I haven’t been following the company at all for the past year or year or so. Maybe @dd1474 can help.

With current regulation by SEBI, where any kind of encumbrance also required disclosure to stock exchange. Hence, structure deal which provided non disclosure undertaking along with guarantee with asset cover is also need to disclosre to stock exchange to best of my knowledge. I am enclosing SEBI circular related to this and this is my reading and understanding of SEBI circular.

https://www.sebi.gov.in/sebi_data/meetingfiles/sep-2019/1568030483196_1.pdf

Hence, only way in which promoter can disguise pledge is to have holding through asscociates which are not technically covered in promoter definition (nor do they get disclosred as promoter holding to stock exchage) and pledge by such entities/individual of such holdings.

In particular case of Shemaroo, to best of my understanding, I believe promoter have not done any such sort of arrangement. The sharp fall in price is due to weak Q3FY20 performance and also moving into various new business area, from Marathi channel to Device to Restaurant etc which result in uncetainity in mind of investors. The change in business model would result in churn in investors holding. For instance, I was comfortable with Shemaroo buying digital content aggressively and gain from distribution of life. However, I was not comfortable in business when management intend to move into Device and movie channel business which resulted me to change my view on company. I sold Shemaroo material holding in November 2019 post Q2FY20 results. I still hold nominal holding in the company.

Discl: Not a SEBI registered advisor, View may be biased due to my dealing and holding in the company. Investor shall do their own due diligence before making any investment decision. It is not a recommndation of any kind on the company.

10 Likes

Can anyone share shemaroo marathi bana trp,weekly impressions

1 Like

At current situation promoter should have come and bought shares from open market

2 Likes

To begin with, I must confess that I got carried away by the excitement shown by VP Seniors on Shemaroo. It is completely my mistake though, that I couldn’t / didn’t keep myself abreast of the paradigm shift happening - be it reduction in Ad rates or di(w)orsification by management. Alas! The losses would be huge. And I am not blaming anybody as I myself am responsible for my actions.

The share price has fallen from all time high of 550 (approx) in Jan 2018 to 50 now. Thats staggering 91% fall. Does the change of business environment and/or business model warrant this? Going by the logic that Mr Market knows something that we don’t - what are we missing here? @bharat19, @dd1474 Kindly share if anybody knows anything or has any views.

Bharat Shah made very valid points about investing in inferior asset.

Good asset can underperform in short term in their journey towards wealth creation, inferior asset can outperform in short term in their journey towards wealth destruction. Inferior asset rises faster than good asset and its this fast rise that gets you instant gratification and if you indulge in this game u disturb your investment process. There are many who does very well in entering inferior asset and exit them quick at the peak.

If you look at Valuepickr, many stocks which have risen very fast and fallen faster. In this process many made huge money who managed to enter and exit at the right time.

I believe market is see fundamental change in the way media business being run. There has been change from content reaching to customer through Broadcater. While still reaching to customer, the medium is changing from broadcaster to new streaming services much quickly. In that context, market is evaluating all business and giving current valuation. This is my thought process and may be completely wrong.

3 Likes

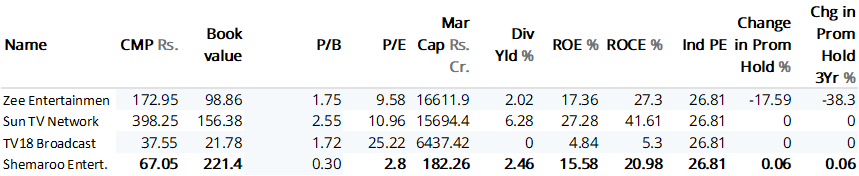

Company book value per share is at Rs ~220 vs market price is at Rs ~45/-, company should go for buy back instead of doing some new risky ventures. It will give boost up confidence level of retail investor about their strategy else it represent their balance sheet doesn’t reflect the right picture.

2 Likes

Hello

I think closure of cinema halls and gatherings is a big positive for shemaroo as people will have more free time and other avenues of entertainment would be closed.

That could be the reason for recent spike…

Will Shemaroo get positively impacted due to crisis arising due to Covid 19 ?

