How to get the breakdown of the data of q2 fy24 revenue? I want to see how the kinetic green and the bs6 JVs are contributing. Could not find it on company website.

Sharda motors posted good numbers for q2 FY 24. Half year EPS at 45. Net cash of 650 crores. This is a company which keeps on churning free cash flows. In concall, management says they are "cautiously optimistic. " New growth engine can be the 3 and 4 litre small commercial vehicles. And the change in emission norms, though part of it could be delayed because of impending elections next year.

Valuation wise, it appears cheap mainly because I think market has concerns related to its terminal value because it is catering to mainly ICE vehicles as of now. Plus management does not give fancy commentary and fancy targets in any concalls. (which actually is a good thing. ) Very conservative management in terms of projections and use of cash on balance sheet.

Technically stock price crossed its previous all time high of 954 few weeks back, posted a swing high of 1100, and then in market meltdown went down and took support at the 30 WEMA at 864 and bounced from there. Post results stock rallied and crossed previous swing high of 1100 and posted another high of 1158, and settled down at a fresh all time high closing of 1100. disc: invested.

sharda q2 fy 24 presentation.pdf (7.5 MB)

12 Likes

Sharda Motor Concall Notes Nov 2023

Volume growth is not shared; gross profit increase is an indicator of volume which has roughly grown by 22-23% QoQ

All new products launched as part of BS VI norms from 1st Apr 2023 are value added sales part; had a good product mix this quarter which contributed to higher margins

Likely delay of new norms due to elections, likely that the date will be post elections

Regarding productivity improvement: Q2 is good indicator of new products(launched from Apr 23) to be streamlined, good part of productivity improvement has already come in this quarter, but there’s always scope for further optimization as products mature

Expect a tailwind(can’t quantify) due to new products; as products have come in, have grown in indicative volumes as well as gross profit leading to higher EBITDA, market grew at 5-7% whereas Sharda’s gross profit grew at 20% this quarter; this delta is due to content per car on a blended basis

On QoQ basis, gross profit indicates volume increase, going through a per vehicle increase in profitability

On entire new process stabilizing over next 2-3 quarters: Nature of the business is very long term oriented, working on a potential index, as a product matures, profitability increases but hard to say how much of it will come and how much has already been captured, markets are dynamic, just to be conservative our focus is to stabilize

H1 had gross profit growth of 15-18% growth,

On plans to monetize Noida land: Land prices have gone up a lot, if they get a very good deal would wait and monetize it

On EV Venture: Products are at Testing queue, it remains to be very dynamic, multiple regulatory changes, there’s cost pressure, will wait for full testing to be done before investing in this venture

Have applied for PLI, have engaged with a consultant. As of now not considering any benefit from PLI in the numbers.

Dividend policy as of now is 10-30% of PAT, but given cash reserves, working on upward revision of the same; work is on to lessen the range of 10 to 30, so there’s more predictability

In terms of next regulatory trigger, there could be delay till FY 26; new market has opened up

Without giving any specific numbers, company remains optimistic for FY 24 & FY 25, also there has been some surprise developments in some business segments such as suspension, have been nominated for few EV programs, international business development cycle is looking good, volumes look solid in terms of how the automobile industry is doing, one more interesting business that has developed is in 3L to 4L segment in CV segment. If co is able to break into that segment, that is a fairly large market, but at the same time have to be cautious due to global headwinds & macro factors

Revenue mix right now in Emission side is 40% PV & 60% in LCV etc

Percentage of catalyst content in revenues is not disclosed; margin goes up as catalyst content goes down

In New products(introduced from Apr 2023) there’s no catalyst, margin profile is similar or slightly improved over the years

On utilizing heavy cash on balance sheet: First preference is to utilize it in M&A activities in powertrain agnostic products, but also want to be conservative & long term oriented in terms of M&A, at the same time looking at benefiting shareholders via dividend

On conducting international roadshows: Augmenting management bandwidth to enable better interactions, last 4-5 years have seen good growth due to great execution

