@vnktshb Sharda’s stake is 74% in the Kinetic JV

Some minor updates:

-

Trem 4 has kicked in as expected.

(ref - TREM IV emission norms may impact 7-8 % of domestic volume, says ICRA | Business Standard News) -

There was only one hiring post related to position related to battery engineering (4 months back). As the location is pune it must be falling into JV with KG. After that i haven’t saw any newer openings related to this JV.

(Ref - Sharda Motor Industries Ltd on LinkedIn: #hiringalert #pune #hiringtalent #automotivejobs #automotiveindustry…) -

No news about the delay of the rde norms from april 2023. This is list of few cars that may get discontinued due to increased cost (just a probability may be).

(Ref - Real Driving Emission norms coming in April 2023: affected cars, SUVs | Autocar India)

Doubt : If the green hydrogen story really kicks in. FCEV would probably be emitting only water vapour and warm air. Is it very easy for oem’s to manufacture their own exhaust ?

My Assumption : As harmful gases won’t be there, so catalytic converter with metals is no more required. Sensors also won’t be that much required. But NHV ( Noise, vibration and harshness) would be still there. So muffler, resonator & tail pipe should still be present. So SMIL can still play with the integration.

3 Likes

Q3 Results. Almost flat on QoQ revenue basis. Employee expense has increased by 7.5+%. Please share your thoughts.

Flattish results from Sharda. Revenue is down 1.7% while PAT is down 14.8% QoQ.

Gross margins compressed by 169 bps QoQ and EBITDA margins by 149 bps.

JV with Eberspaecher had a profit of 21 lakhs as compared to 52 lakhs last quarter. JV not scaling up as expected.

I am also tracking Mahindra, Toyota and Tata Motors quarterly PV sales as a monitorable for Sharda as they are their top customers.

The quarterly PV sales (no. of vehicles) trend has been as follows (Source: FADA):

| Oct-Dec 22 | July-Sep 22 | Apr-Jun 22 | |

|---|---|---|---|

| Hyundai | 133929 | 122362 | 113339 |

| Tata Motors | 124115 | 110208 | 108669 |

| Mahindra | 85025 | 63344 | 61428 |

The PV sales of all the 3 OEMs have been increasing QoQ with Mahindra registering the highest growth. With these OEMs showing good growth, one would have expected it to reflect in Sharda’s numbers. However, the flattish sales growth doesn’t validate this correlation.

Edit

Since Sharda’s standalone entity caters to PV + LCV, we should also look at LCV numbers. Adding consolidated LCV sales data below:

| Oct-Dec 22 | July-Sep 22 | Apr-Jun 22 | |

|---|---|---|---|

| LCV | 130682 | 125464 | 122912 |

The LCV numbers also have shown moderate growth QoQ.

The management has been questioned on the correlation with sales data in the past. As per them, Sharda’s sales are more correlated to engine sales and there is a time lag between when they sell to the OEM and when the actual car sale happens.

The management has also promised to share some metric/index with the investors to track the key monitorables. Will try to goad the management in the concall to provide one.

7 Likes

Q3FY23 concall notes

- 588 crores of cash in the balance sheet

- Management was constantly asked on providing an index so that investors can compare Sharda’s growth against the industry growth on PV/LCV/CV. Management has for the last few concalls said that they are working on sharing an index and are close to having one. The answer was the same this time as well.

- In the CV joint venture, they are working on modularization of exhaust systems. This will allow them entry into older engine families that are in the market.

- No slowdown in CV JV revenues

- On exports, they are working on a large number of RFQs and are expecting some test orders. If the test orders succeed, then this can scale up. China +1 looks to be playing out

- In the EV joint venture, the assembled battery prototypes made by them are still in testing phase. Prototypes were readjusted to the new AIS amendments on safety.

- Management was also questioned on the high cash balance and how they want to deploy/share it. Management wants to utilize it for M&A in a power train agnostic space. Management was requested to earmark a certain amount for M&A and then look at distributing the rest to shareholders.

- The move towards CNG by OEMs in the LCV/MHCV space is neutral i.e. even though diesel exhaust systems have more content per vehicle compared to the rest, a move away from diesel to CNG may not impact the content per vehicle much for Sharda.

- Management was requested to provide a rough cut estimate of the tractor exhaust system market size now that they have TREM 4 sales in their revenue

My impression

- Not much new information from the concall.

