CMP: 330

Market Cap: 900 Cr

Summary:

One of the top 3 content aggregators in India, growing it’s youtube views rapidly (60-80% y/y) now at 100M page-views per month. Amazing business, and growth but management ethics are under the scanner and need a “leap-of-faith”. I’m introducing this idea hoping that the valuepickr community will help dig deeper into the management ethics part.

Bull-Case:

The optical growth rate right now is only 15% in sales and 28% in profits, but this is because the old media business (non-you-tube) grew only 8% and is the majority of the revenues. If the current trend continues, the next few years the sales growth rate might be: 19%, 25% and 32% as the new media takes a bigger share. And the new revenues seem to be relatively cost-free, as we can see most of it dropping to the bottom line. If this continues, the profits will be growing much faster at > 30%-50% y/y next few years.

Netflix for India launch is a tail-wind.

Bear-Case

- The promoter Raman Maroo, of Shemaroo was an independent director with Orbit Corporation, which was classified as a willful defaulter.

- This whole entertainment space is full of corrupt people and Eros Entertainment was recently under the for cooking the books.

- Most of the profits are fully invested in buying up more “Copy-rights” and we just have to take the management’s word for it. They don’t disclose the break-up. Out of 40 Cr in Net Profit made last year, the company spent 80 Cr in purchasing new “copyrights”; (incl IPO proceeds)

December Results and the youtube growth chart:

http://corporates.bseindia.com/xml-data/corpfiling/AttachHis/BE50E8BB_6D72_44A6_A202_43F1F2BFF264_091646.pdf

Investor Presentation: http://www.shemarooent.com/doc/reports/Shemaroo%20Investor%20Presentation%20Nov%202014%20Final.pdf

The company IPO’d at Oct 2014;

• Shemaroo acquires content with either Perpetual rights (complete ownership) or Aggregated rights (limited

ownership)

• The company distributes and monetizes this content across different media platforms.

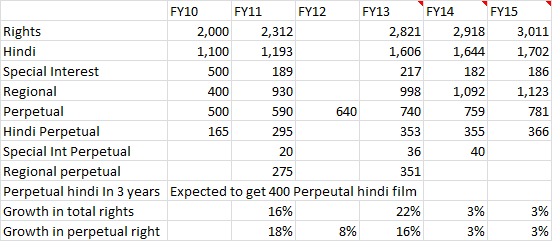

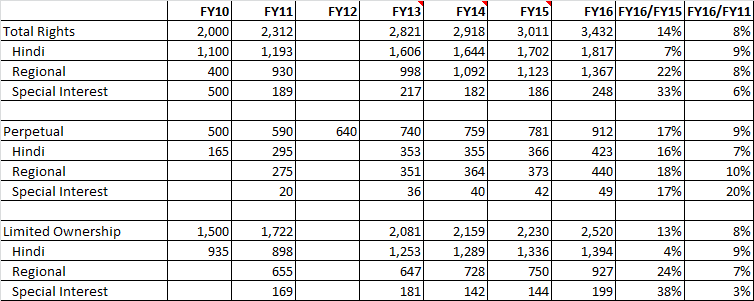

• The current content library stands at 2,918 titles as on 31st July 2014, with 759 Perpetual rights and 2,159

aggregated rights

• Perpetual Titles (Hindi) – Amar Akbar Anthony, Anari, Dil, Disco Dancer, Ishiqiya, Khuda Gawah, Namak Halal

• Aggregated Titles (Hindi) - Mughal-E-Azam, Jab We Met, Don, Anand, Sarfarosh, Shahenshah, The Dirty Picture

Disclosure: Invested in small amounts.