If one looks at the financials for FY22 it would seem that company benefitted from old cheap inventory being recorded at FIFO basis. This led to high P&L margins but cash flow remained poor as the company had to continuously refill the old cheap inventory with the high-priced inventory and hence cash flow was extremely poor (minus Rs 3 crore).

8 Likes

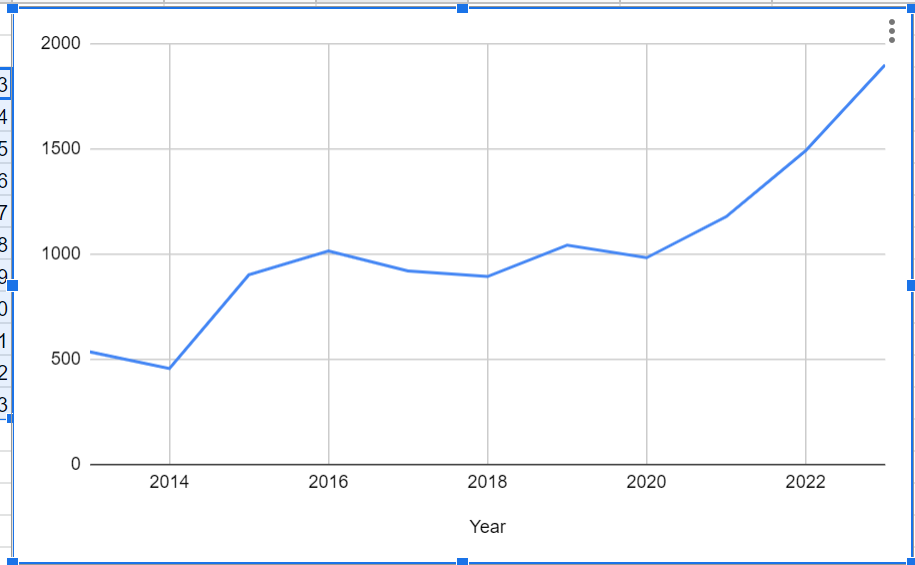

A stab at Shivalik shunt division - Volume/Value/Realization/Copper price co-relation and analysis for longer time frames to find answers/patterns

To understand - whether Shunt realization is structurally moving up or seeing some spikes inline with copper prices

- shunt realizations

- Copper prices trend in last 10 years

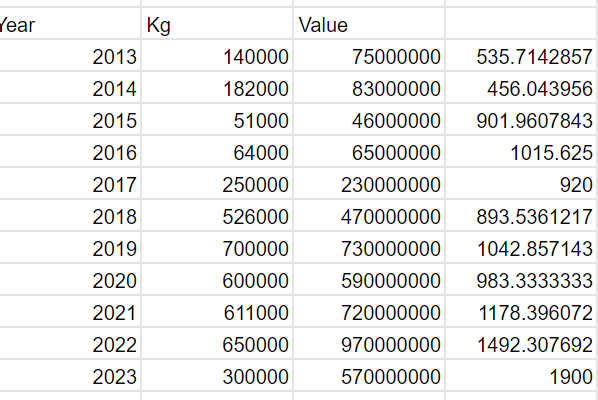

- Above analysis is based on below data - rounded off Shunt volume, value , realization trends for same set of years (only for exports and as per export data at https://tradestat.commerce.gov.in/meidb/com.asp?ie=e )

Key takeaways

-

Kg volume may not be best way to look at Shivalik as directly co-related with end product pricing - answer lies in evolving product performance characteristics and thus value. (low ohmic, tolerance range, temp range/ metal mixes etc) -

-

Shivalik realization have been on uptick over the periods irrespective of Volumes & copper prices. One way to further validate this trend would be as to how end mkt shunt prices have moved historically over years.

-

April 22 onwards Copper prices(4.5$ to 3.2$) have fallen over cliff and stayed low till Oct before bouncing back again in Nov - if there was high priced inventory - should have reflected in last 2 qtrs numbers with some pain - doesn’t seem to be the case yet - either mgmt commentary/numbers. Still better to observe in coming Qtrs.

