I have taken a lot of time to do this analysis. Would love to hear your views

The company has changed in a few different ways and that should be taken into consideration on the valuation.

-

The company lost a 150 Cr deal with ViaCom 2 quarters ago. Hence the unsold inventory that ViaCom did not renew has been added back to the inventory.

-

This is because media companies are going through a huge shift, with the introduction of NTO 2.0. NTO 2.0 causes lower subscription revenues AND subscribers to most channels and people migrate to Netflix/Amazon.

-

The ad industry is also lackluster due to low auto demand, putting pressure on media companies to curtail spending. Media companies react by cutting the most discretionary expense – buying new content, by postponing it for a bit.

-

The auto ad-spend is the one part that might come back, as economy rebounds. NTO 2.0 is here to stay.

-

The company has hence come up with guidance of severe pressure in profitability.

-

All of this analysis of mine and yours thus far, does not talk about the elephant in the room. The real reason why the stock price crashed like a ton of bricks is their ill-fated attempt to dilute like crazy and raise 250 Cr to start new initiatives.

-

Markets are asking if the promoter is freaked out so much about the pace of core business evaporating. As if to confirm market’s suspicions continuous de-growth in profits were announced right after, over the next 3 quarters. Management would be seeing the ad-rate CPM falling and perhaps feared renewals slipping and wanted to dilute the company by 35%; Investors have experienced dilution but never in such magnitude and there was a stampede on the way out.

-

The stock obviously is not available at 3x PE. Because the E is falling on every quarter results they announce.

One should buy considering all of these factors. It might still be a buy at some price afterall.

10 Likes

This is extremely helpful. Exactly why I joined this forum.Really good thoughts. Below is my views

1: Agree.

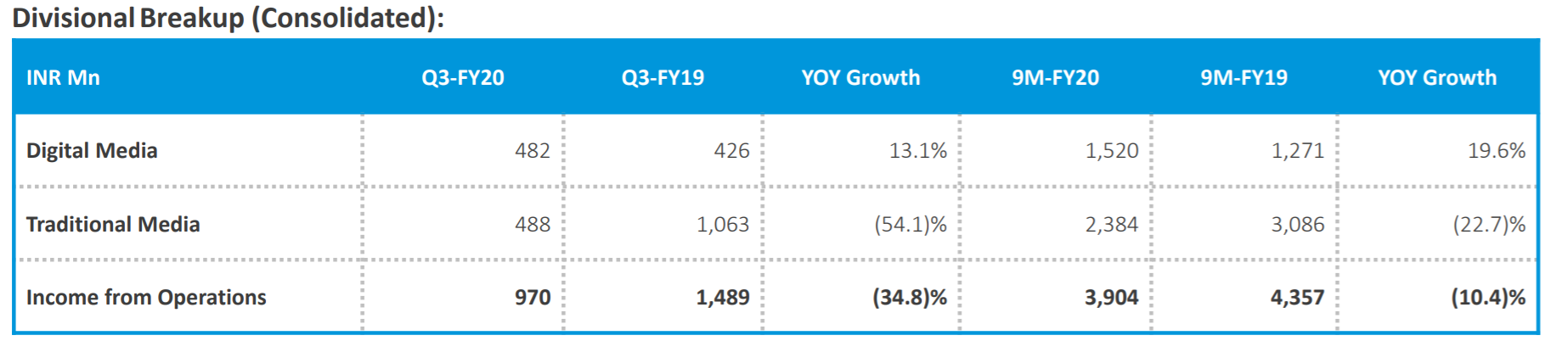

2: Company is now focusing very heavily in the Digital space. Currently traditional business account for 70% of the company revenue while Digital business account for 30%.

