Reproducing my blog post below

Business Model

SG Finserve is a lender. They give working capital finance to MSMEs and earn interest in return.

Founder and Management

This is the biggest selling point of the company for now. It is backed by APL Apollo group. The two promoters are sons of Mr.Sanjay Gupta (who is the promoter of APL Apollo). However, I do not think that the two sons understand the lending business very well. They do not have enough experience in the industry. Also, I am not sure how involved they are in the day to day running of the business. One of the sons was not even present for the AGM. Instead the promoters have hired people with around 15 years of experience in the lending business to run the company. Both the CEO and the CFO come from Aditya Birla Finance and have worked extensively on giving out loans which meet the cash flow requirement of the business. Other people in the team including the Head of Underwriting also come from lending background. It seems that the promoters are completely trusting this team of professionals to run the business. To still keep a tight leash on the running of the business, the promoters have ensured that technology is being used from day one in giving out loans and then in managing the repayment of the loans. Also, the Chief HR person was earlier working with APL Apollo itself and therefore is the loyal trusted hand keeping a tab on what is going on.

Product

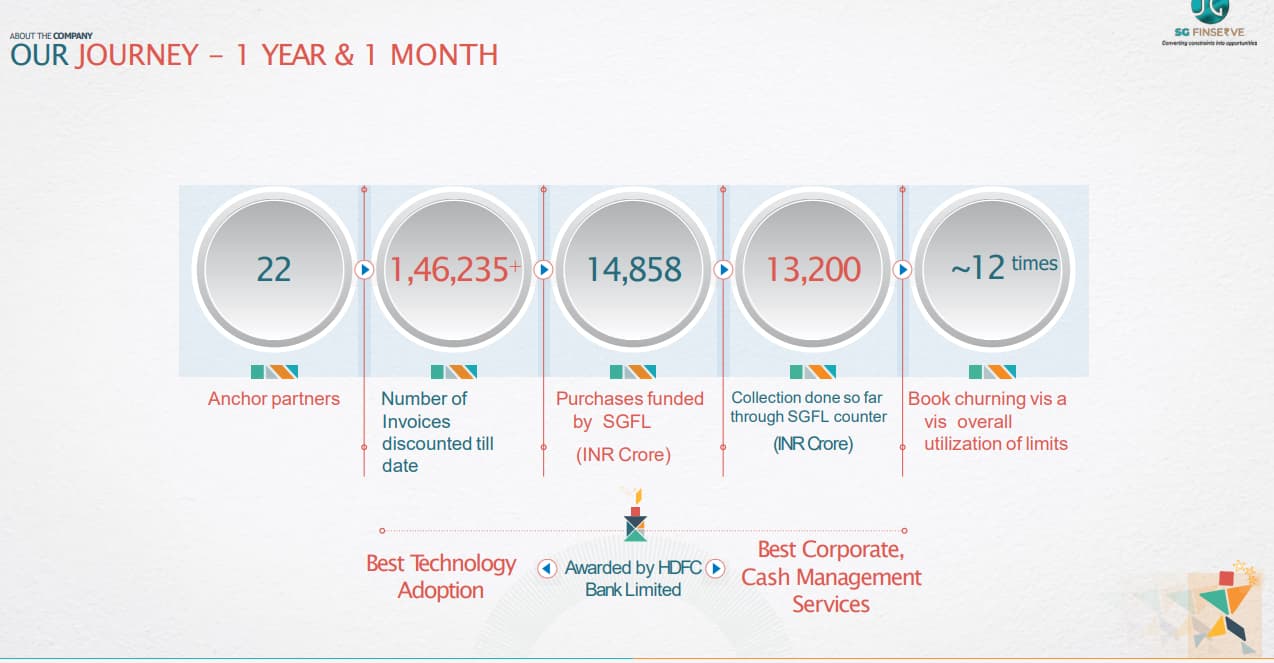

They give our working capital loans to small businesses which either supply to a big company or which help distribute the products of a big company (or an anchor company). They do not ask for a collateral. Instead they have a charge on the inventory that is purchased using their loan. For example if a distributor wants to buy steel worth 1 crore from APL Apollo Tubes, and then pass on this inventory to retailers. Now the retailers would pay the distributor in some time. On the other hand before picking the inventory from the APL Apollo factory, the distributor has to make the payment to APL Apollo. And therefore the distributor needs a working capital loan to make this transaction happen. This is what SG Finserve enables. They also have some sort of arrangement with the anchor company. Under this arrangement if the distributor does not pay back the loan to SG Finserve, then SG Finserve can ask the anchor company to stop supplying further inventory to the distributor. And therefore the distributor would be completely cut off from generating any future revenue. Therefore it makes it very difficult for a borrower to become delinquent. Till date in the roughly 18 months of operations we have not seen any NPA in the business.

Distribution

Basically SG Finserve uses the anchor companies to spread the word about its services to potential borrowers. So SG Finserve first gets into an agreement with an anchor company. The anchor company then informs its whole ecosystem about how quick collateral free loans can be taken from SG Finserve. The anchor company has its own selfish interest in doing so. If its distributors get quick financing easily, then the receivables of the anchor company itself should come down. And this can help the anchor company in optimising how much inventory does it need to carry. For example right now the distributor is not sure exactly when will he have access to financing. And therefore the anchor company produces some excess inventory which stays in its warehouse and is liquidated as and when the distributor is able to arrange financing. But with the help of SG Finserve financing is always available for the distributor. Therefore the distributor can plan his buying decision better and the anchor company can therefore plan its production of inventory better.

