I am not sure if my understanding is correct. But there are a lot of stories spoken on the pharma opportunity but nothing really is showing up on the numbers.

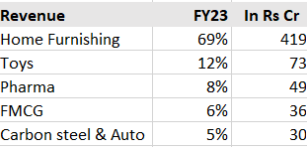

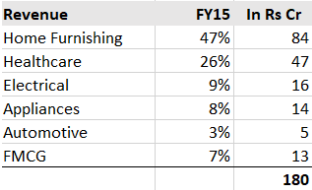

1.Got some scattered segmental numbers - FY23 from crisil report, FY15 - company disclosure. Pharma is flat

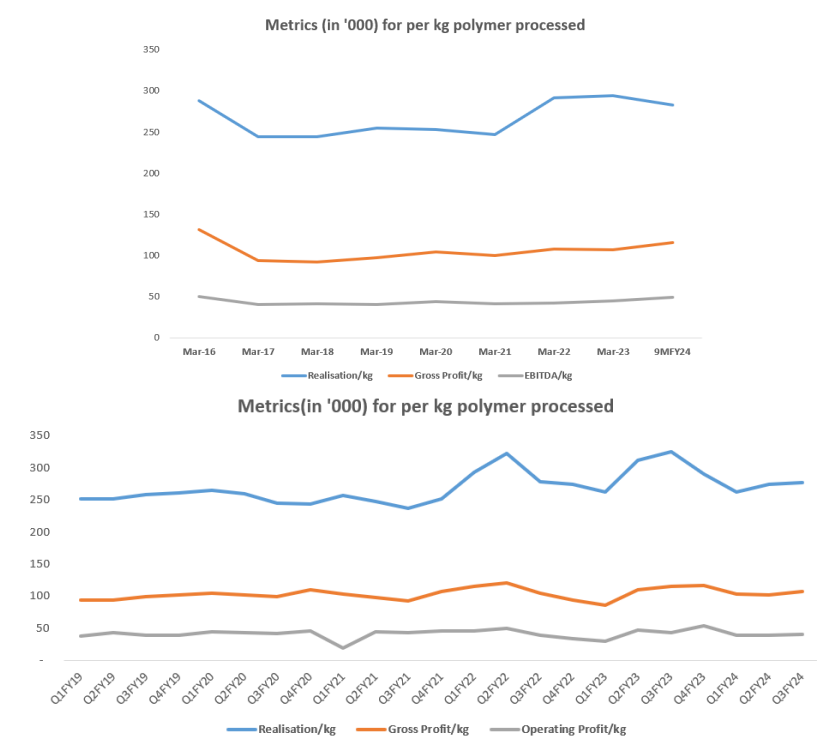

If pharma is really positively influencing, realisation per polymer processed should improve right, how does one view this?

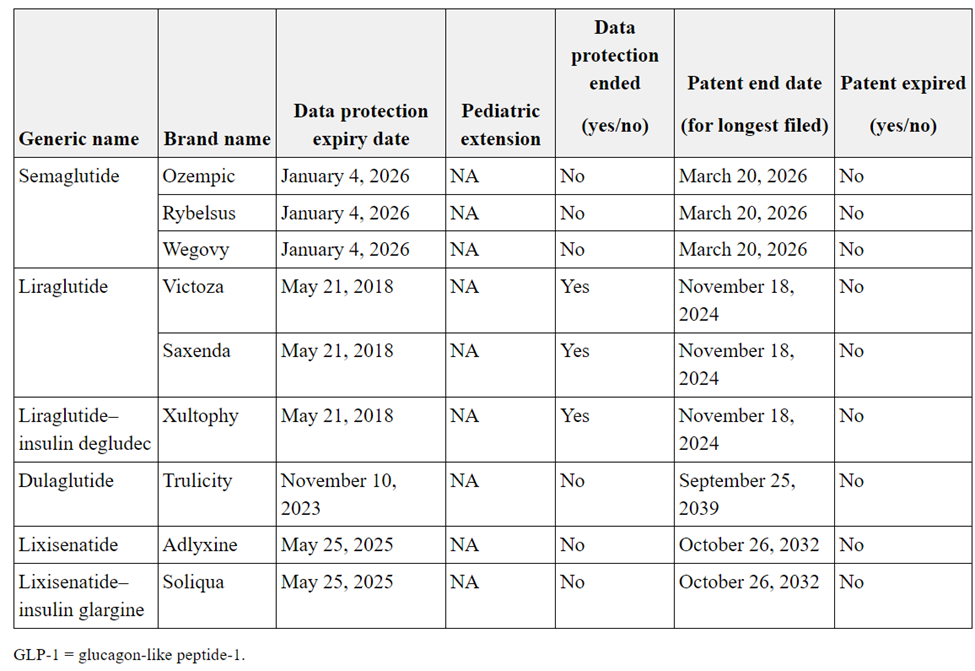

How do you look at the addressable market of the three drugs that they keep speaking about - Semaglutide, Terixxx, Liraglutide? So, $XXXBn of opportunity would be how many pens. Lastly, Their addressable market would be much small right, because they are working only with Sanofi, What about Novo and Lilly?