- Even though the management has been conservative in concalls and not forthcoming on guidance till anything materializes, this time I felt disappointed when the management said that they didn’t have the quarterly and 9M revenue numbers in front of them for the CV joint venture. This is despite the CFO being there in the call. Managements usually have these numbers on their fingertips.

- Will keep watching for execution on exports and RDE in the near term. The larger potential upside due to TREM 5 is still a year away. There is value at current valuations but need to be wary if this can become a value trap.

Disclosure : Invested with a 3% allocation. Slightly reduced in the last 30 days as a part of portfolio rebalancing.

7 Likes

Even though we don’t have any other pure Indian competitor who manufactures the exhaust systems for passenger vehicles , how should we arrive at a correct valuation for SMIL ?.

These are just rough estimates, i also have considered small sales due to TREM V as OEM’s would already procure to make it ready for April 2024 (subject to correction) :

Sales of FY23 would be around ~ 2700 crs (considering one more flattish qoq)

Projected revenue for FY24 : ~ 3250 (20% & being conservative)

Projected EBITDA FY24 : 325 crs (considering just nominal 10%)

Projected PBT FY24: 284 Cr (41 crs , as depreciation for last 3 years were 40,43,40)

Projected PAT FY24 : 210Cr (considering normal 26%)

EPS projected FY24 : ~ Rs 70

so FY24 projected P/E would be ~ 8.6

This is including the RDE & some trem V sales. Is the 20% growth on the higher end ?.

I have tried reading a bit about Faurecia & Tenneco to understand about the valuations. But both are very diverse & are ventured into lot of systems so a bit difficult to correlate. If i just take the Tenneco’s clean air entity, the last q3 has a growth of 25% on yoy & >10% for the 9M on yoy . so there is no de-growth visible even in large mnc’s. (Ref : https://www.tenneco.com/news/news-detail/2022/10/31/tenneco-reports-third-quarter-2022-results).

Also we have a company called Munjal Auto, which is into exhaust systems & rim’s for motorcycle’s which trades at 15 times at the CMP & with just single client constituting for more than 80% revenues.

So, I feel SMIL has good value at the CMP, even considering a nominal median P/E of 14-15.

Also considering very good cash reserves, we may also see an M&A in power train agnostic stream in near future. As the next decade will see a diverse range of power train vehicles coming into the market (Pure EV/Hybrid ICE/H2 ICE/H2 FEV) it is good to be agnostic to the power. Also the exports of subcomponents of the emission system would also be a very good opportunity.

Even though i feel the BMS JV with kinetic green is going a bit slow & also the SMIL management is bit conservative in the concalls. The management of KG has been very aggressive in their estimates of 2W/3W sales. They also have made some good JV’s & tie ups. They also are hiring few talented folks (ref: Kinetic Green appoints Vijay Bhatt as Senior Executive VP for two-wheeler business | The Financial Express). So on an overall KG seem to serious & fighting for the market share. Indirectly it should benefit the JV if it continues.

Disc: Have 6% allocation. Added slightly after the recent fall.

3 Likes

There was one new job posted by the company a few days ago for the manager position to look after sales, customer costs, and commercials for SMIL’s new customers in the western region. More details about the job Ref - SMIL-Manager-western-region.

