Company has come out with perhaps its most detailed investor presentation & communication.

This is for some physical meetings co will do in mumbai in next few days.

Some key takeaways from the presentation:

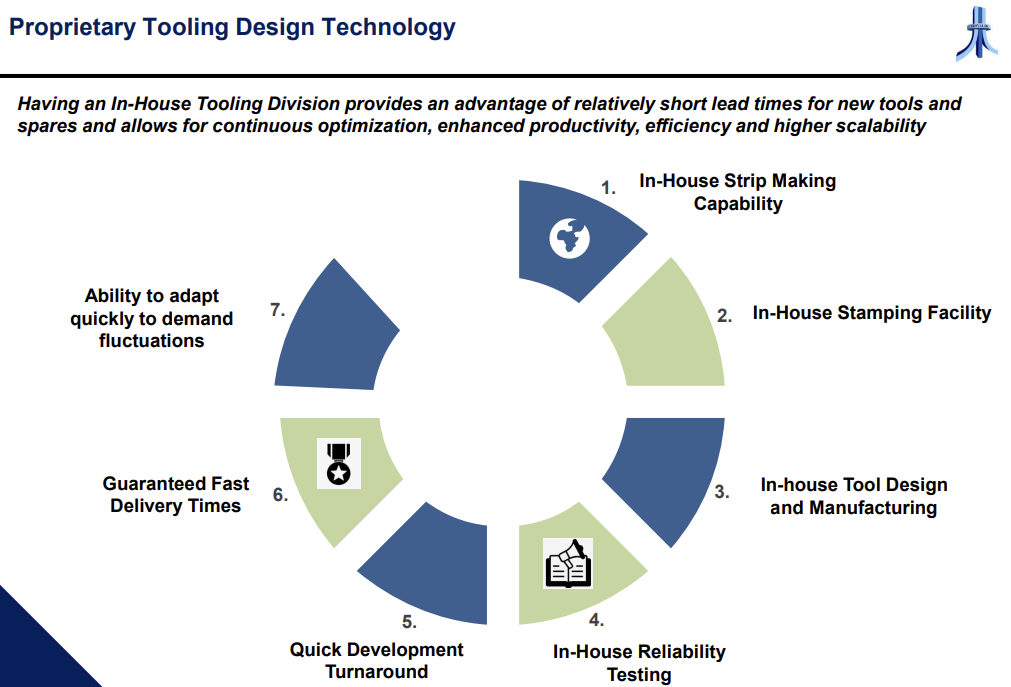

- Company has clearly outlined its competitive advantages - Capabilities across design, development, testing, validation, manufacturing and delivery. Focus on R&D for improvement in product performance, cost, reliability & quality. Some of the competitive advantages like “In-house Tool Design & Manufacturing” which we had called out in the stock story are also featured in the presentation

