12 Likes

The management has been consistently under promising and over delivering. Their margin profile and assurance that they would retain these margins is very comforting.

For every GW of installed capacity, similar transformer capacity needs to be added. So the TAM in India itself is huge and then there’s huge opportunity knocking in US and EU.

4 Likes

But as they have said if operating at full capacity they can only achieve as much as 750-800cr of revenue in an year. To get benefitted from this increasing TAM they need to rapidly expand their production capacity, but then they also need to address the fact that this demand may not last forever, so when it actually dries out what are they going to do with the incremental capacity they have added through these years. Many companies depending on the Energy Transition boom are in this stage where they need to address this before deciding how fast they can expand.

2 Likes

Shilchar announced previous expansion in February which got commissioned in Aug mid. There’s a likelihood that they might announce another post q3 results or before and that might get commissioned in next mid FY. The management also alluded to that.

The management can be called conservative but the reality is that they are excellent when it comes to operational metrics as well. Fully aware that they’d probably hit 100% capacity next FY, they’d have a capex done sooner than we can put a finger on. What remains to be seen is q3 numbers and q4 numbers.

Ideally if demand is robust they should easily hit a revenue of 600 crores this year.

Note: Second biggest holding in portfolio

6 Likes

I think they are going the right way and building capex as per the requirements once the already built capex is ensure to run with optimum capacity and have good order book in hand rather than going bust during some slow down… We have seen many a times in past in other industries like chem pharma very recently.

2 Likes

The management was clear when they mentioned that they will announce capex when they have future orders in hand, hence they are waiting for two months before they announce. The cautious approach is in fact very comforting for an investor as the management will take very calculated call on capex.

As an optimistic investor, I feel that the AI boom and manufacturing power that the country is striving to become, putting up power generation capacity is an inescapable requirement.

Cautious investors must wait for the capex announcement as valuations are rich.

5 Likes

Does something like this leads to increase in revenues as well as margins? Or the increase in revenue is offset by the increase in RM cost?

1 Like

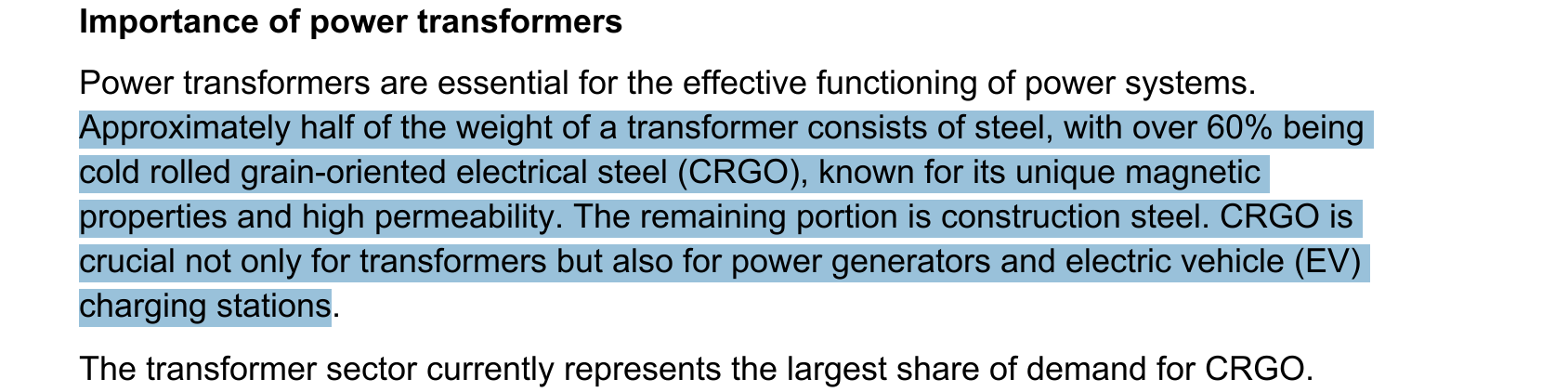

For Shilchar, management is not concerned about CRGO shortage, although voltamp clearly struggled with the shortage. Yes, increased demand always leads to increased topline, although not sure about margins, Shilchar is already sitting on industry leading margins not sure how much they can stretch from here. As soon as they get order they book the RM eliminating RM price fluctuations so increased prices of RM are already factored into order value.

4 Likes

The article suggests that the transformer companies will need massive capex to meet the demand.

7 Likes

Sometimes the price action is a very good indicator of fundamentals and upcoming developments.

1 Like

Continuing on point number 2 it really does not look very promising right now. Might do well for a few quaters but. Just being dependent on one thing hurts. With current political changes around the world. Things might slow down in this sector. Maybe shilchar should distribute thier eggs.

Power requirements are bound to grow and transformer shortage will be there but how much of that would attribute to renewables.

Maybe its time management rethinks the stratergy.

4 Likes

Hi Vivek, In your views, whats your comfortable valuation ? Any specific PE in mind and rational behind this. As most of stocks are down by 20-30% but its still not gone down as compared to peers. Appreciate your views,

Thanks,

1 Like

Please refer my post above Shilchar Technologies - Power & Distribution Transformers - Sunrise Sector? - #193 by vivek_17

As lot is priced in, for someone starting to buy now, one shouldn’t expect stellar returns, but yes fairly good returns.

Don’t treat this as an investment advice.

I have done my first buying in Jul 2023 and last I bought was in Oct when it was on discount around Dussehra.

5 Likes

The reason why the stock price hasn’t corrected much compared to its peers is because, though its full capacity utilization hasn’t been realized yet but the company is already discussing new capex. Just imagine the revenue growth visibility it offers for the next two years.

When they shifted focus to renewable energy, I think it was to cater more private companies, exports for better cash flow and margins. It was a strategic move at the right time, to capitalize the demand for clean energy infrastructure worldwide (but it was not their only business). And now the world needs even more power for the digital transformation/ data/ computing/ AI/ EV/ crypto/ energy security/ cost/ clean energy.

And this company’s annual revenue is below 500 cr, should be easy to double rev from here with similar margin. Investors are paying for the certainty, I guess.

Disclosure: Invested and biased

8 Likes

I am still unable to fully understand how Shilchar is able to maintain 30%+ margins, when bigger and established players are not able to hit even 20%.

I understand they mainly cater to the renewables sector, but what is so special about transformers for renewables? Does Shilchar have some technical advantages etc. which others in the sector don’t have?

The surprising thing is that even though they did a big capactiy expansion, still their margins are maintained. Normally, when do you a major capex, the margins take some time to move up as the new capacity is optimized, but Shilchar has same margin from day one… how?

I was analyzing the stock, but didn’t invest yet as I am not clear about this. I think they are at peak margins and there is significant downward risk to margins. Also, valuations are not cheap at all… So, if margins even contract by 2-4%, stock can correct significantly.

7 Likes

This is because of the highest % of exports they enjoy in the sector.

2 Likes

Higher margin is due to higher export share in the revenue. Getting approval in US and EU takes few years , therefore most of the competitors are not exporting like Shilchar.

3 Likes

Even I have the same question. Key risk is that can they maintain OPM of 31% and NPM of 25% with increased sales. Most other competitors are also adding capacity. If anyone can please throw some light on OPM and NPM for next 8-10 quarters it would be great.

Another thing, with Trump what is USA says that they don’t want to import but rather make in USA then what happens.

3 Likes