Brand

This is a B2B operation. It does not require a lot of brand building to grow for now. That is because the MSME market is underserved by banks and big NBFCs. Money is a commodity. All lenders lend the same quality of money. You can’t charge a brand premium. So the rate that you charge the borrower depends on your own cost of funding. And your own cost of funding does not depend on your brand but on your assets and track record. Actually let me say this another way. As the company grows they would need more and more source of capital. At that time they may even have to issue bonds and debentures to HNIs. At that time, we should see the value of the brand play a role. After all buying bonds of Govt of India seems much safer than buying bonds of Bajaj Finance. For now, the company is not doing much brand building. May be they will devote more resources to it later.

Financials

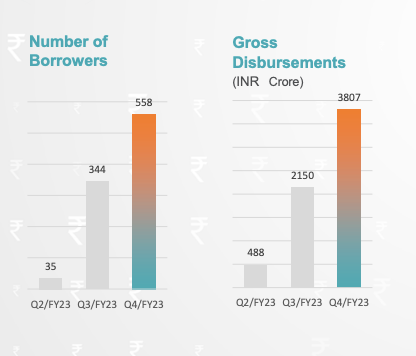

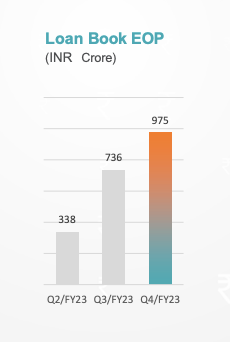

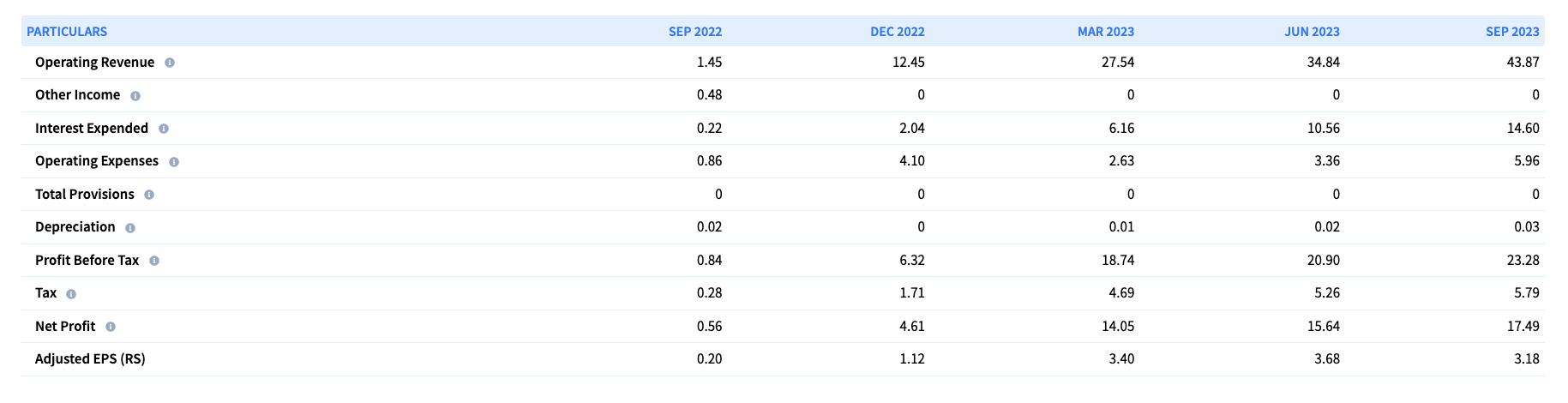

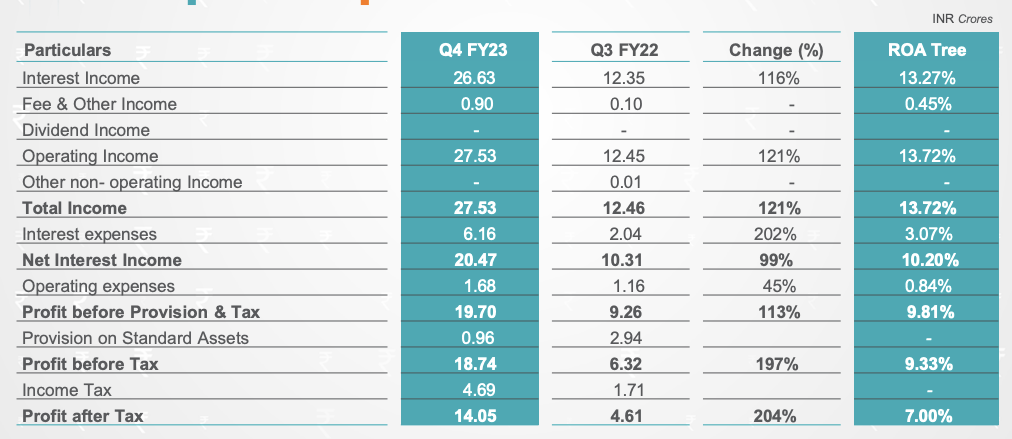

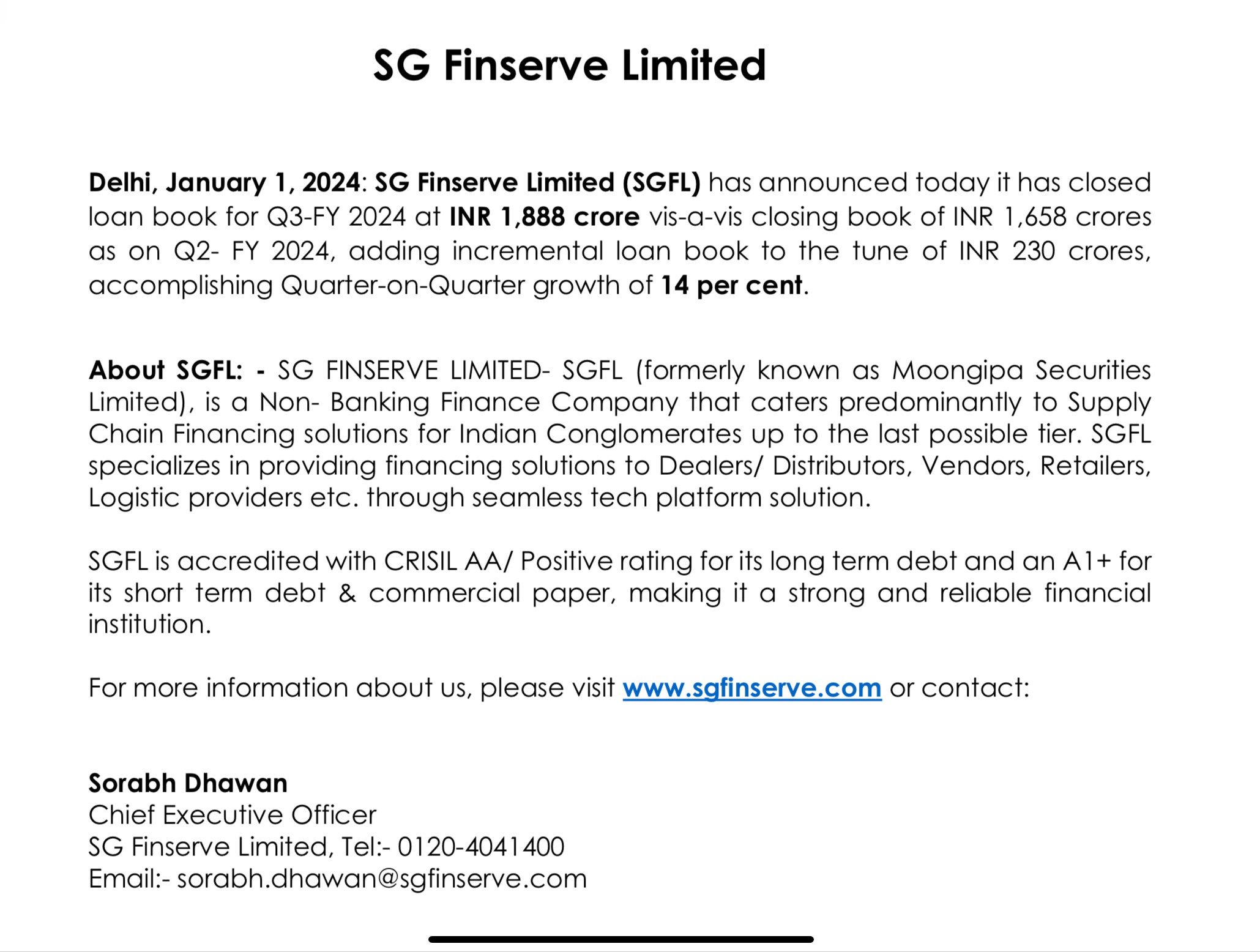

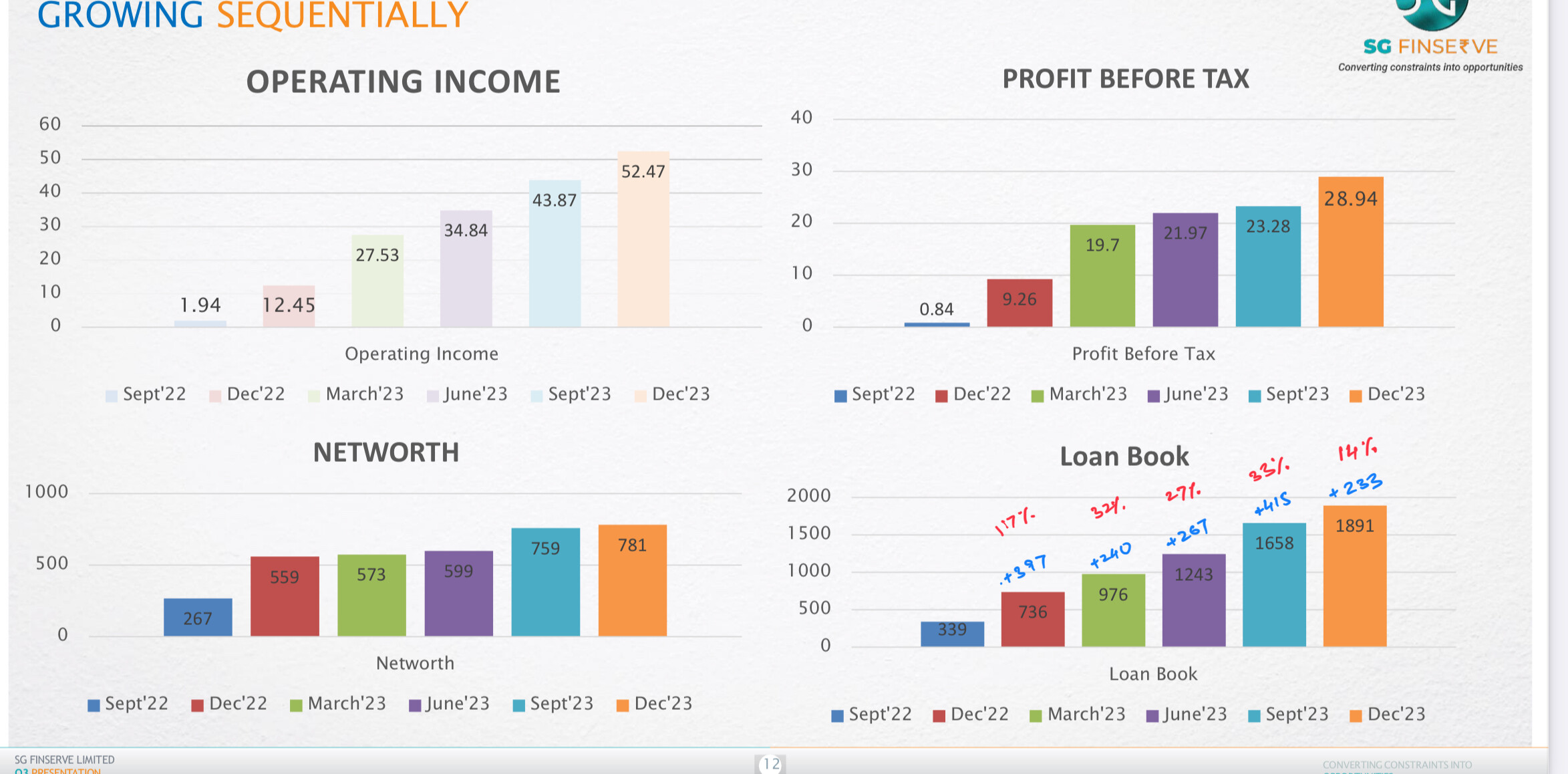

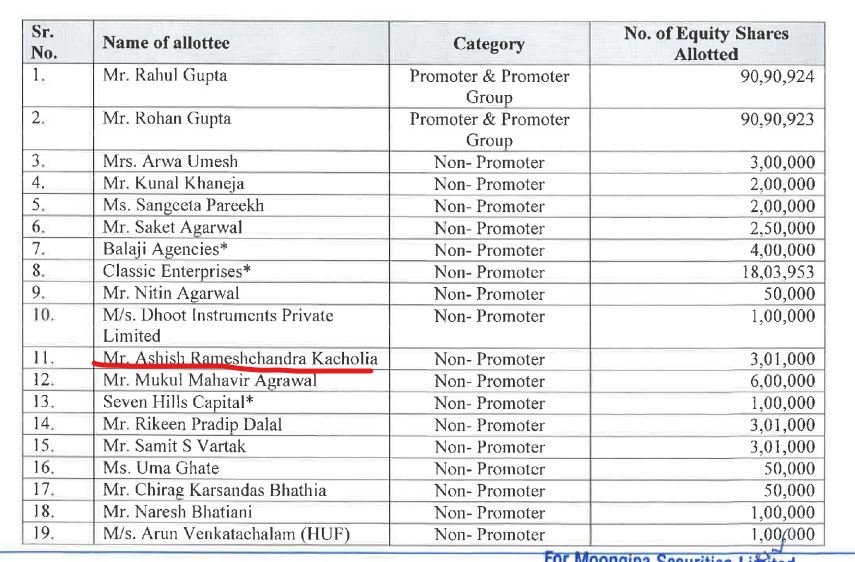

