Food industry frankly has no entry barriers, but one can create a sticky consumer-base by appealing to particular taste-buds and/or offering some unique experiences.

Mukka By Shemaroo’s doesn’t only give filmy names to dishes, which anybody can copy TBH, but going by some comments it seems that they also provide some filmy add-ons.

“Kudos to the team for such fancy & colourful packaging with all bollywood quotes & quizzes. You will also get goodies with your food order. I got a bollywood magnet sticker.”

“The box has a small crossword to solve related to all bollywood trivia which makes the lunch even more interesting.

There is a small complimentary fridge-magnet of ‘baburao’ inside the box. I found it really quirky.”

Agree that Management doesn’t have any experience in Food Delivery industry but they have the acumen to supplement anything with unique filmy experiences (names & add-ons). Honestly, restaurant business is rather easy to form even without any previous experience. They have chosen some popular dishes in their menu and the only thing they need to ensure is the reproducibility of tastes. Delivery is anyway handled by Zomato & the like.

At the outset, it indeed seems like an un-related venture which has no synergies with the existing business, but this could be a way for them to build consumer connect. Shemaroo is more of a B2B brand and they have only recently decided to venture into B2C space through the planned launch of Audio Players, Gifting etc. We may as well see them promoting those items through some quirky advertisements in the add-ons provided with the foods.

I may sound awkward, but believe me, entrepreneurs and intrapreneurs think very differently than us. I understand that the price action may have made the market participants more concerned, but you also have to understand that the people who are sitting at the management have sufficient skin in the game (~65% stake), have built the business from scratch and are keeping that running successfully for nearly 60 years, and so have much more at stake.

On a different note, although Shemaroo is on my watch-list, I usually ignore businesses which suffer from ‘red queen effect’ of sorts.

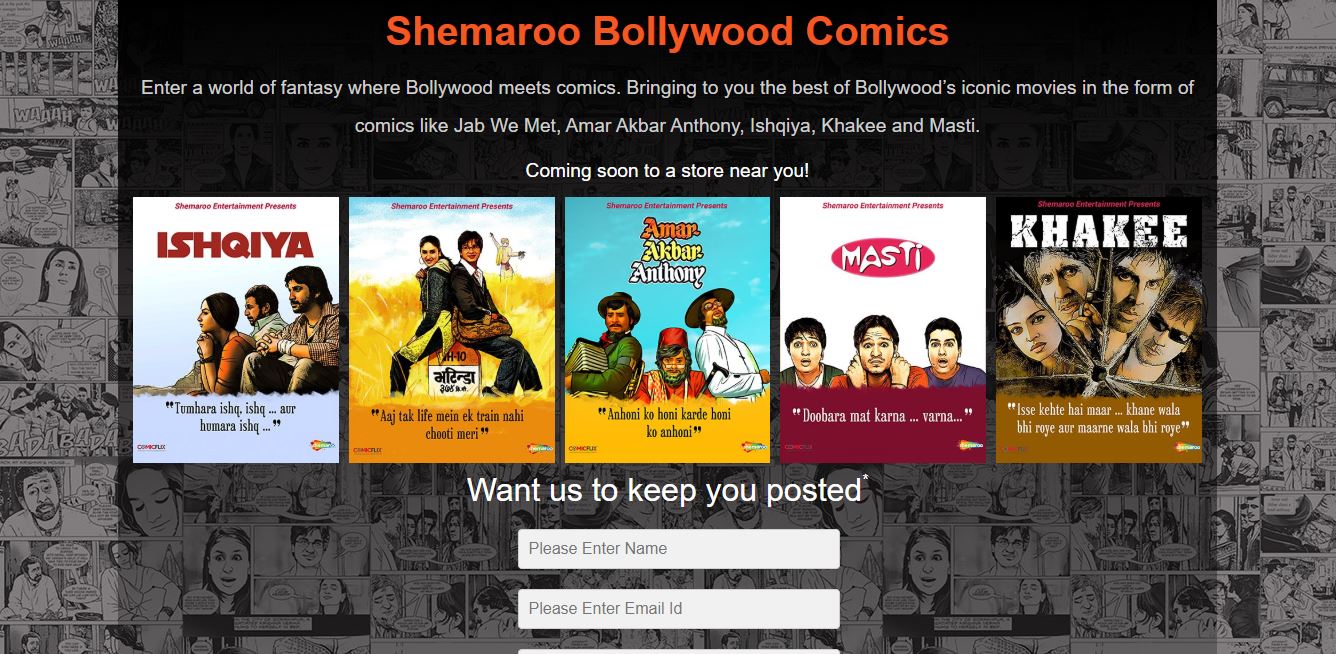

Looks like apart from the Restaurant business , the other initiative management is venturing into is comic books. With Hollywood building an entire money spinning franchise out of comic books, Shemaroo is looking to take a page out of the Marvel book with its latest venture. Let us see how the comics get the response. The content that Shemaroo has , has huge scope to be delivered through different means and Shemaroo has done well over the past few years evolving with the changes in the industry.

Shemaroo Filmi Gaane Youtube channel has crossed 30Mn Subscribers. They are running campaigns on Social Media to make the brand and OTT Platform Visible. Have seen some Shemaroo titles on Netflix and Amazon Prime too. This quarter will be important to track as it will reflect how the Devices Business has received response in festive season.

The apathy towards small Cap stocks and low float have taken the share prices of Shemaroo to new lows. Prices often changes perceptions and diminishes confidence no matter what. Management has to come up with more clarity for the future plan of the company. Have read that they have a vision of 5X in 5 years for the top line but looking at the current scenario , it looks a distant dream. Hope there are no hidden cockroaches here.

True ,why one will subscribe to shemaroo instead of amazon prime and Netflix or you tube prime .Soon reliance jio and mi tv will come with some subscription.

