All the results are out, the businesses as well as the elections. I haven’t been writing here much since I haven’t been doing anything. In a year like this activity is a sure fire way to get your capital cut to size in whipsaws.

Sharda Motors - Posted great results for the quarter as well as the whole year. Continues to remain cheap, as the price performance is purely being driven as of now through business performance. The BS-VI RDE norms have driven both value and volume going by gross profits as its been in the last two quarters as well.

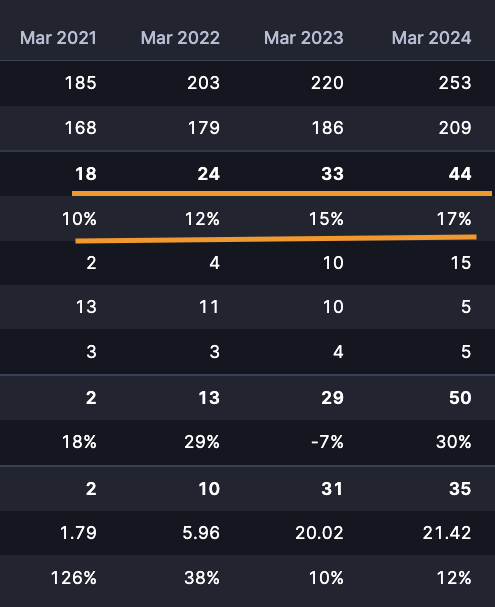

There’s 45% PAT growth annually too and excellent cash flows. Capital allocation as well is quite good with 220 Cr buyback considering the undervaluation and decent dividend of Rs.28/share (almost 2% div yield). There’s an investment in the suspensions segment of 50 Cr towards growth with still about 500 Cr still left after all this for acquisitions and the company continues to generate cash at a healthy pace. How long can this remain as cheap as it is? One of the earliest to show strength in the pf so maybe with story-driven market coming to a close, maybe fundamental driven stories will do well. Lets see