The company has about 780 crores of equity. Most of it has been contributed by the promoters. A small portion is profits earned and redeployed in the past 18 months. There are some notable small investors too who have put in equity into the company. For example Ashish Kacholia, CSL Finance, Gaurav Sud. Right now the size of the book is 2,000 crores which means that the debt to equity ratio is very comfortable. Profitability is high right now because the mix of equity in the capital available is high. As debt to equity ratio goes up unit level profitability should take some hit even though in absolute numbers it should keep going up. The company does not charge usurious rates especially considering that they are doing collateral free lending. Their lending rates vary between 11-15%. The kicker is that they churn 9 times a year. This is because the average loan gets churned every 40 days. Because of this they end up earning (in my opinion) 14% of blended return on their capital. And I am guessing here that they raise money at a blender rate of about 9% and therefore they should make about a 5% spread on their lending. I think a good MSME should be able to raise at 12% from banks directly, but the problem is that banks move slowly and also ask for collateral. Therefore it may be more profitable for the MSME to borrow from SG Finserve.

The company has good operating profitability today and will have tremendous operating leverage since they are using tech from day one to keep their operating expenses limited. I don’t think they have brick and mortar expensive offices in each city that they operate in.

Bull case

The company will keep growing at a breakneck speed without any NPAs or with extremely low NPAs as the anchor companies will wield the stick against any defaulters. The promoters would be smart enough to only raise equity money when the price to book is completely in their favour (may be when it is 6 or more). The management has ESOPs. So their interests are aligned with a long term increase in the share price of the stock. The management would ensure that they continue to capture more market share in the collateral free lending available for MSMEs. Also, as more and more manufacturing starts to happen in India, we will see more and more anchor companies wanting similar services. So there is a tailwind that the company gets without doing much to create it.

