ELEVATOR PITCH

-

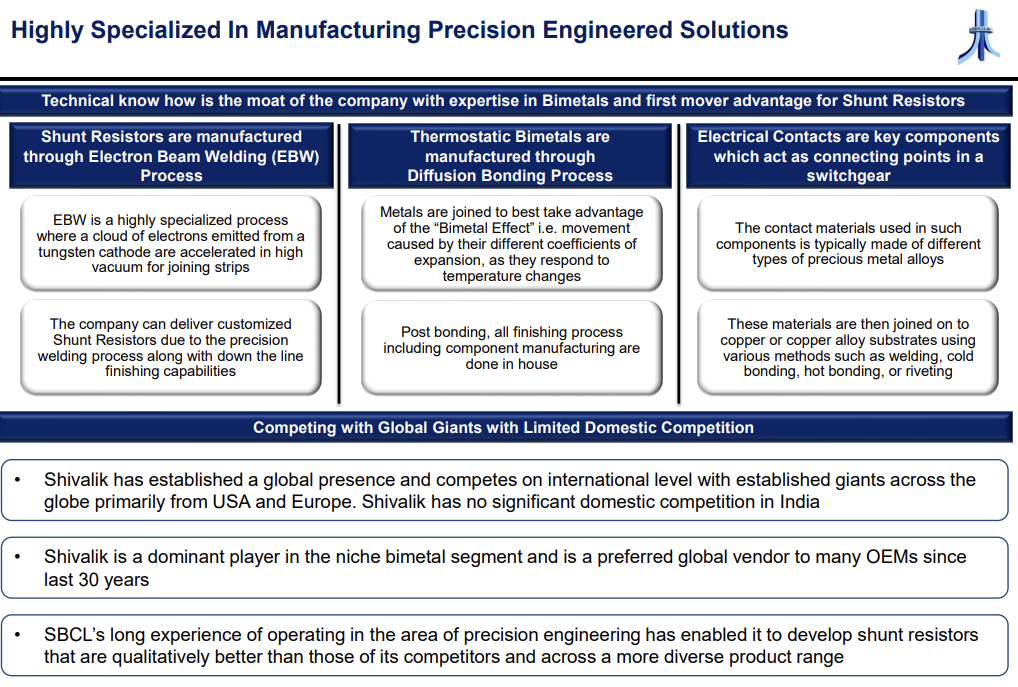

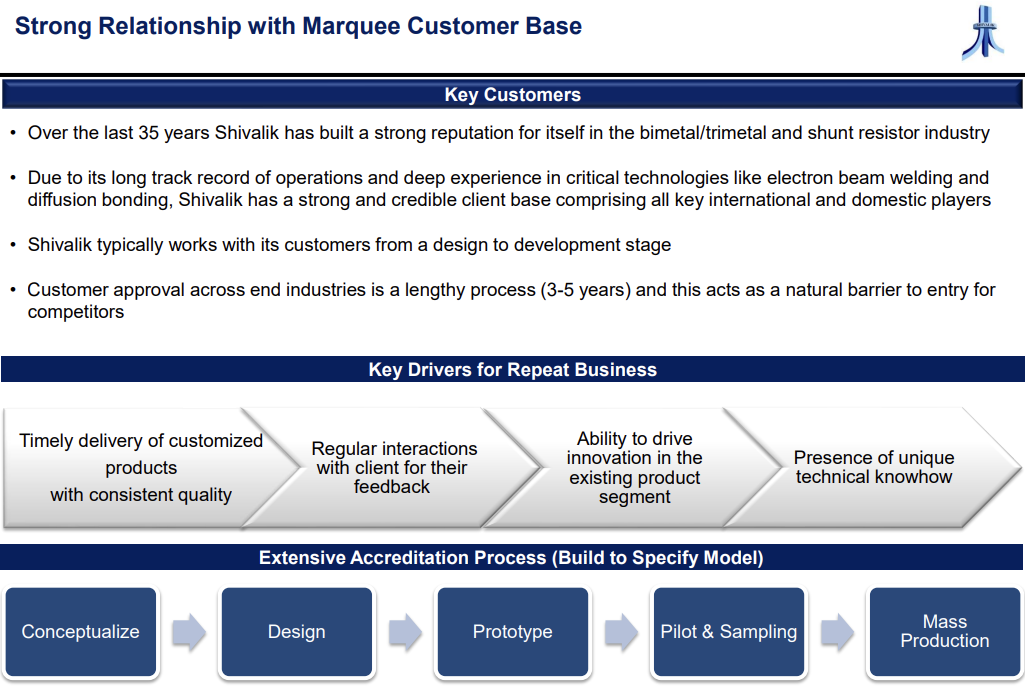

One of the Longest Value Chain among Peers: SBCL is known for the fastest response times on custom projects for Clients owing to it’s superior control/process automation grip on Shunts value chain (unique to SBCL, and unlike other shunts majors) - from RM inventory, Bimetals alloy expertise, to custom design to moulds/tooling, custom in-process inspection/QA automation to fully automated EBW manufacturing process – fine-tuned for specific customer projects. 75% of SBCL business is custom designed, giving customers much-needed flexibility/control.

-

Durable Dominance in a Market with Tailwinds: SBCL’s ultra low-ohmic shunts and bimetals business is a simple linear business (not many variables, and most variables under control) with limited competition. With it’s demonstrated ability to deliver on first-of-its-kind customer requirements ahead of more established peers and at lower cost (recent SMD Shunts EU 5G rollout requirements, e.g.) SBCL is uniquely positioned, today. Quite a few of SBCL products have thus become the Reference industry standard. Reference standard implies the customer asks new vendors wanting to participate to first match SBCL product specifications.

-

Formidable Global Leadership Challenger: IsabellenHuette has been for many years now the undisputed leader in automotive shunts industry with ~50% market share, Rohm, Panasonic, (?) being other leading players. As per Industry scuttlebutt SBCL enjoys global cost leadership, and in just 5 years is catching up fast with a 10-15% market share already. SBCL Management indicates they have the largest shunts capacity today with its factories running 3 shifts 24x7 operations, and another 60% expansion underway (based on 3-4 year customer forecasts) to address next 2-3 year requirements. SBCL is also delivering at 4-20 weeks max lead-times (half that of some shunts majors). With EV shunts market at an inflection point (and 8-16x requirements per EV than conventional ICE), SBCL finds itself in a sweet spot and could prove a formidable challenger as it scales up strongly in next few years.

