Unaudited Standalone and Consolidated Financial Results for the quarter and half year ended on 30th September 2024

I have been following US elections keenly and looks like the Trump could be winning with unprecedented majority allround. As per my friend with knowledge on US govt, Republicans could pass laws as well. JFK jr will be assigned with health and food department if everything goes smooth. And he is very against these weight loss drugs being promoted by US govt as well as individuals using them for weight loss instead of nutritious food. Dont you think it is big risk factor for Shaily and other pharma companies, which depend on US consumer/govt/insurance provider paying hefty amount for all medicine related stuff? On the other hand Indian companies which are pure play generics suppliers could have good business going forward, you f this eventuality materializes. Better keep an eye on RFK jr handling of health food department.

Disc: not invested in Shaily at any point of time. I have very limited understanding of shaily business model as well as overall equity investing.

4 Likes

Shaily Engineering Plastics Ltd -

Q2 FY 25 results and concall highlights -

Revenues - 192 vs 157 cr, up 22 pc

Gross margins @ 46.3 vs 37.9 pc ( up 8.4 pc !!! )

EBITDA - 41 vs 26 cr, up 56 pc ( margins @ 21.5 vs 16.9 pc, up 4.6 pc !!! )

PAT - 22 vs 11 cr ( doubled )

Sharp improvements in gross and EBITDA margins is due to steep improvement in sales in healthcare division which grew by 94 pc in Q2 on a YoY basis

Capacity utilisation across plants @ 42 vs 39 pc

Segment wise revenue breakup -

Consumer - 72 vs 80 pc

Healthcare - 20 vs 12 pc

Industrial - 8 vs 8 pc

Domestic : Exports revenue breakup @ 25:75 vs 27:73 in Q2 FY 24

Expecting healthcare segment revenues to grow to 25 pc of sales inside next 3 yrs ( vs 20 pc currently )

Revenues in consumer segment grew by 10 pc YoY. Have received orders for 2 new products from a big FMCG company in Q2

Have received new business from a marquee customer in the Industrial segment in Q2 ( its an automotive customer ). Revenues in the industrial segment grew by 30 pc YoY in Q2

Company expects their injectable pen volumes to double in H2 vs H1 ( pickup in volumes should start wef Dec 24 )

Teriparatide ( Osteoporosis drug ) launch is expected to first happen in EU wef Q4 FY 25 ( aprox ). US launch has been delayed

Liragludite launch should happen in Q2 or Q3 of FY 26

Semaglutide launch in RoW mkts like India, Brazil, Canada with company’s devices is expected to happen in H2 FY 26. Company is expected to expand their Semaglutide injectors capacity to > 25 million devices by H1 FY 27. Company believes, it should end up having a dominant mkt share in the generic Semaglutide devices in the RoW mkts

To sum up - Between Jan 25 - Mar 26 - company will launch Teriparatide, Liraglutide and Semaglitide in multiple geographies with multiple customers

Company’s capacity on Insulin pens is around 11 million pens. Looking to expand capacity to 25 million pens. This new - added capacity should come on stream in Q1 FY 27

On Tirzepatide - supply of exhibit batches should start in Q4 FY 25. Did not give any visibility on commercial launch

Current capacity of insulin Injectors @ 11 million. Company is adding another 24 million. So the total insulin capacity will reach 35 million. Semaglutide capacity should be another 35 million. All others put together should be another 25 - 30 million. So the total capacity should reach 100 million in next 36 months

Overall spend for all this capacity build up should be around 150-200 cr over next 36 months

Disc: holding, biased, not SEBI registered, not a buy / sell recommendation

15 Likes

Do we have an idea of what the price could be per pen?

I remember one post mentioning Rs 60 for the Insulin Pen. Does pricing vary for the GLP1 pens, or will it be similar?

I’m just trying to calculate peak sales.

1 Like

For GLP -1 pens, it should be around Rs 200 / pen

For Insulin pens, I think it would be around Rs 50-60 / pen

5 Likes

What is the source for this pricing of the glp-1 pen?

1 Like

To be frank, I was unable to find the same. I asked a few analysts ( over Wassup ) who were present on the company’s concall. They gave me this figure of Rs 200 / pen

3 Likes

Plant visit notes from Investsec

5 Likes

Found interesting article mentioning that GLP-1 can possibly be a serendipity drug for fighting alcohol/ opioid addiction but needs Phase 3 trial to conclude it on larger test data.

Snippet of an interesting para from the article is below:

Small clinical trials and larger studies of patients prescribed GLP-1s for other symptoms have shown promising results when it comes to addiction treatment. A 48-patient Phase II study on non-treatment-seeking people with alcohol-use disorder demonstrated a significant reduction in drinking. A report this year from Morgan Stanley concluded that more than half of people on GLP-1s reduced their alcohol intake, with about 16% quitting entirely. A paper published in the medical journal JAMA Network Open found that people taking Ozempic for diabetes were less likely to suffer from opiate overdoses, while another large retrospective study reported a 40% decrease in opioid overdoses and 50% fall in alcohol intoxication for GLP-1 patients.