-

50% of revenue share of lesser glamourous division, Bimetals are doing very well for shivalik (better than shunts in H1 growth) and may continue to surprise with continued client additions etc. Though this division may be more susceptible to RM price movement and impact.

Another stab at quick reality check on Shivalik vs one of key Competition - Isabellenhutte.

Here is the last 3 years export pattern (Volumes in Kg)

Here is shivalik for same duration

note - this may not be comprehensive data and product profile may differ to some extent, idea was to see export trend and volumes over broader periods

some inferences at broad level

Volume trends

- Pre corona Isbl was in range of 25-35000 /mo - now 35000-65000/mo range

- Pre corona shivalik was 25-45000/mo , now 55000 - 110000/mo range.

Both have done well, Shivalik gains are much higher - somewhat aligns to Mgmt claims of being efficient and scalable supplier, mkt share gains.

source - https://www.importyeti.com/supplier/shivalik-bimetal-controls

Above is based on limited data & analysis and could be off/have gaps, feel free to do your own analysis and expand with additional views/points.

Though stock Price action indicates pain/doubts in line with broader mkt small cap under-performance and will test individual conviction.

21 Likes

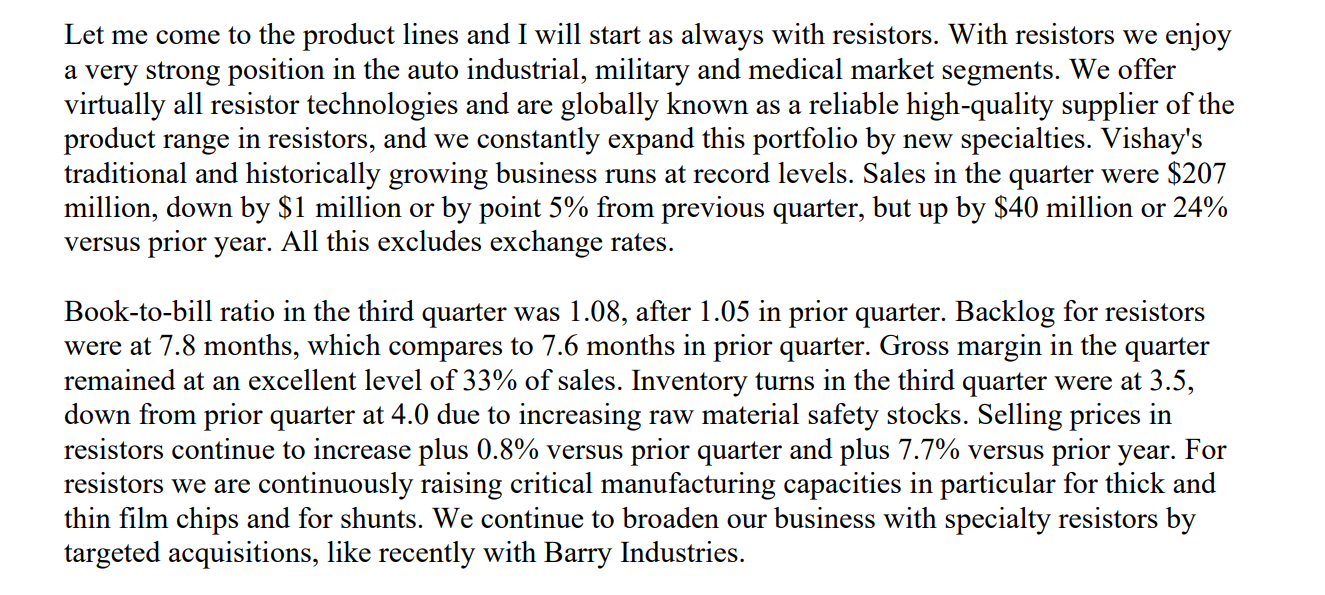

Vishay stock price is near 52 wk high - contrast to US markets - this is in line with their performance delivered+ visibility, highest revenue and margin expansion in Q3(CY) 22 numbers. Stock price reflects market optimism in Vishay future prospects - thus visibility for a sizable demand part for Shivalik.

