Shaily Engineering Plastic

(Scrip Code – 501423).

CMP: 346 Rs. – Face Value: 10

Shaily providing end to end solutions in plastic products and services

Company Over View

Shaily Engineering Plastics Limited (SEPL) is involved in the manufacture of high precision injection moulded plastic components, assemblies, moulds and dies for OEM (Original Equipment Manufacturer) requirements.

Established in 1987 at Halol, India with 2 molding machines Today – 5 Facilities with 87 Injection Molding Machines (35TON to 800TON) .Market Segments Home Furnishings, Appliances, Medical, Automotive, Consumer Goods, Electrical/Switch gears, and Engineering Applications

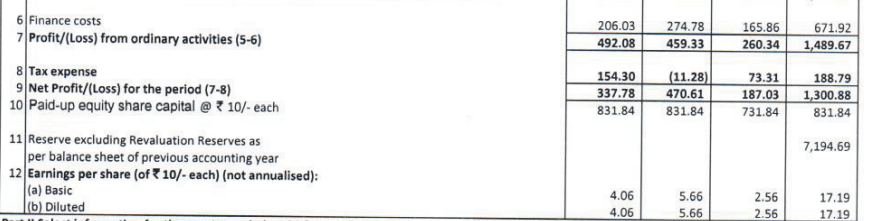

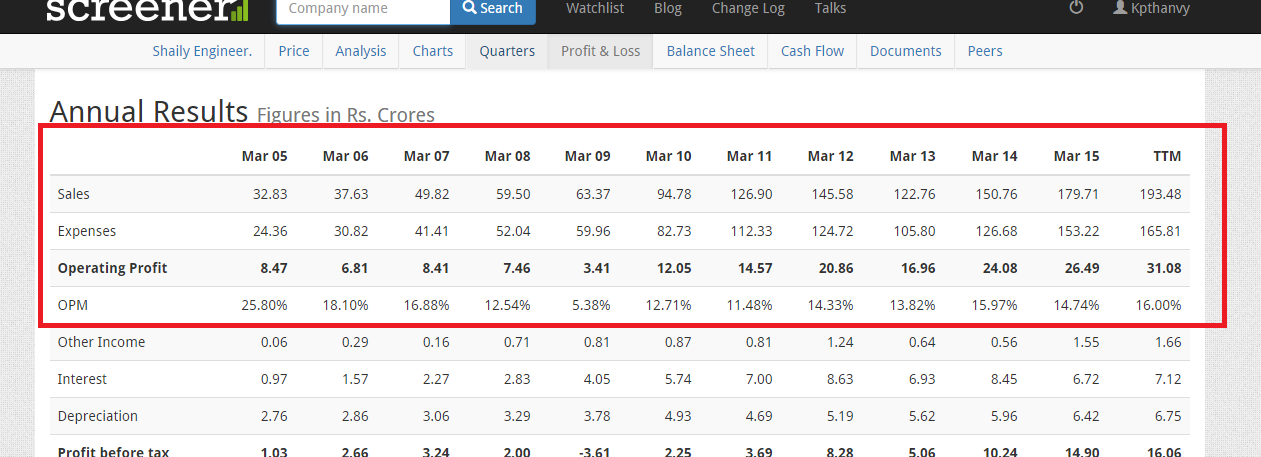

Revenue Growth in last 3 Year

Net profit(in Rs Cr):

2013 – 3.62;

2014- 6.59;

2015-13.01

Client List of Shaily

Consumer: Ikea, Unilever, P&G, MWV-Calmar

Medical : Sanofi, Clearspec , MWV, Sun Pharma, Wockhardt, GE healthcare, Lupin , Dr. Reddys , Zydus Cadila

Appliances: GE, Electrolux, MABE

Switch Gears: Siemens ,Schneider , ABB, L&T, Lucy

Automotive : GE Lighting, Honeywell , Amvian, FAG,Turbo Energy –

Engineering : Emerson, KPT, Phoenix Mecano, IHC , Photoquip

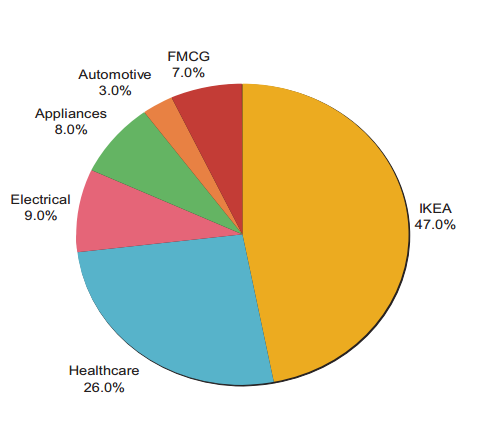

Sales Break up - Segments

Some Interesting Facts Noticed

Promoter holding 54.09% -

Corporate & other biggies – 41.03% (Hardly 5% shares with retailers).

Total Number of the share holders 435 as on 31 March 2015 Report (It was 241 on 31 Dec 2014) Recently started to release some shares to public

Ace Investor Ashish Kacholia Accuired 12% stake in the Company through Preferential Share method

As per Dec 2014 details Company revoked pledge shares and no shares are pledged now

Topline and Bottom Line are growing Continuously.

Outlook on Opportunities

SEPL’s domestic as well as overseas business is developing very fast and getting more and more enquiry for capability to manufacture parts for the clients due to its commitment of standard quality of goods to its present customers and therefore sustaining operations and growing in even tough time. If Shaily can Scale up the operation as per the expectation tremendous scope is there.

Outlook on Threats, Risk and Concerns

The Company’s business depends on customer requirements as the Company is an OEM supplier and any fluctuation in the customers demand can affect the Company’s performance. The Company is also exposed to project risks due to delays in project implementation/cost escalation, risks on account of fluctuation and in FX rates and fluctuation in raw material prices on account of fluctuation in oil prices.

http://www.shaily.com/userfiles/file/Company%20Corporate%20Presentation.pdf

Disc: Invested