Shemaroo is Classic case of “misunderstood investing”. They are “traders” of content, so for main business (syndication), if the own:

Perpetual rights: More and growing VoD platforms (or linear channels for that matter) are good for them. Almost all of incremental revenue flows to the bottomline.

Limited rights: There content acquisition costs are higher if there are more VoD platforms as content producers may ask for a bigger piece of pie - but as they buy in second cycle it’s unlikely for Shemaroo to make money losing deals.

Everything else (Food delivery, merchandise, comics, ShemarooMe etc) is current a footnote to the topline and IMHO most importantly thing to watch out for is if they throw relatively high amounts of good money in these new initiatives even after lack of enough early promise. In other words “fail fast, fail often” is the model they should follow and from management actions/words it seems like the case.

Don’t track Shemaroo anymore (failed to record my disclosure on exit, due to inactive state and regret that).

I don’t know the reasons for recent set of results. Those invested may like to share their perspectives. To me it was quite clear that our bet on Shemaroo best placed for capitalising on super-normal growth in digital consumption in India came unstuck for 2 main reasons:

Sudden crash in You-Tube Ad rates, when major brands threatened to pull out because of premium brand ads tagged on to sub-par content, and/or unhealthy content - That rate crash (and questionable sanctity) was not factored in by me (major goof-up)

In a drastically slowing economy advertising budgets are likely to be tightened, and digital media share likely to shrink even more.

Consequently, it was clear that Industry stability (Media Advertising) was under threat for a prolonged period, and given the earlier track of under-delivering despite humongous digital traffic growth (and robust media ad-spends) showed that our business-model vulnerabilities diligence in Shemaroo was certainly much below par.

Those were my reasons for exit.

I believe the business has great inherent strengths and once the media ad-spends revert to normal, we could see better performances in base business. How long that would take I don’t have a handle but VP Media experts might like to share their perspectives on above. Have not tracked the new initiatives, and don’t have a informed opinion there.

Had listened to the concall for few Mins including opening remarks by Mr. Gada.

The reason for Poor Sales were again attributed to slowing economy and less spends on Ads. The growth in Digital Business is also not encouraging.

Their is an additional spend of 7 Cr in this quarter and 15 Cr in last 9 Months on New Initiatives which affected the Bottomline. The spend of 7 Cr will be again there in next quarter.

Management believes that these strategic investments will bear the fruits from next FY onwards.

Though management said that the Restaurant and Device business has gain good response but i do not think it is anyhow contributing meaningfully to Topline as of now. Last Quarter was a festive season and despite new verticals , Sales are not reflecting these.

Launched a Free To Air DTH Channel Marathi Bana to capture regional Market.

Disc: Invested , not a significant portion of Portfolio now considering the fall. Will not average. Will hold it until any corporate governance issue pops out.

I took some notes, I am mentioning what has not been mentioned by @bharat19

Management says broadcasting business is highly cyclical, however they did not expect ~50% de-growth.

Pre-loaded speaker revenue is mentioned in the traditional business segment and not under digital media (which means that broadcasting revenue was even lower).

The new intiatives will break-even in end of FY21

Gave break-up of digital business (20-25% from telcos, 35-40% from youtube, 35-40% from sindication and ShemarooMe)

Management acknowledged that they are not expert in restaurant business and its just an experiment with total investment of less than 1cr. Plus they will partner with restaurants instead of starting something themselves, however this is at a very nacent stage.

Debt is up by 22 cr. and inventory by 35 cr. (compared to September balancesheet). Part of inventory has gone into acquiring content for free-to-air Marathi channel (ad market size for Marathi is ~800-1000 cr.)

Follows 50-50 ratio of internal accrual and debt for funding new initiatives. Cashflow for main business is ring fenced i.e. they probably won’t have liquidity issues in servicing debt

Undertook cost rationalisation initiatives. Adding people for new initiatives with a net 5% heacount reduction.

As a quick translation, Shemaroo is using “Marathi Bana” as channel name but Chaurang has the trademark for it and its going to court to get Shemaroo to change name of its Marathi channel.

Shemaroo is falling very badly no respect kahi zero na ho jaye, any issues in accounts or mgmt @dineshssairam can you check accounts part and throw some light?

I don’t think there’s anything unethical with the management. But one of my major concerns with Shemaroo was that about 60-70% of the company’s “Assets” were heavily reliant on the management’s ability to estimate the value of their content and the speed with which they can monetize it.

Clearly, when YouTube reduced content rates drastically, it indirectly reduced the value of those “Assets”, meaning the management had already overpaid for the content. Secondly, they were not able to monetize the content as quick as promised (Maybe the slowdown, as cited the management, is the real culprit). This creates a cashflow issue, and probably why the management is desperate to get into unrelated lines of business.

While they may still manage to monetize the major part of the vast amount of content they acquired in the last 2-3 years, I still have no clue how I can estimate the management’s ability not to overpay for future content. Even when I valued Shemaroo, I put in a disclaimer that the valuation heavily relied on the assumption that the management knew what they were paying for.

Be warned that Shemaroo hasn’t nearly begun implementing its Business Model. We have no way of knowing whether it will become successful or not. Considering how its Content and Copyrights form a major part (70%+) of its Assets, Shemaroo’s success will be attributed, on a large part, to how effectively its management can sell off acquisitions quickly or start monetizing them (By streaming them on its own platform, for instance).

So for these reasons, I refrained from investing in Shemaroo. If someone has good competence in the content arena and knows how to value them, they may yet find value in the company. I personally couldn’t.

Hello Dinesh,

I checked from the shareholding pattern that promoter stake is constant from last few quarters. Are there ways in which promoter might decrease stake and not immediately get reflected in the shareholding pattern (something like Yes Bank).