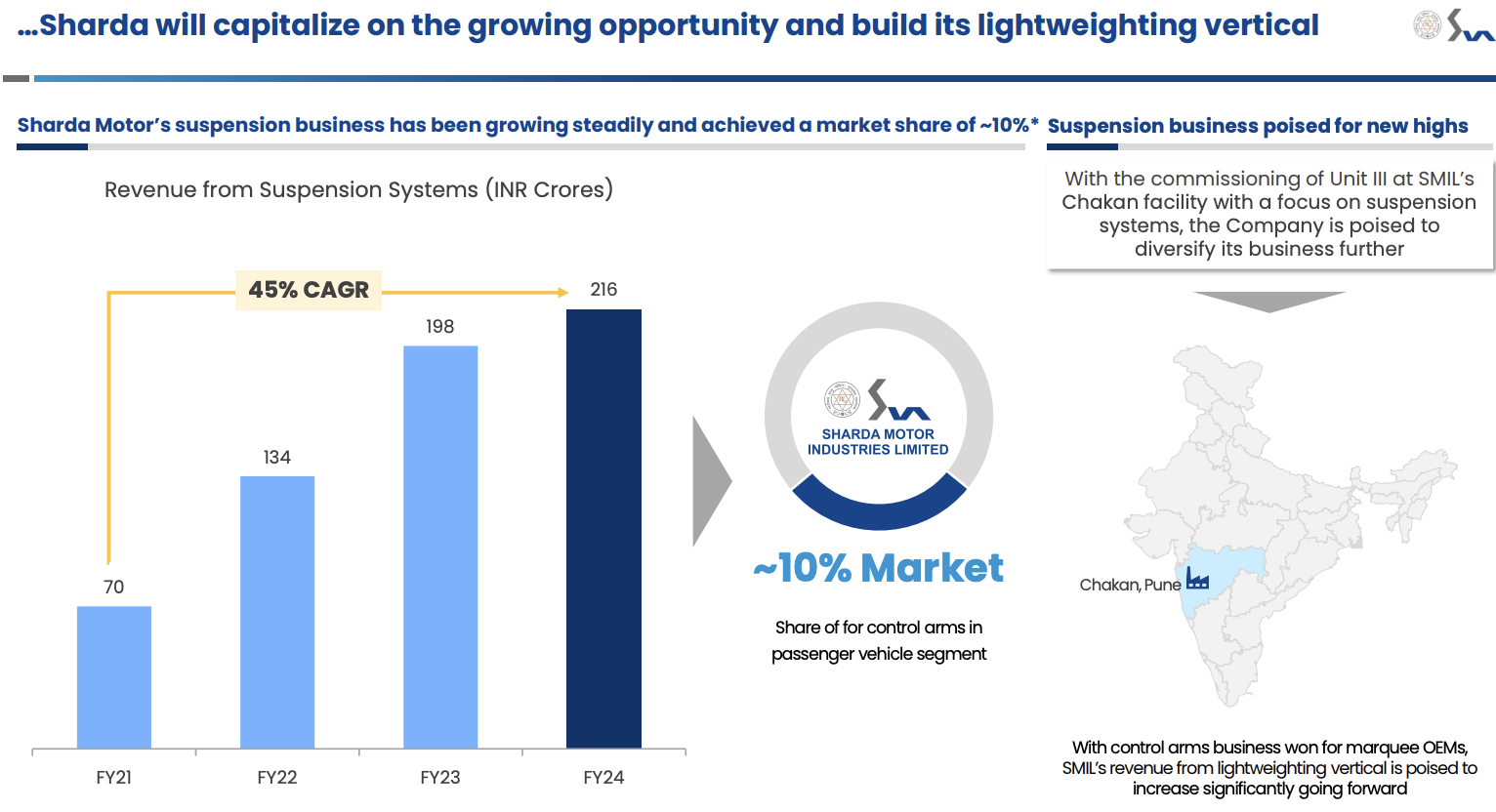

Few things which I found interesting - the suspensions vertical is already contributing 8% to topline and has been growing quite robustly. The reduction in growth likely due to capacity constraint, the 50 Cr investment planned should help resume growth in this platform-agnostic vertical.

