Thanks for your inputs, waiting for @dd1474 comments, but @bharat19 you have put the things very nicely and in perfect way, thanks once again

They are continuously buying content (inventory), how long will they buy… Any question related to this during concall??

1 Like

I got the numbers from screener, I hardly see any net cash coming out.

As I mentioned, I am not following Shemaroo closely since an year. Hence, my buy/sell decision is mostly biased towards technicals.

Their business model requires continuous accumulation of new inventories. Point is how effectively they monetize these inventories and free up their cash. Audio Speaker Devices business will also require high inventories. It need to be seen how they receive response in this festive season.

2018 and 2019 saw positive cash flows. Let us see how they go ahead.

The other initiative I think Shemaroo is going into is Setting up Skill Centers if going by this news article.

Disc: Invested , the correction in stock prices is really frightening !

1 Like

stock tanked, as expected but the magnitude of the fall (on an otherwise, extremely positive day in market) of nearly Rs 50 intraday means that, this has cracked and Mr. market doesn’t like the result

Shemaroo has a target of 5x from here w.r.t business, and to achieve this target they are trying many new things such as business of food,audio device,skill development etc. Investors invested in shemaroo due to the logic that this business will throw out cash from the existing library and that would be enough to fund future library purchases. Now it isa known thing that whatever new things they are trying needs money and that is hurting investors sentiment, it also raises question that cant the “main” Business itself has potential to make shemaroo 5x , or it is the time factor i.e mgmt wants to achieve this target very fast which as per them can be achieved with new initiatives.

Also one thing is to be noted that whatever new initiative are being taken has one positive thing, these initiatives is helping shemaroo to create there brand image,and also new relationship is being created with many more . They could have spent money on advertising in the old way eg advt. On tv,newspaper etc but mgmt might have thought that if it also create something that gives utility in addition to advertisement then it will be more fruitful.

On one point i want the senior broaders to give there advice that , in future also mgmt could get new opportunities in businesses will they at that time also raise equity or use companies cash or they will adopt conservative stance after 5x?

1 Like

Hello Dhiraj,

Could you please provide your views on the concall, not able to get transcript or audio.

Also wanted to know if the management had given any indication in the past of opening a skill centre. I had gone through past concalls but to me this was pretty surprising.

Another thing I just came to know is that Shemaroo has the same auditors as Talwalkars had and Raman Maroo sits on the board of Talwalkars. I am sure this will not be news to most people here, but just wanted to know your thoughts on both these facts as well.

Thanks

1 Like

Hi Sarthak , though your query is addressed to Dhiraj Sir but thought to provide my views. Also request @lingalarahul7 @desaidhwanil @dd1474 to add more.

You can listen the concall on StockAdda.

Shemaroo already operates Shemaroo Institute of Film & Technology (SIFT) as well as Shemaroo Studio. This does not look like a new venture for them. More details need to be ascertained regarding this skill center in Oddissa and will it help the company in revenue terms or kind of a CSR.

https://www.shemarooinstitute.com/about.html

The Auditor is M.K Dandekar. For Talwalkers , it was appointed in 2018 and has this to say for Talwalkers on the accounts for year-ending March 2018: The Company’s operating effectiveness and internal control system for Revenue from Operations with regard to Fees and Subscription is not commensurate with the size of the Company and the same needs to be strengthened by the Management. A material weakness is a deficiency, or a combination of deficiencies, in internal financial control over financial reporting, such that there is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not be prevented or detected on a timely basis . I think the auditors had clearly said about the irregularities in Talwalkers . MK Dandekar resigned in August 2019 citing the company’s failure to provide satisfactory responses to their queries. Independent directors :MG Bhide (former chairman of Bank of India), Dinesh Afzalpurkar (former chief secretary of Maharashtra) and Raman Maroo resigned in July 2019. Also to note Raman Maroo was also present on the board of Orbit Corporation in past which was a wilful defaulter. That is definitely a issue but I think Maroo was only an independent director andhas not any involvement in active functioning of these business. Also Shemaroo being a very old company having many decades of experience , promoters deserves a benefit of doubt in my view. Definitely it may be biased due to my holding in the company.

In the concall , one of the person has requested the company to provide a breakup of revenues from all the streams like SIFT , Devices Business , YouTube, OTT , Yedaz Merchandize , MVAS etc in their quarterly presentation. Let us see if they take it in spirit and action.