Hopefully, the young promoters would keep learning the ropes of the business and partner with the professional management in a respectful way instead of throwing their weight around. Later the company may discover some other adjacencies. For example lending to the consumer also. Also, the company may do deeper in the ecosystem of the anchor company. For example lending to the supplier of the supplier to the anchor company. Or Indian manufacturers may establish overseas operations and then SG Finserve may get a chance to expand with them.

Also, the company may be able to reduce its cost of financing drastically if it is able to raise private debt from rich HNIs. All this will lead to huge margin expansion as the interest rate of lending is unlikely to go down drastically.

Bear case

The promoters fire the management and start to manage the company on their own. This is just speculation. I have seen no interest from the promoters to indicate this for now. Or the competition suddenly goes up. If the rupee becomes fully convertible in the future then foreign investors would rush in. This would suddenly drastically increase the quantity of money available. And this would mean that lenders will mushroom. And the biggest untapped potential source of lending is to MSMEs. Others might try to copy the same model. Think about someone like a HUL trying to do the same model by forming a separate NBFC.

One more bear case scenario is lenders getting extremely good at cash flow based lending. You then dont need an anchor to give comfort to a lender. One company which is trying to do something like this at scale is Paytm. Although the jury is out whether they can keep the NPAs under control while trying to do it. If a borrower does not need to put up collateral and does not need someone else to stand as guarantor, then he would like to borrow based on his cash flow provided the lender can underwrite on the same.

Corporate governance is also a perennial worry when it comes to lenders. There are inter corporate loans being given out today from this entity. This can baloon. So we will have to keep monitoring the company and its risk management going ahead.

P.S. My internal blogs/drafts for this post are below.

Disclaimer: The views expressed in this blog are personal. I may or may not hold investments in the stocks mentioned.

Friday, 5 April 2024 at 8:54:33 AM

So I started studying SG Finserve because I got to know from valuepickr that this is a company with parentage from APL Apollo Tubes. A few years back I had purchased APL shares and then sold out at a neat profit. The purchase was on the advice of a registered SEBI adviser. He mentioned in his note how the promoter is using the best-in-class technology and trying to open up new niches in the steel business. This was late 2019. The steel tubes business has continued to do well since then. And therefore I was intrigued that why is the same promoter now trying to do something in the lending space. And more importantly what exactly is he trying to do.

Actually I read about a company called Veefin Solutions a few months back. They are into deep-tier supply chain financing. They build the software to enable it. SG Finserve (SGF) also is into deep-tier supply chain financing. But they are a lender which is building a book on its own. But let’s take a step back and first try and understand what is the fundamental human need for borrowing.

The short and cynical answer can be that greed drives us to borrow. The quickest way to get rich is by borrowing and then using that money to generate more money. For example assume you borrow 1,000 rupees at 10% annual rate of interest and then keep that money with yourself for one year. Now at the end of 1 year, you would have paid an interest of 100 rupees on this borrowing. But what if you are able to use this 1,000 rupees during that one year to generate a profit of 200 rupees. This means that at the end of the year you have 100 rupees extra. Your lender would be happy because you have paid him 100 rupees on the money borrowed. And you would be happy as the borrower because you have kept 100 rupees for yourself from the profit of 200 that you made. This is the best case scenario that I have laid out. Borrowing can also be a double edged sword. Assume that in the same year we are hit with another pandemic. Now the 1,000 that you borrowed and invested in some business is reduced to 800 rupees at the end of the year. The lender would still want his 100 rupees of interest. So at the end of the year, you would be in a loss of 300 rupees. First you would have to pay the principal of 1,000 rupees back to the lender. On top of that you would also have to pay back the 100 rupees of interest which is due on the borrowing. In the Indian context, when we talk to our elders we are repeatedly told that the downside is what is most likely to happen. No one knows for sure what would happen in the future, but to safeguard you your elders would always ask you to play it safe and just shun debt.

So as an individual or as a business you need to always first deeply understand why are you borrowing. What is the maximum downside you are taking on? Isn’t there an alternative available to debt? After you have done all this analysis you can finally then start to figure out which type of borrowing would you like to do. Once you have decided the amount you want to borrow you would start approaching lenders. But that is when you run into the problem of collateral. Let’s investigate this problem a bit more.

What is collateral? It is basically something which the lender wants to hold on to for risk management. In case you act as an unreliable borrower and don’t pay back in time, the lender would sell your collateral and recover his principal and interest. In older Hindi movies it was maa ke kangan. The lender would seize them when the borrower could not pay back the loan. In our everyday lives also we borrow against a collateral. For example when you take a home loan, your home is not yours truly till the time you pay back the loan amount to the bank. In fact the property documents are physically kept by the bank within its premises till the time all the loan comes back to the bank. This is usually how loans work for individuals. Individual goes to the lender and asks for a loan and promises to buy something with that money and the ownership on paper of that something remains with the bank till the end of the loan.