17 Likes

Came across this great write up on GLP 1 by Xponent. Covers the supply side in detail. Would recommend. Has said the following about Shaily.

Shaily Engineering stands out as India’s only major listed player in GLP-1 device

manufacturing. The company is pivoting from a crowded, low-ROCE moulding business

to a high-entry-barrier medical devices model. Shaily made history as the first to

develop plastic insulin pens and is now tapping into the GLP-1 generics opportunity

with its own IP platforms. According to the management, 70% of generic Semaglutide filers rely on Shaily’s device, as it is the only one globally that closely matches the

innovator’s reference device without infringing on patents.

We estimate margins in Shaily’s IP-driven pens could be more than twice its current

company level margins, transforming both ROCE and overall economics. However,

long-term success hinges on its customers securing approvals and on Shaily’s ability to

shift from high-volume manufacturing to a high-quality medical device business. The

company’s recent decision to expand capacity from 40 million to 100 million devices—

covering both diabetes and weight-loss treatments—reflects its optimism in this

evolving market.

https://drive.google.com/file/d/1Y95O-YayCF47C9frdtercKF4AZlHLR1l/view

26 Likes

Source WSJ

In case Oral version comes, will it not be a serious threat to Shaily ? Interesting days ahead

1 Like

Oral version is already there. Novo Nordisk has it by brand name of Rybelsus. Both have different price points, schedules and apparently some difference in efficacy.

1 Like

Oral Semaglutide is infact a risk.

Even though, Rybelsus in not a significant proportion of Novo’s sales it is growing very fast. Rybelsus is only approved for Diabetes as of now and is available only in small dosages. Currently it is a daily medication against ozempic being a weekly medication. However, most of this growth has happened in International operations, so cant say whether this growth has come from limited availability of ozempic. Cant find any data to say that rybelsus is less efficient than Ozempic. Also, Eli lilly’s drugs even if approved will be patent protected for a very long time and I dont think they will have enough capacity to cater to the demand o/s US