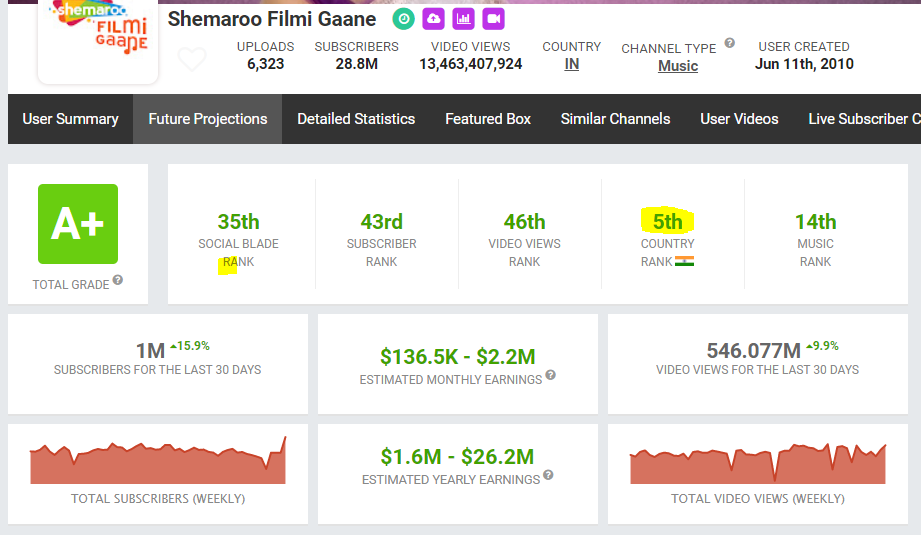

Looking at their YouTube performance in last 1.5 Year : :

Shemaroo Filmi Gaane

April 2018 :

Subscribers - 8.7M , Video Views : 4200M

October 2019 :

Subscribers: 28.8M , Views : 13463M

Subscribers have grown from 8.7M to 28.8M in last 1.5 Years and Views have increased from 4200M to 13463M. Also in last 1 month , Subscribers have grown by 1M and views by 546M. The estimated revenue shown may be different as shared by Youtube and Shemaroo both but the trend is very healthy.

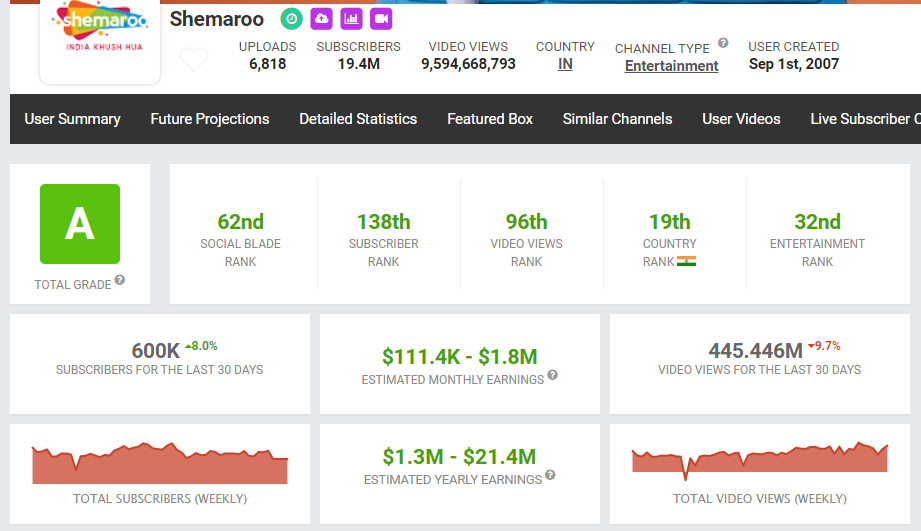

Shemaroo :

April 2018 :

Subscribers : 6.8M , Video Views : 3300M

(One can check April’18 Post on this thread)

October 2019 :

Subscribers : 19.4M , Views : 9594M

In last one month , Subscribes grown by 0.6 M while views grown by 445M. The trend is healthy here too.

OTT Platform ShemarooMe has over 0.5M Install since launch in February 19 which looks a decent number.

Mukka business recently started somewhere around July/August has good reviews on Swiggy and Zomato. It looks a delivery based restaurant and thus would have lower cost than a traditional restaurant. More details need to be asked from Management about this.