But with businesses it’s different. Let me illustrate how. Suppose you run a hardware shop. In your shop you sell cement, you sell steel tubes, taps, lights, hammers, nails, extension cords, etc. Whenever someone is getting their home renovated, they come to your shop and buy whatever it is that they want. Now if your customer comes to your shop and asks for cement, the expectation is that the customer would pay you money and you will hand over the cement immediately. Let us assume that instead you told the customer that first you will accept the money from the customer and then you would go to the cement manufacturer and then you would buy the cement and then you would come back to your shop and then you would ask the customer to come back again to pick up the cement. Will this customer ever come back to you? Think of all the time he wasted because the shopkeeper did not have the cement available immediately to hand over. And to add salt to your wound, what if I have a shop right next to you where I also sell the same hardware items and I have the cement available on premises. How hard would it be for me to attract the same customer to my shop instead? All I need to do is just raise my voice and inform the customer that I have the cement physically available with me right now. So let’s pause once. What have we established? We have till now established that businesses want to increase the convenience of their customers. One way of increasing that convenience is quick fulfilment of the order of the customer. And a great way to quickly fulfil the order of the customer is to physically have the inventory asked for by the customer.

So about 150 years back, shopkeepers did not have formal bank accounts. They did not have access to debt. The only debt they could borrow was from the local moneylender and this guy usually charged a very high rate of interest. And the shopkeeper typically did not have great math skills. So he never truly understood the underlying terms and conditions of the loan that he was taking from the moneylender. And this meant that the shopkeeper usually kept very limited inventory. For example he may only have one brand of bricks.

But then something changed in 1974. The US dropped the gold standard. Post world war 2, the world had decided that in order to avoid hyper inflation (as was seen in Germany post world war 1), the best way to control money supply by the government was to make sure that you only print as much money as the quantity of physical gold that you have. And many countries including the US followed this. But then something changed in 1974. The US said that from now on we will print as much money as we want and we will not adhere to this arbitrary rule of restricting the supply of money to the physical quantity of gold that you have. Now when this happened, this opened a new door for businesses in the world. I am talking about businesses which manufacture stuff. Let’s investigate this further.

Suppose you are a new cement manufacturer. You go to a shopkeeper and then ask the shopkeeper to add your brand of cement to their inventory. The shopkeeper says he does not have idle cash lying around to buy your new cement brand. So now as a manufacturer you are stuck. Customers will not buy your cement till the time they see that your cement is available with the local hardware shopkeeper. You somehow manage to convince the shopkeeper to borrow from the bank and then use the borrowed cash to buy your new cement brand. The shopkeeper goes to the bank and the bank tells the shopkeeper that they don’t have any depositor cash left over to lend. And the bank assures the shopkeeper that they will go to the central bank of the country and ask for some cash which the bank can then lend to the shopkeeper. So let’s look at this chain again. The new cement manufacturer asks the shopkeeper for cash who then asks the bank for cash and the bank itself then asks the central bank for cash. At this time we are stuck. The central bank says that it does not have enough gold reserves to print some money which can then be handed over to the bank. And this communication is then passed on down the chain and ultimately you are back to the problem of the shopkeeper not having cash to buy your new cement brand. This was how the world was pre 1974. This is a rough approximation. But you get the idea. Money was in short supply simply because it could not be printed at will.

Once the gold standard was abolished the situation changed. The central bank now could print money and then pass it over to the bank and then the bank gave it to the shopkeeper and the shopkeeper gave it to the new cement manufacturer. This made the economy move faster. And this is broadly the world we live in today. But there is one part of it we have not covered. And that is the collateral. Because ultimately money has to be paid back. So the shopkeeper also needs to put up some collateral. Now ideally the shopkeeper would tell the bank that since he was borrowing to purchase inventory, he can only offer cement as collateral. But think of this as a bank manager. If the shopkeeper does not pay back in time, what would you do? Would you physically go to his shop, pick up the cement and then try to sell that cement to someone else to recover your loan? A lot of things can go wrong with this plan. The shopkeeper can sell the cement and shut shop and abscond. Or the prices of cement as a commodity can crash because of which as a bank you will only be able to recover a part of the loan that you gave. Or the brand name of the cement has taken a hit because a building collapsed which was using that cement. In that case your inventory is at a complete loss now. Or the shop can catch fire because of which all the inventory can get destroyed. You get the point. So usually banks demand a type of collateral which they can resell easily. For example maa ke kangan. On a side note. Do you know why does gold hold its value? It is because it does not chemically react with air. For example iron gets rusted. Nothing happens to gold. It will look the same even 2,000 years from now. Anyways coming back to our collateral requirement. The bank needs a collateral which is easy to collect, easy to sell. And therefore the shopkeeper is again stuck. After all how much inventory can he buy by keeping his family jewellery as collateral? So the shopkeeper started pushing back. He told the new cement manufacturer that he needs credit from the cement manufacturer himself. And this starts the story of giving credit to participants in the supply chain.

Basically, the shopkeeper started telling the new cement manufacturer that from now on he will only stock his cement, if the cement is provided to the shopkeeper on credit. And when the shopkeeper will sell the inventory to the customer, the credit will be repaid to the new cement manufacturer. So basically the shopkeeper pushed his problem of borrowing on to the new cement manufacturer. Now our new cement manufacturer faces a new problem. Not only does he have to manage manufacturing of cement, he also needs to take the inventory risk on behalf of the shopkeeper. The manufacturer has to pay his employees on time every month, but he will only be able to collect money from the shopkeeper every 45 days or 60 days or 90 days. So again there is a demand for a loan. This time the loan is being asked for by the manufacturer so that he can pay his staff on time. But again the bank will ask for a collateral. So this time, the manufacturer offers his land and machinery as collateral to the bank. The bank gives a loan against the land. The bank knows that if the manufacturer does not pay on time, then the bank can seize his land and sell that land and recover the money.