Now agree that most of the Bollywood latest rights are now a days bought by Netflix/Amazon however company has never focused on first cycle as a business model. It has always focused or bought moves after 5-yrs of release based upon performance etc . One thing we must remember is that Amazon/Netflix usually has time frame based rights and after few yrs of release they depend upon content aggregators like Shemaroo. With Shemaroo having rich library and contents and its continued focus on second and third cycle films, Amazon/Netflix anyway has to keep their tie up on successful movies with Shemraroo and the digital footprint should keep growing. Whats your view?

Also i was listening to Shemraoo management interview and they have mentioned that at some point they expect their digital revenue to cross tradition revenue. With so much focus and new launches and partnership, they should be in a good position to capitalize however i agree its wait and watch.

- Agree. I do expect say by FY21, the decline in traditional revenue to offset growth in digital revenue

- In last 9M results its Digital media has grown by 20% from 1270 cr last year to 1520cr this year

- Traditional media has contracted by 22.7%

With company Youtube and other digital model gaining grounds and i do believe it was a smart move by company, it will be interesting to see at what point the things stabilize which is not yet known as traditional media is linked to microeconomics factors.

-

Completely agree. I do expect NTO impact to be 25-30% at least for all traditional players.

-

Yes but this is the case with all the entertainment houses. All companies have come up with hard guidance on traditional segment and good guidance on digital segment. Impact of COVID in my view will be a propeller to digital segment as lot of people at home these days keep searching for things to watch and YouTube and other OTE platform should further increase its base.

I wont be surprised if after Q4-20 results, digital share this year of company is 40% of total revenue instead of 30% last year ![]()

6-7: Yes agree. Equity dilution has been a key factor for the price crash. Its a tricky to choose b/w Debt and Equity and company has adopted a approach which is not shareholder friendly so yes doesn’t send good vibes in that respect

- I don’t get your point. Its P/E of 3 its its declined revenue. I don’t think revenue can go down more than this ( maybe time will prove me wrong).

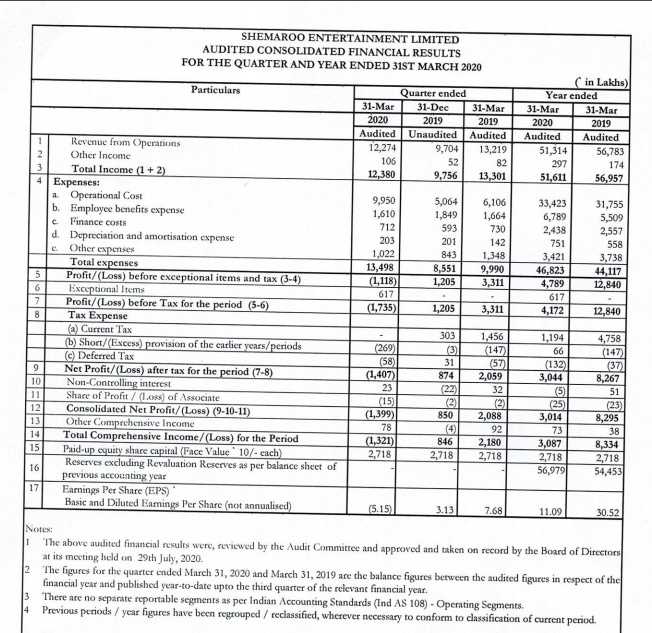

In Q3: PAT was 9.5cr with one time cost of new initiatives as 7cr included so excluding that it was close to 16.5Cr vs 20cr in Dec-18

On YTD basis out of 44cr , new initiative cost was 15.7cr so if we exclude this, its 60cr vs last year of 62cr. This new initiative cost is not expected to repeat next year so infact results are already quite conservative in recognizing the full cost upfront and showing lower profit.

What am i missing here please?

