Shiva Texyarn Limited:

History: Incorporated in 1980 as Annamalai Finance Private Ltd, Shiva Texyarn Limited (STL) was converted into a public limited company in 1985 and later renamed Shiva Texyarn Limited (STL). It was promoted by Mr S V Balasubramaniam and his brothers. The company’s main business is manufacturing and marketing of cotton yarn and other textile products. It has a capacity of 91,488 spindles. The company also 76 windmills having combined capacity to generate 22.54 MW of power. STL is part of the Bannari Amman group. It is one of the largest industrial conglomerates in South India with diversified interests in manufacturing, trading, distribution and financing activities. The Bannari Amman group operates in sugar, alcohol, liquor, granite, cotton yarn, wind power, education, healthcare, real estate, etc.

Current operations: At present, STL is primarily engaged in the manufacture and marketing of yarn to both the domestic and export markets with an aggregate spinning capacity of 91,488 spindles. Until FY08, STL was purely into spinning; however, in the last five years, STL has established a knitting unit with 41 knitting machines and garments unit with 120 sewing machines. The company also focuses on technical textiles which are based on lamination & coating technology. During FY15, income from technical textiles was Rs.40 crore (PY 35 crore), accounting for 9% (PY 7%) of the total income. Dr. Sundarraman (MBBS) is the Executive Director and manages day to day operations of the company. He is also the Vice President of Indian Technical Textile Association (ITTA).

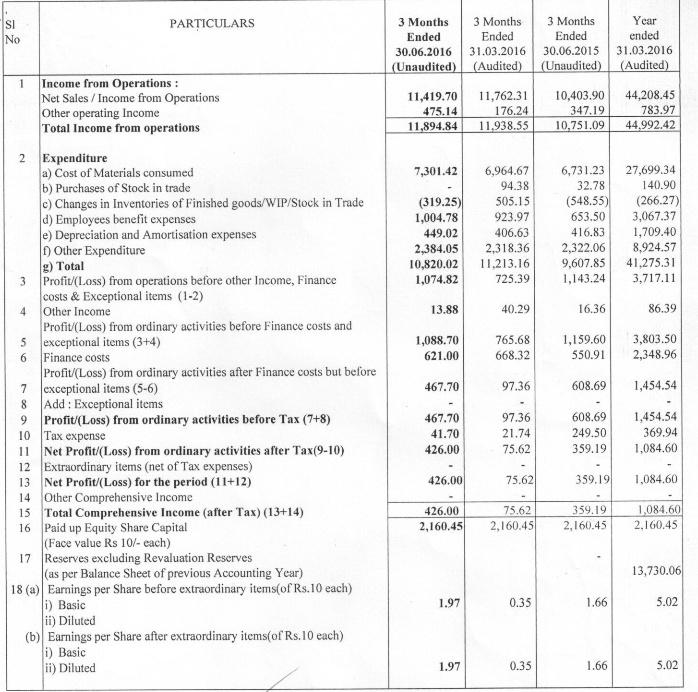

Financials: Obtained from https://www.screener.in/company/SHIVTEX/

Mar-05 Mar-06 Mar-07 Mar-08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 TTM

Sales 84.7 81.07 99.23 96 98.87 194.53 397.27 331.95 419.16 504.47 465.29 443.6

Expenses 66.82 62.39 72.99 78.11 81.87 163.71 326.22 315.52 347.64 432.07 411.07 388.67

Operating Profit 17.88 18.68 26.24 17.89 17 30.82 71.05 16.43 71.52 72.4 54.22 54.93

OPM 21.11 23.04 26.44 18.64 17.19 15.84 17.88 4.95 17.06 14.35 11.65 12.39

Other Income 3.32 2.78 2.71 5.42 1.75 3.66 7.75 1.62 5.98 1.12 0.83 0.66

Interest 7.39 7.08 6.21 4.69 4.66 12.71 23.13 27.99 26.77 23.49 25.47 22.73

Depreciation 7.72 -0.82 7.21 7.43 8.32 13.5 17.66 18.7 19.17 20.09 16.87 18.42

Profit before tax 6.09 15.2 15.53 11.19 5.77 8.27 38.01 -28.64 31.55 29.95 12.72 14.46

Tax 1 -0.09 0.1 4.99 1.27 3.09 11.41 -9.21 9.26 9.09 3.83 3.68

Net Profit 5.09 15.29 15.43 6.2 4.5 5.18 26.6 -19.43 22.29 20.86 8.89 10.78

EPS (unadj) 2.21 6.87 6.89 2.62 1.93 2.24 12.07 0 10.11 9.45 3.91

Dividend Payout 42.44 21.19 21 52.26 43.33 41.7 12.18 0 11.62 12.42 24.3

Historical return rates have not been anything fancy. The company has delivered low ROE, a reason could be accelerated wind mill depreciation but even without considering depreciation the return have been nothing great. The last three quarterly results have also not been significantly better.

What is changing: The company has build up a variety of technical clothing and ranging from consumer to defence related garments. The following categories are emerging from company’s technical textiles portfolio:

a) QuickDry and allied products to target the infant/child care segment: QuickDry is a consumer focused product and it is available through all major online shops (flipkart, amazon, firstcry). The company has also launched a set of allied products like reusable diapers, bibs, carrier etc. A major part of technical textile sales last year came from this segment. My expectation is that this segment can grow at 20% annually.

b) Defence: The company has been working with DRDO since last few years to come up with CBRN (Chemical, Biological, Radioactive and Nuclear) textiles. This is an import substitute product. Along with this the company has actively participating in defence tenders for the Ordnance factory board. Some of the other material that the company is working on are Aero Stat fabrics, High Altitude fabrics etc. The annual requirement for CBRN textile is between 50,000 to 75,00o suits by the Indian army. The current version is MK-V. High altitude textiles are of three types and the most complex are ones used in most high altitudes like glaciers.

c) Wulf bags: The company is in the process of launching backpacks and travekl bags with wulf brand.

d) B2B supply of technical textiles: The company manufactures multiple other technical textiles including canvas products, coated, polar fleece, terry fabrics, velour fabrics, activated carbon fabrics. The company is working with MNCs to figure out a B2B market.

Investment rationale: The company is focused on technical and value added textiles across segments and is moving away from the traditional business. As part of it the company is also demerging one of its units with 40000 spindles in a separate company. The operating margins in technical textiles are in the range of 20% to 25%. Further presence in defence and the kind of products that the company is working on shows company’s technical prowess. The promoters are highly respected and have conducted themselves in a very fair manner.

Risks:

a) The company is entering into unchartered territories. Some of the other companies which havbe tried similar experiments have failed (reasons could be somewhat different though). Some example that come to my mind are Precot Meridian and Lakshmi Cotsyn.

b) QuickDry has been in the market for more than 5 years and has not been able to go up in sales significantly.

c) Defence orders are generally lumpy and have huge bureaucratic issues. The time for defence orders to materialize can sometimes stretch to years.

d) The company’s historical track record in wealth creation is nothing to write about.

Disclosure: Forms more than 5% of my portfolio. No trading in last one month.

Links: http://www.shivatex.co.in/sites/default/files/TheTextileMagazine(10).pdf

http://www.drdo.gov.in/drdo/pub/npc/2016/january/19Jan2016.pdf

http://www.cbrneportal.com/sharaba-the-new-indian-cbrn-permeable-suit/

http://www.wulf.co.in/

http://quickdry.in/

STYL-Products.pdf (984.9 KB)