Source: Novo’s 3rd quarter presentation

6 Likes

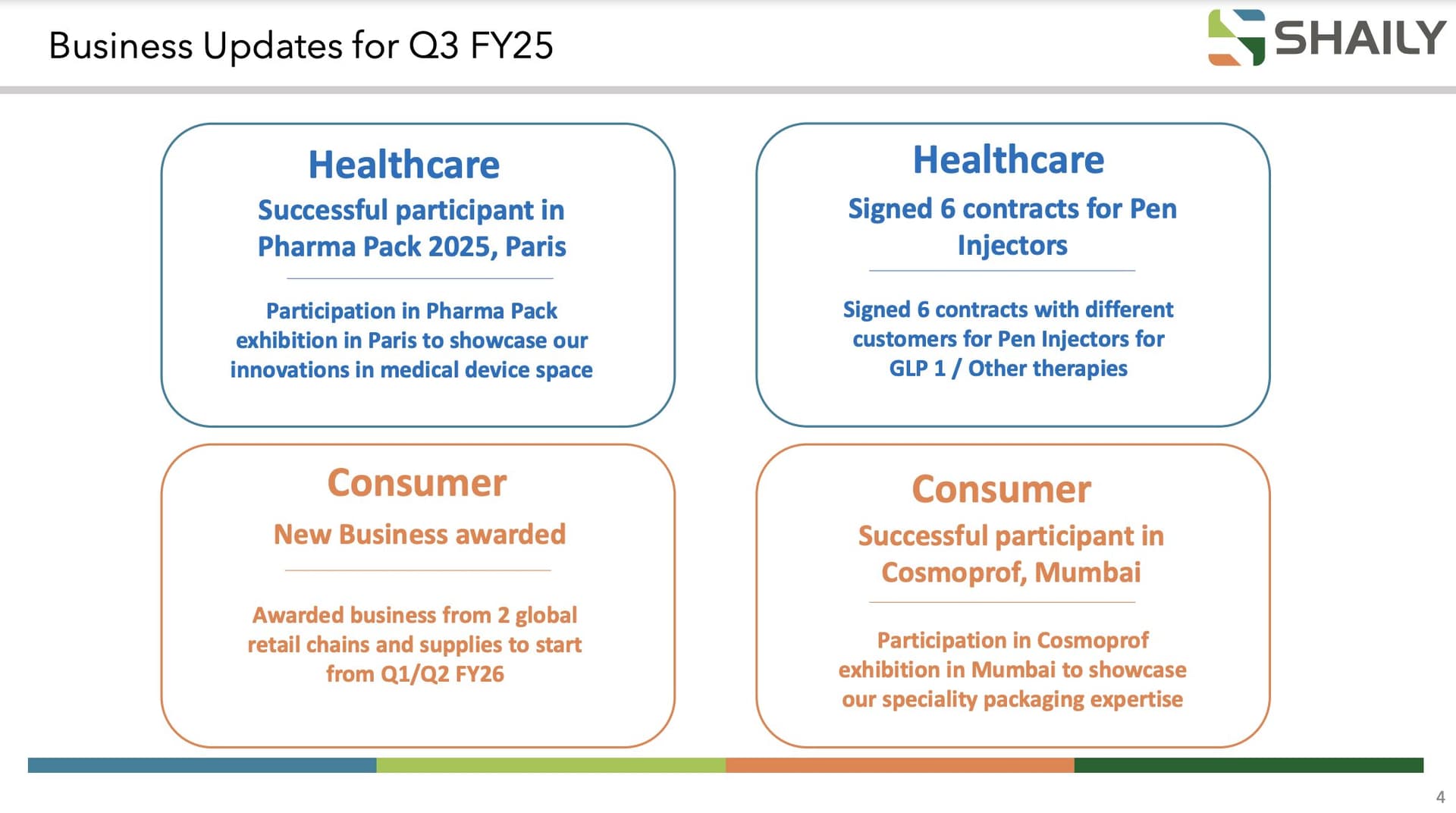

Shaily Engineering: Signed 6 contracts with different customers for Pen Injectors for GLP 1 / Other therapies

7 Likes

Shaily concall ( my notes )

Topline growth 25% 197 cr

Pat margin 23.5 % largely driven by healthcare

9months segment result

Consumer segment 412 cr v/s 364 cr

Pharma 108 cr v/s 69 cr

INDUSTRIAL 47.7 CR V/S 37.7 CR

Medical devise to be 30% of revenue over next 3 years.

6 new contract out of which 3 are gor GLP 1 rest for insuline and migrane

Consumer segment 2 retail chain secured order can eventually scale with them ( my view )

Building 80 parts / min line for sema another line should come up in 12 -18 months.

One 80 ppm line will be ready by sept this year

Capex guideline will be given by next call

Now to december 2026 they are planning to add 60-80 million capacity. Working with some novel potential innovator ( hint given ) which can contribute to buiz .

Q2 calender to Q2 Financial around that time Lira Sema volume would start building up.

Some one ask cost per pen broad guidance range - 2$ - 7.5 $ .

Insulin additional capacity will come.onstream next quarter.

Earlier 10 mln order received less than half will be delivered this year larger part next year.

Gross margin question asked can it be 60-80% ( mgmt you can eatimate ) - personal view sounded positive on margin .

Risk -Question Approval risk of product from top 1/2 customer -

too early for that ( management ) -

Capacity at a glance and capex

Current - 35 -40 million

Addition 50-60 million

Out of 35 mln 6 million Auto injector and out of new capacity 20-25 million would be auto injector capacity.

Sole supplier to most of their customer .

Disc - Invested positively biased . Not a advise

9 Likes

World Class Weight-Loss Drugs Enter India

The Business Standard reported that global pharmaceutical giants are preparing to introduce new weight-loss medications in India to combat the nation’s rising obesity rates. These drugs, known as GLP-1 receptor agonists, help regulate blood sugar and appetite, promoting weight loss. Eli Lilly plans to launch its drug in India by 2025, pending regulatory approvals. Novo Nordisk aims to introduce its drug by 2026, though efforts are underway to expedite this to 2025 to align with Eli Lilly’s timeline.

Distribution strategies include partnerships with local firms to navigate India’s complex market. However, pricing remains a significant concern. Due to patent protections, these innovative drugs are expected to be priced at a premium, posing challenges in India’s price-sensitive market. High costs may limit widespread adoption, especially since long-term use is often necessary for sustained weight loss.

The Indian government is considering incentives to promote local manufacturing of these drugs post-patent expiry, which could reduce costs and improve accessibility.

6 Likes

can you pls share the source of this news? the link i mean

Hello friends,

I am closely tracking this company and trying to get a sense of the current valuations. Here is the napkin maths for next 3 years:

“9M Dec24 Ending” contains the actual 9M numbers.

FY25 numbers are obtained by scaling the 9M numbers (multiply by 4/3).

For Fy26-28, I used a growth rate mentioned in Growth column.

PAT numbers are 16% of Total Revenue (although they are much lower in current FY, than mentioned here).

Looking at the current market cap (8500 Cr), company already seems to be trading close to 40X the FY28 numbers. Even in the current market conditions, this company seems to be going up in last few months. It seems to me that I am underestimating something in my calculations.

Can folks who are tracking this business, pls shed some light on this? How are your numbers different from mine?

| 9M Dec24 Ending | FY25 | FY26 | FY27 | FY28 | ||

|---|---|---|---|---|---|---|

| Division | Growth | |||||

| Consumer | 15% | 412.00 | 549.30 | 631.70 | 726.45 | 835.42 |

| Medical | 30% | 108.00 | 216.00 | 280.80 | 365.04 | 474.55 |

| Industrial | 10% | 47.00 | 94.00 | 103.40 | 113.74 | 125.11 |

| Total Rev | 567.00 | 859.30 | 1,015.90 | 1,205.23 | 1,435.08 | |

| PAT | 16% | 90.72 | 137.49 | 162.54 | 192.84 | 229.61 |

Disc: Invested

1 Like

Your medical segment estimates are very low. You should read the recent concall. There they have mentioned approx selling price of the pen. And in the previous calls, you will get an idea of estimated capacity and capacity utilisation for coming years!

2 Likes