Hello Harsh,

How did you calculate market share. Is it based on weekly impressions.

Thanks

Hello Harsh,

How did you calculate market share. Is it based on weekly impressions.

Thanks

Yes. Although it will not be exactly true because the weekly impressions are only available for the top 5 channels. But the trend can be seen

Company has taken collective personal guarantee from related parties to the tune of Rs. 135 cr against its borrowings from banks. The above loans from related parties are unsecured and payable on demand as per the reports of 29th july20. In other words, can banks sell their shares though it is not pledged but are personal asset of the promoters. the co has also taken a new long term loan of Rs20 cr.

The recent CARE rating report reveals that there is delay in release of enhanced cash credit facilities and term loans. Does this mean banks do not want to give loan to the company? The current inventory levels of 700 cr.+ is putting serious problems on company’s liquidity, with cash position of below 1 cr. and a term deposit of 5 cr. Working capital is 94% utilized and overdraft facility is fully utilized. They have upcoming debt obligation of 11 cr. in FY21, out of which 4.6 cr. has been so far in FY21. This rating report is pretty comprehensive.

Just wanted to check if there are any other resources to check progress of Hindi and Marathi channel other than barc rating. Thanks

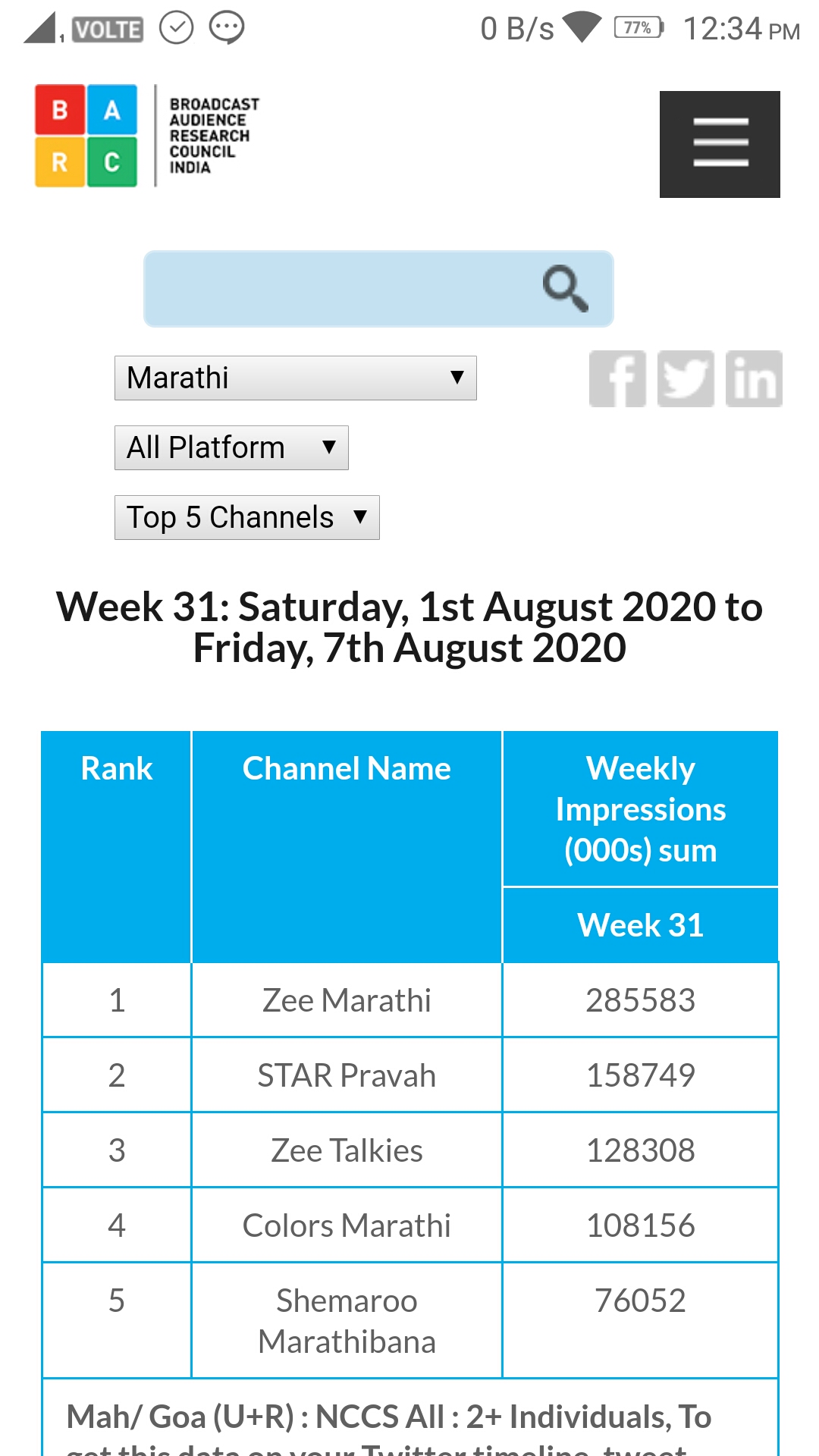

Shemaroo Marathibana has reclaimed top 5 spot in latest barc ratings.

Looking for help on how to measure progress of the Hindi channel. Don’t see many ads on the channel yet.

hi guys new and this is my first post here if i make any mistake please let me know,so have been leaching from this forum for quite some time and it best not to be selfish and help others if i can so first of all thanks to @myprasanna have tracked your past records and thanks to you discovered this stock

i am going to put simple pros and cons why i invested in this stock plz do your own due diligence

pros

1)extremely undervalued picked it up at 50 something which gives this a pe of 1.xx from 2019 income plus 18%cagr for 10 years is just icing on the cake

2)going forward all thing will be digital cheap data and east availability we have seen a spike in social media influencer to travel bloggers going forward i see a slight chance in in more 3rd party content low budget movies like paranormal activity not AAA movies but movies which shemaroo can capitailize on.

