10 Prioritised Questions for Shivalik Bimetal AGM

(Thanks for collated collaborative efforts from @nirvana_laha @GourabPaul @spatel @Chins)

1. Competitive Positioning

Automotive EV BMS Market for Shunts is reportedly served by only 6-7 vendors globally. Isabellenhuette commands 50% market share. Shivalik Bimetal is now close to ~10-15% market share as per some Industry players.

Is it a fair argument to say that Bimetal (Alloy)/EBW expertise is the KEY differentiator for this segment, which is augmented by Shivalik’s cost leadership position. And that Shivalik is de-facto cost leader today, globally?

Is Shivalik growing by progressively taking away market share from top incumbents like Isabellenhuette, Hella, Continental and others like Rohm and Panasonic.

2. SBCL JV with Aparam Infy - Innovative Clad Solutions (SBCL stake 16%)

Given that the JV has been in place for more than a decade, are there any insights regarding tech transfers in alloy-making that may have happened or are likely to happen from Aperam Imphy to SBCL?

a) Clad metals find diverse uses outside of the electrical industry in cookware, heat exchangers, energy storage solutions etc. Does SBCL have any plans of tapping these industries?

b) Does SBCL see the JV as strategically important and have any plans to increase their share in the JV?

3. New big-name Customers in Bimetal segment (38% Exports)

Cutler Hammer

Fenix Manufacturing

Robertshaw Controls

New customer wins contributing ~20%?

Would you like to us through some of these recent wins that seem to have scaled up significantly. What helped us gain entry and penetrate deeper so quickly in these – bimetal alloy improvements/customisation?

4. Recent Customer Losses?

Sensus DUB used to be a large Bimetal customer of Shivalik till 2020, and stopped thereafter? Did the company get winded up/merged into some other entity, or it has shifted to other vendors, reasons?

Landis GYR Meters, Wieland Werke – large customers in EBW Shunts stopped after 2020? Comments