Q3(CY) nos and commentary - note Shivalik shunts are part of resistor family - Higher book to biil ratio and thus backlog continues

-

End segment demand and inventory - shivalik related segments (energy infra, auto- EV etc) demand stays strong - note the tone of EV and charging infra being a future growth driver (shunt application areas)

-

Is demand slowing down for Vishay end customers/order deferment ? doesn’t seem to be the case.

- Additional infrences - growth has healthy contribution of volume + realization. Vishay seem to be emphasizing growth by volumes, thus sustainability.

good read in current mkt context

27 Likes

On domestic front too there is a huge opportunity. Below are the extracts of a conf call from domestic Electronic System Manufacturer.

“See, India as a country currently a negligible electronic component base. So the

electronic component by and large have to be imported. So what we believe and what

we are witnessing is that once the electronic manufacturing industry in the country

grows as it is growing currently. It will attract investment in assembly and some of

manufacturing of electronic components and I’m not referring to the semiconductor

policy, which is the big policy of the government of India to have the Fab Lab. I’m

talking of the normal components, the passive components like pastors, resistors.

Currently India didn’t have a demand which justifies the setting of a component base.

Now with the growth in the electronic manufacturing which we are witnessing, it is

but natural that the component manufacturing base would come in. As an analogy I

would say, when Maruti came in, there was hardly any automotive component based

in India, but Maruti or Suzuki at that point of time revolutionize the whole state and

today India has a very, very strong automotive component base compared to the best

in the world.

We believe that going forward, so it’s not a short-term sort of a low fruit hanging, it’s

a long harvest. Going forward, the component base would naturally come up in India,

once the electronic manufacturing goes up.”

Thats next phase. The exponential phase would be seen once semiconductor fabs start operation.

26 Likes

Thank you to all forum members for the wonderful discussion in this thread. Thanks also to @sahil_vi for his brilliant research in the stock story thread of SBCL.

I like many believe that this business has superlative potential in the next five years. However, its the current valuation (as has often been the case with me) that repels me.

- I took the last 3-Year median PE (20.00) of SBCL as reference

- Multiplied with the TTM EPS of ₹11.08 which works out to be ₹221.60

- The CMP is ₹361.00 which is 62% above it

While I know this is at best an amateurish method of calculating fair valuation. But I reckon that the 62% gap does state that the stock is overpriced. Thus I will wait.

Disc - Not invested but interested with at least a 3-Year investment horizon

3 Likes

Capex coming up at OEM Levels for EVs.

3W electrification is almost at 50% level.

| Company | Investment amount in cr |

|---|---|

| Tata Motors - PV | 16,000 |

| Suzuki Motor Gujarat | 10,400 |

| Mahindra & Mahindra | 10,000 |

| Ola Electric | 3,500 |

| Simple Energy | 2,500 |

| Hero Electric | 1,200 |

| Okinawa | 1,000 |

| TVS Motors | 1,000 |

| Tube Investments | 1,000 |

| Bajaj Auto | 1,000 |

| Ampere Electric | 700 |

| Ather Energy | 330 |

| Total | 48,630 |

Source : ICICI Security research - “Domestic Themes to hog the limelight in CY23”

17 Likes

We all know how well connected Adani group is with the central government projects and recently there is a news that Adani transmission has incorporated an arm to undertake smart meter business(links below). Although smart meter related news is within the market for many years but now it seems certain that it going to take off in full throttle and Shivalik would be the beneficiary.

In short, it seems like that both the EV and smart meter business is going to takeoff in upcoming years. This is indeed very good signs for Shivalik as this two business stream would contribute the maximum growth for the company.

19 Likes

Adding the chart to the great fundamental thread.

The earlier resistance at 370-380 became a support. Then there was a inverted head and shoulders breakdown followed by a sharp reversal. The volume impressions are very large on upward direction so this looks like a positive structure so far. IF 420 odd level is crossed then it would be a good sign of strength, crossing 450 will be a confirmation.