More likely ad rates will come down further and dent the revenues. ![]()

2 Likes

Looks like the shares have been under non-stop selling pressure since the big FII - New Horizon Opportunities Master Fund - has been selling:

https://trendlyne.com/equity/share-holding/1217/SHEMAROO/latest/shemaroo-entertainment-ltd/

They still have a lot to sell left, it looks like!

1 Like

Any idea about recent price momentum wherein all economic activities are on standstill…

Hello,

Shemaroo has launched shemaroo marathibana and shemaroo TV. But on both channels, I don’t see a single advertisement. Also, the channels are free. Just wanted to understand how does shemaroo make money from the two channels.

Thanks

From the advertiser’s perspective

While the FTA space is driven by advertising, brands at this moment are cutting down on spends. Shemaroo doesn’t have advertisers on board right now but the conversations with marketers have been positive, shared Gada.

“Fundamentally, advertising follows viewership. So it doesn’t matter if you’re a new channel or an already-existing one. There may be some relationships and legacy deals in place but today, TV advertising has become much more scientific. When we mapped the FTA space post the new tariff order, we realized there’s a natural opportunity opening in the space to capture a considerable share of the estimated Rs 2,500 crore FTA advertising market. Also, with leading broadcasters pulling out from Free Dish, Rs 1,000 crore of advertising opportunity opened and was potentially available for existing and new channels in the FTA space.

Hi All - i did investment on this stock last week friday. Sharing my analysis as below

Quick Snapshot

CMP: 67 as of 20th June

Market Cap: 182Cr

P/E : 2.8

Div Yield: 2.46%

ROE: 15.58%

52W H-L: 399/40.25

History

-1962: Started as a book circulating library in Mumbai

-1993 to 2003: Entered broadband syndication business, Digital production and entered overseas market for distribution.

-2005: Evolved into a content house by acquiring perpetual rights.

-2008-2009: Started content distribution to MVAS and digital platform like YouTube.

-2014: Listed on NSE and BSE

-2018: Refreshed the brand identity after 55 years

-2019-20: To enhance digital presence with growing trend, it launched Shemaroo ME OTT application

Segment

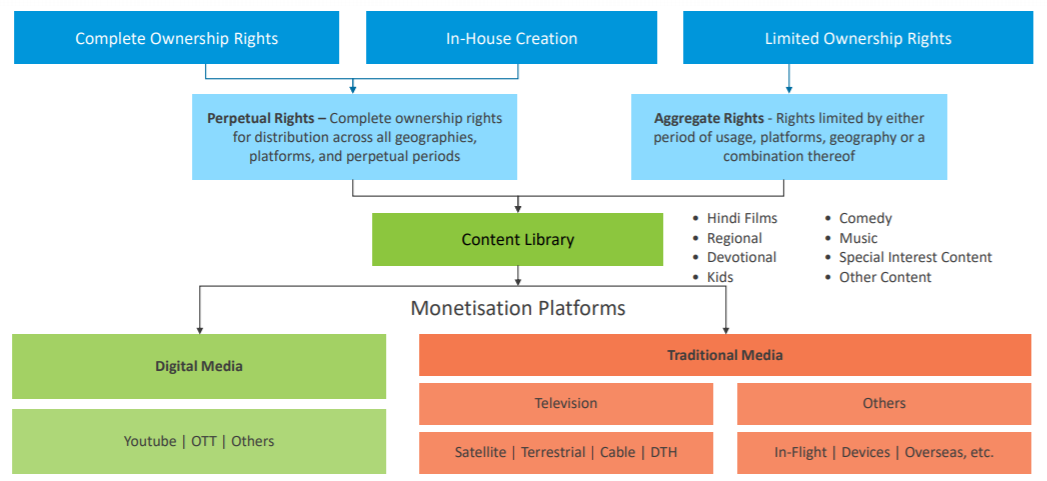

Shemaroo is a content distribution house which participates in the second and subsequent cycle of film monetization i.e. in simple words post a firm is released, it takes right of the firm ( perpetual / aggregate rights) and monetize it.

Risk is obviously lower as you can think of it like film is already released, the company already knows the review and performance of the film in the box office and its just acquiring right to now distribute it when its confident that it can generate desired level of Return on investment (ROI) by acquiring that film.