Looking at other players in the drug delivery market - they are growing pretty well it seems, where is Shaily lacking?

Hi. I am going to study this in detail and get back. Please confirm what is the data source or sources for the figures and charts you shared in your post. Just to make sure that we both are looking at the same thing.

I agree that in terms of revenue the company has not shown any increase in pharma or healthcare.

Once again, I agree. We are not seeing any meaningful difference in realisation per kg polymer processed.

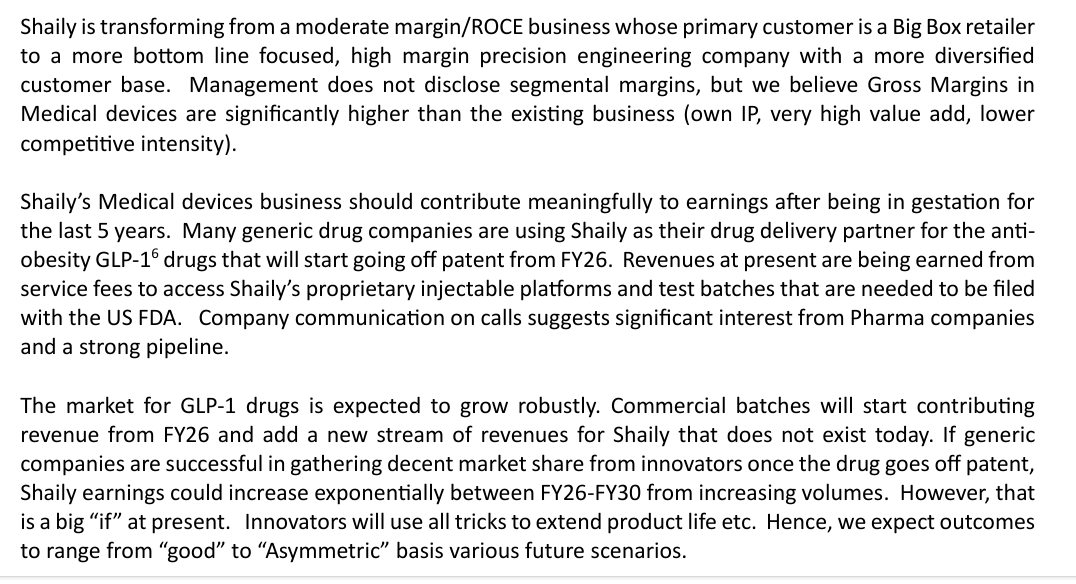

I am going by what the company has referred to in their latest concall. See the below screenshot. Amit is referring to how this market may grow to half a billion pens a year. But you are right. The company is totally dependent on how big a share of that market does Sanofi get or how much market goes to generic manufacturers who also then use Shaily’s products.

I think they took some time in trying to understand how to organise their business. For example they started the toy business a few years back and are now retreating from it. In the interim they also kept looking for a CEO but have now put that project on hold. They have recently done a capex of 100 crores specifically for Pharma and my guess is that they are now feeling confident of that getting converted to revenue real soon. Otherwise why would they sink so much money into capex which will lie underutilised for the next couple of years. But this is my optimism talking. Let’s wait and see what kind of revenue and profit starts getting generated from the pharma business.

@aadhar.aggarwal@Cuckoo_Invests The main hope pharma division is flat over almost a decade, management has repeatedly missed guidance and now saying pharma will actually break -out. Beyond hope, what is the strategy here for investors?

Tried to decipher and digest all the useful information in the last concall. Due to the great questions, a lot more details on the healthcare business came out in this call - especially regarding the active ongoing accounts, molecules and platforms. Although its not complete, its a good start and I’ve tried to capture the information here.

Healthcare revenue at 107.7 Cr in FY24 (~17% of revenue) up from 57.6 Cr in FY23 (~9% of revenue). The growth in healthcare is 87% and is expected to grow 50-60% in FY25.

In this 107.7 Cr, the difference in standalone and consol. is 28 Cr in topline and 22 Cr in EBITDA. We know that this 28 Cr is all in healthcare business of Shaily UK (platform access fee) which means the standalone entity has a revenue of 80 Cr in healthcare.