-

Customer-Driven Innovation Curve: Given SBCL’s superior metallurgy skills, ability to completely custom-design-build fully automated EBW in-process inspection/machinery, and cost leadership SBCL is often pushed by MNC customer majors to innovate and deliver complex components for their specific product roadmaps. This has led to deeper penetration and major scale up in SBCL customer relationships, as can be noticed (from recent export data) with a European switchgear major.

-

Rare high EPA/Sales Small Business: SBCL has been growing Sales over last 5 years at ~20% CAGR with EBIT and PAT north of 30% CAGR. 5 Year Rolling Incremental ROIIC today stands at ~65%. EBIT/Invested Capital has reached north of 30%. Consequently Economic Profit Added (EPA) has been accelerating (over last 3 years from 3% to 8%) to 12% of Sales today which is special to see in any emerging small business. Highly profitable mature businesses exhibit double digit EPA/Sales. If SBCL continues to execute well in the next 3-5 years and harnesses the opportunities before it, there is great headroom to continue to invest higher capital at high rates of return for many more years.

CURRENT MARKET/INDUSTRY TRENDS

-

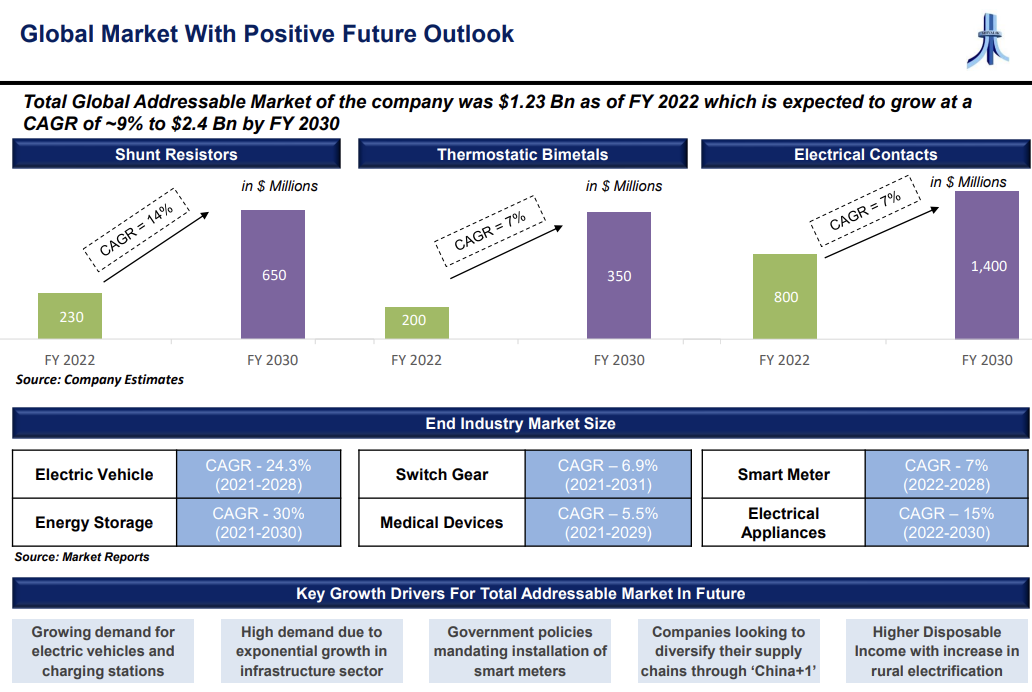

SBCL current sense shunts primarily address the Internal Combustion Engine (ICE) Battery Management System (BMS) requirements today, and account for ~10% of low-ohmic shunts global market share, currently. The EV market in India is likely to increase at a CAGR of 36% until 2026 as per this IESA report. Additionally, the EV battery market is forecasted to grow at a 30% CAGR during the same period. As per SBCL Management, EV applications typically require 8x-16x current sense shunts, as compared to ICE BMS requirements.

-

Another large opportunity for SBCL shunts is the move from legacy electric meters to smart meters. The global smart electric meter market size is projected to reach USD 36.00 billion by 2028, exhibiting a CAGR of 8.1% during the forecast period. Domestically, Smart Meter National Programme (SMNP) aims to replace 25Cr conventional meters with smart meters in India. As per this National Smart Grid Mission update though, only 5Mn (of the sanctioned 11.3Mn) Smart Meters have been deployed in India under various schemes/states, as of 30th September 2022.

-

SBCL Next-generation thermostatic bimetal/trimetal strips serve Switchgear markets primarily, and account for ~16% global bimetals market share, currently. The Global switchgear market is expected to grow at a CAGR of 5.7%, from an estimated USD 90.9 billion in 2022 to USD 120.1 billion by 2027 (Switchgear Market report). As per Management, SBCL is currently gaining share from incumbents and likely to reach ~22% Bimetals/Trimetals global market share in in the medium term.

-

India Switchgear Market is projected to grow at a higher rates. CAGR of 7.17% during 2021-27F (6wresearch report); CAGR of 15% (TechSci Report). Electrification programs running across the country and the development of transmission and distribution networks are fuelling Indian switchgear growth. Further the infrastructure development schemes initiated by the Indian government, like Smart Cities, Make in India, Deen Dayal Upadhyaya Gram Jyoti Yojana, Green energy corridor, among others, are contributing significantly to the growth of the switchgear market in India.