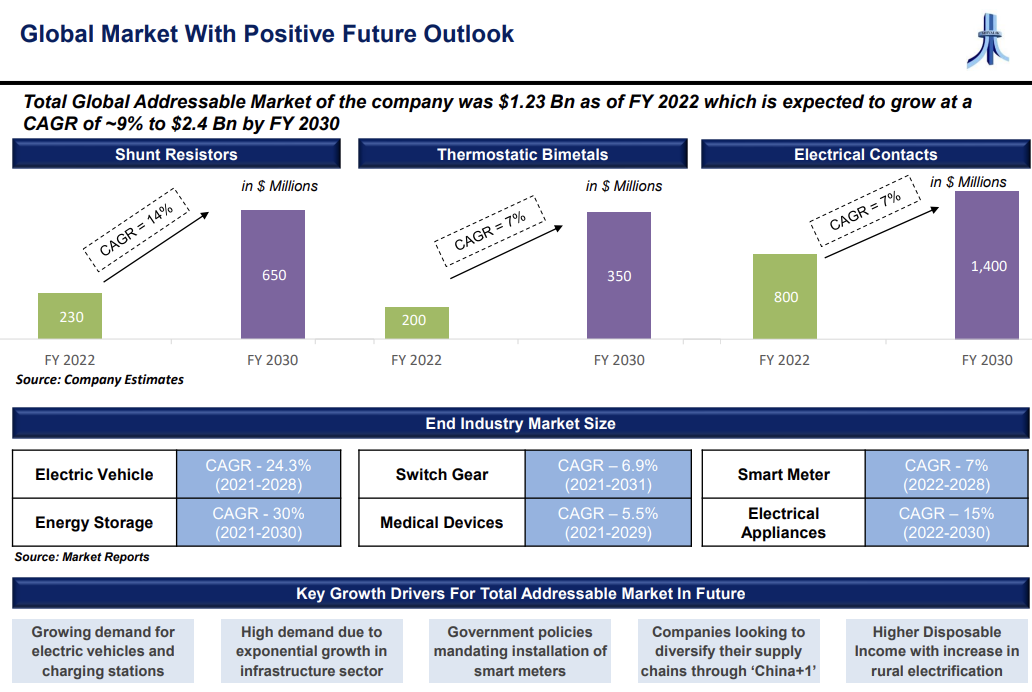

- TAM for shivalik products is outlined. ~2000cr for Shunts, ~1600cr for bimetals, ~6000cr for electrical contacts (i dont think we have focused on this much). Shunts market could expand ~3x in next 8 years led by demand for EVs & Energy storage solutions

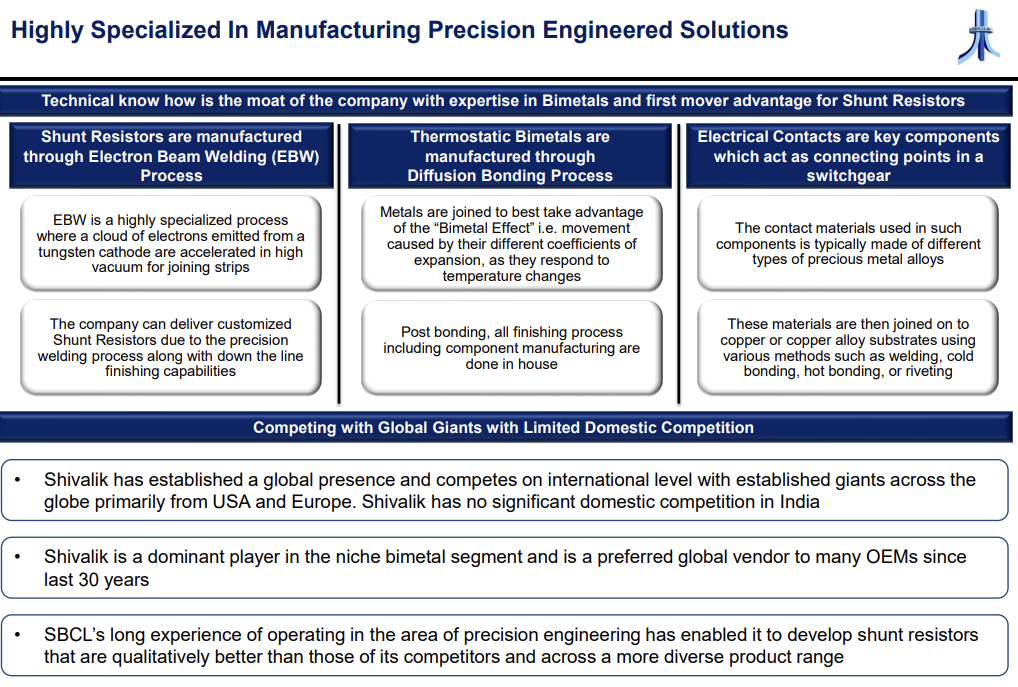

- Shivalik’s precision engineering experience has allowed them to develop shunt resistors

that are qualitatively better than those of its competitors. Lack of any domestic competition is called out. Technical knowhow in metal joining is called out as the moat of the company.