And this arrangement started working. Now over a period of time the cement manufacturer kept doing well. His brand grew and grew. Everyone started appreciating how good the quality of his cement was. There were homes and buildings 20 years old which stood really strong due to his cement. Even during earthquakes when other buildings got damaged, the ones made with his cement stood strong. As a result the stock price of his company grew. It reached a market cap of 1 lakh crores. The banks kept lending to the cement manufacturer. But after a point of time, the bank started having other priorities also. The bank got so much demand for home loans that the bank did not feel the need to fund the supply chain of the cement manufacturer as much. So the bank started charging a higher rate of interest to the cement manufacturer for supply chain finance. Or the bank took too much time to disburse the loans. Sometimes the bank took a week for handing out the loans.

So now the cement manufacturer is again stuck. And this time he is a bit irritated. He can’t understand what is he doing wrong. He is making strong cement. He is building more and more manufacturing plants all over the country. He has never defaulted on any of his loans to the bank. Why is the bank still not being sensitive to his need for capital? So the cement manufacturer takes a drastic call. He decides to build his own bank. He asks his sons to buy out a company which already has a banking license. And then they start their own bank.

This is the oversimplified story of SG Finserve. Instead of being a cement company they run a steel tubes company called APL Apollo Tubes. The holding company APL Infrastructure Private Limited (AIPL) holds about 30% stake in APL Apollo Tubes. That stake is valued today at roughly 12,000 crores. AIPL is the guarantor of all the debt that SG Finserve is taking from banks. Banks believe AIPL as the guarantor because AIPL has a stake worth 12,000 crores in APL Apollo Tubes. And then SG Finserve as an NBFC is lending that debt to the dealers, distributors, retailers, suppliers of APL Apollo Tubes.

Actually now let’s investigate the credit requirement of small businesses which act as distributors, retailers, suppliers, transporters of big anchor companies like APL Apollo Tubes. Typically these small businesses don’t have the kind of collateral that banks want. They don’t have a lot of jewellery. They do not have big fixed deposits as all their capital is in the form of working capital and is therefore always stuck in their business as inventory. Ideally they should ask banks for cash flow based lending. They should share their bank statement with the lender and then the lender should offer them credit because the bank statement would show that they are an active business with frequent inflow and outflow of cash. But cash flow based lending is always tricky. After all as a bank how will you recover against a default? Therefore banks or NBFCs are very reluctant to fund such small businesses. Now the anchor business or the main business which is dependent on such small players will always be unable to grow at the pace at which it wants to if these ancillary businesses are not able to peacefully run their own business. Think about the steering wheel in your car. If Maruti wants to manufacture 50 lakh cars every year going ahead, then does it not want its suppliers to be ready to supply 50 lakh steering wheels next year too. And then does the steering wheel supplier not require working capital finance to fund its own requirement of raw materials? Similarly it is in the interest of every anchor business to ensure that its suppliers or dealers always have access to working capital finance which is available quickly and at affordable rates.

So the anchor business sort of uses its own credibility in front of banks and sort of offers to stand as guarantor of any debt being extended directly to the ecosystem around the anchor business. Now the anchor business also needs to do some sort of due diligence of its own. You can’t treat a new distributor just like you would treat a distributor who has worked with you for 20 years. Also, you need to really understand what is the kind of risk you are underwriting. For example let’s say I supply coal to APL Apollo Tubes. Now if I supply 1 tonne of coal on 1st January, then APL Apollo Tubes is supposed to pay me after 45 days i.e. by 15th February. Let’s assume those are the credit terms I have given to APL Apollo Tubes. Now let’s say on 2nd January, the internal QC team at APL Apollo Tubes has given its confirmation that the coal is as per the required standards. As a supplier of coal, I should then be able to take my invoice to a bank and ask the bank to pay me today against that invoice. Let’s say the invoice is for 10 lakh rupees. The bank would ask APL Apollo Tubes if they guarantee that they would pay for the coal by 15th February. In case the confirmation comes in, the bank pays me 9,90,000. As a supplier I receive the money and I can then carry on with my business. The bank would wait for 45 days and then recover the money from APL Apollo and make a profit of 10,000 rupees. APL Apollo is also happy because they were always going to make the payment on 15th February. And the depositor of the bank is also happy because he would receive his savings or FD interest as promised by the bank every month. So this is the kind of cycle that SG Finserve is trying to achieve. Depositor lends money to bank, bank then lends money to coal supplier, coal supplier lends that money to APL Apollo Tubes. On the way back APL Apollo gives the money back to the bank, bank gives the depositor interest on his deposit.

