I feel the bigger challenge will be knowing when this capacity expansion cycle ends and the supply starts exceeding the demand. And with relatively more supply being added in the next year or so the margins would take a hit!

3 Likes

2 Likes

Can u please share your insights on how this article is related to Shilchar…

we can look a bit differently. Data Center will drive power demand. More than 50% of new power is being generated via renewable sources and that is where likes Shilchar and Danish Power specialise

2 Likes

I don’t really think data centres will demand so much power. Generally with each release cycle of new chips they are more power efficient along with processing capacity.

We should take these articles with a pinch of salt. With so much capex going on I would rather wait a little and see how the supply demand scenario is shaping up.

1 Like

Power demand future aside, there is another interesting chart I shared the link for…age of grids.

Pasting the screenshot here

Regarding the kind of demand… it is a race right now. B200 is rated at 1kw and it is fully booked for 2025. Current h200 gpus are rated 700W for reference…Sovereign AI is just beginning. Efficiency improves gen after gen when you are only pushing the nodes while the demand is at usual rate. This is abnormal demand scenario where hyperscalers and enterprise is plonking whatever comes in. The concern about power is only starting now.

3 Likes

Keeping all the froth aside, we know Shilchar has Capacity Constraints, even at peak demand revenue potential is more or less fixed because of that. They’ve already clarified they’ll be able to do 550Cr for current FY, and around 700-750 for the next FY, even if they decide to come up with another capex, it’ll only be operational in the next to next FY, this comes from the the time they took in capex that recently got completed. Don’t you guys think chances of re rating are impossible, at current valuations.

8 Likes

I think the power demand for DCs is not only driven by the new chips or the AI itself but the adoption of AI by more organizations.

- AI need stronger computing power/capacity which needs more power. But this, as you said, may be offset by the more efficiency by newer chips.

- AI by itself provides more incentives for more and more organizations to go for IT computing. This is the main driver for power demand increase that we see today (and likely to see in near/mid future), in my opinion.

4 Likes

I think we do not need to bother about this at least for next 2-4 yrs as the below 2 factors are main driving force for demand and making the demand explode. I learnt this from various news that captures the experts opinion.

- AI adoption and the need for more power for AI itself. Data Centers are required to upgrade their power sources.

- More push for renewable energies. Renewable energy installations are more of scattered in nature by the virtue (as opposed to thermal energy which can be generated in lesser number of plants). This requires different kind of distribution infra that needs more/different transformer infra.

8 Likes

Picking up from here, does anyone have any update on whether the company is planning to do further capacity expansion? They informed in the last conference call that they’ll be taking a decision on that by December 2024, based on the demand for their product. We haven’t heard from them since then, would anyone mind asking the IR team of Shilchar about this, if they are in contact with them.

Thanks.

1 Like

All shares have fallen…market is discounting nothing but just retail investors are in panic mode .In this kind of environment nobody who sells is thinking about the company prospects .

2 Likes

Investment Thesis: The Indian Transformer Industry – A Power-Driven Growth Story

Key Drivers of Growth:

- Strong Domestic Demand: Rapid infrastructure development, national grid upgrades, and state-level investments are driving consistent demand for both power and distribution transformers.

- Renewable Energy Expansion:

- Solar capacity additions are projected to grow from 15 GW to over 50 GW annually over the next 6–7 years.

- Expansion in solar, wind, and other renewable energy capacities necessitates grid-level and distribution-level upgrades.

- Government Support:

- Significant grid-level investments by Power Grid Corporation of India Limited (PGCIL), with investments expected to double over the next 4–5 years.

- Favorable policies aimed at modernizing energy infrastructure.

Emerging Opportunities:

- Export Potential:

- Ageing grid infrastructure and supply constraints in Western countries (US, Europe) are creating strong export demand.

- Indian manufacturers are well-positioned to meet global requirements for renewable energy-compatible transformers.

- Sectoral Capital Expenditure:

- Traditional industries like steel and cement are increasing their investments.

- Emerging sectors such as data centers and corporate green energy solutions are diversifying demand sources.

Market Segmentation:

- Power Transformers:

- High technology requirements and stringent pre-qualification norms.

- Demand primarily driven by central government and industrial capex.

- Distribution Transformers:

- Fragmented market influenced by state-level spending.

Industry Outlook:

- Supply Constraints & Improved Realizations: Global supply shortages continue to improve realizations for Indian manufacturers.

- Diversified Growth Drivers: Combination of domestic infrastructure upgrades, renewable energy adoption, industrial expansion, and export opportunities ensures long-term growth.