On sustainability of margins & exports: This quarter did see a very good product mix, also was the first quarter with full products coming in which are on value added basis; will maintain 10% plus margins, quarter was a favourable product mix quarter, new in terms of exports, started 1-1.5 years back, exports would not be a large %, mainly supply to the US markets, have now developed a complete team for intl business, macro is a huge tailwind for India, China + 1 theme is playing out much more than the co imagined, initial learning curve is there for exports, do see a very large opportunity

Will stick to core auto business, as of now no plans to do diversification, good opportunity in gensets

Broadly 5 year growth plan is to maintain or increase market share LCV, Enter new space in 3L to 4L,

More focused on 2 wheeler and 3 wheeler side on EV

In tractor segment, there are only 3 cos that are present in India and globally only 4 to 5 cos, competitive intensity is lesser due to tech requirement, in general tech that is reqd is much higher

Very early to comment on PLI scheme as there’s lot of ambiguity

Disc: Invested

11 Likes

The reason for such cheap valuation is 1) there traditional vehicle focused portfolio or 2) uncertainity in capturing EV market or 3) some kind of promoter disputes?

1 Like

Thank you @nirvana_laha and @manpritaurora for this awesome thread. Loved the detailed analysis. This came to my attention after @hitesh2710 and @phreakv6 had posted about it recently. It’s run up a bit, but still seems reasonably valued.

I had a question regarding sub-component exports. I guess it’s still early stages, but what subcomponents are they seeing the demand for - is it only related to exhaust systems and gensets? In their latest earnings call, they said “…establishing an export business, which is for emission systems for smaller tractors, gensets as well as subcomponents, which is part of our backward integration already.” So are these subcomponents related to emission systems and gensets only? What about suspension related opportunities? While they are not that big in India there, they still claim to have a market share of 10% in suspension systems in their Q2 investor presentation. Are export opportunities strong there too?

Will be great to get any additional insights on this. Thank you.

2 Likes

Few observations from FY23 AR:

-

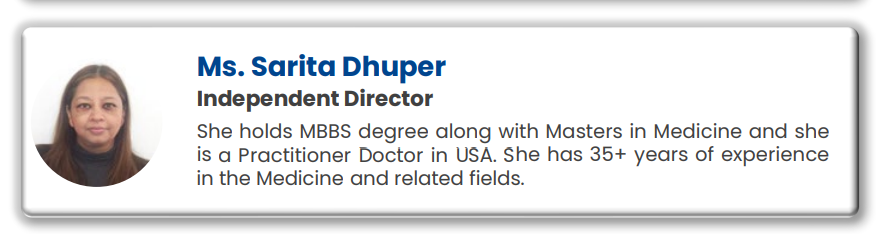

Weak Independent BODs: Most of the independent board members profile is irrelevant to the operating business. On ARs Page 62, I was chuckling while reading competence for most of the names…Practicing US based doctor’s expertise helps in CSR | 87 Yr old director takes care of day today affairs etc.

-

Slow spend on CSR Activities: The Company has created a provision for unspent amount of

214.06 lakh in FY 2022-23 (March 31, 2022:199.94 lakh) and transferred the same in separate bank account on April 21, 2023 and April 27, 2022 respectively as per notification no. G.S.R. 40(E) and January 22, 2021 issued by the ministry of corporate aff airs (MCA). -

MDA loaded with boilerplate statements. No insights about the business. May be because they covered it all at the start of the AR.

-

CEO and Co-Chairperson are not mentioned as Relatives of Key Managerial Personnel. It took some effort to map the family tree.

-

Major Customer Dependency [83% of FY23 Revenue from 3 customers | Details of each name not provided]: Revenue from 3 customers (March 31, 2022, 3 customers) of the Company’s manufacturing & trading business are Rs. 225,337 lakh (March 31, 2022 Rs.176,418 lakh) which is more than 10% of the Company’s total revenue.