3)No one can predict the future but i think the worse phase is over going forward ad spending will increase as economy does well .

4)very conservative management doesn’t use leverage to expand whether it be main business or secondary business

cons

1)going through the thread i found that one of the promoters is not honest so for me that is one of the biggest red flag also various discussion has pointed out that management might be cooking the books.

2)discussion that promoter has taken a collective guarantee of 135 cr is also red flag that can hammer the stock price

3)management not focused in core business (opening restaurant)

4)piracy is still a big thing in our country going forward don’t know it will effect the core business.

5)As the movie 3 idiots tells us no one knows who the second astronaut who went to moon was similar story is with this business . when it comes to subscription based business everyone want the best so i see no reason for me subscribing to shemaroo rather than Netflix or even similarly priced amazon prime forget second i don’t think shemaroo OTT platforms comes in even top 10.

DISC :invested

Main issue with Shemaroo is that it is a very small company and does not have deep pockets like Netflix and Amazon. It is trying to go digital but does not have enough money to buy rights to new movies or new content. Also its new regional tv channels are doing well but are still not subscription based and hence not earning any revenue.

Its seems to long tough road ahead of shemaroo

Hello,

If anyone attended the agm, could you please share notes.

Thanks

Bottom seems to have fallen out of their sales, revenue from operations goes down from 150 cr. to 58 cr. H1 sales are 145cr. with receivables of 91.6cr., making receivable days as 230 (FY20 receivable days were 75).

Operationally, company has done well reducing losses to 9.2cr. from 12.8 cr. in Q1FY21. Inventory increases to 743cr. from 713.6 cr. in Q4FY20. I am not sure of the quality of inventory, given that they have systematically lost market share in their marathi broadcasting venture (weekly impressions have reduced to 31’706 in October from more than 1 lakh when they launched in March). They haven’t been in the top 5 for quite a while now. Overall, business is not picking up.

