Many good and dear friends have written about the business above. Certainly fantastic growth over the years / decades, which few firms can match. It is highly likely that many of those who have posted have enjoyed the substantial run up in prices over the past many years.

I want to direct my post to those uninvested and part-time investors but keen to put their savings to work fastest to generate returns. They are likely to get carried away and set unrealistic expectations on how well the stock will do hereon. Not because what’s painted above is hypnotizing (which it is not); but because it is likely to lure him to think any price is good enough for this wonderful business. There is hardly any discussion on the intrinsic value of the company (about 3 - 4 out of 282 posts above allude to it). Market prices fluctuate. What is ~ Rs 700 today can go down to Rs 500 or go up to Rs 1000 in short time. For someone who bought it at say Rs 200 or so, the down fluctuation is bearable than for someone who buys it today. And if you hear only from those who have made it big here; it is nearly impossible not to get swayed to the upside and pay little attention to the downside.

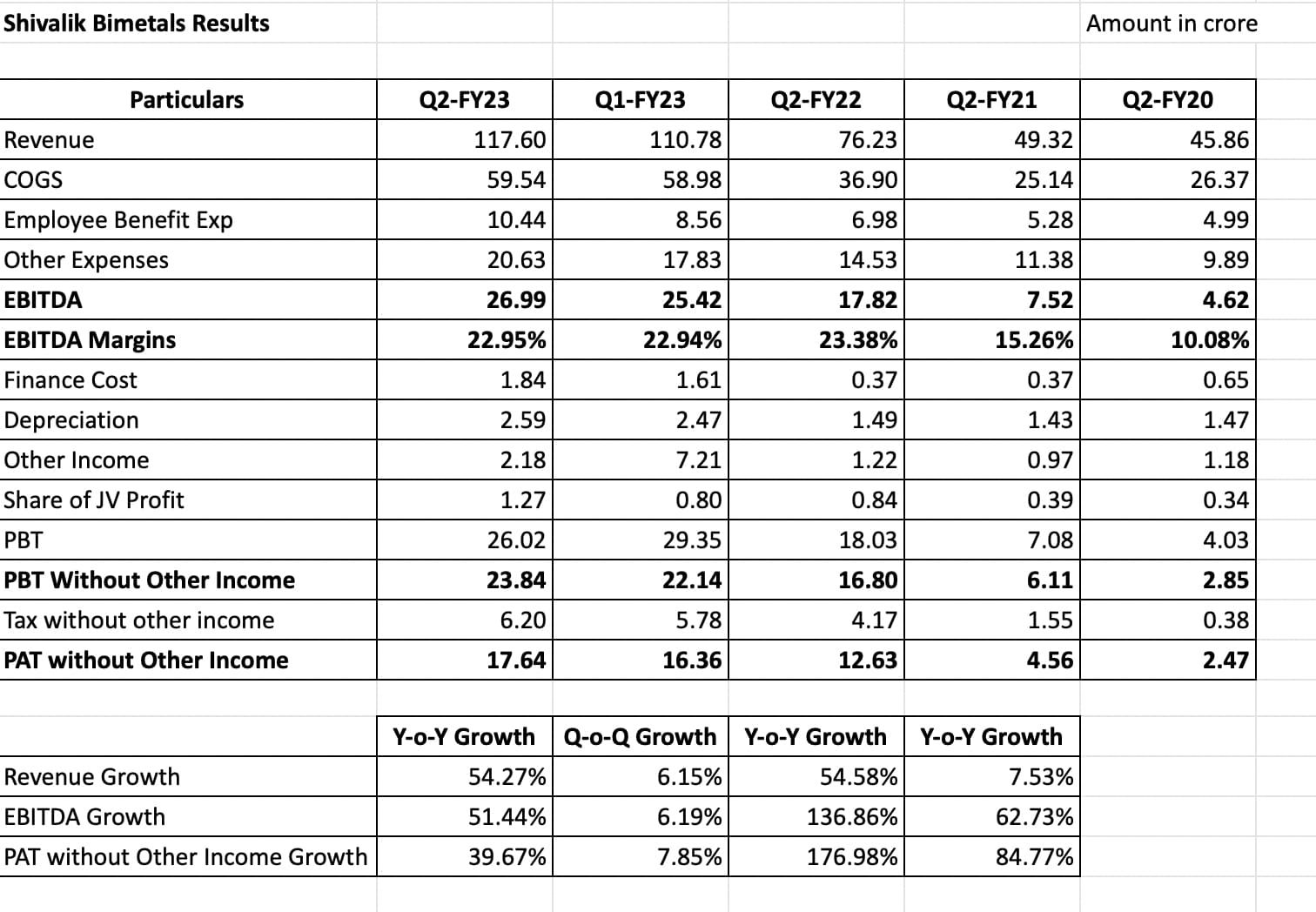

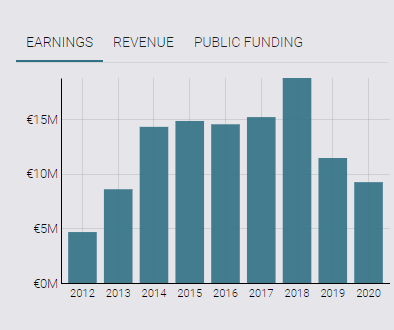

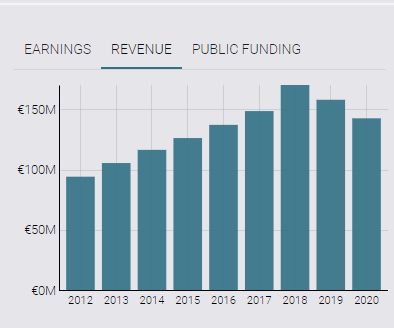

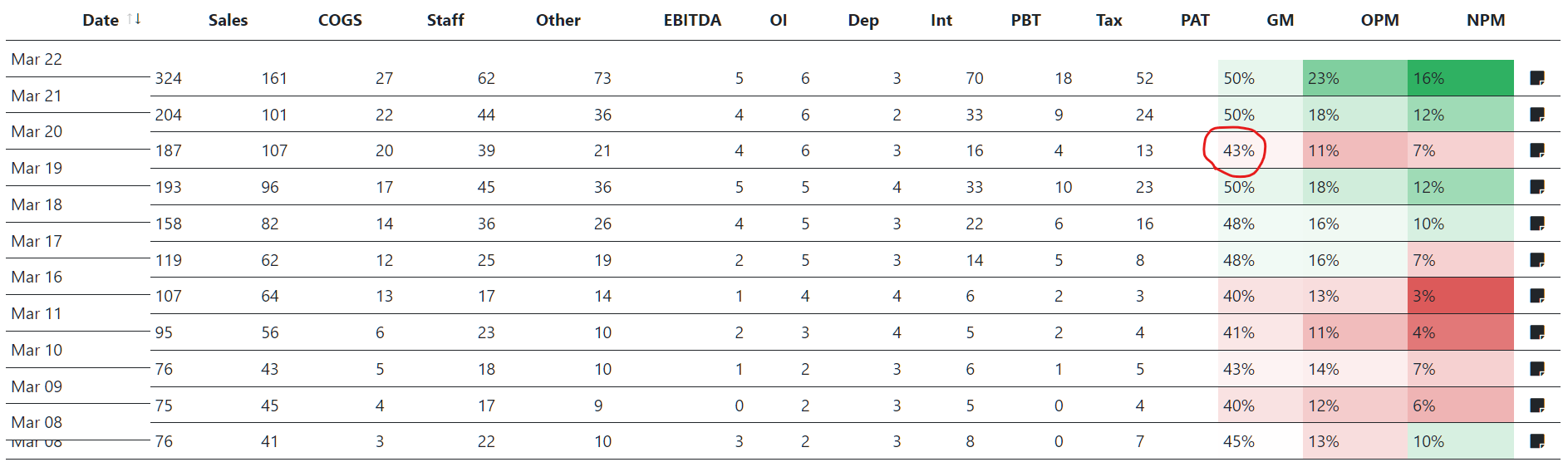

To put some balance to the price side of the discussion; consider this - that the business has grown revenues roughly by about 5 times and earnings by about 13 times in the past 12 - 13 years. During the same period the market price has grown more than 70 times*. The business thus has become substantially expensive now than those who had the foresight to buy it when it was much cheaper.

Ask yourselves, can earnings over the long run keep growing much faster than revenues? Can prices keep growing much faster than earnings? If so ask why and if not then imagine your downside risks vividly ![]()

Maybe the business will really explode and you will make lots of money as prices rise higher; but it is more maybe that the price today factors much of all that explosion.

*From Annual Reports / BSE (adjusted price without dividends), and Q1 FY 23 earnings extrapolated linearly to FY 23