-

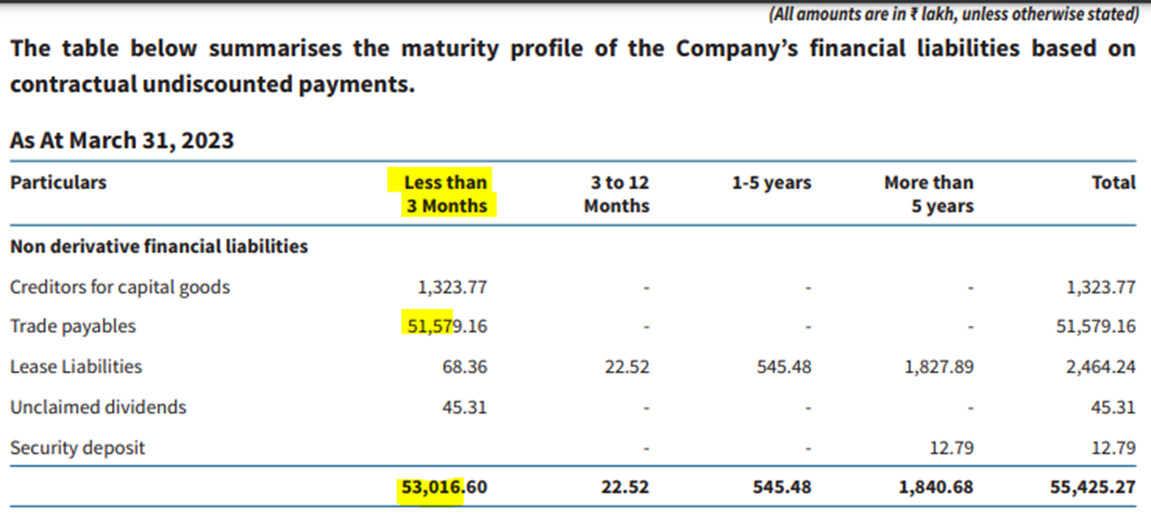

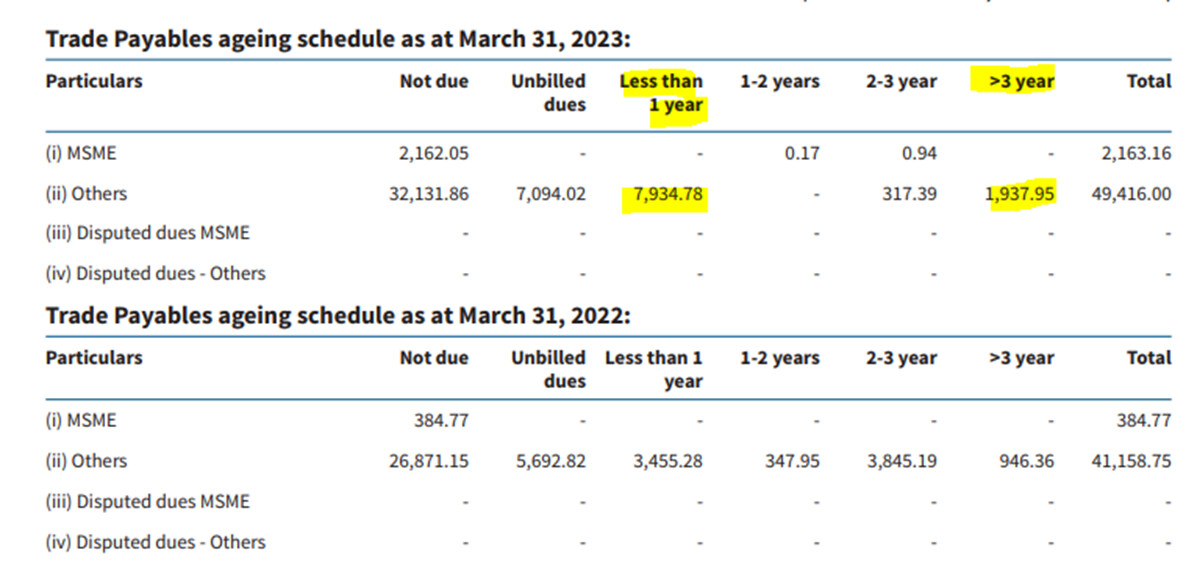

Debt free and cash rich seems mirage: Cash seems to be a business NEED to fulfill obligations due within 3 months

-

Suppliers seem to have tough time to get their payments released:

-

Heavy churn in the top management [particularly COO and CFO Roles | MD and CEO roles are occupied by the promoter family. Both are from non-technical background]. Relevant data-

Disc: No Position.