We know that standalone entity does contract manufacturing and own IP pens and we know from this concall that the ratio by value is 70:30 or 60:40… lets take it as 65:35 which makes the contract manufactured insulin pen revenue at 52 Cr and own IP pen at 28 Cr (excluding the platform access fee of 28 Cr)

Volume growth in pens to be around ~45% (17 million pens vs 11.5 million pens). This growth is expected to come from Insulin pens as well as GLP-1 pens. Insulin pen growth could be driven by Ypsomed getting out of contract manufacturing which could be Shaily’s gain (and also since insulin pen base is still considerably small as compared to Ypsomed). Since value growth is guided for 50-60%, GLP-1 volume could be bit higher than the Insulin pen volume.

New business wins in last quarter - 2 Sema and 1 Lanreotide

Platforms

Platform

Molecules

Clients

Misc

Maxim

Insulin, GLP-1

Protean

Insulin, Victoza (Lira)

Low-cost platform. Insulin in non-regulated markets. Good scale-up expected here

Axiom

Teriparatide

7

Approval expected by end of year in regulated markets

Neo

Saxenda (Lira)

Toby & Tristan (Auto-injectors)

Wegovy (Sema), Mounjaro/Zepbound (Tirze)

4

Shaily safe lab

Lanreotide

2

Under discussion for adding 2 more.

There’s also ongoing work on on-body injectors with electronics that will be used in Onco and pain management (under development).

Molecules

Molecule

Clients

Misc

Lira (GLP-1)

5-6

Sema (GLP-1)

6

Tirze (GLP-1)

2

Looking at adding fair bit of new clients in NCE-1 filing. Maybe 4-5 total (2-3 more new expected this year then). Supply of clinical batches by Nov this year.

Teri (PTH)

7

Insulin

2

Total

23

12-15 added in last FY in this

Approval expected in US/EU regulated market for Liraglutide and Teriparatide this year (Lira second half and Teri maybe first half but Teri will hit the market by end of year if all goes well). IMO, this could be a huge trigger as it opens up large opportunity size in the long run to work with Novo or Eli Lilly. We also know for certain that there are 4 new accounts in the pipeline (2 for Tirze and 2 in Lanreotide).

2 new FMCG products, 2 new pen injector contracts (1 lanreo and 1 sema), 2 components for automotive customer

Getting into Human Factors Engineering to cater to big pharma

1 pen injector purchase order for 10 million devices per year (own IP insulin pen) - context is 11.5 million pens done in FY24 and most were contract manufactured

Revenue growth will be much higher over the next 5 years

Tirze clinical batches will start end of year or next year (tooling and design work going on now)

Teri/Lira launches this year in regulated markets in EU/US. Sema in '26 India/Brazil/Canada/China. Rest by 2029. Tirze 2030 RoW and 2036 in regulated

Every pen in the market except Novo’s FlexTouch and Shaily’s Neo are mechanical pens for Semaglutide and not spring driven - others have IP challenges

3 Exhibit batches (3 PQ batches) are supplied on each contract for pen injectors. Per batch is 10k so 30k total in PQ batches. For different strength, there are separate exhibit batches - so for sema, it could be 90-120k per customer. Then operational qualification, design verification, final assembly trials are extra

Of the 25 projects, most of Teri, Lira, Sema (Ozempic) exhibit batches have been supplied. Sema (Wegovy) is starting

Shaily UK will see above 35-40% growth in FY25. Pipeline is quite strong

Two new projects in Shaily UK for two new type of drug delivery devices - which aren’t yet generating revenue but under active development (Premium Reusable device, Nasal soft-mist inhaler)

Working with some consumer electronics companies - very early stages

Home furnishing 50 Cr, Pharma new applicator 35 Cr and Engineering plastics for GE around 40 Cr have started and on track in Q2 (no delays)

Home furnishing demand in plastics and carbon steel - no big growth expected but some growth will be there from new projects. Carbon steel there will be some growth

Q1 healthcare business had a lower growth because of a technical issue which has got resolved and supplies have resumed in Q2

CDMO fill/finish partner has no involvement in verifying design (limited knowhow in India). Shaily’s contracts are with pharma companies and verification happens there

Working on Monoclonal Antibodies using autoinjectors but its too soon.

18-24 months to capacity expansion. Currently at 40 million devices (some platforms might need expansion)

Ypsomed moving away from Insulin towards GLP-1 opening up the space. So several ongoing discussions underway and order pipeline is getting stronger. (The 10 million order could be a precursor for more such)

2-3 million pens in Lira possible by FY26/FY27 - could be more depending on launches and Customer’s success rates

70% of sema generic market can be captured by Shaily. Working with MNCs and small biotechs as well, alongside Indian generic players

Consumer electronics - will be working with HPP (High-performance Engineerig polymers) than ABS.