Discl: Invested

17 Likes

I am clueless why people are claiming that it is the only manufacturer of Shunt resistors. You can get many manufacturer after checking on google. Take a look at Indiamart, one guy is selling a resistor for 20 rs.

Now imagine what kind of market size these shunt resistors would be having.

These shunt resistors will be used in BMS. Now a BMS hardly cost 2000 Rs, lets assume half of the cost would be resistor (1000 Rs). Now the lifecycle of resistor should be of multiple years.

Again imagine what kind of market size these products would have?

Similarly for Bimetals

1 Like

Please read the full thread. It will help. It is not just shunt it is the ultra low ohmic shunt which is the forte of Shivalik.

You will find many data points here.

Regards,

Raj

6 Likes

Discussion with domestic client of Shivalik from auto industry

Shunt helps measure current, both low and high amperage

Shunt is an intrusive tech- you need to put it in and measure the throb. There is non intrusive tech - hall effect sensor. Advantage of shunt Is lower cost and higher speed (Speed at which u want to measure current bandwidth) - Need high speed sensing for short circuit currents

In hall current sensor- Inaccuracy is a problem

Shunt has problem of thermal dissipation – if current flowing through go very high, this dissipates heat which could affect overall casing and architecture and cause other parts to get heated

Bigger battery or high performance battery – could go for hall current sensor. It is 3-4x more expensive than shunts however

This client will stick with shunt for now though

Use a low ohmic shunt resistor … for high current measurement impact- temp impact should be minimal to ensure drift away is lower.

Besides these 2, there are no other technology in the works.

Use Shivalik shunt resistor. Have 2 more vendors but their cost is more expensive. Also work with Vishay. Shivalik offer same specifications… peers are 3-4x more costly

Primary vendor- Shivalik, other 2 are secondary

No reliability issue faced with Shivalik in the past

BMS - Shunt costs is 8 rupees x 2 No of shunts in BMS (There can be shunt requirement outside of BMS as well)

Does product % of overall cost matter when it comes to negotiating on pricing with part supplier? OEM will attack the bigger cost Products first, but over time will squeeze the other vendors as well

59 Likes

Thanks Anirudh. Apart from BMS, shunt or Bimetal has any other use in auto?

second, don’t you think market size for the product is too small?

1 Like

Very Good insights. The ohmic value and temperature coefficient (tolerance) are two critical parameters of the shunts. Shunts are used not only in BMS but almost all electronic circuits use SMD registers, so market for Shivalik products is not dependent on BMS only but also from overall electronics manufacturing worldwide.

21 Likes

The subsidiaries are dragging the performance of standalone down. They work at low gross margin.

Also, the JV company Innovative Clad Solutions have turned loss making in this quarter. The company has posted a loss of 1.55cr this quarter compared to profit of 1.27cr in second quarter of FY23.

The company was profitable last year according to last year’s annual report -

Shivalik hold 16.01% in the company.

Google search for Innovative Clad Solutions throws the following page -

But the website is inoperative -

Indiamart throws the following page, which is little more descriptive -

14 Likes

Seeing the latest Q3 results, thermostatic bimetal/trimetal strips have been the ultimate growth driver for the company and have grown at 41% YoY faster than shunt resistors which has grown by 25%.

driven mainly by addition of new clients.

The following is a list of clients they have supplied these bimetal/trimetal parts to from December 2022 till now -

Some new companies can be seen being added. Will update if i get names for any new clients.