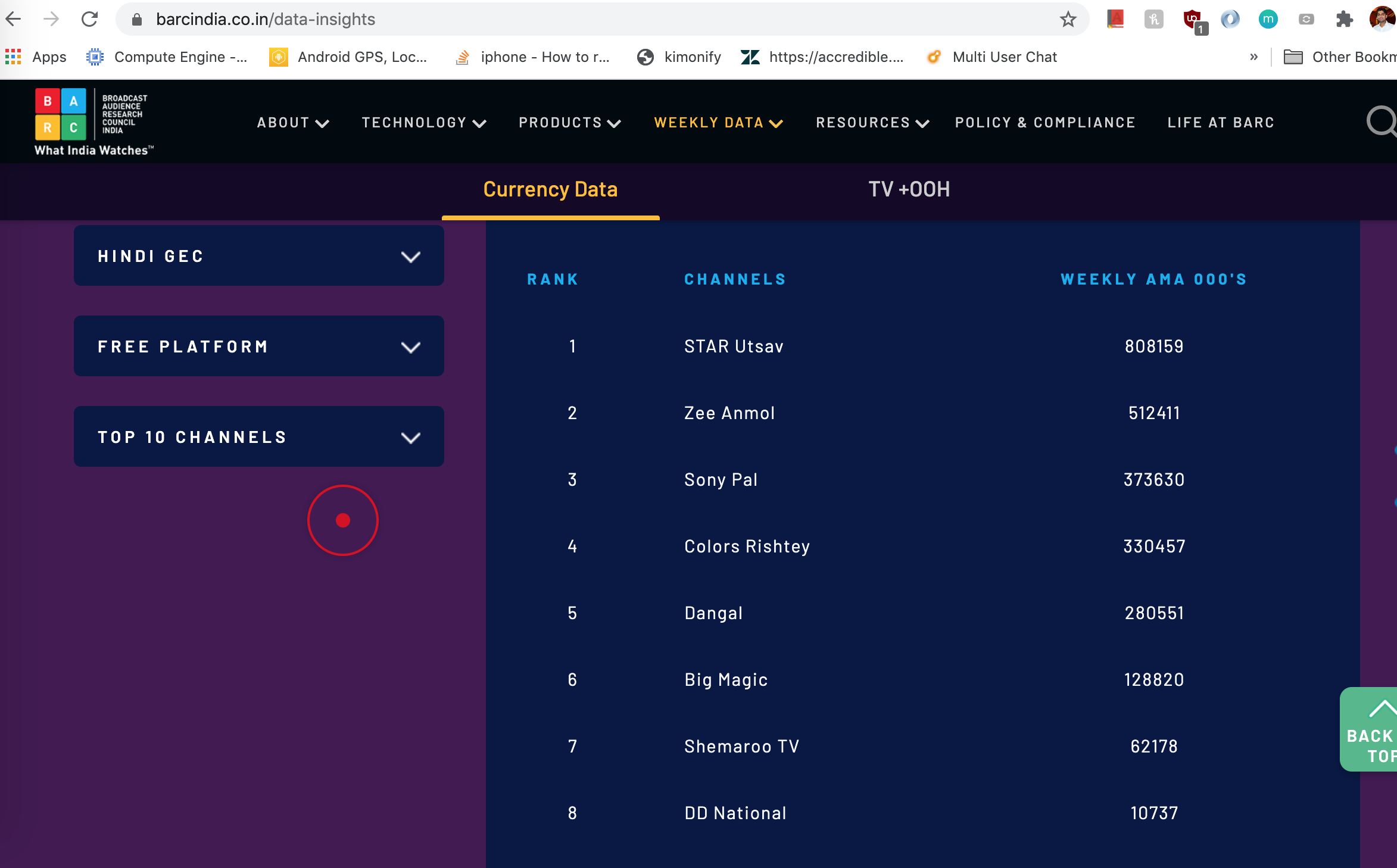

Shemaroo TV is now under 10 channel all over India in free platform GEC.