13 Likes

Sir, it is because Sharda Motors is catering mainly to ICE (as mentioned by you) or any other reason why the stock is not moving fast in upward direction (though it has risen from 1100 to 1415)

Because in 2Q concall Mr Ajay mentioned/asked about the undervaluation of the stock

Sharda Motors Q3 results.

9M EPS at 71. (not annualised) 9M Net profit 211 crores Market cap 4100 crores. Net cash 660 crores. Saleable valuable land in NCR region.

Technically on charts stock price close to previous swing high of 1380. All time high at 1494. Stock price has been making a series of higher highs and higher lows on weekly chart.

sharda q3 fy 24 results.pdf (1.3 MB)

disc: invested.

8 Likes

Thanks Hitesh bhai for the succinct summary of the results.

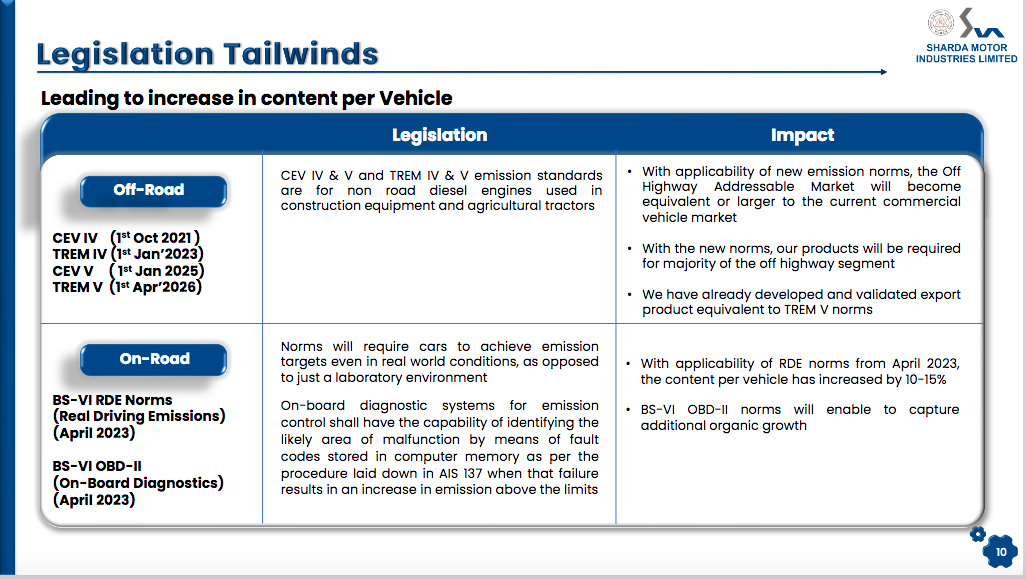

Another important thing to note from the investor presentation uploaded here is the following slide:

It appears that the timeline for CEV V has been moved forward by 9 months to Jan, 2025 and more importantly, the timeline for TREM V has been moved forward by 2 years to Apr, 2026 ! TREM V was a major growth trigger for the company and has now been kicked down the road by 2 years. Will need to question the management on where the next immediate growth levers are.

4 Likes

I listened to Sharda Motors q3 fy 24 concall. As usual it’s very difficult to expect easy to understand and forthcoming answers from management. Management is very conservative in answering questions in concalls. But whatever I gathered and deduced from concall is as follows…

Since past 2 quarters company has been benefitting from change in RDE emission norms for Passenger vehicles. The TREM emission norms have been pushed to fy 2027.

On being asked about the growth in company per quarter, management says a rough estimate can be made by looking at Gross profit gorwth. On calculating the gross profit, for which I used sales minus raw material numbers, I get figures of 139 , 131, 144, 137, 175, 172 ( all figures in crores) for last six quarters. It is a clear indication of benefits since past two quarters. On being asked how long this benefit can last, management was largely evasive.