34 Likes

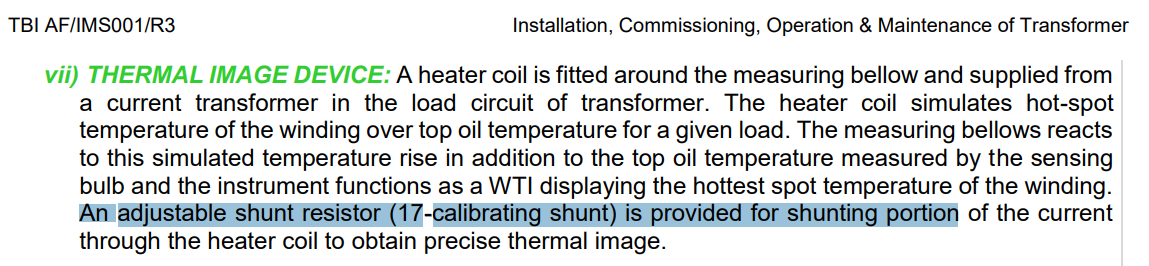

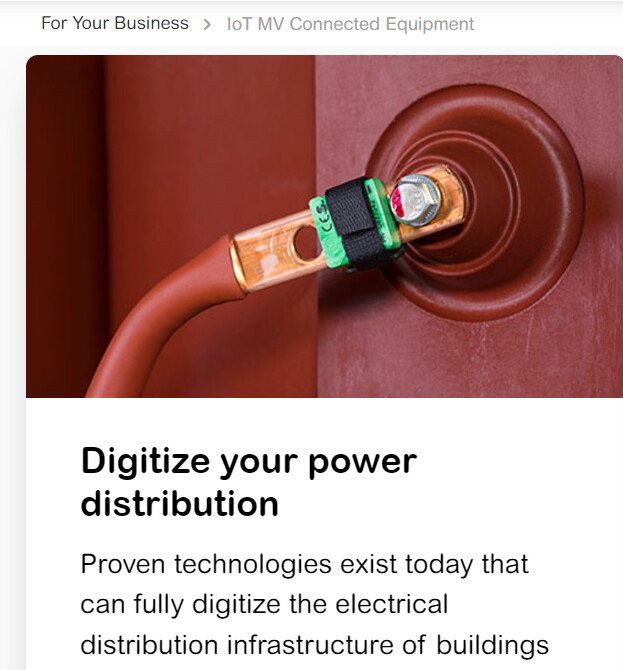

Uses cases of Shunt resistors are often associated with Auto/Smart meter etc, here is one of many lesser talked about use case

A quick google search will tell the transformer shortages worldwide - which is an essential critical path item in mega electrical infra upgrade that most countries are carrying out.

Here is how transformers are evolving ( IoT enabled, sensors and preventive care etc)

shnieder Q3 deck has focus on these wins

Here is a screenshot form Their transformer manual

IoT universe is key focus for Schnieder and many large organizations - Circuit breaker, sensors etc is essential to this digitization

Schneider is a known long time customer for Shivalik.

Point being, Shunt/Bimetal usage are quite vast, Opportunities should continue to evolve as EV, IoT and other Digital tech adoption scales.

While Shivalik hands seem full at this point, Forward integration in IoT sensor universe (own or via partnership) could see a good extension of TAM.

18 Likes

I was going through the list of exhibitors at Elecrama 2023. Exhibitors list – ELECRAMA.

Shivalik Bimetal is an exhibitor at Stall -H12J3. If someone from the community is around and can attend, would give more insights. They have listed for Switchgear and Controlgear and Other Products category.

11 Likes

Solenoids are common for valve control.

