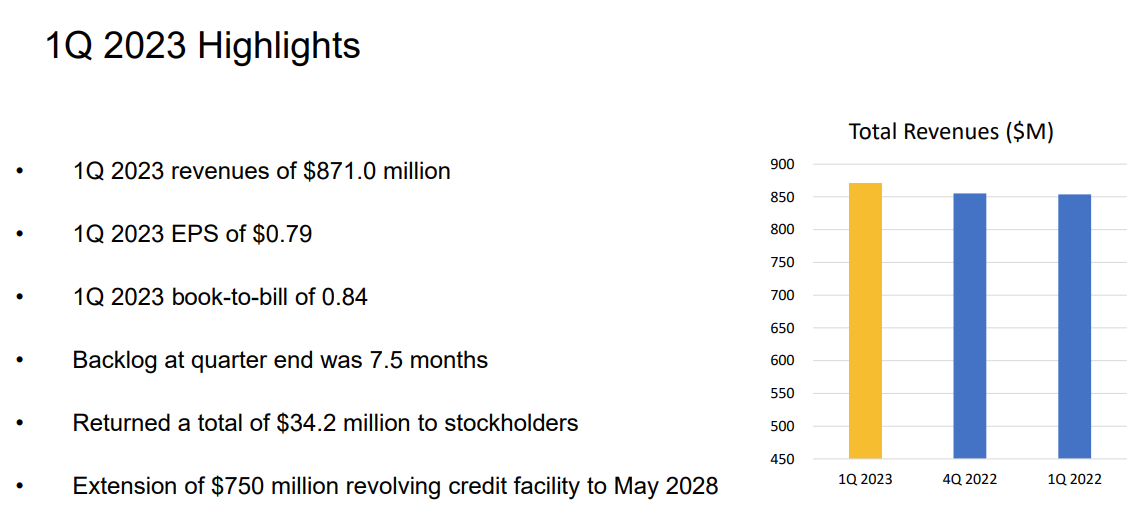

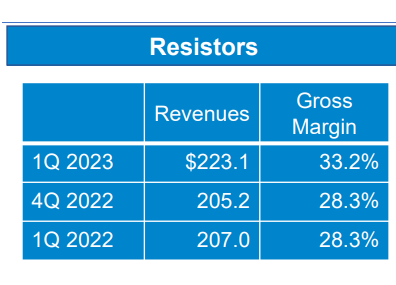

Vishay results were on 10 may.

Book to bill & order backlog are still high indicating a healthy demand supply situation.

In fact, gross margins in resistor segment expanded 500 bps for vishay and showed a reasonable growth QoQ & yoY

They also talked in the concall about increasing capacity for resistors (& MOSFETS)