8 Likes

Wow, excellent work and insights, need your opinion that how traditional business can grow in future how revenues will increase,please do post your opinion, if you can post a detailed note.

Thanks

Nice work Bharat, especially on the auditors part!

Let me start with my comments on each business. Please feel free to differ from my thoughts and engage in the discussion.

Traditional business:

The struggle here is due to ad revenue. Zee’s ad revenue just grew by just 1.2% this quarter. So not surprised if content owners of movies begin to see a decline in their revenues. Once the slowdown ends, the growth they see should come back. However, there is no slowdown in neither Zee nor Shemaroo during the 2013 slowdown. I don’t have an answer to this. Still need to research further.

But everyone accepts that TV business growth will be muted going forward and won’t take the company to 2000 crores by 2023.

Digital business:

MVAS is declining continuously as everyone must know by now.

YouTube revenues don’t see much growth even though subscribers / viewership grows. I personally think this will be the case going forward. The whole point is that the new users who are entering the ecosystem are people with low affordability. So the ad companies won’t be able to sell their products. And hence no new money will enter the ecosystem and this implies that CPM rates will fall. So I don’t expect extraordinary growth here and this won’t lead the company to 2000 crores revenues.

OTT syndication revenues should keep rising with time and I believe this shouldn’t face too many headwinds in the near future. But again this won’t be the company’s knight which will take it to the next level.

Overall, the growth in digital business is moderating and should help take the company to 800-1000 crores in next 4-5 years but not more than that.

ShemarooMe:

Though this is a good initiative, I don’t see this going bigger than 50 crores few years down the line. Subscription revenue should be very very low for the company. And ad revenues will come with low realizations. See below article which says that Hotstar’s ad revenues were at 168 crores in FY18. FYI, Hotstar was started in FY14 and gained quite popularity by FY18.

Yedaz & Mukka:

It is not very easy for the company to build a big clothing / accessories brand given their in-experience in this category. I wouldn’t put too many expectations on this line. I doubt if this will even hit 50 crores brand by 2023. If not convinced, look at sales numbers of small cap retail brands who have been running the business since years.

Though Mukka restaurant is an interesting and innovative initiative, the important question we need to ask is how big can this become? To give you a perspective, Jubilant foodworks has about 1200 restaurants and they did revenue of about 3600 crores in FY20 implying 3 crores / restaurant on average. So Mukka will definitely not be a game changer.

The good thing about Yedaz and Mukka is they will improve the brand perception by general public and that can indirectly help the devices business. Revenue wise, they will just be side-pocket income.

Devices business:

Shemaroo has launched various kinds of portable speaker devices which one can find in Amazon. The devices look good with a premium finish. If anyone has bought any of them, please comment.

This business is still at nascent stage and would be a bit pre-mature on my part to say that this ‘will’ be the game changer. Lets rather focus on whether this has the ‘potential’ to help the company achieve 2000 crores. Remember there is a gap of ‘execution’ between ‘will’ and ‘potential’. And ‘execution’ is what all matters.

Saregama which was in a similar line of business has achieved revenues of about 300 in FY19 (perspective: Shemaroo revenues in FY19 is 550 crores+) in this segment. And it reached this scale in two years. Saregama CEO Vikram Mehra has been claiming that this is just a tip of the iceberg and they should increase their sales with better distribution and has been the case. Q1FY20 saw growth of 33% YoY in caravan sales.

I personally think IF executed well, this line of business can go very well and take the company to a new level. But how can we trust the execution of management here given no previous experience in this space? I still think achieving 1000 crores revenues out of this line is difficult as that means selling about 30 lakhs to 40 lakhs devices per year.

One bad thing about this business it won’t create a continuous stream of revenues. A buyer of one such device will mostly not buy another such device. And once the craze fades away for these devices, the management should find another such line of business. I should probably study some toys / gifts company to understand this part further.