2 Likes

Also just to ad few more things:

-

On performance on YouTube continues to grow; Shemaroo Filmi Gaane was the sixth most

subscribed channel in India and 36th most subscribed in the world. They crossed 30 million

subscribers on YouTube on our channel Filmi Gaane and 20 million on ShemarooEnt. -

Traditional segment is highly cyclical in nature and linked to microeconomic factors. Company in their last concall did mention that they have been seeing certain sector specific issues getting resolved and there have been some improvement in sentiments since January thereof. Also they have taken various organization wise cost rationalization measures in order to offset the impact. Lets see their Q4 result when out. I am expecting digital to grow again QoQ and traditional to obviously decline. We have to exclude the new initiaitves one time cost which will be part of Q4 too to get a complete true picture and impact of digital growth vs traditional decline .

-

Many of their new initiatives are at nascent stage of investment and hence have impacted the overall margins. Most of these investments are expected to reach breakeven levels in FY21 as per the company so again a wait and watch game

-

Company gradual transition from B2B2C and B2C as per me is a game changer. Search online on Netflix model. It started too as B2B2Cand moved later to B2C. Company area of specilisation like Amazon/Netflix etc is very different as they focus on Second and third cycle which i was earlier highlighting. With this in mind they launched ShemarooMe at the end of the last financial year which is their subscription based OTT Digital platform working primarily on partnership model and

available on existing platforms like Telcos like Vodafone Play Airtel etc. as well as various newer

platforms. The traction on this platform so far has been encouraging as per company and as seen from their 9M FY20 result of digital segment post launched ShemarooMe globally and it is now available in 150 countries. -

Further strategic partnership with MX players for ShemarooMe and it also has been made available to Cloudwalker TV, TCL TV, Android TV globally and local devices in USA. Preloaded devices which were launched in Q1 of this financial year have also seen a very good response and

appreciation from consumers as per company. They launched two new preloaded audio speakers in this quarter which were Amrit Bani,which is a Sikh Devotional speaker and Sai Bhajan Vani.

Overall i think its a interesting space they going into and they have to get it spot on. Also i think the result shouldnot go down further from here as most of the new initiative cost has been factored upfront and digital space on which its betting should provide good growth

its difficult to price it after massive correction in price and result being conservative in pricing upfront costs ( exlcuding this we are almost at same YoY), i do think the true P/E at which its trading is even lower than 3 to be honest.

1 Like

-

I’m bullish on the stock and have invested a decent chunk of my PF in it. I’m a buyer at these prices. Probably from the new horizon seller, who keeps selling desperately every single day.

I’m going to focus on the bear case in this thread, to balance out how bullish you are.

I’m going to focus on the bear case in this thread, to balance out how bullish you are. -

I don’t share your clarity on earnings though.

If earnings have turned a corner, I don’t think the company will come out, as recently as 20 days back and say, profitability is expected to be under severe pressure. If your earnings are going to be higher than the last declared quarter, would you put out that press release? I feel it is to prepare for the bad news on the June quarter, which will be declared 4 months from today. -

YouTube has definitely been the sweet spot, perhaps for a while now and growth has been good there. Although last quarter, management came out and shared the actual revenue break ups for the first time. And YouTube is around 35% of the digital business. And digital is around 50% of these revenues post the digital crash. So YouTube is only contributing around 18% of the overall revenue. Growth in youtube should be seen in that context and expectations need to be tempered a little bit.

The rest 80% of their revenues are under attack. -

In my last post, I had detailed out the issues facing the traditional business. The ViaCom impact might not been fully felt in the December earnings so there might be some more pain to come on that – I do not know how much exactly. One reason why Shemaroo is such a great business is it’s operating leverage – i.e., it’s a fixed cost business and incremental revenues flow straight to profits. But it also works in reverse right now. If 150 Cr in revenues get wiped out, due to the lost deal, it is hard for me to believe the profitability loss is only 1Cr. Maybe more impact to come in the upcoming quarter? Also shouldn’t the 7 Cr be added back to the revenue, instead of profits directly? Last quarter as well, traditional revenues did fall by 50%, by 50 Cr but somehow the OPM% did not crash. Instead the content got pushed into inventory and debt went up by 30 Cr. This feels like funny accounting to me. If you look at their operating profit, which is revenue - cost of revenue, the cost of the content is marked within the cost of revenue. So are they not charging the content depreciation if it’s not sold? The management is saying operating margins are a constant, with a lot lower revenue, how is that possible? In this company, you are often left to wonder whether how management marks the inventory is correct and represents market reality.