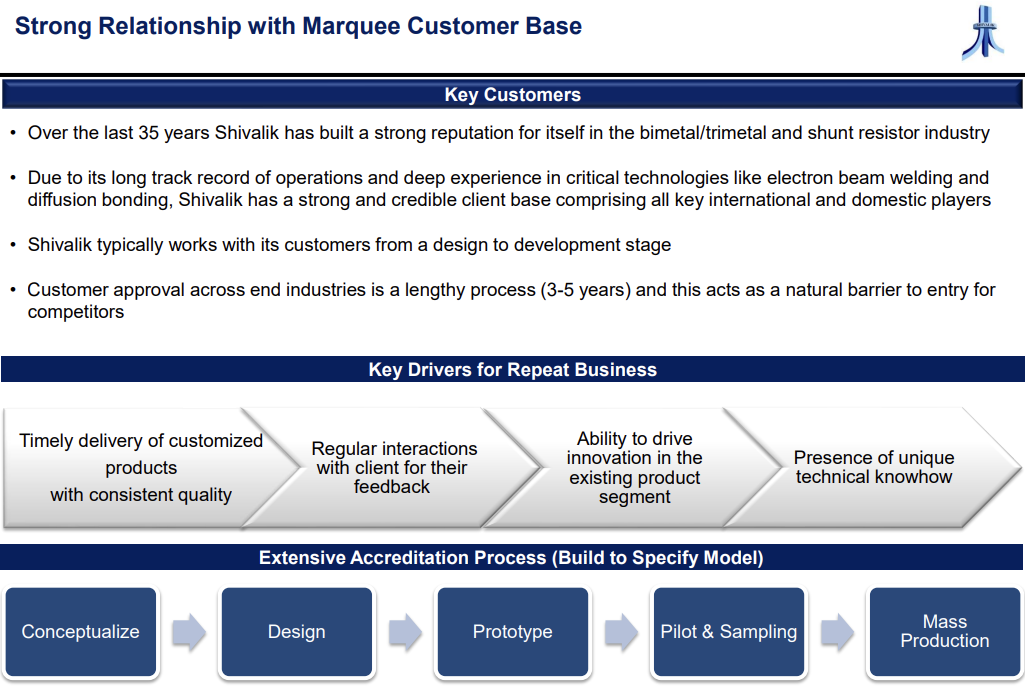

- Client relationship is called out as a key source of competitive advantage. Shivalik co-designs these shunts custom for its clients & the full process of conceptualizing, designing, prototyping, piloting & sampling & mass production can take 3-5 years. Shivalik also calls out that it is preferred supplier for many cos like Siemens, Legrand, Schneider.

- Perhaps the biggest incremental information addition has been the quantification of just how much revenue the new plants can add to shivalik. The total revenue potential of all 3 plants (including 1 old plant & 2 new plants) is called out to be 1600 cr rupees. Looks like large part of capex is done for Plant 1&2. Perhaps some capex for plant 3 might be required. Only capex requirement called out in slide is 20-30 cr for debottlenecking in next 3 years

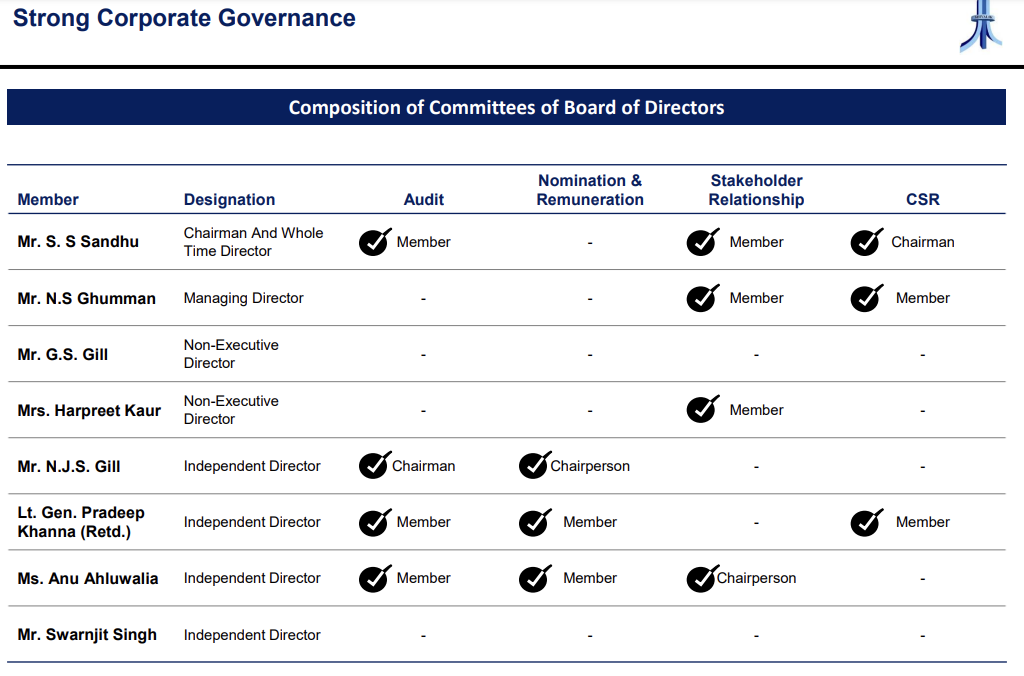

- Another interesting callout is that the remuneration committee doesnt have any sandhus or ghummans on it, only independent directors

- One thing that i personally found interesting is that only 11% of revenue comes from eletrical contacts but it is the largest market by far. 3x larger than bimetals & shunts. Why then has shivalik not chosen to go after it aggressively (even in expanded revenue potential this is hardly 300 cr, (19% of eventual projected revenue) Needs a bit more digging into. Perhaps lower margin product? More commoditized? higher competition? (Only 11% of revenue currently)

Disclaimer: Same as before.

If anyone is planning to attend the in person conference please reach out to me, we could discuss the questions which we can ask the management in order to make best use of the opportunity.