I agree I should have known this. I was far more enamored with the technical side that I missed this obvious question. Although the mgmt. did acknowledge their slightly risky debt position and are looking to work on it.

1 Like

Fantastic. Thanks for the MOD Annual Report, and the other doc. Useful ![]()

You are answering a different question.

It was never the case that Technology was closely guarded/unavailable.

On the contrary DRDE technology was easily available to anyone who cared. Not many cared why?, especially if the Market is 650,000 suits or 12x the initial order in Dec 2015 (well-known by 2014)??

Specifically on Vijay Sabre: From all the information that I could gather they did not look like a company that can execute an order of this size. Both from their epfo disclosures and sales value. I could be missing something here.

You are asking the same question again and as I said before I don’t have the answer now ![]() .

.

MK IV Suits were ordered at ~11326/- per suit.

Advanced technology MK V suit bids were probably won at 18000/- to 20000/- per suit, assuming a 90-100 Cr total order of which Shiva Tex Yarn was awarded say 60%. (the 55 Cr mentioned by Mgmt in interview)

Interestingly, the Report does not mention reason for non-acceptance of sample - whether it failed to meet specs, etc. Doesn’t seem to mention any pre-qualification by DRDO/DRDE either.

A slightly dated (Mar 2014) Baseline survey of Technical Textiles Industry in India from Textile Commissioner/ICRA Management Consulting.

The survey is useful for identifying large number of companies who have been involved in Technical Textile categories - High Altitude Clothing (29% market) Fire Retardant (12+17%), Bullet Proof (14%), NBC share was a mere 1% (of total 1340 Cr spend) then.

It emerges that Ordnance Factory had been the largest manufacturer of MK IV suits in India, as also for High Altitude clothing ( in both categories Lakshmi Cotsyn Defense had started production/had major plans - very interesting to study that puzzle and the learnings). 3 private player names also emerge Entremonde Polycoaters, Sri Lakhsmi Cotsyn Defence as having started production of NBC Suits and Kusmgar for breathable fabrics and other fabrics for NBC use.

Laksmi Cotsyn in its own AR mentions of this order FY14 but does not say anything about it in FY15 AR. They do mention that they have a 10 lac meter capacity of CBRN cloth. Would be interesting to know if the cause of failure was financial or technical.

This is a very valid concern and I agree with you that any delay on Technical textile side can impact the debt serviceability prospects. @aveekmitra did some calculation based on the last year’s results (upto Q4 last year) and extrapolated them to FY17. A status quoist approach does show the company’s vulnerability in this aspect. The good part as you said the company is reducing debt and the management’s awareness and acceptance of the situation.

Attaching the same excel.

SHIVA TEX 2016 QUICKCALC25052016.xlsx (12.8 KB)

1 Like

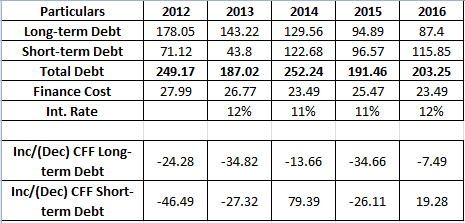

With reference to the above point I started looking into the debt and finance cost figures…to see if I can find any pattern, as to why the huge interest burden.

To make things easier I plotted the debt figures (break-up in long-term & short-term) & finance cost. Additionally, to get a better picture I incorporated debt inc/dec figures from cash flow statement. (Please, find the table below).

The concern I have after looking at the table is, the reported finance cost figures, even though the debt figures are varying over the period, finance cost is roughly the same.

Like, in 2013 Total debt was down to 187cr (PY 249 cr) but the finance cost was marginally down to 26.77 cr (PY 27.9 cr). Again, in 2015 total debt went down to 191.46 cr (PY 252.24 cr) but, finance cost increased to 25.47 cr (PY 23.49 cr).