Some additional things to ponder about:

-

Why would the management shift their focus to a new line of business at the cost of raising funds? One thing to conclude is they are desperate. They can be desperate in two ways. Either they find that the current business model may not be sustainable and desperately plan to raise cash. Or that the new devices opportunity they found is too good to be desperate

-

Shemaroo’s market capitalisation is about 500 crores now. What is the amount of money they used to acquire rights in FY18 and FY19? FY18 => 272 crores and FY19 => 352 crores. (You can find these numbers in Operational Cost notes in Annual Reports.) Just the value of rights they bought in last two years (624 crores) put together is greater than their market cap (511 crores). Either the company is dead cheap at current prices or the 624 crores amount used to buy rights is bogus. The management can just sell those rights if company is on the verge of bankruptcy. That 624 crores amount sounds reasonable to me as purchase cost per movie / label in that year is about a reasonable 1.5 to 2 crores as per number of movies reported in Annual Report (See below table). Now only thing to verify is => are the number of movies reported in the library correct / fake? Not sure how to verify this part, it is work-in-progress as of now. Does any one know the number of movie titles we have uploaded in YouTube?

| Content library (#) | ||||

|---|---|---|---|---|

| 2019 | 2018 | 2017 | ||

| Hindi perpetual | 498 | 471 | 443 | |

| Hindi limited | 1466 | 1454 | 1423 | |

| Regional perpetual | 637 | 511 | 456 | |

| Regional limited | 1028 | 1017 | 984 | |

| Special interest perpetual | 60 | 55 | 49 | |

| Special interest limited | 252 | 243 | 230 | |

| Total | 3941 | 3751 | 3585 | |

| Perpetual % | 0.3032225324 | 0.2764596108 | 0.2644351464 | |

| Limited % | 0.6967774676 | 0.7235403892 | 0.7355648536 | |

| Revenue / Library | 14.40830754 | 13.02671021 | 11.86978243 | |

| Revenue / Library Growth | 0.1060588056 | 0.09746832269 | 0.08616057736 | |

| Library Growth | 0.05065315916 | 0.04630404463 | 0.04458041958 | |

| Purchase Cost (lakhs) / Library Increase | 185.5702632 | 163.9207229 | 201.3262745 |

Overall, I’m more disappointed about my research work than the mgmt / company as I didn’t properly factor in the MVAS decline part; higher expectations in ShemarooMe potential; quick accumulation without industry wide research; believing that the price of old movie rights increases with cycles and many many such… I’m actually not super disappointed by the management. The management is quite pro-active and seems fully committed to achieve their 2000 crores revenue dream. The question is more on their ‘ability’ and ‘execution’ than their ‘intent’ according to me. We have to see how well they will fare in the devices business.

Discl: Holding from very high levels but it is small allocation now (given the fall in stock and recently pumping in fresh money in other companies). Didn’t sell any share as of now. Still pondering and don’t want to take any decision in panic mode.

17 Likes

Excellent work from both of you. While most of points are covered by your messages, I would not repeat and would like to put forward my thought process.

What were my reasons to buy to stock?

I bought the stock due to expectation of high growth and better profitability and cashflow, resulting from improving operating leverage of better utilisation of content business. My investment thesis generally provide very limited tolerance to business which need cash (either in debt/equity/quasi equity even for growth). Shemaroo raised funds in past to acquire Digital rights which were expected to gain is value from explosion of data usage. With Reliance JIO roll same played out very well with growth in YouTube viewership is anything to go by. The management also paid out Debt raised for content from cashflow.

What has changed?

Now, the management is intending to move into new horizon of growh which also involve developing new distribution business as indicated over call. Over last 6 quarters (since first reference of growing business mutifold), the company is in process to develop new capacity built-up in varous segments. Further business environment also turning not so encouraging in last two quarters.

Where I went wrong?

In my orignial investment thesis, everything worked well, but what missed was decline in realisation with rise in volume with constained cashflow and profit growth.

What are material information to decide way forward?

While managment has managed business destruptions/changes very well in past 5 decades, the key point at this point is whether I would like to stay invested in business which is moving into new horizons with limited information about growth prospect and no information about evaluating cashflows? I am in dilemma and decide on either way (exit or stay invested). Share price is least of my concern if business strength is intact. With this announcement, I would have revisiting my investment reationalein Shemaroo evenif price was say 1,000.

Discl: Still among my Top 10 holding (despite fall on Friday), Not SEBI Registered investment advisor, Investor shall do own due diligence before making any investment/divestment decision. I may exit from investment in case I find other attractive opportunities in the market.

13 Likes

Hiren Gada was recently on BloombergQuint. Main points from his interview:

- ShemarooMe is mostly focused on B2B business rather than B2C, which is good in my opinion as B2C is already a very crowded market.