BARRIERS TO ENTRY

-

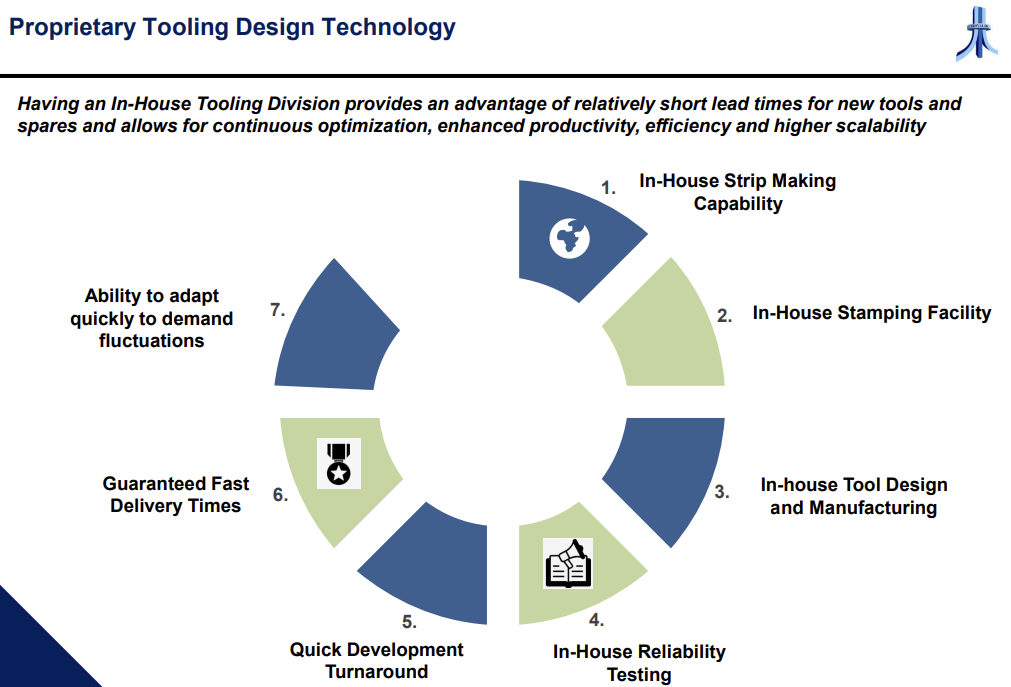

Unbeatable Technology/Capex Investment (?): SBCL has a large number of Electron-Beam Welding (EBW) machines today. Each machine would cost ~Rs 20 Cr plus, at today’s prices. Over the last many years SBCL has greatly enhanced it’s in-house expertise for custom design & development of EBW machines, and automated custom in-process inspection/testing procedures, fine-tuned to customer needs (in partnership with EBW equipment manufacturers and 3rd party developers).

-

Superior Metallurgy/EBW Knowledge: The effectiveness of electron beam welding depends on many factors. The most important are the physical properties of the materials to be welded, especially the ease with which they can be melted or vapourised under low-pressure conditions. Probably the biggest barrier to entry is thus through SBCL’s in-house metallurgy (bi-metal/tri-metal) knowledge base honed over last 30+years coupled with EBW (Electron-beam welding) equipment/process know-how. SBCL Management has indicated the JV since 2008 with Aperam (parent Arcelor Mittal vintage) has had a significant role.

-

Niche Market: SBCL operates in what is still, a niche global market (~2500 Cr). That Clients like Vishay, Riedon Inc, Robertshaw Electronic Controls despite their strong $Bn balance sheets are unwilling and/or unable to get into manufacturing shunts (at scale) works well for SBCL.

-

Long Gestation period: Specially on auto side of business, it takes 3-5 years to break into new business with an auto OEM, even with the right certifications. SBCL has been working with many such clients over last many years.

-

Client Stickiness is huge with OEMs resistant to change what already works well for the supply chain, and is a very small fraction of their product costing. Besides the fact that globally very few players are able to meet the quality deliverables.

BUSINESS MODEL

-

75% of Products sold by SBCL are custom-designed for its customers. Major customers also invest in the Tooling/Moulds designed/used specifically for the custom products. For bulk of the customers Repeat Business/Customer Lock-In is thus baked-in, in SBCL Business Model (till the time Customer continues to sell that product).

