This would be my first post in VP. Looking at the good financials, I decided to dive little bit deeper into this company and have few questions:

Company is capitalizing its R&D cost on balance sheet which tends to artificially inflate profits for a while until amortization comes into play. Isn’t it a bad practice, other company in this sector are doing the same?

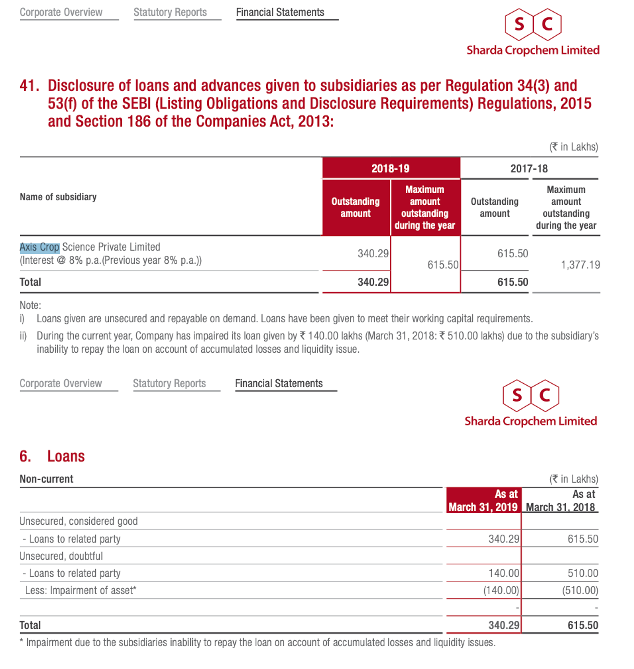

Company has given loan to one of it’s subsidiary namely Axis Crop Sciences@8% and wrote off around 6.5 Cr during FY18 & FY19 on the account of subsidiary inability to pay (screenshot from balance sheet is attached). Now from what little knowledge I have, its look like promoter may be siphoning money as he has 100% stake in subsidiary company and may be deceiving minority shareholder of Shardacrop chem. Is my understanding right? I may be wrong as I am still learning.

Superb set of results from Sharda (sales growth of 78%, PAT growth 112%). Management was very bullish in their commentary. Gross margins have finally turned around from the lows of 30% to the 34-35% trajectory. Management is seeing Chinese raw material prices cooling down and expects current margins to sustain. They are even guiding for volume growth of 20% in FY23. Here are my notes from today’s concall.

Europe is the most expensive geography to get registrations, prices can go up to 4-6 mn Euro. Time required for procuring the registration can go up to 8-9 years.

EU approval process: First need to get an EU wide AI approval. After that, formulation approval needs to be procured in countries individually

Most products are sold through distributors and not directly to farmers

Current focus is on widening product portfolio rather than geographical expansion

Recent growth expansion has been due to company strategy + strong market connect. These sales are sustainable and company is expecting volume growth at 20% going forward while maintaining current EBITDA margins

Have witnessed easing of Chinese raw material prices in FY22. This quarter gross margins recovered to 34%. NAFTA gross margins were 36% (even higher than EU gross margins of 34%)

MNC strategy is to keep a high listing price and then provide additional discount to dealers. This has probably contributed to 26% pricing growth for Sharda

In the broader context, they are a very small and diversified player. There is not even 1 molecule in any geography where company has a 10% market share

Most of the non-agro business is made to order resulting in negligible inventory holding. This is largely a services business. It is mostly conveyor belts. Gross margin in this business line is 30-40%

Product pricing strategy: around 10% below innovators

If I draw parallels to the generic pharma sector, we see significant price erosion within a couple of years a molecule goes off-patent. We have seen well run companies like Alembic Pharma succumb to this issue, when statins prices plummeted.

Isn’t this a structural risk to Sharda’s margins? Especially when they have little control on their costs due to the outsourced strategy?

Risks are in every business, we should try to discern what risk exists in a business, how well a company is positioned to take care of these risks and how we can position our own portfolio to take care of these risks (through purchase price and position size).

Sharda’s business model is actually more resilient than a lot of technical manufacturers due to their low cost structure (mostly working capital + registration cost). Techical manufacturers derive most of their sales from a few products. If demand for any given product declines, they are hit in a much more significant way as they have dedicated manufacturing lines in their factory. On the other hand, a formulator like Sharda or UPL owns a large portfolio of registrations and face less product specific risk. They can change their procurement strategy depending on the end market demand as they don’t have to run dedicated manufacturing lines in a factory and pay salary to the workers. Sharda’s business model is nowhere close to that of alembic pharma as alembic operates across the entire value chain (API, formulation, marketing). Sharda’s business model is closer to that of a Chaman lal setia (albeit from a different industry) where they largely manage working capital and product registrations.

Sharda is coming out of a bad patch where their gross margins went <30% from the normal gross margins of 35%. Also, in this whole downturn, they have grown sales and profits by >20% CAGR (much higher than industry growth). At the end of the day, global agchem is a cyclical business and we should try to understand where we are in the cycle and take appropriate decisions. Hope this clarifies my thought process.