I found this a bit unusual ![]() …is it possible that company is paying back the loan towards the end of the financial year to report lower debt figures (as the balance sheet is reported “as on that date”) and is again taking these loans in the beginning of the next FY.

…is it possible that company is paying back the loan towards the end of the financial year to report lower debt figures (as the balance sheet is reported “as on that date”) and is again taking these loans in the beginning of the next FY.

Since, the finance cost is an expense, which forms part of the P/L statement (transactions are recorded “over a period of time”) is unaffected by this debt movement in balance sheet and is getting reported at similar levels.

@Anant Sir & @Donald Sir above table might help to validate the concern I have…please let me know in case I am missing some point here and interpreting the numbers incorrectly. If not, then we should raise this concern with the management and try to get a better sense of it.

Regards,

Yogansh Jeswani

Disclosure: Not Invested

8 Likes

There are two ways I want to answer this. Firstly a data based answer:

I do not see the variance too much and hence do not see that as a possibility. There are too many vagaries in interest rates and that could result in interest cost going up/down by a few crores. What is heartening is both the long term debt and also interest cost coming down. I have also jotted down their mid year debt position and the mid year interest payments and they look more or less in line too.

Further the company gives complete details of its long term and short term loans in the Annual report and they are inline with the payment schedule.

From a debt perspective I would be more interested to know the reason for their not availing TUFS as Donald had stated above.

On a more philosophical basis “You first trust the man and then trust his accounts it cannot be the other way round.” ![]()

4 Likes

Hi @Anant,

Thanks a lot for sharing your in-depth work on Shiva Tex. You have done very good work.

I was going through the annual reports and we tabulated the quantitative details mentioned, I noticed that the company was doing good numbers on the fabric side till 2013 and then that fell off by 75% to recover back to those levels only now. Any idea as to what were they doing under this earlier?

Also its interesting to a substantial number from sale of waste cotton - why would the number be so high?

Don’t you think the overall margins are quite low given that they have some segments which might be very high margins?

Thanks & Regards,

Ayush

4 Likes

The amount of cotton waste to cotton yarn production is roughly 1/3 across other companied that I checked. I have looked in Bannari Amman Sinning, Kallam Spinning. I think it is the industry dynamics and not something specific to Shiva texyarn.

4 Likes

Most of there sales until last year came from commodity yarn. Technical textiles only contributed 10% roughly. There would be enough operational costs to squeeze out the margins in technical textiles. As far as commodity cotton yarn margins are concerned they are pretty much in line with the Industry.

1 Like

The typical waste generated in cotton yan manufacturing would be depend on combing and carding. Typically, high counts above 40s are generally combed and hence wastege is around 25-30% of cotton input. However, in case of lower counts, there only carding process which result in waste of around 10-15% only. (It is possbile also to get lower count combed yarn but then the prices are higher due to waste of cotton and superior quality as compared with same count Carded yarn). The enclosed link give broad numbers. So the waste would depend on whether the yarn is combed or not. Higher the combed yarn, suprior realisation, and also high waste quantity and value.

http://textilecentre.blogspot.in/2013/09/yarn-realization-control-of-waste-in.html

4 Likes

These are the AGM notes (got delayed due to travel) during and on sidelines of AGM. Most of the questions were to understand the future direction of the company and to the points made in the interview given in the textile magazine. Other folks who attended AGM kindly add/correct if something is inaccurate:

-

Evolution: The plunge into technical textile started with QuickDry and it was accidental. They had bought some extra machines just for trying out laminated textiles. Continuous experimentation lead to QuickDry they first wanted to market it with the biggest player in the market since they had the entire market nearly (40 cr at that point of time) for rubber sheets used for infants but they refused saying it is 2.5 times costlier than their product. The company and the management were very satisfied with the product and hence launched it on their own.