-

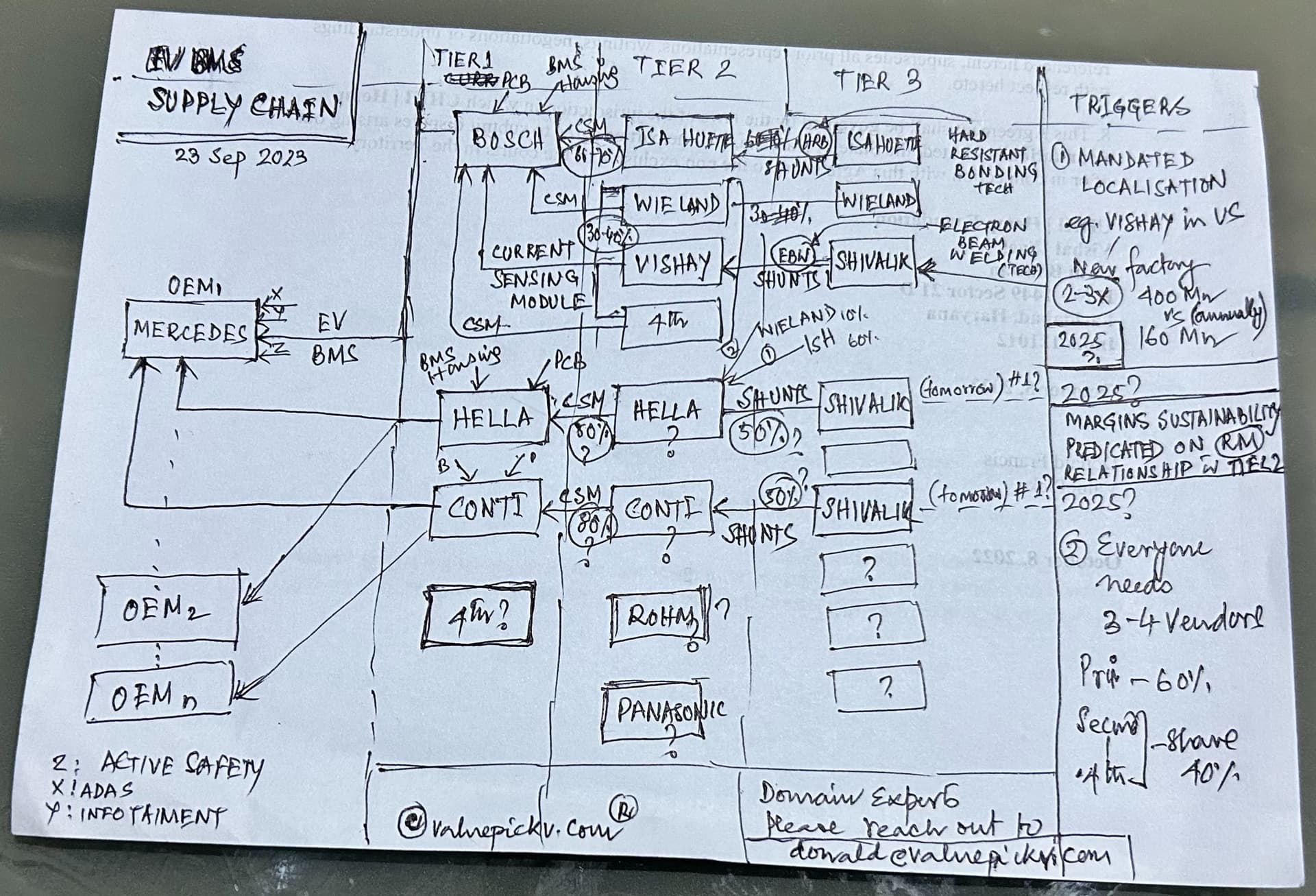

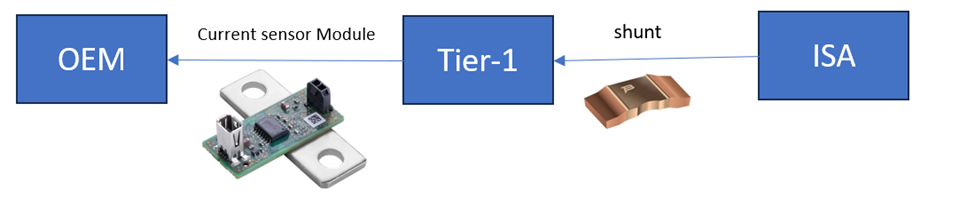

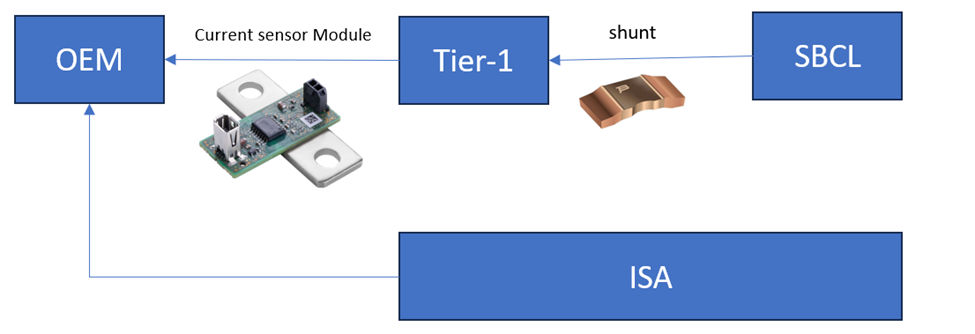

For Shunts bulk of the Sales were to Tier 2 Suppliers like Vishay, TTE, and others who supplied to BMS Vendors/OEMs. Again bulk of the Sales were for ICE BMS only, EV BMS Sales (even Vishay’s) is not significant today. This is set to change with direct EV SMD (surface mounted device) Shunts Sales to prominent Tier 1 Suppliers to global EV OEMs (relationships in place, today) set to go commercial and attaining scale in coming 2-3 years. Also locally to major EV players like Tatas, Mahindras [Refer [Fig 1].

-

Raw Material volatility is mostly pass-through. Contracts are entered into based on last months average pricing and/or last quarters average pricing. Management is confident on its ability to maintain margins at similar levels.

-

Right to win based on global Cost Leadership, Metallurgy Skills, Fastest Response Time, Lowest Lead Times. Largest Shunts Capacity in the world working 3 shifts 24/7 (expanding by 60% again for next 2 years). Fastest response times for custom projects owing to complete control on value chain - from custom design, moulds/tooling, and in-process Q&A automation, fully automated manufacturing process.

-

Future Expansion plans based on 3-4 year Forecasts/Orders Visibility from Customers. Major customers committing large multi-year volumes to secure Supplies.

-

Future Growth in Bi-metals likely from gaining market share from large incumbents. Management indicated current 16% market share can likely go up to 22% in coming years. Shunts growth will be driven by huge expansion of end market. 10% of global auto sales are already EV.

-

Joint-Design/Customer Handholding is becoming the norm for many EV customers who are new to Shunts. Many such customers are using Shivalik’s advanced moulds/tooling and design facilities, automated in-process testing facilities, and best-in-class manufacturing facilities from Solan facilities.

-

Given the fast growth, SBCL has to hold large inventory positions (Mar-22 inventory is ~35% of FY22 sales). This is needed to ensure that the reliability SBCL is known for is sustainably delivered. This has impacted its operating cashflows (Negative operating cashflows for FY22). Primarily (~60% of) this is raw material inventory. Part of this can normalize in an operating environment if and when global supply chains go back to pre-covid normal (~25% inventory position pre-covid). Raw materials inventory of around 120 days is maintained as procurement is imported and includes a variety of alloys. Receivables and payables are along expected lines (~66 days and ~46 days respectively in Mar-22).

INTERESTING VIEWPOINTS

-

Global Cost Leadership.

-

16% stake in 2008 JV with Aperam Imphy, the alloys division of Aperam S.A (spun-off from Arcelor Mittal in 2011, $5bn annual sales) called Innovative Clad Solutions. JV makes Clad solutions - applications in industries like cookware, energy storage, bearings beyond electronics. (160Cr Topline with 5x growth in PAT in FY22). The metallurgy strengths (parent) has helped Shivalik up the ante in Bi-metal/Tri-metal technology curve

-

Fastest Response time among peers with Shivalik controlling the longest value chain in bi-metals and shunts. Superior metallurgy knowledge, ability to completely custom-design-build fully automated in-process inspection/machinery (with global partners) - unique among peers. Turnaround time for some unique customer-specific projects have sometimes been less than half that of major incumbents.

-

Quite a few of SBCL products have thus become the Reference industry standard. Reference standard implies the customer asks new vendors wanting to participate to first match SBCL product specifications.

-

Indian domestic EV Shunts market (yet to really take off) is likely to be completely dominated by SBCL. EV leaders like Tatas and Mahindras have been working for long with SBCL on the products. As per industry scuttlebutt, some of the leading players are actually working from SBCL Solan factory, to jointly design/automate/test custom products. EV Shunts use will be 8x-16x standard ICE BMS use.