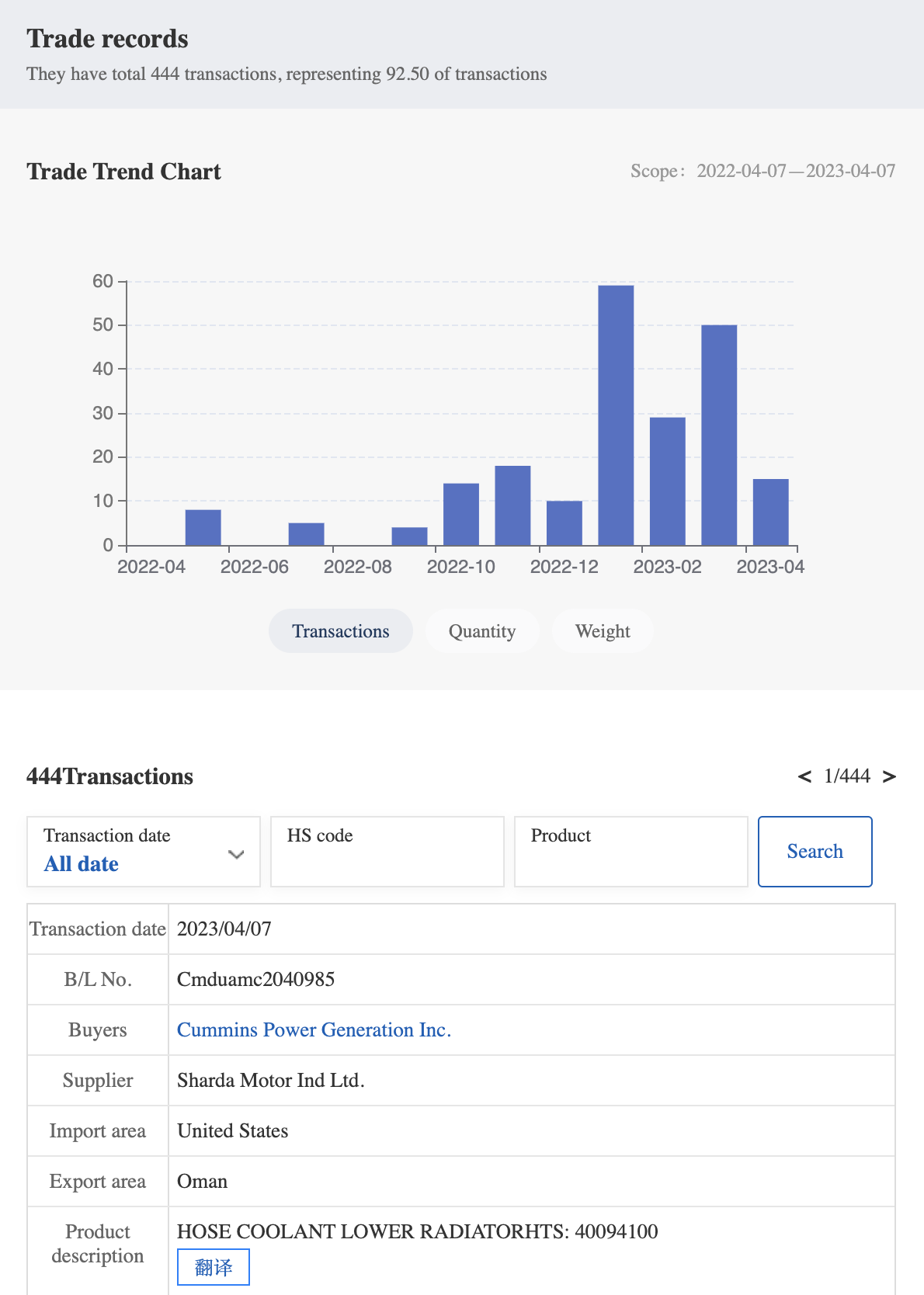

I also have tried looking at the export numbers of the company on monthly & yearly basis. The exports timeline have actually picked up from Dec-2022. This data only is upto April 1st week 2023.

Based on the superficial data, the majority of the exports are seems to be going to Cummins, USA. Sample trade snap ref :

Some of the product categories that i could extract on high level are :

- Coolant Hose for the radiator.

- Silencer/exhaust related

- Other coolant system parts (Mostly radiator related again)

- Other generator related parts. etc …

It looks like the exports have picked up finally, which management has been talking about in the last few concalls. The job opening position also kind of validates the data.

Disc : Biased & Invested. No transaction in last 30 days. No buy/sell reco.

10 Likes

great result with a final Dividend of Rs. 17.27 per equity share

1 Like

It appears that the Q4 concall scheduled on 19th May was cancelled? Does anybody have any update on the status of the call - did it happen and if not, is there a new date? There are no exchange notifications or emails from the company as far as I can see.

Called Sharda motors office today to enquire if there is a new date decided for concall. The person at other end had no idea about it.

Same experience.

The person on the other side of the call is the security guard. Company has mentioned that number everywhere, even for the IR details as well.

Hi Shahikanth, Since you have obviously done a bit of reasearch in SMIL and you are invested. I would like to put a few questions to you. The company is obviously very healthy. Zero debt, good market position, favorable financials and a pile of cash. The promoters also seem reputed. Why doesnt the company have any expansion plans. The JV and other investments are incremental and also in unrelated fields. If they enjoy such a monopolistic position, why arent they expanding. No doubt they have a healthy topline growth but i feel a lot of that comes from recent inflationary reasons or better sales and product mix. Am i correct or am i missing something? Regards.

