A look at the macros first, w.r.t the industry -

Domestic demand

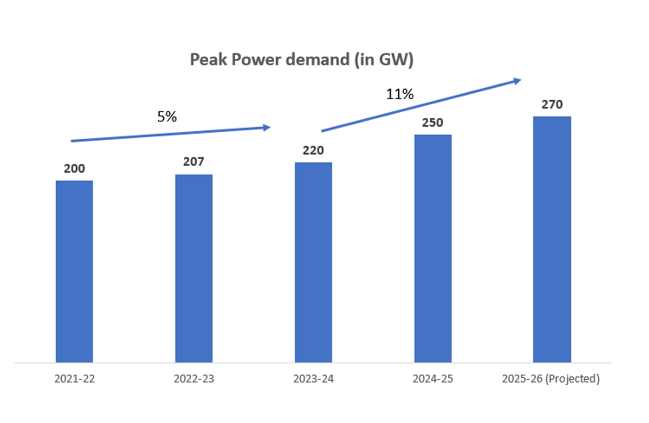

We successfully met an all-time high peak power demand of 250 GW during 24-25 ; this is expected to increase to 270 GW by next fiscal year. Further its likely to soar to 446 GW by 2030, as per CEA estimates. Clearly its increasing at a faster pace now vs the 5% CAGR achieved between FY 22 and FY 24 (Source : CEA and Powermin website).

Exports : Multiple elements driving demand like replacement of aging infrastructure, EV adoption, renewables demand in Middle East, etc

This Forbes article cites – ‘Unprecedented imbalance between supply and demand for transformers in US‘ with analysts estimating the problem to persist till Q4 of 2026.

Budgetary allocation for the sector

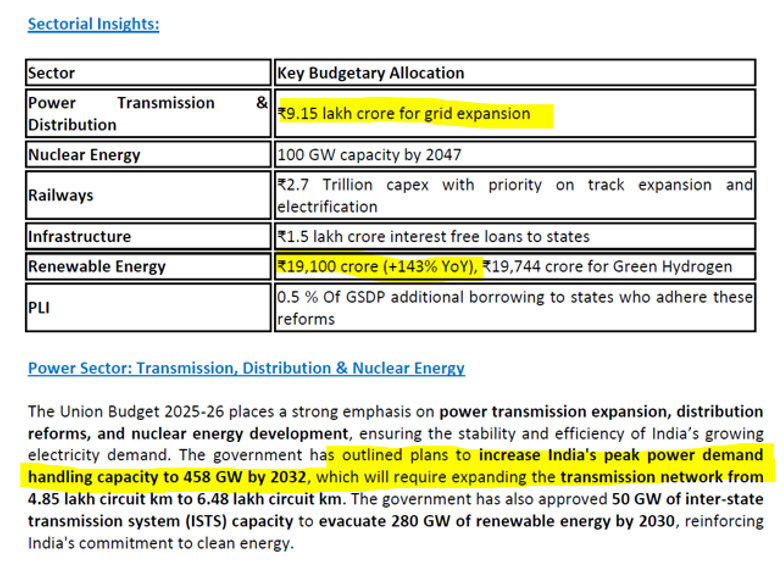

TARIL released a note on key budgetary allocation and growth opportunities for the sector. Highlighting some key stats :

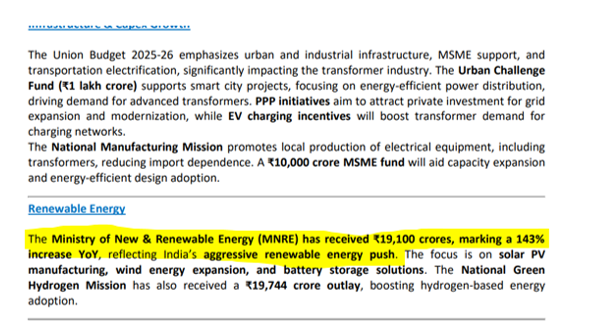

Renewable energy : 143% increase YoY towards Renewable Energy

Most of the capital goods companies have seen a very sharp correction in last 3 weeks or so. Concerns on lower capex spends in the Budget being a factor perhaps, it got exacerbated further for companies like Shilchar owing to low float.

The slowdown in capex spends was primarily due to relatively lesser activity in Q1 (owing to elections, etc). However, Dec 24 capex figure of 1.2 lakh crore is actually higher than the monthly run rate for 9 months (from Apr to Dec 24) around 76,000 cr. This gradual uptick along with the budgetary allocations mentioned above, provides belief that capex story is intact for next FY.

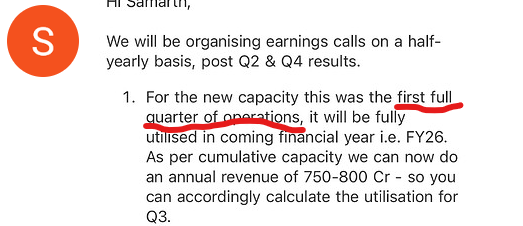

Coming to Shilchar, they will look to utilise the incremental capacity (commercialized in Aug) in FY 26.

They take 6-8 months to put up and commercialize new capacity, so even if they were to announce it in April / May - its should commercialize by Nov 24. Knowing the management and their prudent capital allocation strategies, they are likely to put up the additional capacity, catering to segments with lesser competitive intensity such that the margins remain intact.

They have indicated 750 to 800 cr as the peak revenue potential from the incremental capacity in place, in FY 26 - that would mean roughly 40% growth over FY 25 (this is without factoring in any contribution from the incremental capacity that is probably on the cards)! And an Operating Profit of more than 200 Cr. Both domestic and export demand remains strong, as alluded to by the management too, in the last call.

So consistent 30%+ growth at relatively higher margins than peers. With no dilution so far and with marginal institutional ownership! Some of the peers with lesser margins trade at higher PE multiple.

Disc: Invested; added a small quantity in the recent correction