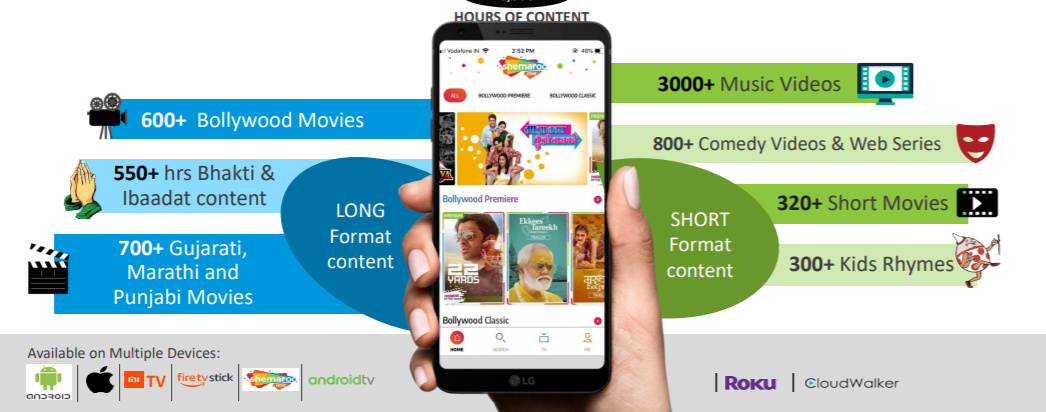

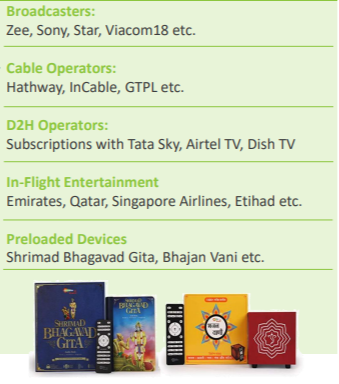

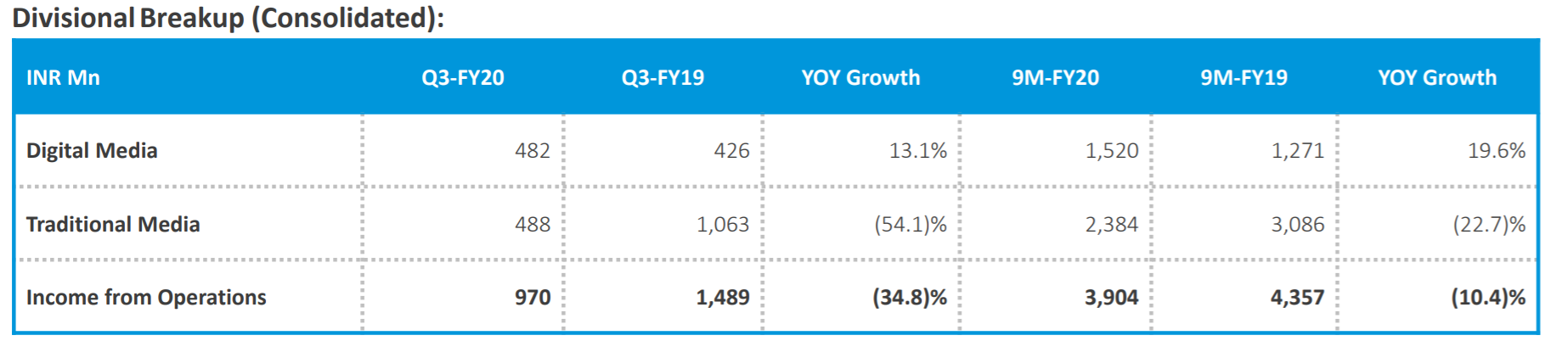

It then distributes these to the (1) Digital Media and (2) Tradition Media platforms