-

They continue to buy inventory to fund the Marathi channel, and other new initiatives, even though there are no ads right now and the existing inventory remains unsold, causing cash flow issues and rising debt.

-

Digital media also is under attack and the segments of the revenue, here are shrinking as well. They have the telco business, which is the ring tones and mobile WAP etc, that was contributing 50% of the digital business a year ago, which has now de-grown to 25%.

-

And finally as you have mentioned are the new business lines that the management is funding. They have zero revenue contribution so far. On ShemarooMe there are deep pocketed players as competition and it’s a winner take all market and IMO Shemaroo doesn’t have a chance. The revenues here need to grow from 0 to substantial to make an diff to thee stock price of a 180 Cr company.

-

So overall, pretty much both digital media and traditional are shrinking, except YouTube, which is only 20% of revenues. In YouTube as well, CPMs have just fallen post Covid. How do you have clarity on earnings given this and how are you confident the bottom on earnings have been made?

-

Longer term as well, there is a question of whether being a content reseller / middle-man is useful as a standalone business. Markets are questioning that right now.

Disclosure: Invested hence biased. ![]()

7 Likes

A few points:

- Do not get enamored by growth in youtube subscribers. Youtube shouldnt be seen as the primary value driver. If you read this thread completely, you will realise that advertising on youtube creates most value for youtube and very little value for the content providers. You can verify this with youtube channel owners. Basically, its like running on a treadmill where you need to create a lot of content just to maintain revenues

- Advertising is a cyclical business which goes thrown to the woodchipper in a recession (like now) and does very well in economic expansion. Typically, buying advertising companies is similar to buying cyclical companies where we buy when they are trading at a significant discount to their tangible book value and sell during an economic expansion phase. Shemaroo shouldn’t be looked at differently (ignore their earnings, we buy cyclicals when earnings are low or negative and sell them when earnings look good).

- Shemaroo is not venturing into B2C space, management has clearly stated this. They are going to be a content provider and don’t have pricing power in their traditional business (look at their debtor days when digital revenues were not so high). Digital medium has better terms of trade

- Their recent foray into marathi free to air channel is quite interesting and it is something which you haven’t mentioned. If they can garner enough eyeballs, that will be a value creator as it would mean that they have moved up the value chain. I track weekly marathi market share data (as of now, they are have managed 20% market share but zee has maintained their close to 50% market share). You can track it here.

- The interpretation of equity dilution is incorrect. Management did an enabling resolution and never came to the market. They have previously stated that they wont dilute equity at low valuations (at that time, share price was ~200). So its unlikely that management will dilute now.

- To track the pre-loaded device business, I attend concalls of Saregama which are the market leader. COVID has hit this business bad! No to say that it won’t come back

- I don’t know how to track the number of eyeballs for the hindi channel of Shemaroo as BARC only reports top 5 channels and Shemaroo is not there (obviously!). If anyone can help me out here, it will be quite useful

Disclosure: Not invested

5 Likes

This was after, the shareholder yelling in the last conf call requesting management to do a buy to show “confidence” ![]() And then they go and buy for just 3L!!

And then they go and buy for just 3L!! ![]()

Blockquote

Sarvesh Gupta: So here again the question is if we are not able to sell as fast then why are we

continuing with our inventory purchase? Why not just probably sell what we have right now?

Hiren Gada: So, one more aspect to it is what that we did for example was the Marathi channel

launch. So to that extent we held back some of the inventory as well as we invested further in

that to make it a complete offering for the Marathi movie channel. So part of the inventory

addition is also to fuel some of these new initiatives that we have taken.