- Business to telecom has degrown substantially because of their prior focus on feature phone consumers. Their transition to ShemarooMe is to target more smart phone consumers and this should (hopefully!) bring growth back.

- Traditional media has degrown in-line with the advertising industry (in-line with Zee management commentary in their last concall).

- Focusing on expanding the marketing reach for physical devices segment (bluetooth speakers for devotional music)

1 Like

Shemaroo Management has recently indicated over conference call that they are exploring option to finance new growth initiatives. While the prospect appears to good, same is now appear to be difference from my thought of growth of business. They are attempting to explore option of Shemaroome to Device to capitalise the oppotunities. Further, recent increase in Mobile space about increasing subscription revenue from all three players may also have impact (not sure positive/negative) on Shemaroo as nearly 15-20% revenue is coming from Telecom business for the company.

However, in the current market, I find other opportunities which were better matching my risk profile and hence moved from Shemaroo and invested amount equally between Ratnamani Metals and Maharashtra Scooter.

Ratnamani Metal in my opinion a good management, conservative nature doing capex to double the Stainless steel Tube capacity (current capacity around 28,000 tpa which would be increased by 20,000 tpa during FY20). Stainless steel currently accounted for 45-50% sales.

Maharashtra Scooter is holding company having investment in Bajaj group (Bajaj Finance, Bajaj Auto, Bajaj Finserve and Bajaj Holding). It is currently trading at around 37% of value of holding value.

Since I was regular contributor to the thread, I thought to update members about development at my end.

Discl: I continue to hold a very small tracking position in the company. My view may be biased due to my sell decision during last fortnight. I am not SEBI registered advisor. Investor shall consult their investment advisor before making any investment.

20 Likes

The way the stock is falling and the sheer intensity is usually signs of either financial trouble or corporate governance issues.

Any viewpoints?

@8sarveshg, would love to hear your thoughts on Shemaroo. Heard your questions in the concall.

My limited understanding

Chances of fraud are less given the trend of shareholding pattern and taxes paid. The market seems to be disliking the uncertainty due to new business ventures. Slowdown in advertising is for the entire industry.

Thanks

Yes, so the earnings performance has been slow due to:

a) slowdown in ads which is obvious due to the slowdown in the economy and consumer demand

b) multiple new business ventures being incubated (audio player business like Caravan, delivery only veg restaurants, gifting and many others) - while the costs of incubating the same are small maybe a million dollar for each business and will be a one time impact assuming none of it succeeds - the same is being treated as recurring cost by the market while the revenues currently are small enough to absorb such costs. The company needs to do a better job of explaining what is happening on this front to the investors but are probably too stingy about releasing information fearing competition or low numbers or both.

c) multiple changes in the TV distribution due to TRAI drastic changes of rules early this year - how it will play out remains to be seen fully.

d) reluctance on part of management to slow down inventory growth as guided earlier - whether this is due to new acquisitions or because of a slowdown in sales (since gross margin costs are taken out of inventory) needs to be seen.

So because of all the above uncertainties as well as general apathy for small caps, the market has given the stock a huge derating. Big announcements by Jio in the media sector haven’t helped their case either. The company needs to either start delivering well on any one of new businesses where scalability is good and/or come back to previous levels of margins (~30%) and growth (~15%) in their core business to get re-rated (while keeping debt levels at similar numbers)

Another additional factor is the very low level of liquidity in the stock. Promoters, Fidelity and NT Asian Fund together have 85% plus of stock. So the movement has been very swift on the downside as float and volumes are very low. The same can happen on the upside IF the company starts reporting positive numbers or stories on the new business.

8 Likes

I really wonder why they are venturing into already crowded restaurant business

1 Like

Restaurant business may be crowded and competitive, but available market size is huge and is steadily growing thanks to the delivery apps. And Shemaroo is not into generic kind of restaurants. They are giving filmy names to the dishes. So, they are in fact trying to build a niche inside the restaurant business. So, I am not seeing this as a deworsification but an interesting experiment.

Disc. Tracking. Admire the tenacity and competence of the management to tide the company over through several technological disruptions across decades.

1 Like

I feel the food delivery/restaurant business is a completely un-related venture which has no synergies with the existing business or management’s experience. In so far as giving filmy names to the dishes is concerned, I doubt that creates any entry barriers or something that has not happened already or for that matter someone is going to order food just because it has a filmy name.

6 Likes