-

Europe 5G - One-time requirement of Surface Mounted Device (SMD) Shunts during installation/rollout phase. Shivalik delivered quick solution, likely to be the de-facto choice. Interesting to see if Indian 5G Network rollout/installation phase (getting rolled out as we speak) sees a big spurt in requirement of SMD shunts.

-

SBCL has set up a fully automated Rolling Mill and fully automated Bonding Mill with the ability to roll bimetal strips down to as thin as 0.09 mm with a precision of +/- 1 micron. Rolling Mill is a machine that reduces the thickness of metal without sacrificing any of the material, material is displaced, never lost, no scrappage. Bonding Mill fuses a central strip of pure metal to outer strips of alloy-metals.

-

As per industry scuttlebutt supply lead times currently for some Shunts majors are more than 50 weeks, while Shivalik’s lead time time for any customer product supply has never exceeded 20 weeks

-

SBCL increased stake in subsidiaries: SBEPL: valuation 3.15cr, sales multiple- 2.5x , net assets multiple 1.37x, net profit multiple 14x, SBECPL, valuation 23.56cr sales multiple .59x , net assets multiple 1.75x , net profit multiple 9.77. These have been value accretive EPS accretive valuations which are helping consolidated revenues grow much faster than standalone due to the low base effect.

-

Can forward integrate to Current Sensing modules from bare Shunt Resistors (~5x value adddition). As per Management, these products are on their radar. Huge potential for current sensing modules in charging applications infra, heat/temperature control applications for BMS add-ons,and so on.

-

In recent UP & Gujarat government smart meter tenders, only 3 companies’ shunts qualified -Isabellenhuette, SBCL, Redbourn engineering. Redbourne is now bankrupt, further consolidating supply side.

-

SBCL used to make CRT (Cathode Ray Tube) monitors till 2014. in 2011, CRT revenue contribution was 30% but fell to 0.5% by 2014, and the project was shelved. SBCL wasn’t able foresee the technological obsolescence of CRT in favour of LCD/LED TVs. To their credit they were able to adapt the business model towards scaling up Bimetals and Current Sensor Shunts over time.

BULLISH VIEWPOINTS

-

Largest capacity for Shunts globally (already). Another 60% expansion in next 2 years. Expansions are based on 3-4 year forecasts from Customers.

-

Global Market share 10% plus in Shunts, and 16% of Bimetals. End markets like EV are growing at 30%-40% even at global level (Domestic market is faster growing but smaller base and relatively lesser appreciation for high quality). Given oligopolistic product dominance market, good scope for market share expansion and overall market growth. Shunts/EV Shunts market is just getting off the blocks (scope is explosive but unquantified, as yet). Bimetals is a more matured market, but Shivalik has been increasing market share, especially from FY22 onwards

-

Raw material prices are a pass through for Shivalik which we can see in terms of how stable gross margins have been in last many years.

-

High Fixed Asset turns, reasonable working capital intensity, high operating margins mean that Shivalik is able to churn out 30%+ ROCE. Low competitive intensity helps with latter. Low capital intensity helps with former.

-

High technological & technical knowhow based, volume based, cost based, learning curve based entry barriers, first mover advantage, client (Auto OEM) stickiness, high customization requirement both on revenue and capital equipment side ensure that industry structure is in favour of incumbents like SBCL

-

Government of India plans to convert all installed conventional electric meters to Smart Meters. Total installed base of Smart Meters in India will thus go up from 50 Lakhs (can track status here) to 25 Cr. Each Smart Meter typically uses 2 shunts (source). Demand for Smart Meter shunts is thus expected to go up 50x cumulatively from current levels. SBCL being a leading shunt supplier for Smart Meters is expected to be a major beneficiary.

-

Various Switchgear MNC majors like Siemens, Schneider doing capex in india to meet both domestic demand & to export using india as a low cost base will aid further in increasing SBCL Bimetal sales.

-

Shunts are a critical application low cost product. A small part of end product cost (1 shunt costs ~1$. Even with 10 shunts, cost as a % of a 10000$ Car is < 0.1% of end product). This makes shunts an unlikely component on which OEMs would try to squeeze the supply chain for margins.

-

Mr. Kabir Ghumman & Mr. Sumer Ghumman sons of Shri N.S. Ghumman (Managing Director) have been working at SBCL for 14 years. Mr Kabir is a mechanical engineer and responsible for the supervision of all technical and process engineering aspects of the Company at the manufacturing unit. Mr Sumer is a qualified Graduate in Accounting & Finance having experience in Corporate Strategy, Governance, Finance, Regulatory/Legal and Risk management. He is also serving as Managing Director of the SEPPL. Thus, Succession Planning is reasonably clear in SBCL.

BEARISH VIEWPOINTS

-

Case of Peak Margins (?): Post covid demand surge has resulted in shortage for electronic components. This has led to expansion of margins for key clients like Vishay. Could this be a case of peak margins for SBCL? If margins come down for Vishay (or in general across supply chain) it could impact SBCL negatively.

-

One-off Revenues share: Although SBCL has helped some customers execute 5G launches in Europe by improving design/cost competitiveness this means that part of current & near term revenue might be one-time demand and non-recurring business.

-

R&D Team Expansion behind the curve (?): The R&D activities are led by the MD Mr Ghumman. He is 70+ years of age. There is a risk to the R&D pipeline of the company given that previous breakthroughs like Bimetals & Shunts have been led by Mr Ghumman. SBCL Management has indicated R&D Team expansion is a key focus area for the near/medium term

-

Client concentration risk is high. Though headed in right direction as dependence on Vishay has come down from 50% of sales to 30% of sales.

-

Volatility in raw material prices and forex rates: With metals such as nickel and copper forming around 50% of overall cost, operating margin remains susceptible to volatility in commodity prices. As per SBCL Management, though metal prices may continue to fluctuate, this risk is mitigated by order-backed processing undertaken by SBCL on highly customised products.

-

Rapid Expansion Spree: Anticipating high demand for its products SBCL has been on a rapid expansion spree. Management though has indicated that all expansions are being undertaken on the basis of customer-driven 3-4 year forecasts. However, It is possible that major competitors have embarked/might ramp up capacities in similar fashion in order to defend/gain market share. This could lead to stretched working capital cycles and/or margin deterioration In the medium term.

