shivalik maiden concall transcript…

some observations:

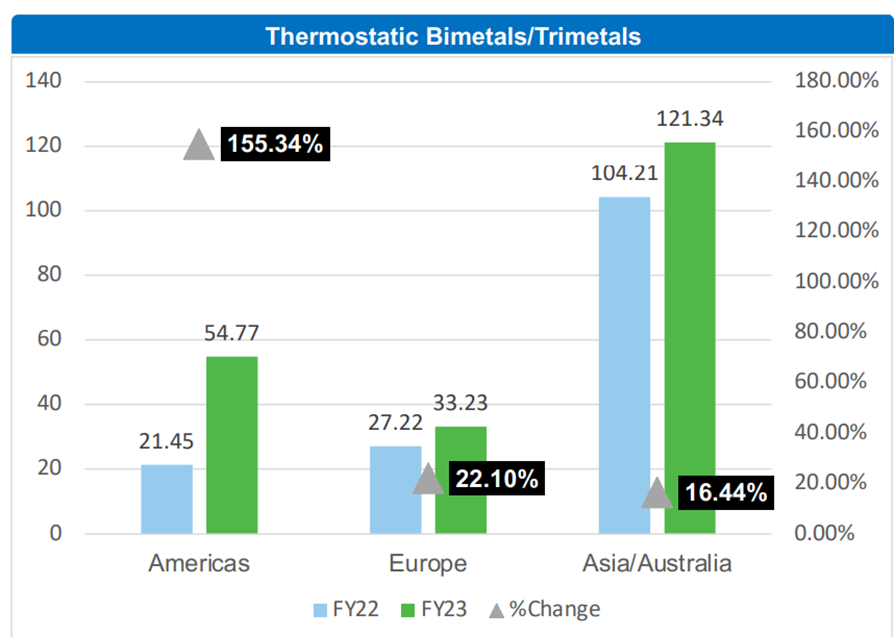

there were mentions in several places about future prospects -

why bimetal is seeing such growth rates and why it will continue

how resistors applications in EV are still small and co is just at tip of iceberg in this

how even in resistors, apart from EVs, prospects are strong in the auto applications…

other applications as smart meters, energy storage etc are in addition to this…

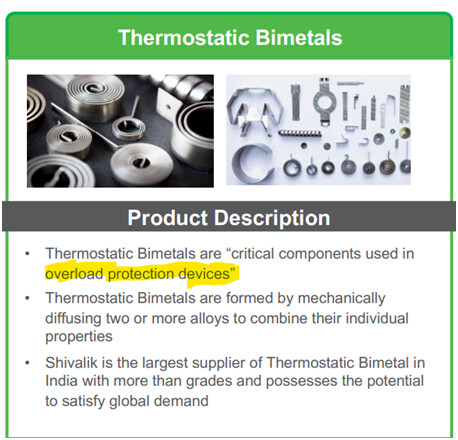

how value is being added in bimetals by increasing the proportion of components vs plain strips…

how contacts is an extension of their product offering as it goes in the same switchgears where their bimetals are supplied…

how contacts can be a large volume business and that while it is a low gpm product today, how they are exploring to increase the margins by reducing material cost by making more value added products here…

how their overall cap util is 35% still…and how increase in volumes is like to atleast maintain margins, if not improve…

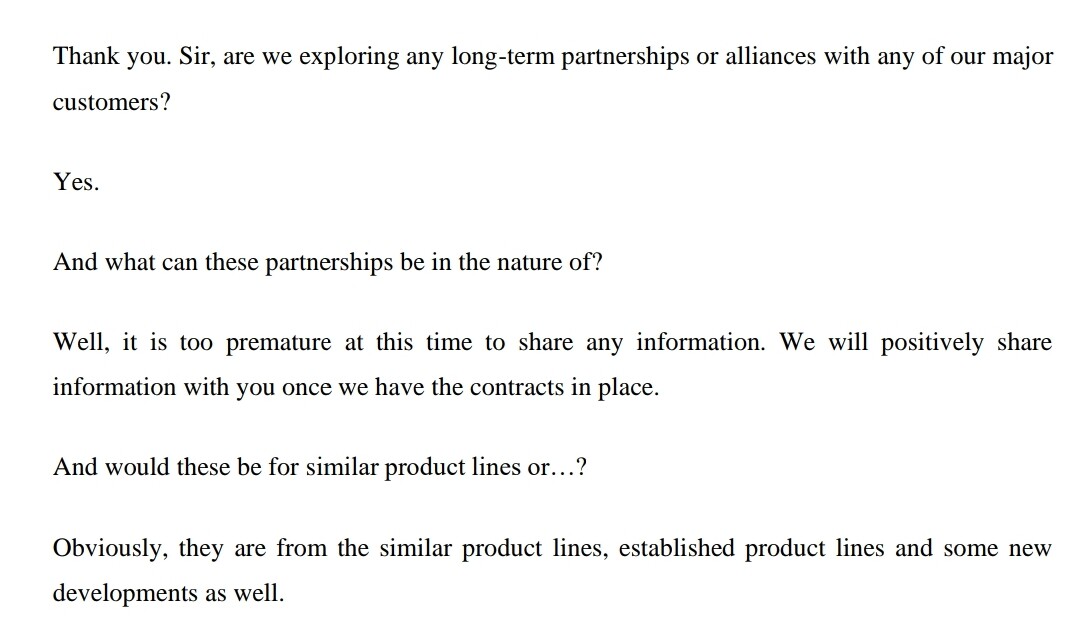

how they have been working with customers for many years, esp in usa, and how things are falling in place for them to take advantage of their efforts and investments going ahead…

how commercial supplies have been started for some components for some customers in some geographies and how they are like to increase penetration in these customers by supplying the same components to more geographies where these customers supply/operate in…

how with the same customers, they are in various stages, including seed stage, testing stage and commercial stage for various products…

to a q as to why they were not affected by semiconductor issue which the auto industry was grappling with till now, one answer was ofcourse the diverse applications of their products but also the fact that it was hinted that now that semi cond issues are behind and auto is like to resume its growth, shivalik will grow further with them.

how is their competitive positioning in india and at global level

how they derive low cost of manufacturing advantage from using machines built by themselves at 1/5th the cost…

how some wc efficiency has been derived from inventory management…