-

Product lines (not as stated by the company but as per my differentiation) and their future prospects:

a. Legacy yarn business: The company post demerger of the other unit will continue with the remaining spindles but there will not be further investments in this line of business. It will remain a commodity business. The products from this line does not feed into technical textile.

b. Coated Textile: The Company mainly supplies canvas in this product line. It is a relatively smaller product with sales hovering around 10cr – 20 cr with margins in the range of 15% to 20%. These are majorly exported and the company does seem to have a very good short term visibility here. From a longer term perspective this line does not have a bigger opportunity size and the company does not intend to further it. There is little or no domestic competition here most of the competition comes from China. A ban on PVC flex which is currently used can be very good for the business and can change the fundamentals completely (Despite environmental and safety hazards, the political class being largest user of these banners it may not materialize anytime soon but if it does the upsides are huge as company claims to have differentiated solutions in this space. ).

c. Laminated textile: The laminated textile business has multiple sub units majorly feeding into Consumer (QuickDry & WULF) and Defense segment (CBRN, High Altitude). More importantly the lines for one business can be used for another. This takes care of high employee count related risks to some extent since Defense orders can be lumpy.

i. Consumer: The business here is cash & carry and does not require too much working capital.

• QuickDry & allied products: The Company is looking good to achieve 30% growth in this segment. There are more than 10000 POS and the plan is looking to increase the same.

• WULF: There is change of strategy here. The earlier WULF products had an issue with regards to product placement and the company is now focused of specialized utility bags. They have launched camera bags under the WULF Pro line . The company can look for more specialized scenarios and introduce WULF Pro accordingly.

ii. Defense: Overall the defense payments are in one month of despatch. Most of the times payments get stuck due to incorrect specs or bad quality. The company is extremely focused on quality so much so that they would not just meet the quality bar but exceed it by a high margin even at additional raw material cost.

• CBRN: The management confirmed that they have recd an order of 55 cr for CBRN textile and the dispatch for same would start from Q3 this year. Generally there is a follow up order of ½ the quantity and the company expects bigger order going ahead. There could be orders from different wings of Armed Forces and also from CRPF. Worldwide there are very few manufacturers and even less suppliers of the product since a lot of countries produce only for self-consumption. There is a scope for exports as well to smaller countries but the company is currently not too focused there. The shelf life of products is 5 years and it is more from a preparedness perspective that the various customers want to own it. The risk from a Defense supplier perspective here is that there are only 2 suppliers and any impact/restriction on even one of them could lead to a single supplier scenario which the Indian Army does not like.

• High Altitude: The company has certain products for high altitude and extremely low temperatures the trials for which are currently ongoing. This involves a lot of technology on insulation side. In the tests conducted upto now the company has been among the best outclassing the currently used German products. These products need to go for trials this winter and any tendering can only happen in FY18. There is a huge commercial scope for these products and the stamp of approval from Indian Army in extreme conditions can help in a big way in acceptance by commercial entities.

d. IKEA supplies: The Company is looking to ramp up supplies to IKEA and expects to grow this segment strongly for the next 3 to 4 years. The company does not intend to add any more B2B customers due to relatively low margins and would only focus on IKEA.

- Debt: Company is cognizant of debt situation and would like to go to zero debt as soon as possible. The company does use TUFS. Due to lack of time we could not get answer to this but the company said they can revert to us over email.

- Capex: There is not much of a capex requirement for next two to three years.

Core Positioning Strategy of the Company

Overall Impression: The company is moving into right areas and has made products which have clear competitive advantage in terms of entry barrier and customer stickiness. CBRN and High Altitude textile shows the technical prowess of the company. A lot now depends on its execution of Defense orders and Q3 and Q4 would be key indicators towards that. If the company is able to execute on its plans this year and the next it will emerge as a much stronger player and will be in a shape to harness global opportunities. A bet on Shiva Texyarn is also a bet on Mr. Sundararaman who seems highly competent but at the same time introduces key man risk.

Discl.: No change in position in last 3 months. Forms more than 10% of my portfolio.

