Yes, the company’s annual report has this typo.

Why the company not made any intimation to the exchanges regarding the news of winning defense order worth 55 Cr ?. Because there are no announcements regarding the orders in BSE.

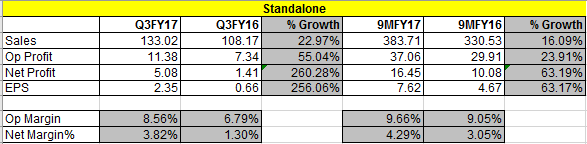

Q3FY17 Results

5 Likes

Looking for the exact volume of IKEA shipments from Shiva Tex.

Anyone has a subscription for this service ? I can see names like Shaily and Trident who are known IKEA suppliers. Thanks in advance.

1 Like

@Anant Since you tracked this closely, thought you would be the best person to address this.

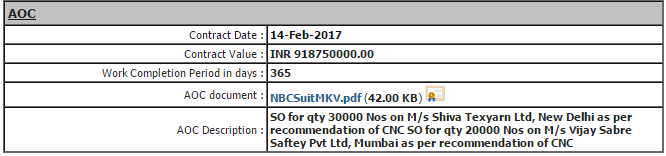

When I look into the final AOC (Award of Contract) acceptance, I see a date of 14.02.2017 with a 1 year period, which ideally means the revenue would accrue in sometime in Q1-Q2 of 2018, and not earlier as we were expecting, Kindly let me know. Thanks

2 Likes

I think a part of this will accrue in Q4 and remaining in Q1/Q2 Fy18. Anyways a quarter here and there is of no significance

Thanks @Anant . Just helps in aligning with revenue expectations  for forthcoming quarters. Otherwise of no larger significance.

for forthcoming quarters. Otherwise of no larger significance.

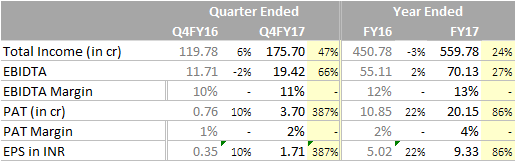

Results are good. Annual debt reduction is 22 Cr which augurs well against reported full year earnings of 20 Cr

2 Likes

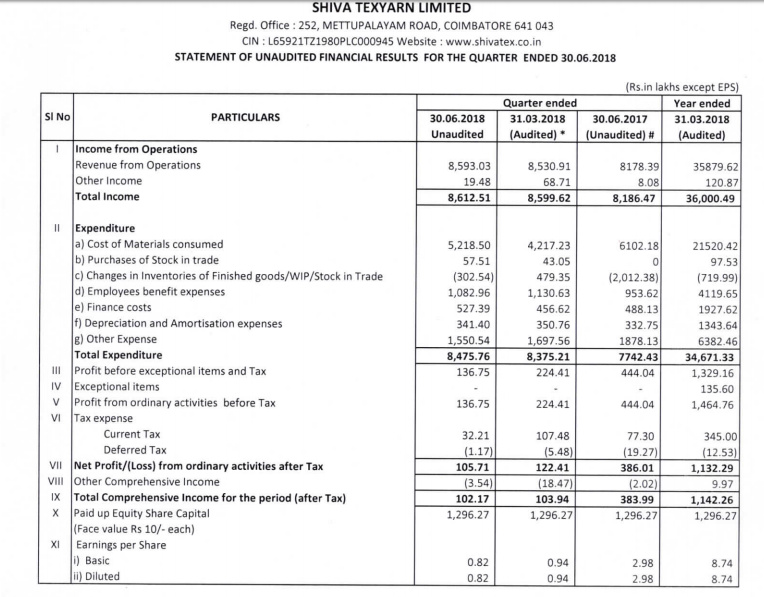

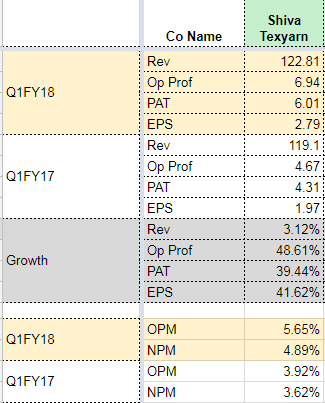

Q1 Results for Shiva -

2 Likes

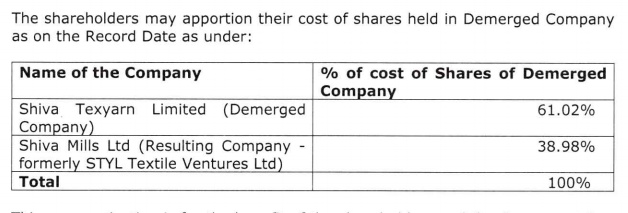

Details about the Demerger including the share distribution ratio

http://www.bseindia.com/xml-data/corpfiling/AttachHis/8f77e610-e8ef-4c14-b006-cc63d0a4c28a.pdf

Best

Bheeshma

Sharing notes from Shiva texyarn agm :

Mr. SK Sundararaman in his opening remarks expressed excitement in welcoming everyone to his first agm as MD of the company.

Shiva texyarn has 2 divisions:

-

Coating division: Largest mfrs of painting canvas globally, supplying to customers like Faber Castell etc.

-Mgmt expects reasonable to stable growth. -

Lamination division:

-Focus area for medium term (next 3-5 yrs).

-In the process of ramping up employee strength.a)Quick Dry : No.1 in the country. Foresees strong growth over the next year.

b) Military Production unit:

CBRN: Completed half the order qty for cbrn suits from Indian army. Balance qty expected to be completed by Jan/Feb. Hopeful of continued demand over the medium to long term from Indian army.

High altitude suits:

i) 0 to -20deg : Extreme cold conditions:

Shiva tex has qualified as one of the two Indian vendors in a global bidding process

ii) -20 to -50deg : Super High Altitude terrain (ex: Siachin): Shiva tex is one among 6 global suppliers short-listed for Indian army & is awaiting technical clearance (end user testing during current winter season is in progress).c) Heavy Stitching unit: Compliance/quality norms from customers like Ikea are very stringent.

-Working on developing new products for Ikea & engaging with Decathlon for new products.

-Expect 100% growth over the next 3 yrs.

Management said they would continue to focus on product innovation, catering to niche segments in technical textiles.

Discl: Forms >10% of my pf. No transactions during the past 90 days

15 Likes

Any updates related to the listing of Shiva Mills ? Kindly share if available.

I had spoken to Company Secretary and he was confident that listing of Shiva Mills should happen in last week of Feb

2 Likes

Good to see fairly detailed investor presentation from Shiva Texyarn →

https://www.bseindia.com/xml-data/corpfiling/AttachLive/786c5454-375b-465d-bf5e-871050f16daa.pdf

Good to see management laying out a little bit details about industry & more importantly laying out future growth plan. Hope to see investor presentation every quarter from hereon.

Another interesting thing is difference in two valuation metrics, namely EV/EBITDA (13) & P/E ratio (44). I’m hoping one good year will take care of the debt/interest outgo.

Disc - I continue to hold, > 10% of portfolio.

4 Likes