The above issue came into play because the newer products sold do not account for Catalyst ( a part within the emission product chain) as it is not used in design of products for latest emission norms. And earlier too, Catalyst was only a pass through part for the company, not accounting for any margin. So minus the Catalyst, the sales amount shows decline but this calculation does not reflect the true picture.

e.g An emission product which earlier used to cost say Rs 120, ( with cost of catalyst being rs 20) will now cost 100 rs. If profit on each product remains same at rs 12, then earlier profit margin used to be 10% (12 % 120 multiplied by 100) but with the newer product (minus catalyst) margin is 12% ( 12 % 100 multipled by 100)

Near term growth tailwind is the new RDE norms based products. As the product matures its contribution to sales and margins improve. How long this lasts is anybody’s guess. Management is very reticent about this question.

The other growth driver is exports. China plus one factor is playing out better than expectations of the management. From the management answers, it appears that this could play out atleast partially in FY 25.

On use of net cash on balance sheet, management says primary focus is to go for a well thought out acquisition which could aid growth. Dividend distribution policy is spelled out which stipulates payment of anything from 10 to 30% of profits as dividend according to judgement of management. A couple of times mention was made as to provide shareholder returns and that something was being thought about it. ? Buybacks besides dividends. ? ( no clarity here)

On the information about land parcel in NCR region which everyone knows has appreciated a lot in recent times, there was no information about approximate value of the land being talked about.

All in all a concall which is reminiscent of most past concalls wherein while listening you try to grasp whatever you can and after listening when you think about take home message, it remains same as before. ![]() Nothing new.

Nothing new.

If anyone has better understanding of this company and concall, please put pen to paper and share details. I have put up whatever I have understood from a difficult to grasp concall.

14 Likes

I too listened to the concall. My takeaways were similar but as a macro understanding, from such a conservative management, the line that “the China plus one demand is much bigger than we anticipated” was interesting.

Thank you dr hitesh for clarifying what the catalyst price affecting sales figures meant. Wouldn’t it be possible for them to present the previous sales figures in the same manner? As of now I couldn’t make out whether there’s volume growth or degrowth but as you pointed out, management says better to look at gross profit figures and not top line.

The export market they are looking at is chiefly off road vehicles rather than PVs or CVs, and for that too, it will take time to build trust, but the emission norms in Europe are more or less similar to India, and they do have the technology to meet them, but again as Dr Hitesh said, the management was cagey in answering whether they are prequalified or not. They did say that if they are successful, can lead to substantial orders.

No clear answers about Capex spends for the next two years except saying that they will be “incremental” which I took to mean as not requiring significant investment beyond 40-50 crores.

I thought the management was indicating towards either a bonus or buy back by end of this quarter, but it was vague.

The only clearcut guidance is that “we will outgrow the automobile general market growth by around 10 percent”.

3 Likes

Listened to the conf call.

Basically, the business is a high NFAT one (and being decently profitable) and therefore generates more cash than regular business can utilize. Thus, it is imperative that the management shows a sense of urgency to deploy this cash which seemed missing. The last few calls, the updates have been static on this front. Management wants to buy cheap, which is good, but waiting for it too long is also a cost which management doesn’t recognize.

Else, their response to every question was generally non-committal barring they will outgrow industry.

1 Like

Hi Everyone,

While looking at Q3 24 PPT, I noticed in board member we have a MMBS degree holder and Practitioner Doctor in USA. Not sure why she has been added to the board.

5 Likes

Hitesh sir with company’s PE now trading around 16 with PB around 4.5 after recent results, do you see valuation comfort in this company and average up scope in growth story? I first time attended concall and promoters seem cautiously optimistic (not very optimistic) (in after thought, it may be good to under commit and over-deliver).

1 Like

Good set of numbers with QoQ and YoY growth.

9.92 rupees dividend. 50 crore capex in existing products in Chakan, to commence operations by Nov 2024. Was expecting higher dividend. Looking forward for concall.

buyback is already in progress.

buyback price: 1800 per share

type: tender offer

quantity: 10,27,777 shares

results of postal ballot will be announced on Friday, 24th May, 2024

after announcing the successful completion of postal ballot, record date will be announced and it will usually be within 10 days after that. so, tentatively the record date should be on or before June 4, 2024.

1 Like

I don’t think, the buy back record dates are announced yet…

Record date is 5 June.

What was the success ratio of Buyback for retail investor? Mean to say for retail investor, how much you were holding and how much bb debited? Thanks in advance…

Around 60%. The term is AR or Acceptance Ratio. 57/94 were accepted.

3 Likes