I have interacted with this company earlier in a professional capacity. The company is run by a fantastic, fanatical promoter who micro manages everything even at this age, which is both a big plus as well as a big minus.

Also the biz model is very unique where they don’t have any mfg capacities and procure/import most of their products which is a risky strategy.

Basis an initial reading of the publicly available documents of this company,

this company comes as a global distribution and marketing firm for generic agrochemical molecules/products. To put it in a crude fashion, this business is a play on the intangibles with hardly

any skin in the game, merely matching the demand and supply (third country sales).

Considering the nature of the business, would expect the business to command higher ROCE/ROIC,

However, with China being a major manufacturer and supplier of agrochemicals to the world, what prevents a chinese firm from entering this business? Is there any entry barrier/challenges or are there some global competitors to Sharda already?

Moreover, the business is faced with the risk of annulment of the acquired registrations, leading to

increased write offs of the intangibles, which could be detrimental to the business. Any thoughts?

Are there any annulment of the Sharda approvals in various countries in the past ?

Entry Barrier - Understanding the nuisances of each country and then getting approvals itself is a big barrier to entry. A typical end to end approval for product takes 5-7 years

Regarding china dependency, after all this China + 1 and Atmanirbhar from India still the world is dependent on china. Tomorrow if the AIs are available in India or any lowest cost producer then the Sharda goes to them to make for them.

Yes, anyone can enter but there is a huge gestation period

From what I understand, there are two major competitive advantages of Sharda:

Holds a very large portfolio of formulations registered in regulated markets which is expensive to get (can cost $3-10mn per formulation), requires time (3-10 years on average) and know-how of bureaucratic setup of each country. Registering technicals on the contrary is cheaper and that’s where most manufacturing cos focus.

Very strong supply chain capabilities. This was clearly evident in FY22 where majority global agchem companies struggled to procure adequate quantities of technicals to make their formulations (see numbers of global marketing agchem cos). In this setup, Sharda managed to grow volumes by 50%+ despite sourcing mostly from Chinese cos.

Now the more useful question to ask is who are the suppliers that Sharda is sourcing their technicals from. Management has said in the past that most of their sourcing is from smaller cos, maybe they were not adversely impacted. But I don’t have a definite answer. All I can say is it seems Sharda’s supply chain is more resilient than other agchem cos. Another thought process can be that Sharda maintained higher inventory in US due to just in time delivery model, maybe that’s why they were not impacted and gained market share. But if this is the case, they cannot deliver 15-20% volume growth in FY23 (which management is actually very confident of delivering).

To create a portfolio of 20 technicals, it will cost cos more to register these products in regulated markets than to build a factory. So its expensive + requires long time. Also, Sharda sources most technicals from smaller cos who may not have the same balance sheet capabilities.

In Europe, a formulation registration is valid for 10 years after which they need to be re-registered. This is true for every company and part and parcel of the business. About intangible write-offs, I think this needs to be monitored as I don’t understand the exact reasoning behind these. Below are the numbers (~12% of EBITDA)

FY19

FY20

FY21

EBITDA

372.21

352.53

455.17

Intangible write off

42.24

54.65

38.32

Write-off % of EBITDA

11%

16%

8%

Disclosure: Same as before (no transactions in last 30-days)

Is the validity of the formulation registration 10 years across all geographies or is it only in Europe?

Trust the tenure is the same for AI and formulation. How about renewals?

There is mention of data compensation charges to MNC/Innovators, which is also being capatilized. Any idea what are these?

I dont know the period of validity in each market, in USA its around 15 years.

About Pesticide Registration | US EPA.

For other markets, maybe you can look it up and keep us updated. For renewals, management has talked about it numerous times, the process varies across molecules and markets. You can find the same in concall transcripts.

If you want to understand this, a simple google search result reveals the details.

I don’t think any management will reveal these charges on a molecule or an aggregated basis, just like no pharma company will reveal how much they paid for a ANDA application and where they got their bioequivalence done.

The fundamental question then is - if the registered molecules/products are valid for as long as 10-15 years, why is the amortization of the intangibles over a period of 5 years only, incurring a steep depreciation of 20% yoy? Probably a question to the management if the answer is not known.

I think there is no right or wrong answer here. Though the length is 10-15 years, the potential of the molecule might be more during initial phase and over a period of time the sales might slow down. (This is my wild guess). If it is allowed to amortization intangible assets in 5 years period then it helps company paying less tax.

The potential of the molecule being more during the initial years could be true - this thought did occur to me.

In my opinion, the window of 5 yrs to milk a molecule seems too short a period considering the various

uncertainities/challenges around raw material costs, product demand/price, seasonalities, increasing registration costs, macro issues, governmental beaurcracies, cancellation of registrations, to name a few. Because, once a molecule is completely amortized, it cannot contribute to the cash flows.

Q4 results are declared. Super results to say the least

Debt pared by a small quantity with whatever cash flow has been available. Big receivables will help to address more liabilities next year. Revenue growth has been phenomenal as guided by the management