20 Likes

Thanks @Anant for a crisp note.

Let me add my impressions/focus areas from the AGM/Sidelines Interaction:

1.Management Quality/Whats in the DNA

Seems very committed, patient, long-sighted entrepreneur - who knows what he is doing. Like the systemic thoroughness in his approach. Defence Segment being key to future plans - was happy to note how he described ShivaTex graduating from a “greenhorn” status to now enjoying “mindshare” among decision-makers. More importantly, that they now are familiar with the systems and processes (every stage of sampling, foreign lab testing, evaluation, competitive bidding, at least 2 vendor, etc.).

Seemed focused on quality execution. Mostly rated among Top2 in Field Tests in different climatic conditions/regions. Also happy to note their competency in alternate RM sourcing - may prove crucial while harnessing global opportunities, in coming years. (Source: Management Claims)

2.Defense Order Continuacy/Execution Risks

Again good to note Mgmt did not brush off execution risks on this front. That even failure of other vendor to meet quality standards can jeopardise things. Good to know DRDE has the processes of making sure selected vendors are in touch with each other at each stage - approval, pilot supplies, and subsequently. Effective documentation at every level of testing, demo, approval, ordering ensure subsequent orders may not be scuttled on other (vested) reasons (other than product failing to meet quality standards).

3.Next Level for the Business

Good to see a confirmation of our hypothesis that Defence Execution is key. There is a decent pipeline of products in their niche (like High Altitude is next) where Shiva Tex again should be among qualified leading suppliers - Process is underway. Other segments are supporting lines.

If they continue to execute - bag other product line orders and deliver on quality - this will be a different business altogether. Many more optionalities (incl. global supply) should emerge - which there is no reason the business cannot then harness.

4.Concerns

Higher cost of financing - not explained. Did acknowledge though that there could be better financing models. Promised to revert via email

@Anant kindly pursue on this; given Bannari groups competence, can’t say am not a bit surprised here

5.Valuation

Having said all above, current valuation range seems to have priced in all the good things - lot of assumptions embedded  . Prefer to wait and watch them execute for couple of years, and then make an entry if fully convinced - (coy in the first couple of months of execution now - in key segment)

. Prefer to wait and watch them execute for couple of years, and then make an entry if fully convinced - (coy in the first couple of months of execution now - in key segment)

Disc: Not invested. Not interested at current valuation ranges.

18 Likes

I have noted few things about changes in defense procurement policy 2016 while evaluating ZEN Tec which maybe relevant to STYL as well.

Change in govt policy:

DPP 2016:

1.A new category Buy Indian (IDDM – Indigenously Designed, Developed and Manufactured) has been introduced and it will be given first preference.

2.Increase of indigenous content under Buy Indian(iddm) category from 30% to 40%. Under Buy and Make Indian category the requirement of indigenous content has been raised from 30% to 50%.

3.Single vendor situations:Previously Ministry of Defence was insisting for having at least two vendors even under Buy Indian category. The new DPP ensures that even if single vendor situation arises at bid stage, the procurement will be concluded, if the product qualifies and due process is followed.

4.Make Procedure has been modified to ensure that smaller companies participate as Developing Agency One encouraging feature for all the make projects where the product development is successful is that if the Government does not place the order within 24 months of developing the product, the Government will refund 100% of contribution made by the industry. This increases the Govt’s responsibility tremendously and insures the risk taken by the company.

5. Increase in offset threshold to 2000 cr from 300 cr for foreign vendors. Offset is the foreign vendor’s obligation to source locally (buyer’s country) amounting to certain percentage of the contract value, that go into the building of the purchased product. But with increase in offset threshold its not mandatory for a foreign vendor to tie up with local partner if the order is less than 2000 Cr.(THIS MAY BE NEGATIVE INDIAN COMPANIES)

STYL has developed its products with DRDO essentially comes under BUY IDDM CATEGORY.

DISC: INVESTED

3 Likes