2 Likes

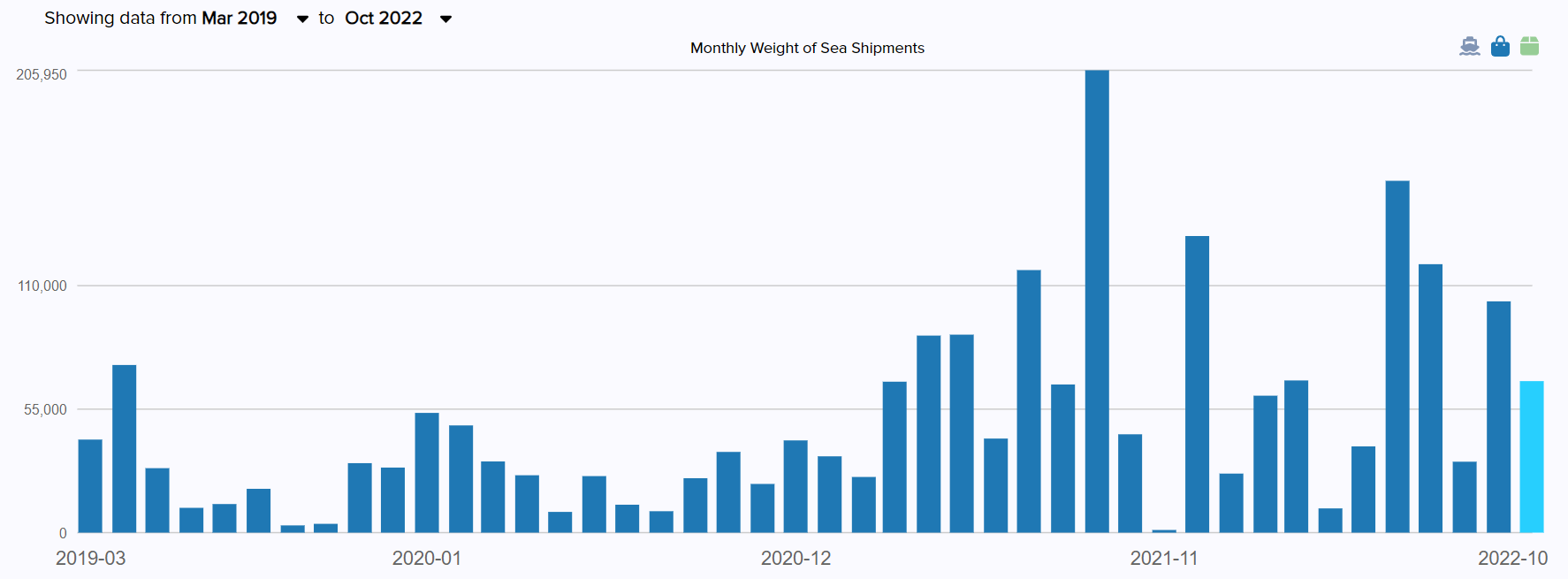

One key watch out for Shivalik has been - Non Vishay Dale customer wins/supplies in USA in Shunt division. We have seen many names in bimetal space but not much action is Shunt space(beside a small qty to a mktplace).

Feb exports show some interesting development here - sizable shipment to a new customer, supply volume is similar to Vishay dale typical shipment hence not small.

Now https://davidccook.org/ is a non profit education setup hence difficult to say the quality of win or sustainability of future supplies. Difficult to see direct co-relation of shunts demand with education focused non profit inst. However lets see if future supplies show up as this volume isn’t small / pilot type qty.

We also don’t know if Vishay and Shivalik arrangement/contract is now at a stage where Shivalik gets room to supply broader universe(assuming exclusivity element on original setup with Vishay), this supply is very positive sign though on future possibilities.

Thoughts welcome on above if anyone has more info or can connect any dots, this aspect is key for shivalik to scale shunt volumes in USA geo, though they seem to be doing quite well outside US.

Another small update is that Shunt monthly export volume growth which was kind of nothing to talk about/negative in last qtr Q3 at 127000 Kg(given higher base in Q3 22 = 198000 Kg during shipment craziness and stocking times, we saw large shipments than usual to Vishay in those times) is inching back upwards in volumes per recent month shipments - though would be worth to wait and see this updated in Min of commerce site soon. However not as many Bimetal volumes in shipments in recent months - unless this is the lever management is consciously using to shuffle capacities to keep utilization high.( Bimetal logically would be slightly lower GM as was case in Q3).

One key inference is that Shivalik has delivered decent growth even with Shunt destocking(for lack of better word given normalized shipment scenario) in Q3, demonstrates management having multiple growth levers that they pulled effectively to deliver a respectable Q3. Worth noting that Realization and inventory losses risks were put to test as well in Q3.

If above plays out - will know soon if we are again looking at good Q4 (Given high expectations mkt will look for QoQ growth not just strong YoY as well GM).

Pl note above is based on a very high level assessment/tracking and could be off, do apply own discretion.

Invested

28 Likes