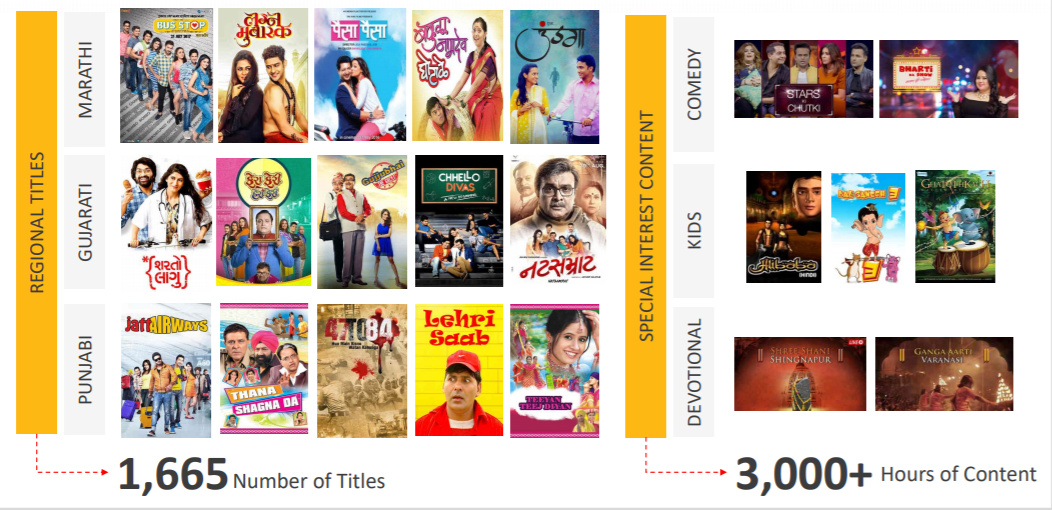

As taken below from annual report, we can see that it has perpetual rights for nearly ~1195 firms and Limited ownership Titles for 2756 films as of May2019 taken from its annual report. Given the vast library it has , it can be assumed that all major distribution players have had relationship with Shemaroo in some time in past and this also give company a unique advantage to the company in this fragment industry to monetize on this .

Below taken from investor presentation of the company gives a good idea regarding the business model of the company.

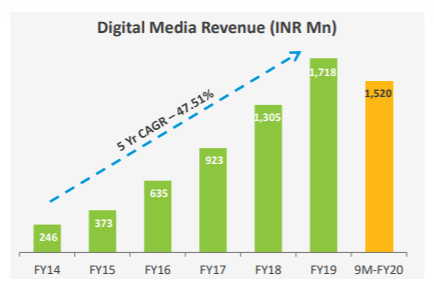

(i)Digital Media : Contributes ~30% of the company revenue with CAGR of ~45% in last 5yr.

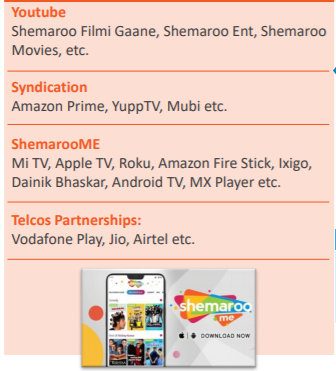

Below are some of the platforms company is currently publishing its content to:

Youtube

ShemrarooME

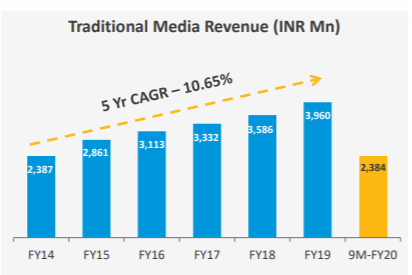

(ii) Traditional Media : Contributes ~70% of the company revenue with CAGR of ~10.5% in last 5yr.

Below are some of the platforms company is currently publishing its content to:

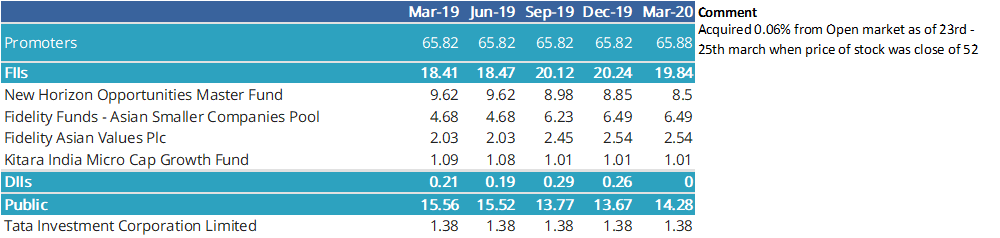

Promoter Holding

- Promoter holdings has increased by 0.06% marginally in last one quarter and promoter holding is quite good at 65.88% as of March-20

- FII’s good funds like Fidelity and New Horizon has almost 20% ownership in this company which has been quite consistent with time.