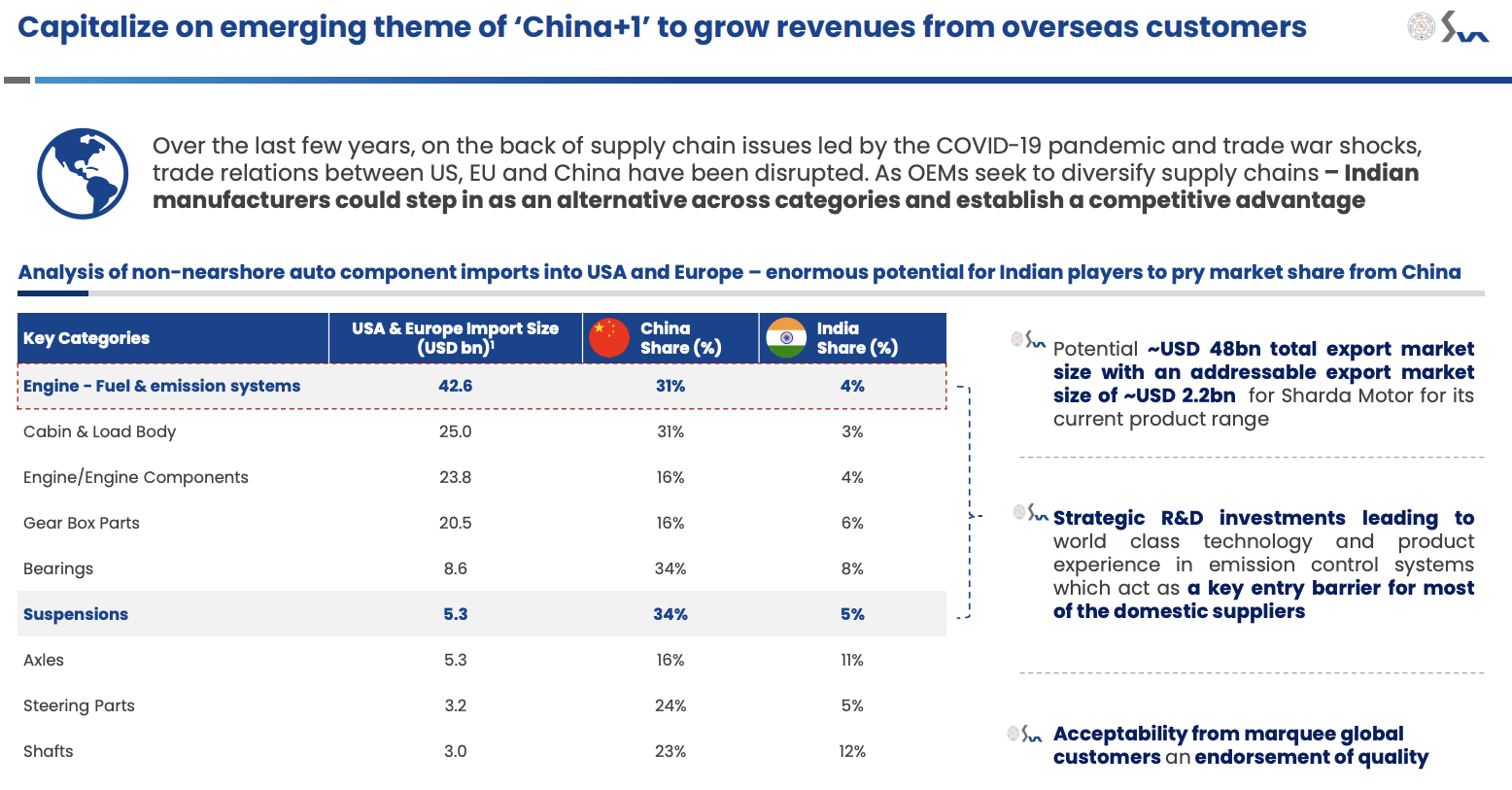

The company seems to be focusing on exports and this slide shows the TAM. With developed nations cutting down on investments in ICE components, there’s good scope for SMIL to get some growth going in exports.

They have made a new CEO hire today as well (Deepak Manchanda with good exp. at Minda, Motherson, Banco etc.) for the global business. There’s definitely a vision for growth in exports as well as looking out for acquisitions in non-ICE segments which if they pull off, should certainly re-rate the stock.

Wockhardt - There’s nothing much new in the results other than some write-offs. 390+ patients signed up for phase-3 trials of WCK-5222. The trial should end in Q4 of FY25 hopefully. The meropenem resistance trials should end by Nov as per the update.