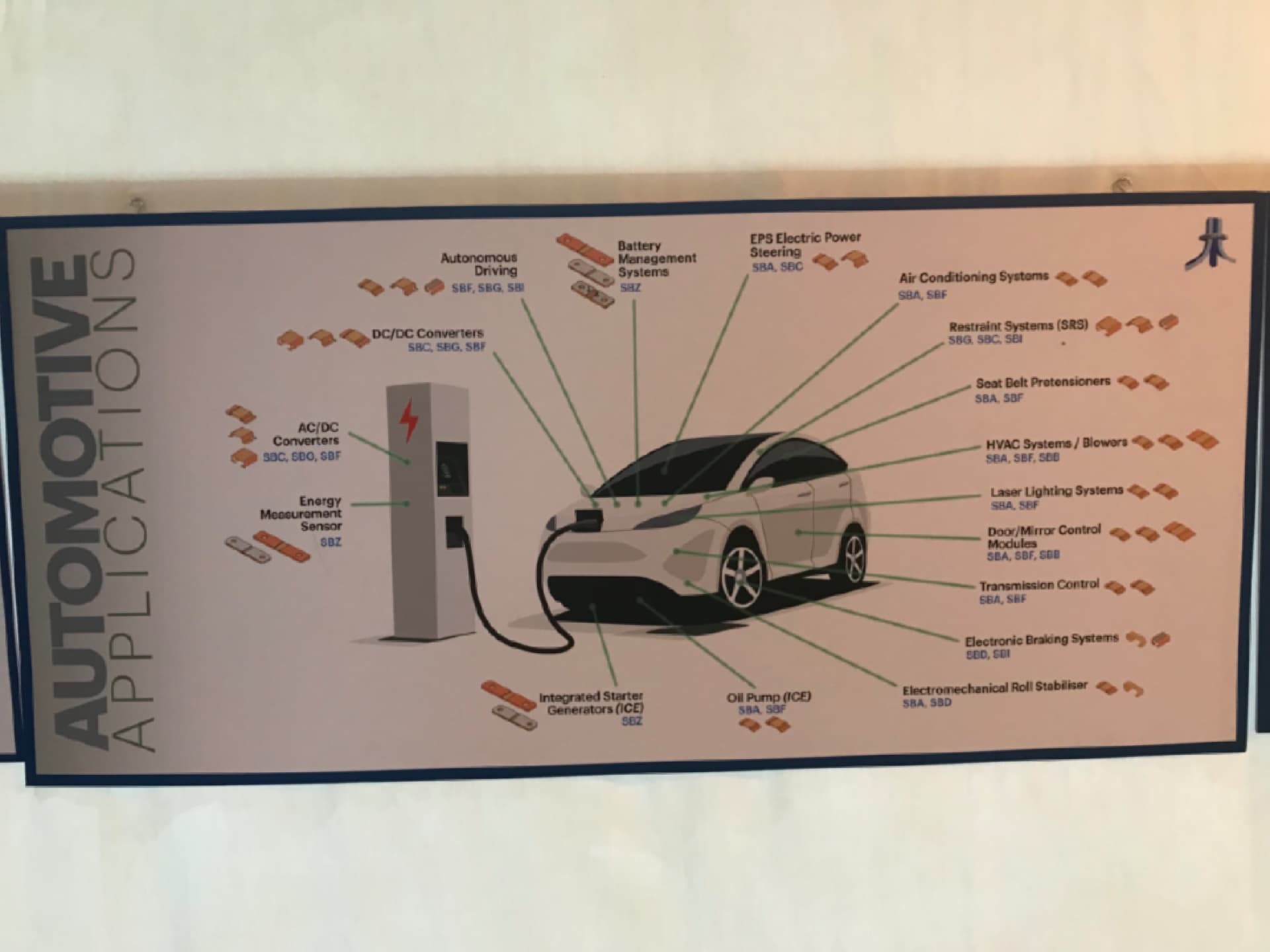

5. Non-BMS Shunts in EV/Battery Space

a) Are any of the shunt strips going to a standalone current sensor module which is integrated to the BMS

b) Are your shunts being used in inverters, dc-dc, electric motors in an EV. Scope for OEM supply?

c) Is there a medium-term vision towards making a current sensor module in-house for 2W and 3W markets in India. If not, what are the impediments towards that? Reportedly, that’s a 5x value-addition?

6. EBW Shunt Segment (62% Exports)

Vishay

Shin Shih

TT Electronics

EMH Metering

Bimetal Japan

Top 5 contribution 90%

Top 3 contribution 80%

Top Customer concentration has been steadily reducing, but there is still a huge dependency ~90% contribution from Top 5 customers?

What is the right way to look at this situation from Management Perspective/Targets?

a) What is the ideal segment mix EBW Shunts: Bimetals: Smart metering given industry tailwinds in next 3-5 years

b) what is the ideal diversified customer mix SBCL is looking at in 3-5 years

Have we seen instances of direct supply to OEMs/Tier 1 Vendors scaling up? Does that remain a distinct possibility, or supply will mostly be through Tier2 vendors?

7. Smart Meter Opportunity

Globally US $36 Bn by 2028 growing at 8% CAGR

India replacement Market – 250 Cr Legacy Meters

4.8 Mn smart Meter Installed base (as on date) of 11.6 Mn tendered Jan ‘22

Would you like to characterise this segment opportunity for us – Industry tailwinds, Shivalik Competitive Positioning in India and Globally, major competitors and customers.

8. Shivalik Product positioning – Proxy play/beneficiary of major market shifts?

ICE to EV

Legacy Meters to Smart Meters

Fuel Dispenser to Charging Station

Fossil Fuel to Renewable Energy

(Battery Storage, Switchgear current ammeters; Isabellenhuette works in this space)

This is an interesting perspective from an astute industry observer. Other major market shifts happening - say Wired to Wireless, and Manual to Robots. Does Shivalik see a place for its products in other such market shifts?

What is the Management’s perspective on the product space it wants to occupy?

9. EBW Shunts and Hall Effect Sensors

Mercedes uses only Shunts for EVs

Mercedes uses both Hall Effect sensors and Shunts sensors in Hybrid EVs

Could you give us a better sense of how this sensor type/usage decisions are firming up. Is this a settled case in favour of Shunts, or use cases for usage of both sensor types are going to prevail going forward too in Automotive applications.

10. Lead Times

Shunts lead time today standing at 40 weeks?? (as per some industry players)

Good thing for now? May lead to surplus capacity investment leading to a glut situation again – couple of years down the line?

Would you care to throw more light on this aspect, what is Management’s perspective?