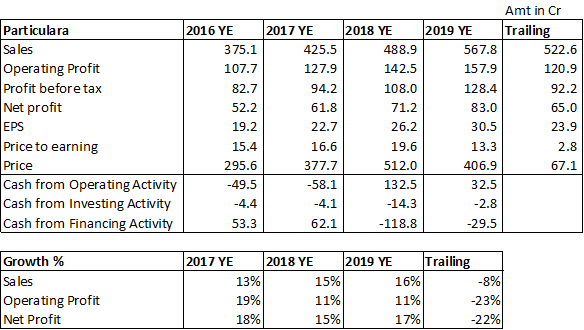

Financials

- Financial performance has been quite good. It has increased its sales every. This year its revenue has been impacted mainly due to traditional media due to COVID . COVID has impacted consumption hence also decreased advertising spending.

Interesting thing in its financial has been the growth in Digital media inspite of the slowdown. Shemaroo management has said in past also that at some point in future it expects its digital media to overtake traditional media. Given the digitization focus of the company company has taken multiple steps for future growth.

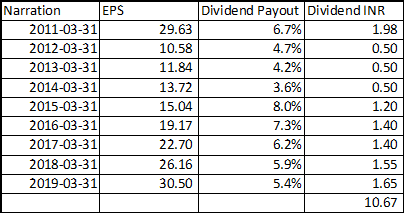

Company has also paid a good dividend of 10.67 in last 9yrs. Its currently trading at Dividend yield of 2.42% . This dividend payments are expected to continue given the growth of the company and consistent positive cash flow.

Future growth drivers ( many initiates taken by company. Just few given below) :

-

Company has launched Shemraoo Me ( You can find this is Apple and Android store…do download this to check it yourself )…this is now available in 150 countries.

-

Signed strategic partnership with MX player to enhance its digital footprint

https://www.televisionpost.com/mx-player-inks-strategic-in-app-partnership-with-shemaroome/

-

Its now available in Cloudwalter TV, TCL TV, Android TV globally

-

Youtube has contrinued to grow and its the 6th most subscribed channel in India. It has crossed

-

30Mn subscriber on YouTube channel ‘FilmiGaane’ and

-

20Mn subscriber on YouTube channel ‘ShemarooEnt’

Overall in terms of revenue the performance of the company has been very strong

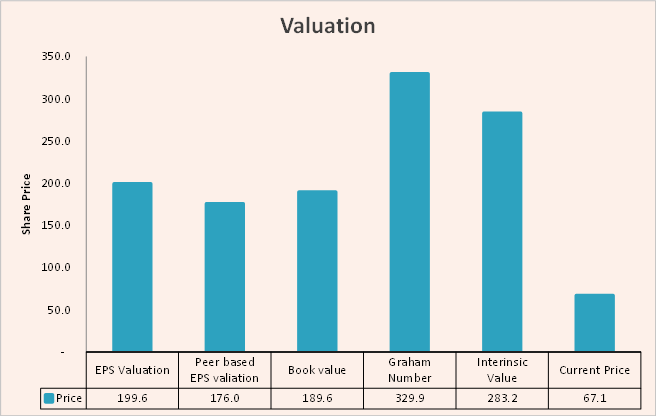

Valuation as per different methods:

Looking at the valuation right now, we do have a chance of more than 100% upside. These evaluations are made under certain assumptions which are given below.

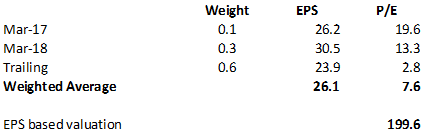

- EPS based valuation:

Shemraroo has been historically been trading at a P/E of 10-15 as an average over the last 2-3 yrs. Lowest P/E has been 2 vs 2.9 its currently trading at and highest has been around 22.

We have a fairly good upside of ~200% on this stock-based upon EPS remaining the same over the next few yrs ( which is quite a conservative assumption) and P/E reverting back to somewhat normal of 7.6 times instead of 2.9 times currently more inline with the past historical average.