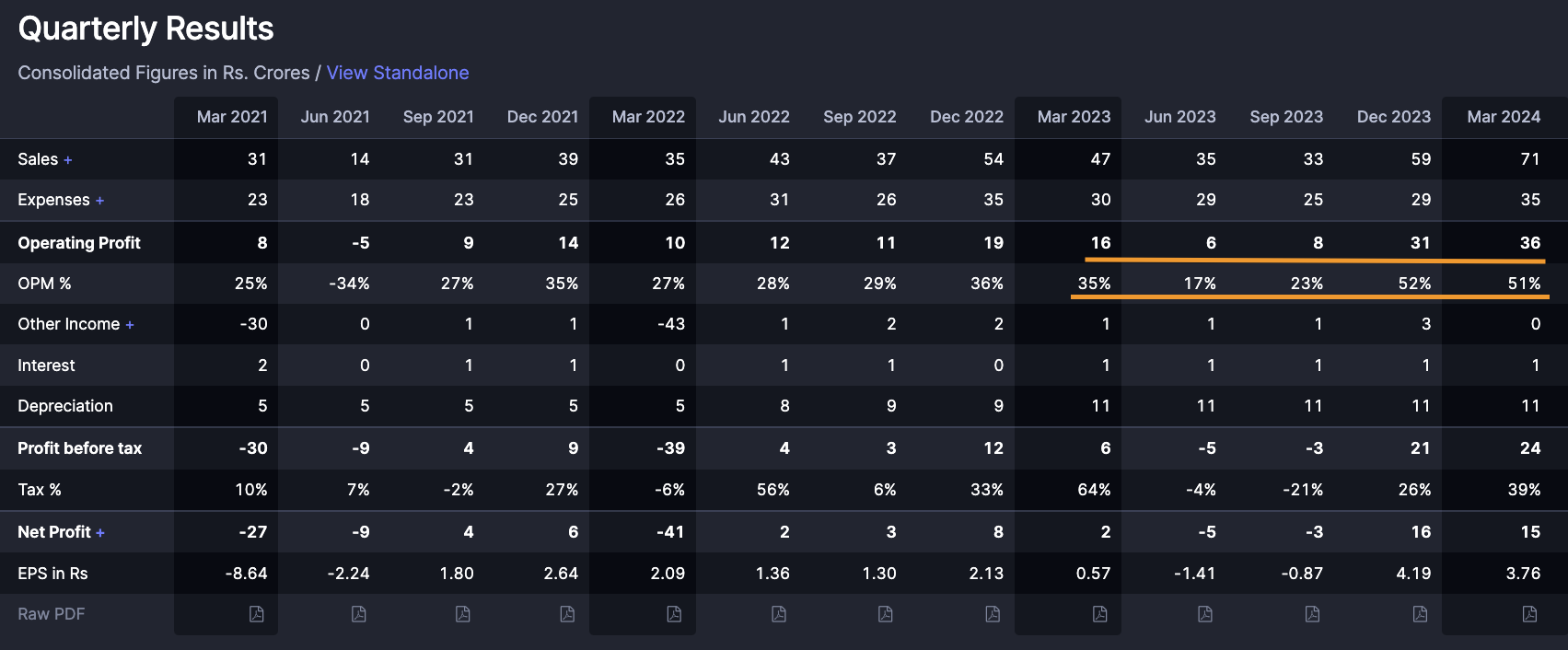

Shaily - Growth continues here in the healthcare division and also the Ikea business. The operating leverage is showing up in the higher margins. I think there’s a lot more to go here. I have captured my thoughts on the healthcare business in the Shaily thread. Though the presentation was sparse this time and no details on the platforms/molecules as promised, the concall was very informative and sheds a lot of light (crux of it captured in my post linked)

Ceinsys - The results were bad on the margin front. The topline had grown but didn’t translate to profits. The company has mentioned in the past that results aren’t comparable across quarters and should be seen over entire year due to varied nature of projects and execution timelines. There are however lot of positives

There’s healthy growth for full year for last 3 years, along with expansion in margins.

There company has a healthy cash conversion as well and it shows up in good reduction in debt and increase in cash and investments. The order book is healthy as well at 650 Cr.

The CEO they hired 2 years back now owns 9% of the company (4.5% options converted and fresh 4.5% given). They have hired ex-GoAir CEO Kaushik Khona as well to manage India business. The EGM conducted recently mentions an acquisition abroad for which they are raising cash to the tune of 240 Cr. If they are raising the cash as planned at 560/share, and promoter is participating, current levels at 400 are perhaps quite cheap.

Genesys - The numbers have started coming here in last two quarters. If what the management envisions plays out, these could be very early days. If current run rate sustains, we could have 70 Cr PAT which means its trading at around 25x 1 year fwd

Both Ceinsys and Genesys had political risk which played out and has beaten the price down. It also matters non-trivially that both were social media favorities which brings in a lot of short-term players that don’t care much about valuations and were buying them at 650 and 700 and levels. While those were expensive prices, i feel current levels are cheap. I don’t see why there shouldn’t be policy continuity in geospatial sector even with coalition govt. I could be wrong (I don’t understand politics much)

Garware - The numbers here were quite good like it was in Q3. There’s expansion in capacities as well which could mean that they might achieve the 2500 Cr topline guidance in the future. I sold my holdings here though after last quarter runup since the exports data appeared weak but the numbers reported are contrary to that. Maybe there’s a lag here and it might show in Q1? I am not sure and would like to wait and watch.

Smaller positions

Eimco - I continue to hold Eimco which has been performing well and lot of the earnings here is in the future as I shared in the thesis in this thread.

Tarachand - Private capex is picking up and don’t see it being affected meaningfully by the coalition govt. This was purchased at 200-220 levels on a whim without a thesis based just on charts. Not sure if current levels are cheap enough.

AVG - I have misread this completely and should have paid attention to the notes to accounts in past years when they moved from SME to main board. The growth isn’t as stellar as it seems and it isn’t poor either. The management somehow doesn’t inspire confidence as main board requires at least an ability to prepare and present PnL statements well (They included other income in EBITDA for eg. in the presentation). I have exited this position with ~10% loss

Disc: Not qualified to advise. These are thoughts on my portfolio and my decision-making for clarity to myself. No recent transactions other than selling AVG and buying more Genesys at 420-430 levels and Ceinsys around 400 levels (both small incremental purchases - Ceinsys avged up and Genesys avged down)