Sarvesh Gupta: And now you know coming to the issue of this the share price which is getting

battered everyday so my only suggestion is that now promoter should try to give some

confidence to the markets by either coming in and buying from the open market or you guys

doing the rights issue. The details of expenses that you have given that is good, but against that,

What is the revenues that we are going to have, Can you give some more details, I also think it is

high time that you guys are enthusiastic about the prospects going forward and that has to be

shown with money on the table in some way.

Hiren Gada: I will note down your suggestion because at this point I am not able to comment

beyond that on that aspect.

1 Like

Yes, I do understand that they never did the dilution. As soon as the resolution passed, stock reacted violently. The fear really wass around the magnitude of the enabled resolution relative to the market cap (250 Cr attempted raise for a 600 Cr market cap).

Hello,

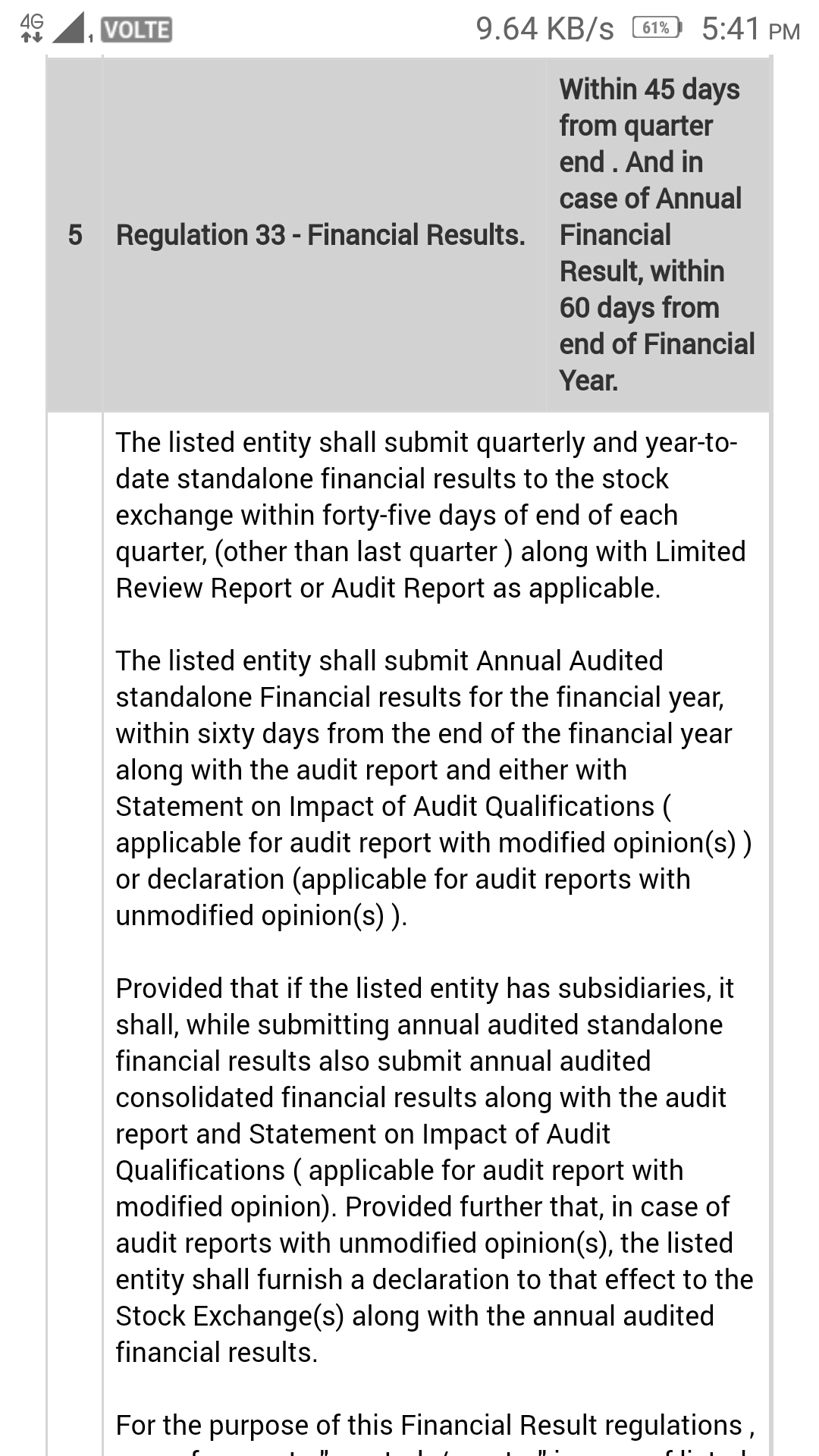

Shemaroo hasn’t declared q4 results as yet. I read on bse website that results must be declared within 45 days of end of quarter.

Can someone please explain.

Thanks

1 Like

I wrote to the company secretary and got a response.

SEBI vide its Notification No. SEBI/HO/CFD/CMD1/CIR/P/2020/106 dated June 24, 2020, has further extended time for submission of financial results for the year ending 31st March 2020 till July 31, 2020.

Accordingly, the Company will adopt its financial results for quarter/year ended March20. The same will intimate in due course.

Update: Company will come out with FY20Q4 and FY21Q1 results together

1 Like

Shareholding of retail (<2lacs) in Shemaroo has gone up considerably. Although this is not a good sign but retail participation overall in stock market has also increased in last 3 months.

Also, have started seeing some ads on their Hindi entertainment channel.

Overall, sitting on a 70% loss and not quite sure what to do.

It was expected, as expressed by @myprasanna explaining to us the covid 2019 statement issued by company

I request @myprasanna to guide on present statistics, debt, balance sheet, and how he sees the future of shemaroo

Thanks🙏

Hi guys,