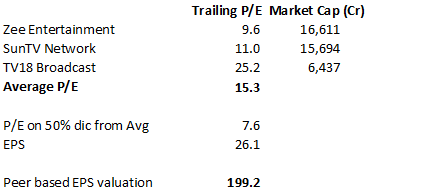

- Peer-Based Valuation

Again we have got a 200% upside against Peer-Based valuation under a conservative 50% discounting to average P/E of the Peers. This I have done as I have highlighted risk earlier of COVID impacting consumption

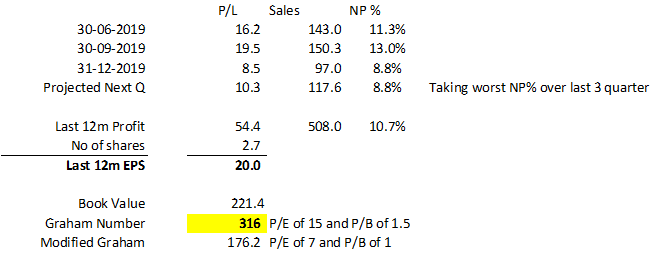

- Graham

Looking at the Graham, we will come up with a much higher valuation of INR 316. However, the Graham formula has certain flaws like P.E of 15 and P.B of 1.5 is assumed

this is obviously going to show the stock as massively undervalued. However, the core concept of Graham is still relevant, blind usage of the formula without understanding will not yield a correct result like below its yielding 386

In the below, I have modified the Graham formula to take a P/E of 7 which given the historical range of 2-22 and average of 10-15 P/E looks to be a much more reasonable and conservative P/E and P/B is assumed to be 1 given a growing company should always trade at least equal to its book value.

Given the modified Graham formula, I get a price of 176 which shows an upside of >200% in relation to the current stock price.

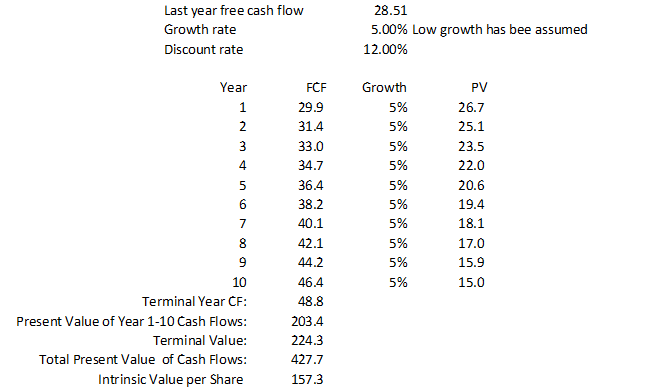

- Intrinsic value

Intrinsic value also is very good given a very conservative assumption of 5% growth in Cashflow and 12% discounting.

Below is the historical growth rates in Sales and Profit of Shemaroo. Given the impact on this year due to COVID and focus on Digital spending which has continued to show growth, company should be able to easily sustain this in coming months

- Book value approach

Looking at the book value, this stock is trading much lower than its book value as compared to its peers. In this sector a normal trend is to see P/B of ¬1.5 times to 2 times. Due to recent fall in price, its P/B has plunged to 0.3 times which is very cheap.

Risk:

-

Company new initiatives doesn’t kickoff the way it expects and if suffers on the digital front print. This looks less likely to be honest given the focus company has on digital media esp YouTube success and its tie up with Amazon , Apple and OTE App ShemarooME

-

COVID situation has certainly impacted traditional media advertisement spending and consumer spending. The sooner the spending power comes back, the sooner will be the comeback. The timing of the comeback need to be monitored as situation due to COVID is still tricky and uncertain.

Overall its a company with good historical growth, the strong rights and good focus on Digital media. With its past growth and recent crash in price from 400 to just 68 currently , it has now gone to become one of the lowest P/E in the Industry and trading at all-time low P/E. Company new initiates are exciting and position company well to monetize its rich contents.

I have invested in this at the current market price of 67 for long term purposes given the above.

Disclosure:

-

I have an investment in this stock so my views might be biased. I request you to take your own judgment call before you make any investment in this name.

-

I am not a SEBI registered analyst so don’t have any recommendation service/Paid service. It’s an educational website that is just meant to share the analysis I do before I invest.

8 Likes