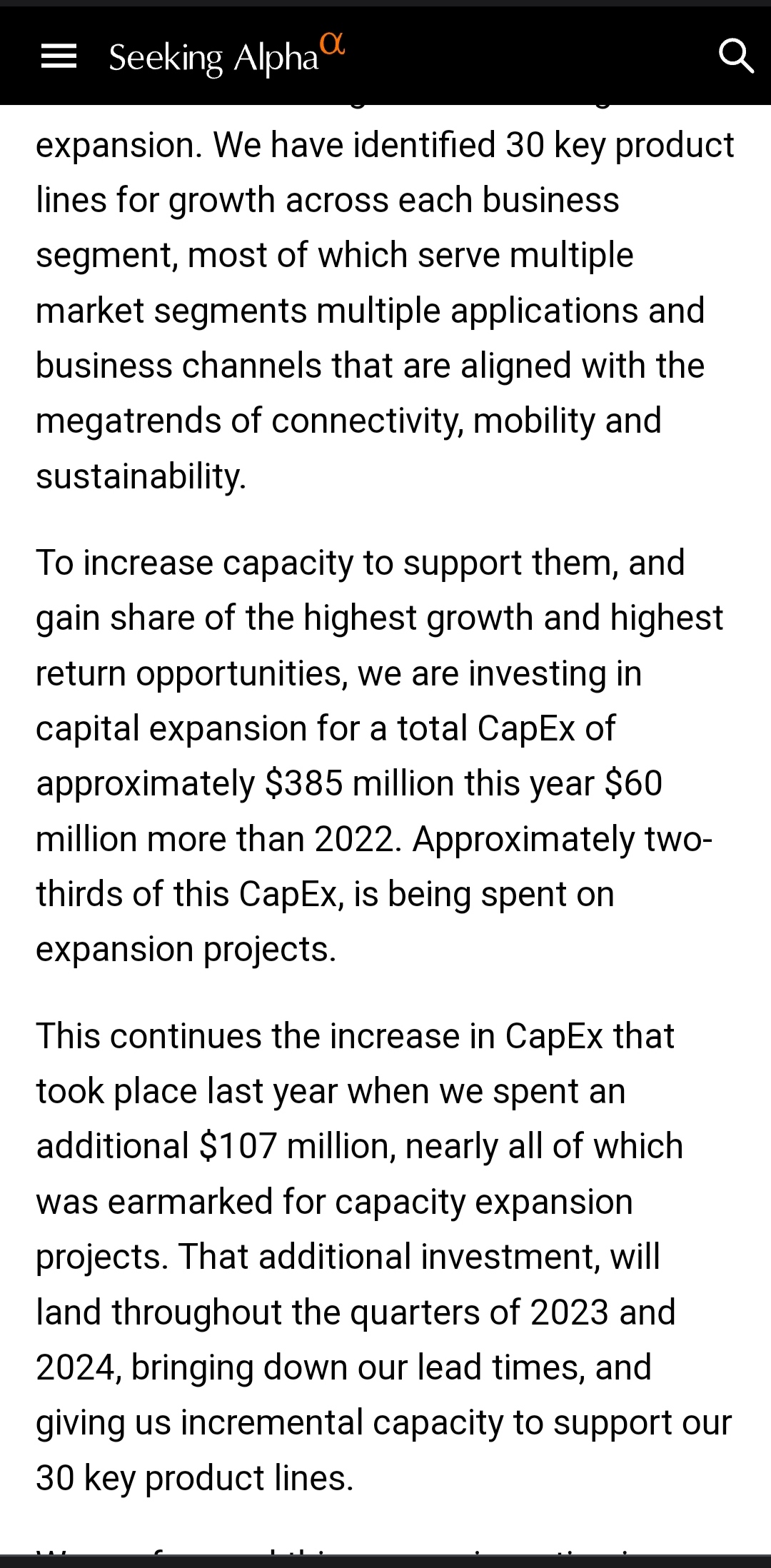

We are focused this year on investing in capacity expansion projects outside of China. Our customers tell us that the value that they see in Vishay being regionally located, the manufacturing footprint as they pursue onshoring or near-shoring efforts. Some of this capacity expansion is already allocated to our established customers, especially for MOSFETs and resistors, which still have long lead times. Some of it is strategically reserved, to serve new and emerging customers that are leaders in driving megatrend-related demand.

This quarter, we put capital to work in a few ways, in fabs located in Germany, Taiwan and Italy, geared primarily toward growth segments of automotive and industrial for our MOSFETs Diodes and OPTO products; new factories in Mexico, for power metal strip resistors and power inductors. Custom magnetics is another part of the inductor portfolio that we invest in. In the Dominican Republic, we have increased the floor space by 50%, to better serve our aerospace defense and medical customers. This increases our overall custom magnetics’ capacity and floor space by 6%.