Shaily devices won’t infringe - $180k spent to conduct FTO (freedom-to-operate) to ensure same

One of the informative pieces I came acrossfrom Ypsomed. Highlighting a few things I found interesting

The market is much beyond glp-1. Pretty much anything that’s a biological is a potential market and this market is growing. Some of the existing interferons, monoclonal antibodies are offered through pre-filled syringes (most generic humira launched last yr for eg.) and due to patient preference might migrate to auto-injectors as well. It is nice to know Shaily is working on auto-injectors for monoclonal antibodies as well.

Ypsomed has 220 projects (commerliased + pipeline) and shaily is today at 25 total. Shaily is picks and shovels player in the generic market which means a lot more projects for same molecule/therapy than a device maker that primarily works with innovators

Disc: Invested. Added in the last 30 days and likely to be biased

Hi wanted to get your sense on valuation for stock. How do you see buisness doing in terms of sales and profit growth. Pharma buiz ( pen injection ) seems to be on a good footing where growth could be high 30-40% or more. How about other line of buiz as managemnet hasnt given much guidance . Heard last 2 calls to understand buiz.

Also they mentioned of new capacity in 18-24 months does that mean they are currently at 45% uttilization and will exhaust all capacity ( is this for overall buisness ) missed this in concall.

How do you see the buisness growing in terms.of nos .

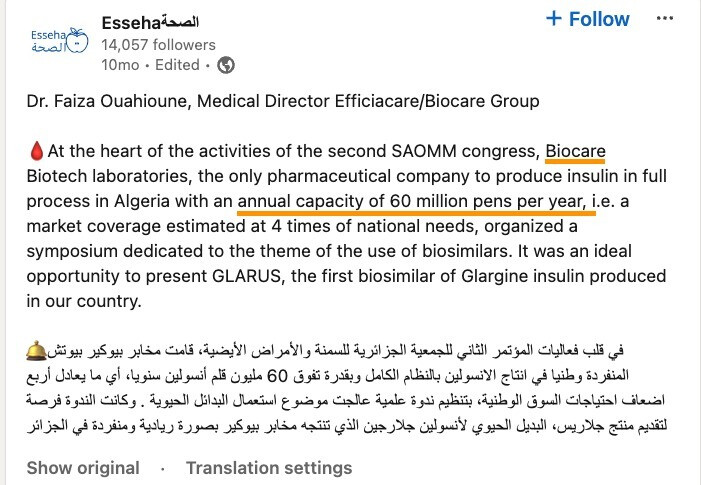

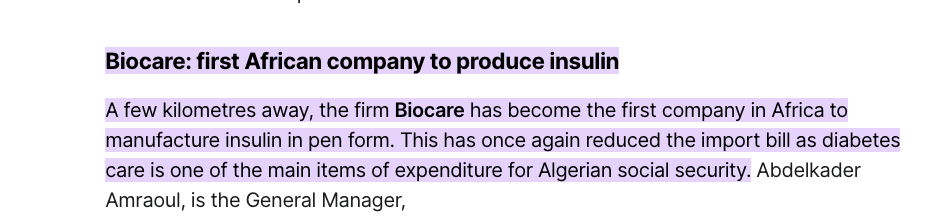

There’s a gradual scale-up to Biocare Biotech seen in exports data last couple of months - almost to the tune of 200k pens. It appears more or less likely that this is the source for the 10million own IP insulin pen order.

BioCare seems to have started production fairly recently and has capacity for 60 million insulin pens

It looks like Sanofi, Algeria was importing insulin and probably doing fill and finish there and had a capacity of 100 million pens (was also exporting to rest of Africa).

Somne regulation seem to have changed (either duty on imports or withdrawl of subsidies, its unclear) which has made things difficult for Sanofi once the import substituion plant of Biocare started production.

So two things are clear, there could be more to the 10 million pen order, considering the total capacity of 60 million pens at Biocare. The increase in volume from contract-manufacturing to own-IP is structural since regulation across the world have made things difficult for players like Sanofi (Lantus having price restriction in US as well at $35). Shaily volumes and margins have a potential to go up. To put it in perspective, at Rs.60 per pen, the 10 million pen order is worth 60 Cr. The whole of healthcare revenue for Shaily in FY24 was just 108 Cr in FY24 with 80 Cr coming from manufacturing. That puts this 60 Cr in context and any further volume scale as well in better context.

This may also have to do with the supply not able to meet the demand for weight loss drugs offered by Novo Nordisk in the USA and there was shortage of Ozempic, Wegovy, Mounjaro and Zepbound there.