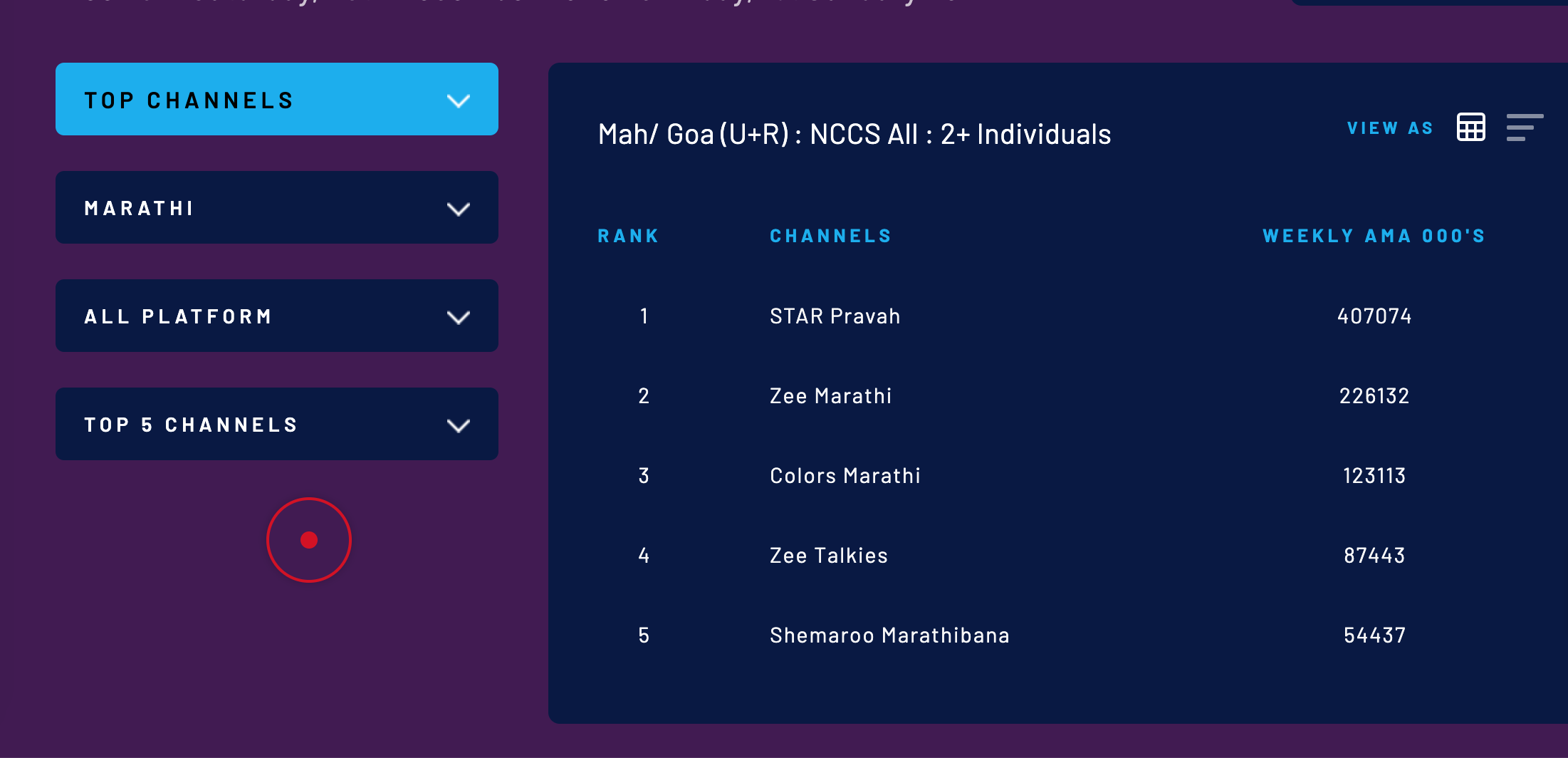

Shemaroo Marathi channel no. 1 in Marathi under free platform and 5th in all platform.

Q3 results are out. Suppose decent recovery in topline and has small loss comparatively to last two quarters. We will know more about operational performance in conference call / transcripts.

Hello,

If anyone attended the concall, could you please give the summary or your thoughts about the concall.

Thanks

I attended the call and mostly individual investors were part of it. Brief notes I made.

Apart from conf call, I have some data from BARC and Ad revenues (from a friend who works in industry) - it corroborates with what management indicated. Viewership is steady and can see decent top line AD revenues. Many leasing FMCG Cos are contributing to this. I feel, once Auto Industry launches new products there will be promotional spend from this sector as well.

Disc: Invested.