-

Supply Disruptions: Nickel and copper supply disruptions due to geo-political effects of continuing Ukraine conflict and/or US:China semiconductor/rare earth metal conflicts cascading effects.

-

Increasing Competitive Intensity: Although it may seem like SBCL is in a sweet spot for the near to medium term, the profitability and huge growth prospects of its product markets is bound to attract enhanced competitive activity - a key monitorable. Even local competitors like Permanent magnets have been trying to crack the high value shunt market for some years now.

-

Technology Substitution: Shunts are an alternate current sensing technology to Hall effect sensors (HES). HES are also used by some clients but is currently more expensive (than shunts) and reportedly less suitable for high temperature applications. Advancement on HES in terms of costing/applications could result in them becoming more competitive than shunts

-

Single Point of Failure Risk: All of SBCL’s factories are in Solan. Himachal is a high seismic activity zone. The tail risk of seismic activities disrupting production cannot be ruled out.

-

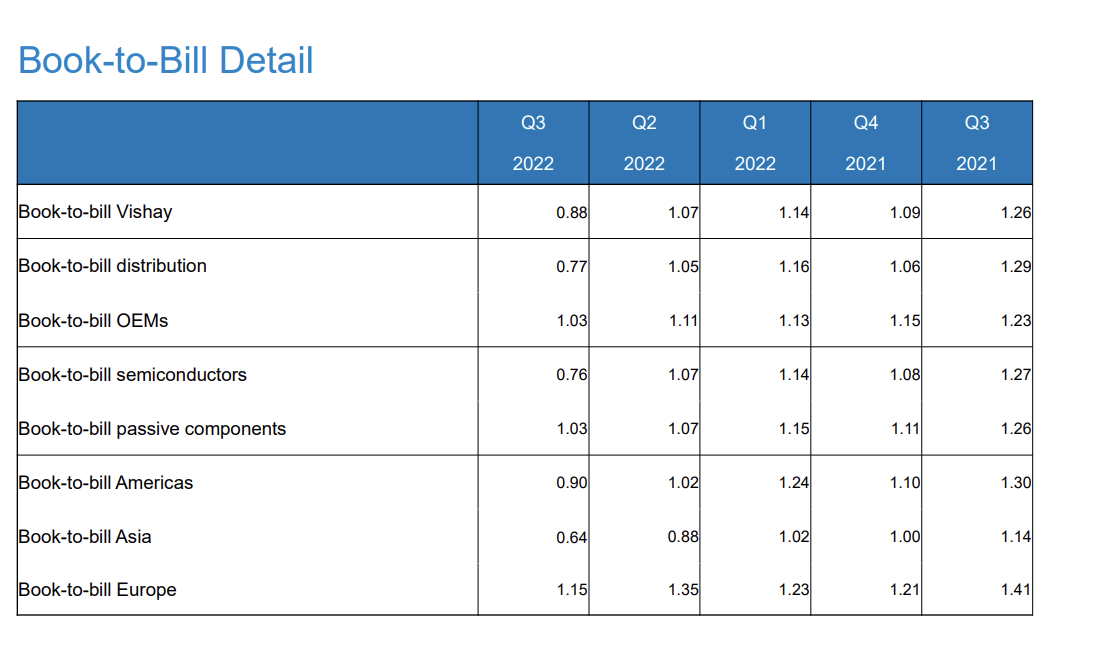

Largest client has reducing book-to-bill ratio: Vishay’s book-to-bill ratio has been decreasing (see line item for passive components).

This indicates some softening of demand. This could result in reduction of margins, or growth, or both.(Book-to-bill for passive components/Resistors segment is holding up better than other segments of Vishay) -

Customer Losses in recent past: SBCL Export Data points to 3 longstanding customer accounts going off Shivalik Books since 2020. One in Bimetals segment and a couple from EBW Shunts segment. Though compared to major new accounts signed up this is probably negligible, will be good to check with SBCL Management reasons/significance.