Hello Nitin,

There are different layers here.

Exhaust Related: There is no need to go for an aggressive capex or expansion here. Fixed asset returns are generally very high here, just like many other auto ancillaries or other manufacturing companies. Like stated in the above thread JV on MHCV, Trem 5 on tractors, RDE to some extent are growth triggers. As per management incremental small capex is enough to cater these opportunities. In terms of PV, ex-Maruti market is mostly consolidated here. There is still some opportunity on the CV side. Again all these depend on the OEM enquiries & particular engine to do well.

BMS JV Related: My impression is they are slow here. Management still refers to only design & assembly of BMS. Management commentary also seems over cautious & want to be asset lite. They want to understand more on the market & opportunity. They might actually even miss the bus also if they are so much conservative. So backward integration is possible in BMS pack. Atleast one good part is the partner KG is having good plans & they seem to be on the track. Kinetic Green New plant

M&A and Cash: I’m fine if the management is being cautious here. we can’t expect every management to be aggressive in deploying cash or go for capex every now & then. Some say likes of (Deepak nitrite, SRF etc) are unique or in other cases business expects you to do (laurus etc). The power train agnostic space is pretty large, they have to analyse so much to finally settle on something.

Exports Related: They have just started, SKU’s might be so many here. I only see cummins as the major client here. Capex depends on the size of orders. Management can elaborate more on the opportunity. Good thing is atleast i can see the trend continuing, exports visible in April & May too.

4 Likes

Hi!

I have a few questions related to the company and hope to get some help from here:

- Did the Q4 2023 conference call happen?

- Does anyone know the outcome of the search/seizure by the IT department at the company?

- In the 2023 year-end balance sheet, other financial assets (current) have increased from 4 cr to 405 crores. Does anyone know a further breakup of this category?

Thank you!

@manpritaurora @nirvana_laha @T11 Thanks for the detailed insight about industry and company specific

@nirvana_laha sir, you had raised question on 330 cr increase in other financial asset, did management revert on this subject, since details were not handy during the call (In reference to Q1 FY24 earning call).

Is my understanding correct?

Catalyst procurement will be stopped going frwd which will optically impact just the topline, whereas % margins will jump.

Thanks.

@nirvana_laha sir, you had raised question on 330 cr increase in other financial asset, did management revert on this subject, since details were not handy during the call (In reference to Q1 FY24 earning call).

This is just a re-classification of FD with > 12 months maturity from CCE to Other Financial Assets. You can check Note 15 in the consolidated statement of accounts in the AR.

Is my understanding correct?

Catalyst procurement will be stopped going frwd which will optically impact just the topline, whereas % margins will jump.

He did say for new models and RDE components, catalyst will no longer be shown as pass through. For older models, I guess the earlier arrangement will continue. So yes I guess that should result in the true EBITDA margins showing up gradually as new models’ share increases. There is no material change in the quality of business due to this.

1 Like

- Did the Q4 2023 conference call happen

No, it didn’t. And no explanation was provided either. We have to assume that management was too busy handling the IT Dept. But it did leave a bad taste for shareholders.

- Does anyone know the outcome of the search/seizure by the IT department at the company?

The company has said there is no update yet from the Department.

- In the 2023 year-end balance sheet, other financial assets (current) have increased from 4 cr to 405 crores. Does anyone know a further breakup of this category?

Replied above.

1 Like

Hi, @nirvana_laha

excellent research on competitors and their customers.

As per SMIL’s management they have a market share of 30% in PV & LCV (combined) and it’s a concentrated industry with 3-4 major players (which you have covered). If they are largest player, then essentially, rest of the players market share is less than 30%. In that case, my total is not adding up to 100%. Is it possible that the competitors are not reporting their revenue under one entity but multiple entities?

Your thought on this would be helpful.

Thanks.

1 Like

- In the 2023 year-end balance sheet, other financial assets (current) have increased from 4 cr to 405 crores. Does anyone know a further breakup of this category?

You Just read Annual Report FY23

Note 8: Other Financial Assets (Unsecured and considered good, unless otherwise stated)

with Note 15: Bank Balances Other Than Cash and Cash Equivalents

a) The above deposits include ` 210.04 lakh (March 31, 2022 :90.53 lakh) which is given against Bank Guarantee to Various Authorities.

and FDR for more than 12 Months is classified under this head.