Please make sure to join the conference call and ask questions to the management directly today at 2:30 PM. The losses were high and surprising, no doubt and the question really is when things will turn around. I look forward to management commentary on that.

Thanks,

-Prasanna

1 Like

I was not able to join the conference call, if someone can post details of conference call

Recent management initiative, pay-per-movie at Rs. 100 for new movie rental for three days.

Hello Prasanna,

Would request you to share your thoughts on the latest result and concall. Heard you in the concall.

I think the management sounded non-commital on most things but am unable to pinpoint exactly what is going wrong for the company.

Thanks

Hi Sarthak,

As you can see markets have delivered their verdict on the results.  Stock is continually on a lower circuit with no end in sight. I’m down ~30% on the stock and is my largest position. I sold 10% of my position when the results came out.

Stock is continually on a lower circuit with no end in sight. I’m down ~30% on the stock and is my largest position. I sold 10% of my position when the results came out.

I think Shemaroo offers excellent value, if the 400 Cr of movie buying in FY20 that they did was actually a proxy for owner earnings. i.e., If it is freely distributable cash that management chose to deploy in buying inventory for the new TV channels. Then it’s a complete no-brainer, with a 150 Cr market cap. I don’t know how to fully establish this.

And the other issue with Shemaroo is if it’s a fraud or not. All earnings accumulates as inventory which produce lower and lower EBITDA per capita over the years. I am unable to explain this. So just like Zee, is Shemaroo also manipulating the accounts? Again, IDK how to fully establish this.

That’s the risk/reward on this trade IMO. And I continue to like it barring the bleeding.

Thanks,

-Prasanna

3 Likes

One additional data point is that Shemaroo seems to be losing market share in their marathi market over the past few weeks, they used to feature in the top-5 channels and in the last week they are out. Colors has come back with a bang. I am not sure how cyclical this is, Shemaroo got their peak market share in the last week of May (~21%), which went down to ~11% in the week of 11-17 June.

1 Like