VALUATION MODEL

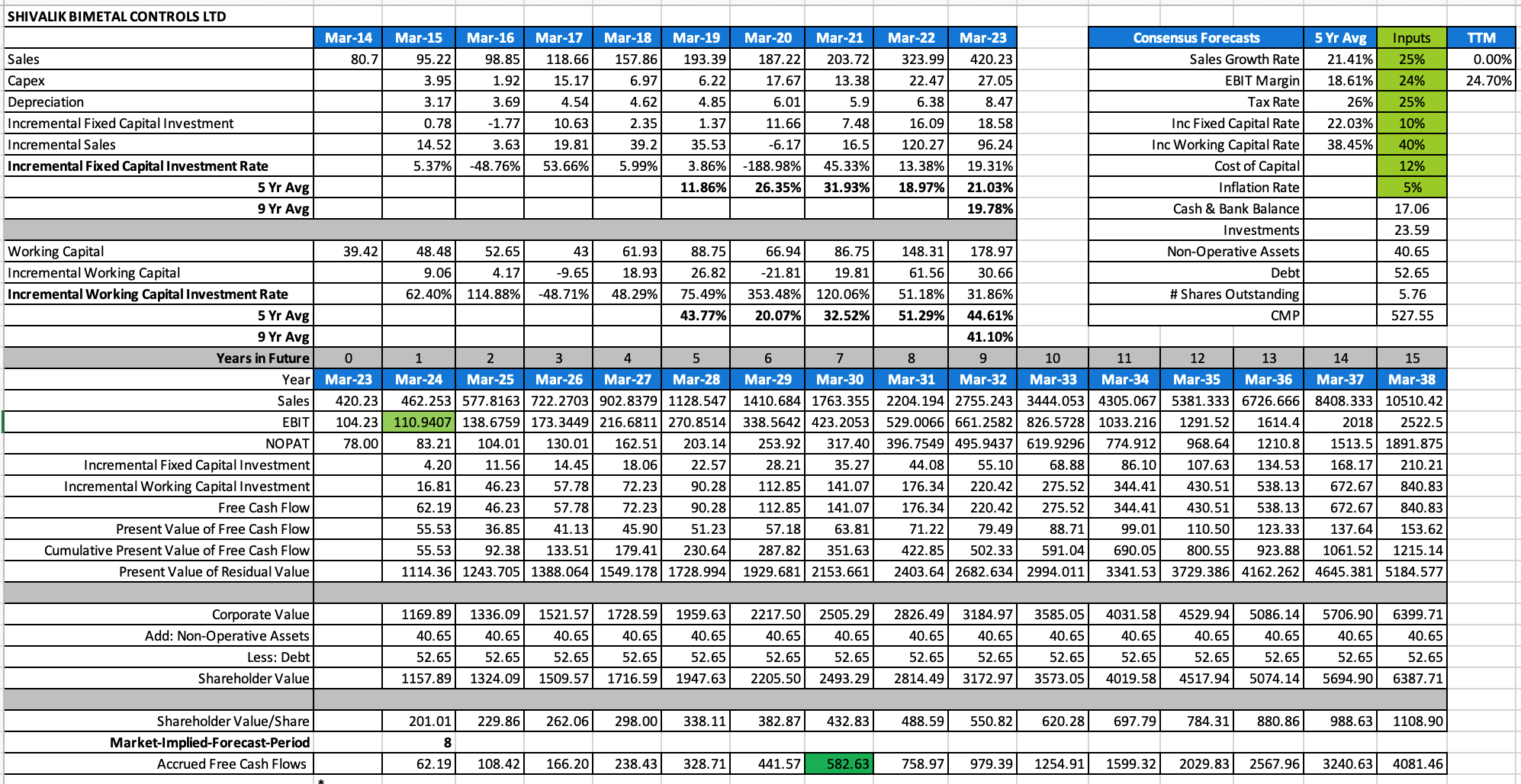

At CMP 472, SBCL trades at around 2700 Cr Market Cap - 40x H1FY23 annualized consolidated (ex other income) earnings boosted by exemplary performance, of late. Near Term growth has been good - 59% in FY22 including 47% volume growth - well supported by Industry Tailwinds and SBCL Competitive Position growing stronger, as enumerated in the Stock Story.

Management guidance (FY22 AGM) has been conservative, as always, and one can model in 20% top line growth and margin maintenance with 25-30% ROCE for the medium term (~150 days WC, Fixed Asset turnover of ~4x, EBIT margins of ~17-22%), given SBCL past track record and competitive positioning.

Medium-Term Optionalities:

- EV Shunts Market huge expansion and/or significant EV customer penetration by SBCL

- Margin expansion through forward integration into current sensing modules

CORPORATE GOVERNANCE SCAN

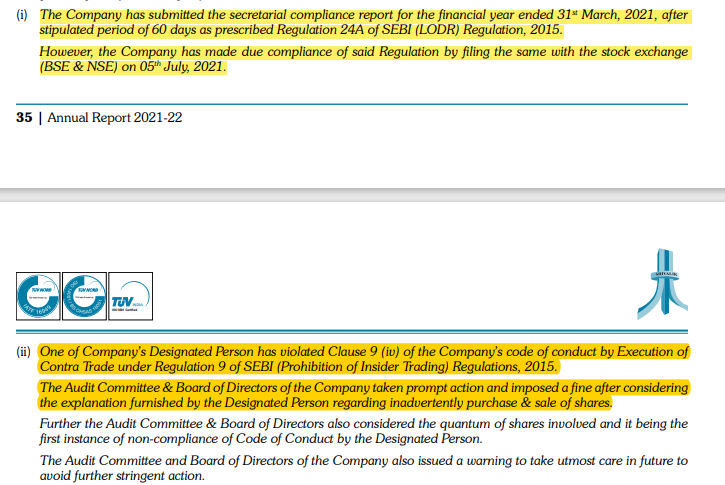

The company reported two adverse compliance related issues in FY22. First was related to delayed secretarial report filing with stock exchange, and the other related to insider trading violation

RED FLAGS/FORENSIC SCAN

Negative Operative Cash Flow in FY22:

With a lot of money stuck in Receivables (16 Cr) and inventories (45 Cr), operating cash flow has been negative.

Interest Accrued and Due:

FY22 AR indicates interest accrued and due of Rs 9.41 lakh as on 31st March 2022. Typically, such entry would mean company is not able to honour its obligation on time. However, during AGM, Management clarified that it was due to new accounting standards which resulted in booking interest, while bank charged interest only on 1st April. The explanation appears acceptable but such entries, at best, shall be avoided in financials.

Interest on delayed income tax payment:

The company paid Rs 24.33 lakhs during FY22 and Rs 21.84 lakhs during FY21 as delayed in income tax payment. Management clarified that the company did not envisage growth in profit would mainly came in Q4 of year resulting in higher than expected tax liability and hence company had to pay interest on delayed income tax. However, this does indicate scope for improving internal systems so that company is on-time in paying tax liability, and avoid such delays.

Accounting related issues:

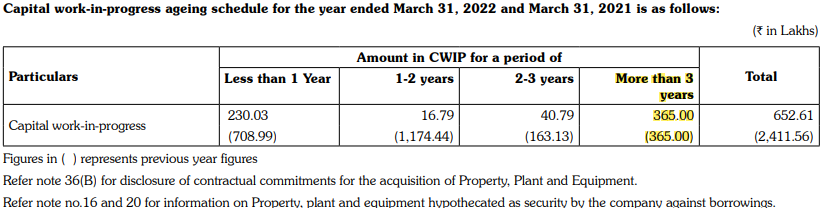

Large CWIP ageing more than 3 years:

Conservative accounting policy would suggest writing off such amounts to P&L, unless there is logical base to assume that such expenditure can be capitalised and useful for future projects of the company.

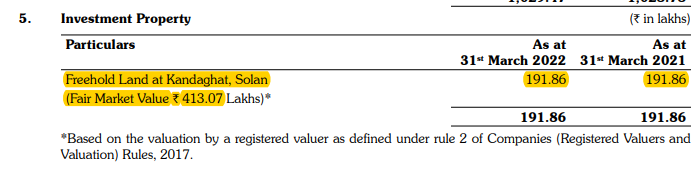

Non-core assets not being liquidated

Management could prioritise disposing off freehold land and gold bond investment and utilise that fund in business capex. While the amounts are not very material, but still, if the future of such investment are not core to business, it is better to liquidate, at the earliest.