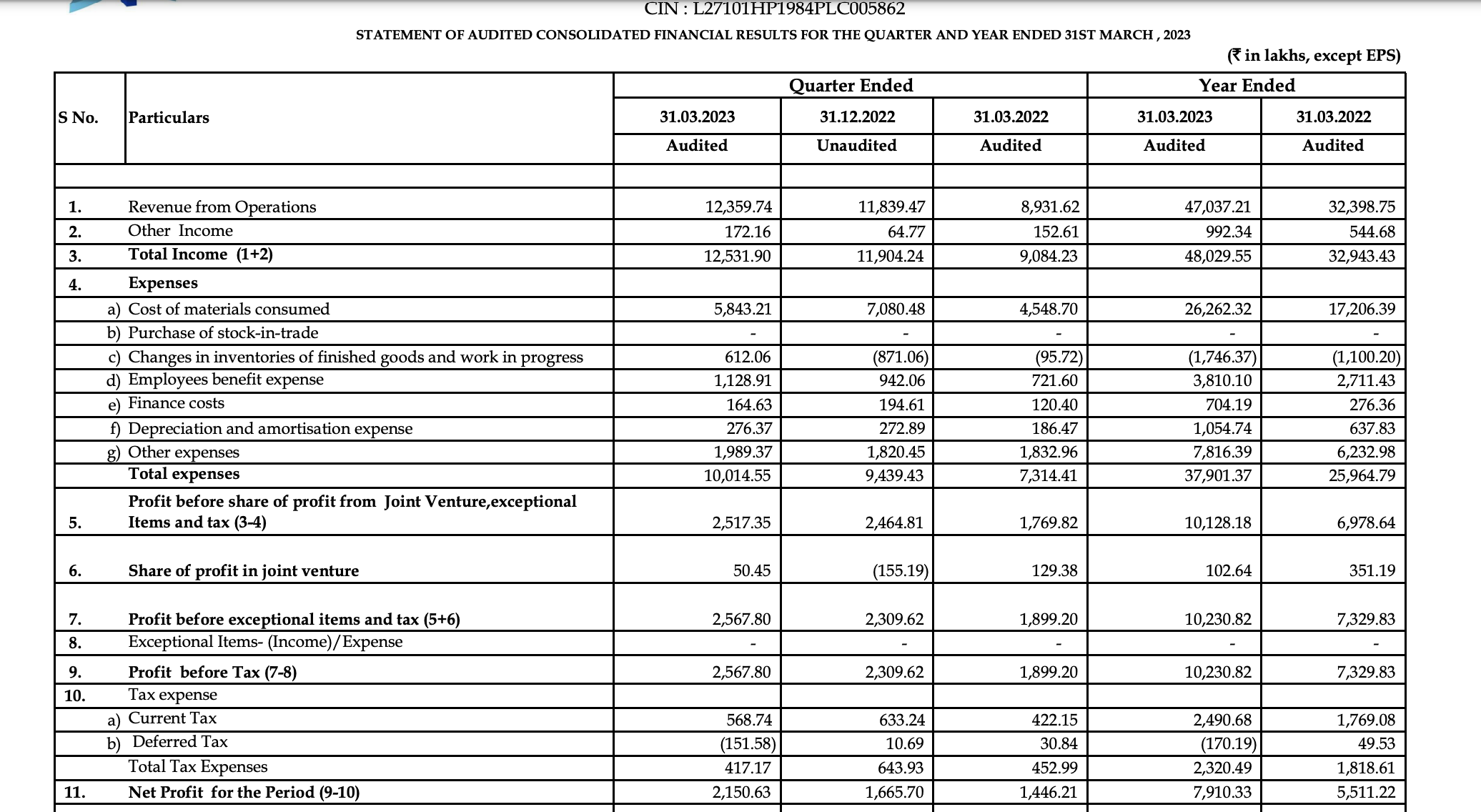

Shivalik’s results are in couple of days will be interesting to see the results

EDIT:

Co is doing first concall in few days. Should be interesting to join the call & ask questions around sustainability of growth & specially cashflows

Disc: invested, biased

34 Likes

After a very long wait, they have come out with a detailed investor presentation.

It shows that they are now willing to reach out to the investor community and institutional investors.

34d4f835-6b0f-40f0-9061-03fa453266ac.pdf (7.9 MB)

The concall scheduled tomorrow is another welcome move.

12 Likes