Conclusion:

The Indian transformer industry is at the cusp of unprecedented growth, backed by robust domestic demand, renewable energy expansion, global supply constraints, and significant export opportunities.

Companies like Shilchar Technologies are strategically positioned to capitalize on these trends and play a key role in India’s energy evolution.

Source: Shilchar Technologies AR 2024

4 Likes

I think their October’24 Concall has a clear guidence which is missed:

Quote:

Coming to the company updates, after fully utilising our 4000 MVA capacity last financial year, we have

successfully commercialised an incremental 3500 MVA capacity in August 2024, taking our total installed

capacity to 7500 MVA. The results of this expansion are already becoming evident. We observed a notable

increase in production during September, contributing to both year over year and quarter over quarter growth

in Q2.

Unquote:

But the falling price of the stock and that too repeated lower circuits create doubts whether any negative insider information is leaked or what?? Otherwise, since last 12 quarters their revenue and Net profits have excelled YoY.

Disclaimer: Invested

5 Likes

Shilchar results announced. Investors might now wait for concall & further expansion plans.

1 Like

Management is on track to deliver 550 cr in rev for FY2025…

Should be a cakewalk to hit 550 crores. Also what needs to be seen is what was the capacity utilisation with added capacity. One shouldn’t consider a straight line impact immediately in revenues. But that’s how I look at the results.

Different investors might have different take on the results but mostly seem to be inline.

At peak capacity utilisation before capex they were doing 400 odd crores annual revenue.

One can do the maths. The story remains intact.

But really think management should do a concall & give further visibility on capex if planned & business overall.

Disc: Invested & biased

5 Likes

Had put a few queries to the investor relations team & attaching their response to the same

Disc: Invested & biased

21 Likes

What I have oberserved from the result was the stark increase in cost of raw material to proportion to sales, It was around 66% in q3 ,compared to 59% in q2 and 62% in 9M FY2025,This might have been the key reason for fall in margins will need clearity from the management on where they see these costs heading.

1 Like

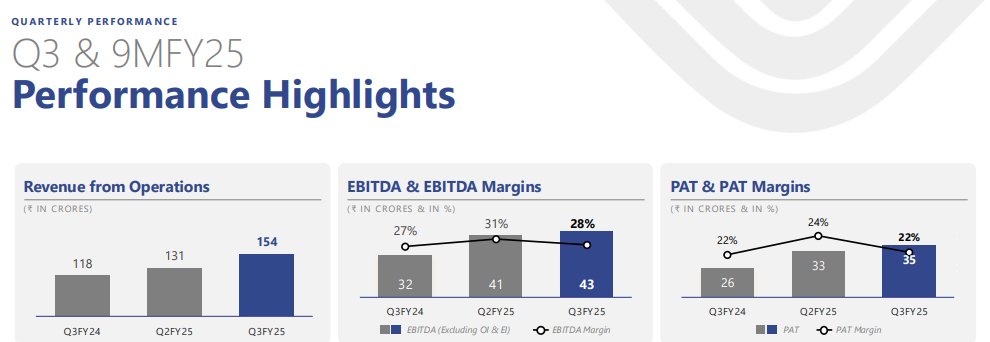

Shilchar Technolies Q3 FY25 - Investor Presentation

- CRGO Steel cost to moderate as BIS has renewed licenses for several CRGO suppliers and no challenges in CRGO procurement in the foreseeable future. This should allay the concern of spiralling RM cost denting the margin.

- New capacity to fully reflect in FY 26 results as the new capacity from 4K to 7.5K is getting ramped up.

- Sufficient land parcel available to build capacity to 30K MVA.

- Suppliers of Power and Distribution Transformers upto 66 KV class.

992bb31d-8c2e-4d5d-af38-2603e333f50e.pdf

Discl: Invested

9 Likes

Below is from the investor presentation:

As per the same, the new capacity is fully utilised in Q3 which gives revenue of ~155CR with PAT margin of 22%.

If we extrapolate it to full year, it would be ~620CR (which management guides to 750-800 and i assume they would be right but it cannot be more than this) and considering 800Cr rev, the PAT to be ~180Cr.

With this, the stock runs at the 25-30 forward PE, which is quite expensive given no further growth visibility, until management announces further expansion plan.

Disc: Not invested but got interested in overall sector story and recent corrections in all these stocks. Tracking others too, but still feel these like SHilchar, Indo Tech, Danish are quite expensive at these levels.

1 Like