DISCLOSURE(s) OF STOCK STORY CONTRIBUTORS

Sahil Sharma: Invested, ~15% of portfolio

Dhiraj Dave: Invested ~17% of portfolio

Donald Francis: Invested

BACKGROUND

Shivalik Bimetal Controls Ltd. is a company specialized in the joining of material through various methods such as Diffusion Bonding / Cladding, Electron Beam Welding, Solder Reflow and Resistance Welding. Our present program includes Thermostatic Bimetal, Clad Metal, Spring Rolled stainless Steels, Electron Beam Welded Material with multi- Gauge and Multi- Materials strips and Thermostatic Edge- Welded Strips for a board spectrum of industries. [1]

MAIN MARKETS/CUSTOMERS

The company products are exported to around 40 countries around the world. [1] India accounts for 40% of company’s revenues, followed by America (35%), Europe (14%) and rest of world accounts for 11% of revenues. [3]

MAIN PRODUCTS/SEGMENTS

The company is in the business of manufacturing & sales of Thermostatic Bimetal /Trimetal strips, Components, Spring Rolled Stainless Steels, EB welded products with multigauge, Cold Bonded Bimetal Strips and Parts etc. [1]. Thermostatic Bimetal/Trimetal Strips contributed ~46% of revenues and Shunt Resistors contributed to ~52% of company’s revenues in FY22.

The shunt resistors division of the company is relatively new and was started 4-5 years back by the company. [2] and caters primarily to Internal Combustion Engine (ICE) Battery Management Systems (BMS).

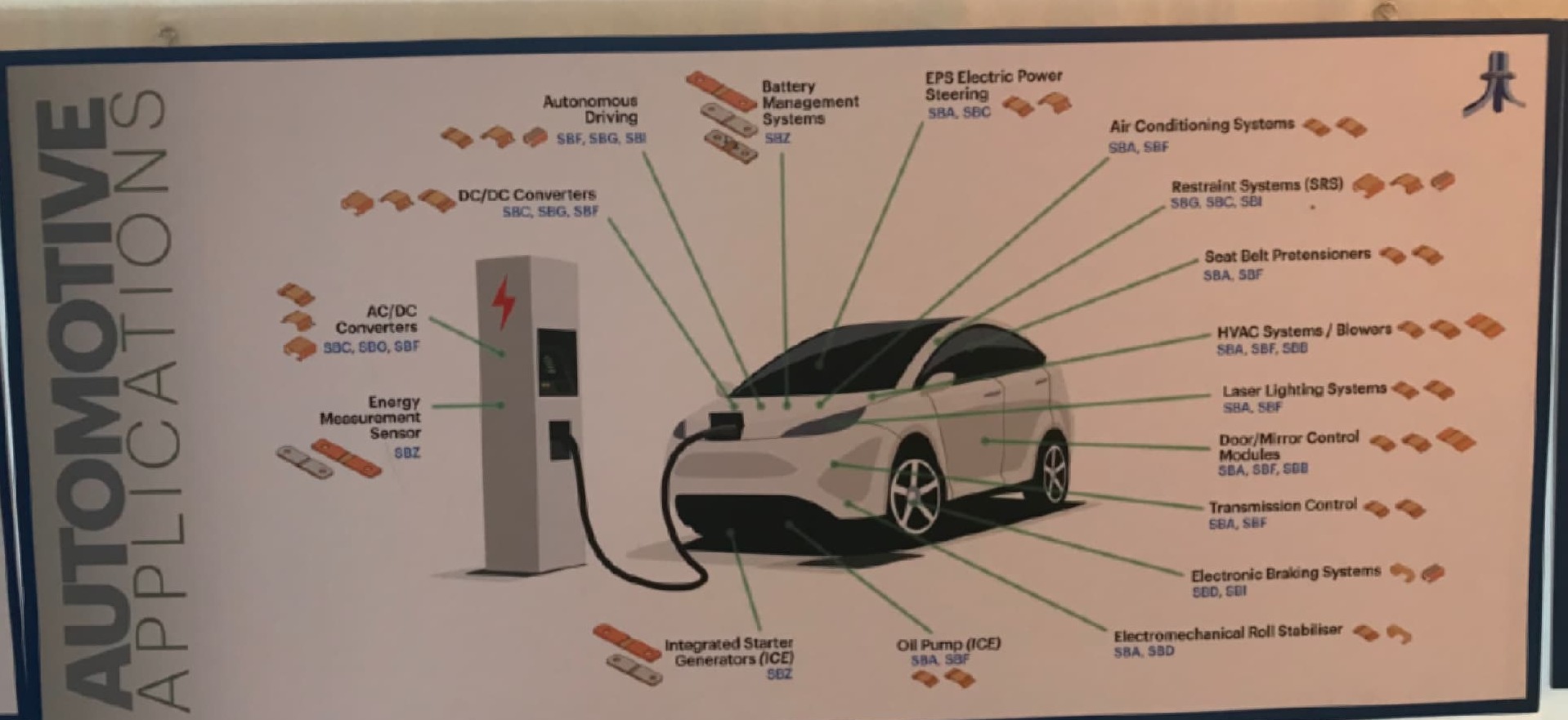

Electric Vehicle (EV) Automotive Applications

Target applications market (figure above) for Shivalik’s products in the EV domain (yet to take-off) is now hugely enhanced with SBCL working directly with some EV OEMs and Tier1 Suppliers to EV OEMs. From Air Conditioning Systems, HVAC systems, lighting systems, door control modules to AC/DC converter and energy measurement sensors in EV chargers, in addition to EV BMS.

MANUFACTURING FACILITY

The company has an established facility in Solan, Himachal Pradesh from where it carries its manufacturing business. It has its head office situated in Delhi. [4]

JOINT VENTURES AND ASSOCIATES

Shivalik Bimetal Engineers Pvt Ltd - It is wholly owned subsidiary of the company. It owns capabilities for designing of press tools (CAD) & their manufacturing. [6]

Checon Shivalik Contact Solutions Pvt Ltd - This is also a wholly owned subsidiary of Shivalik Bimetal. It makes silver & silver alloy based electrical contact materials and assemblies. [6]

Innovative Clad Solutions Pvt Ltd - The company is a JV between Aperam & Shivalik wherein company is a minority shareholder with 16.01% stake. [2] [6]

SOURCES:

- AGM - Sep 27, 2022

- Industry Scuttlebutt with some Tier2 Suppliers

- Investor presentations

- Annual Reports