There have been a few doubts that management tried to clarify on the call.

Value of inventory: Management believes that because their youtube platform which is doing so well in terms of viewership is the reason why the value of inventory is correctly stated on the balance sheet. The contra point is viewership is not 1:1 related with revenue, also youtube barely makes 30% of digital and 10% of overall revenues. So if inventory is only getting eyeballs and not making money, then how can I one assign value to it?

Digital revenues: have gone down because a large part of this was coming from deals with mobile companies with feature phone customers. Now with people migrating from feature phone, shemaroo faces more competition as a lot of other competitors have their own application for smartphone customers and shemaroo is not the only one in this game. The large bet in the case of shemaroo was digital revenues will keep growing at high double digits, however with shift to smartphone, this puts the whole thesis in doubt as smartphone market is much more competitive.

Losses: The large investments into new ventures is the reason why company is reporting losses. For 9MFY21, investment into new initiatives have been ~45 cr. The core margins if considered without investments are still at 20-25%.

TV venture: Marathi bana has not broken even yet, as it only started monetization is Q2FY21. Steady state advertising spends on Marathi tv channels is 800-1000 cr/year. They are currently #6 player and a large part of the advertising pie goes to the first 6-8 players.

Overall, the transition of a B2B company to a B2C company has taken a toll on the financials. Management believes that ad spends are coming back. Lets see what happens!

Disclosure: No investments

Hi can someone clarify how much loan has been given by promoters to company , is it 30 crores or 3 crores?

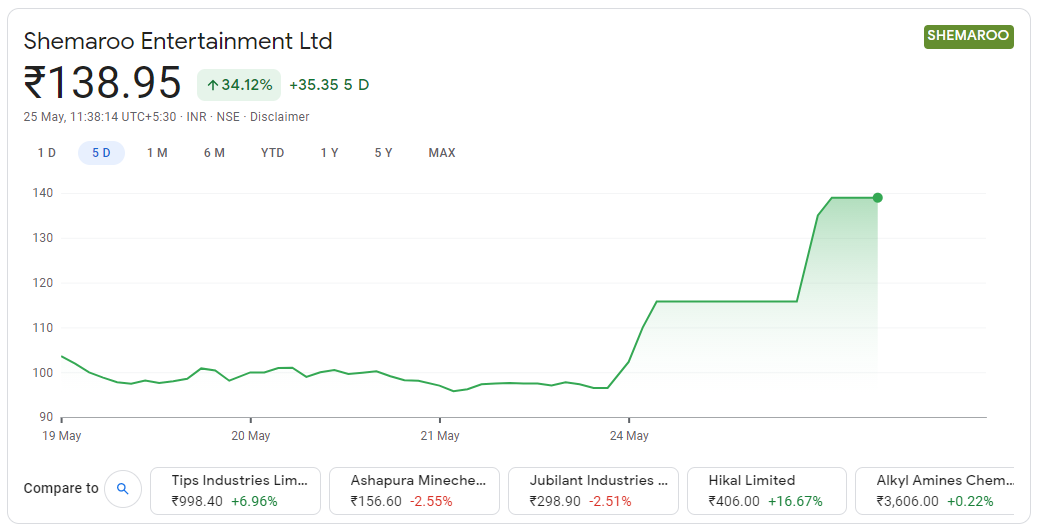

2 consecutive upper circuits. There is no news on why. On the BSE, 80155 shares were traded on the counter so far as against the average daily volumes of 24566 shares in the past one month.

Does anyone here have any thoughts on this?

Disc: Small holding

This is just my speculation,Amazon is buying MGM studios and there is lot of buzz in content space about this acquisitions.

Also if you look at the price of Tips and Saregama in last year they have multiplied by more than 5 times. Although it’s not an apple to apple comparison these are just my thesis.

If we speak about takeover basically one has to look at the book value.

When we compare the book value of shemaro vis a vis Saregama we find that at the present cmp shemaro is very cheap / available at steep discount.

May be this is the reason it is buzzing.

Basis historical pricing movement, it might be due to some speculative trade.

This is a good time to exit in this script.

Discl: Invested for last 4 years but recently exited.