And this works in a similar manner also with the distribution network of APL Apollo Tubes. APL Apollo Tubes gives inventory to its distributor. The distributor borrows from the bank and pays APL Apollo Tubes at this time itself. Now the distributor passes on the inventory to a retailer. The retailer again borrows from the bank and pays to the distributor. So the distributor is now safe as he will use the cash received to pay off the bank. The retailer will then take a few days to sell the inventory to the final consumer. And then the retailer will return the borrowings of the bank. So understand all the players. There is the anchor company. There are its suppliers. And then there is the other side where you have distributors and retailers of the anchor company. Whom amongst these will take on borrowing from the bank? This depends on who needs whom more. If there is a new territory that the distributor is trying to open then for that territory the distributor may offer credit to the retailer. After all the distributor wants the retailer more right now in that new territory. However if it is an established territory, then any new retailer joining in may need the distributor more. In that case the distributor may not give any credit to the retailer and the retailer may borrow from the bank to buy inventory from the distributor. In some of these cases where APL Apollo Tubes has sufficient power and control, it may agree to stand as guarantor in front of the bank. Digital technology will help them figure out without much effort how to avoid defaults. Let us take one example of this.

Suppose there is a distributor for APL Apollo Tubes. Let’s say he has submitted a refundable fee of 50 lakhs with APL Apollo Tubes to get the distributorship rights for a particular territory. Now, let’s say APL gives him inventory worth 30 lakhs. And APL lays down the condition that they will only release the inventory when the distributor gives them 30 lakhs immediately. Please note this is on top of the 50 lakhs that the distributor already has submitted as refundable fee. Now to make life easier for the distributor, APL Apollo Tubes lets him know that he can borrow 30 lakhs at 13% annual rate of interest from SG Finserve for a period of 90 days. After all the distributor will further give a credit of 60 days to retailers. So ideally he should get the money due to him from the retailer within 60 days and then repay SG Finserve. Now if on the 90th day, the distributor does not return the money to SG Finserve then he is defaulting. In this case APL Apollo Tubes may step in and repay the 30 lakhs to SG Finserve on behalf of the distributor along with the interest due. And APL may deduce the same amount from the refundable fee that the distributor had earlier submitted. Also, APL’s ERP will automatically block any further inventory being released to this distributor and he may also be blacklisted. This way all parties get what they deserve. This is the kind of model that SG Finserve is trying to create. And all of these parties can keep up to date in real time using API calls between different software systems. The software that APL Apollo Tubes is using can talk to the software that SG Finserve is using and automatically such kind of checks and balances can be implemented.

Now till now SGF has mostly been doing this for APL Apollo Tubes. But recently they have also started replicating this for other anchor companies like Vedanta and Bombay Shaving Company. I am still trying to figure out how much of the AUM is coming from these other anchor companies. After all you need a lot of trust to make this system work. This kind of trust is easy to establish when the promoters of both the anchor company and the lender are the same. That is the case for SG Finserve and APL Apollo Tubes. But that is not the case for SGF and Bombay Shaving Company for example.

Also, I need to understand how much of their technology stack is being built in-house. Or do they not think that is relevant? May be they can buy off the shelf software which can help them drive this business. Basically they have grown their book very quickly since they started in September 2022. But that was primarily because they were lending to trusted ecosystem partners. After all if APL Apollo Tubes had been working with a distributor for 20 years, then SG Finserve could trust him with working capital lending quite easily. But how will they replicate the same when it comes to another anchor company and its ecosystem?

The promoters have infused about 650 crores of equity in SGF. And their current book is about 1700 crores. This means that the NBFC has about 1100 crores of debt which means a debt to equity ratio of about 1.5. I am researching what would be a comfortable debt to equity ratio for the company. May be 3? After that if you want to continue to grow fast, you would have to dilute equity. So I want to observe how so the founders do that.

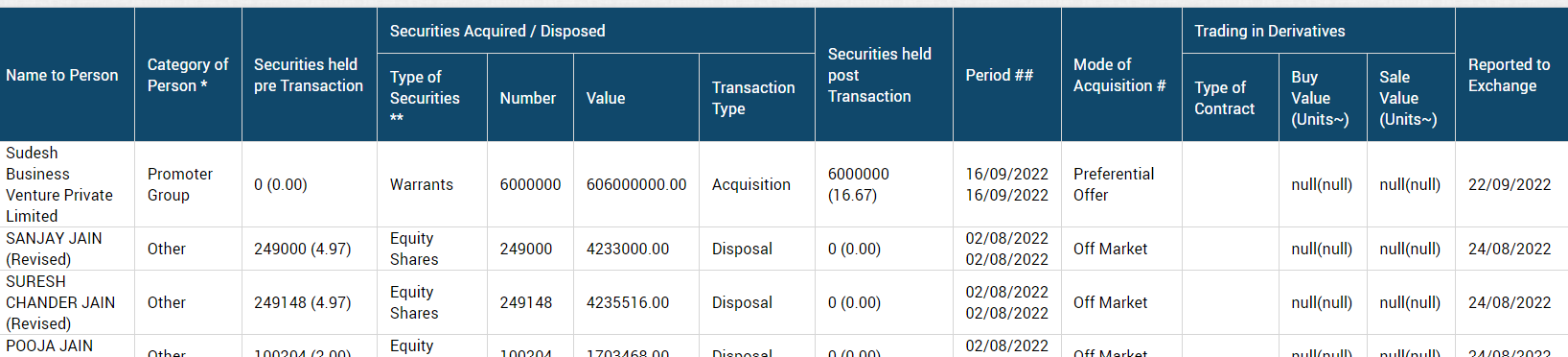

Also, when the promoters first completed the open offer for the company they held about 73% of the company. Right now they hold about 48% of the company. If the company is growing so quickly, why are the founders so quick to dilute? Why not put all the additional equity into the company themselves instead of letting people like Ashish Kacholia also invest in the company?

Let me write back on this thread as I get more answers.