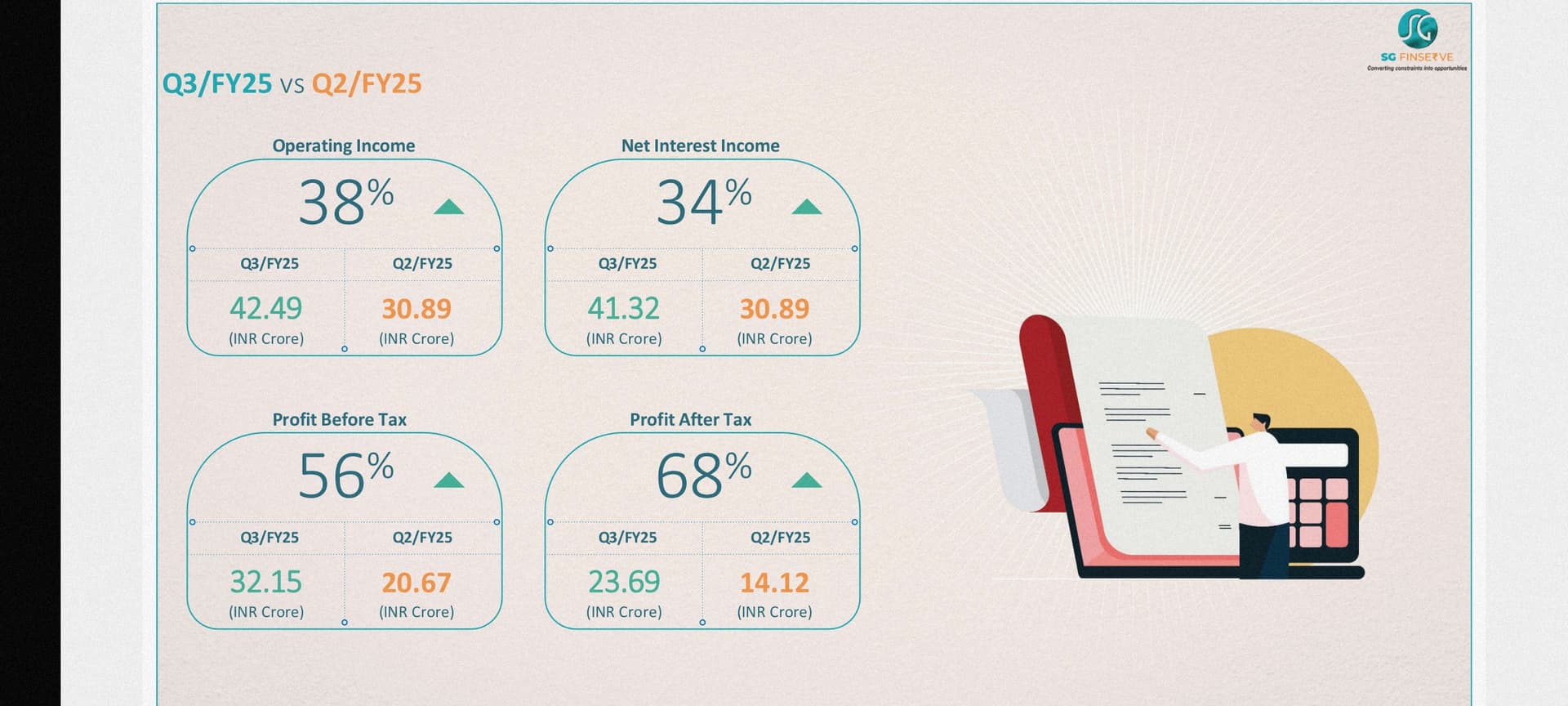

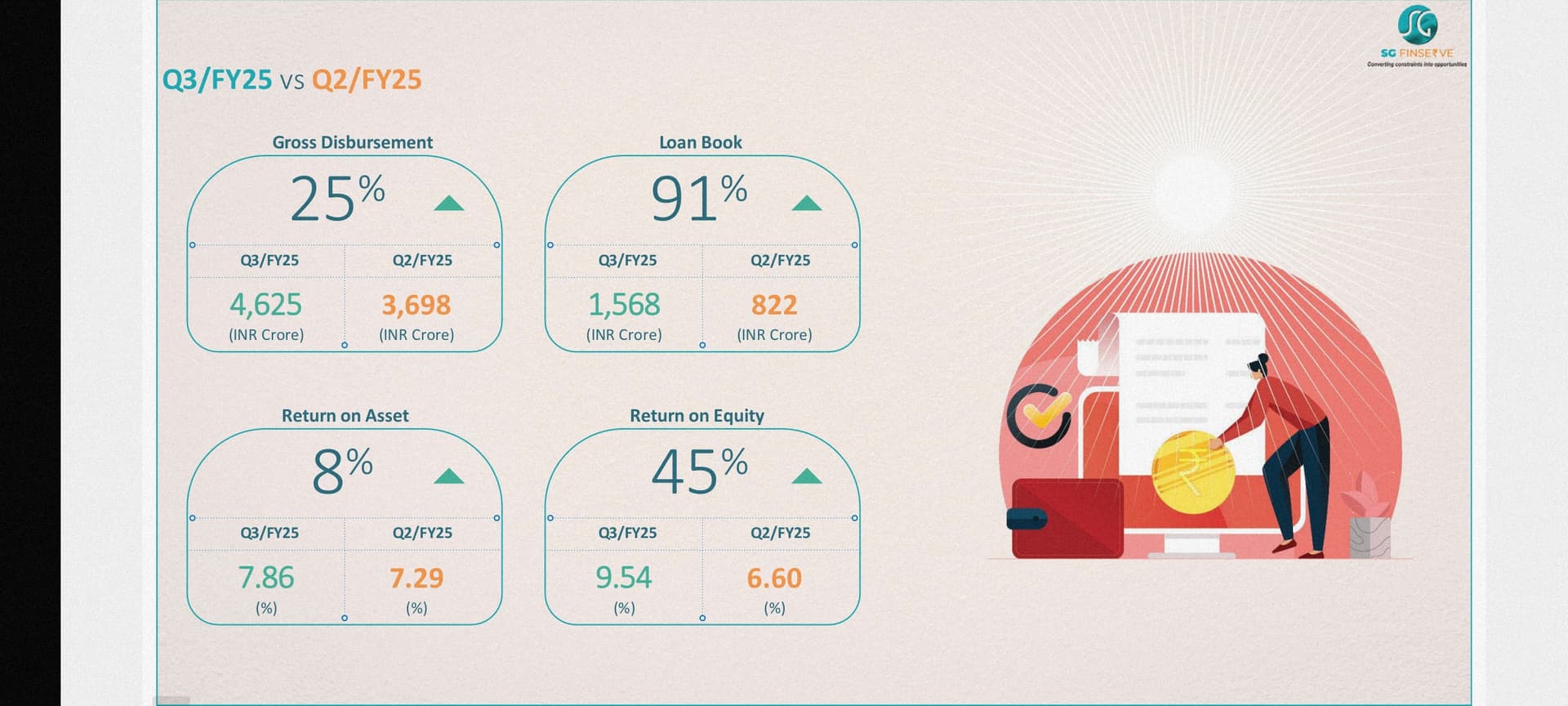

gross disbursement q4fy2024= 4437 cr >>gross disbursement q3fy2024=4139 cr,

reduction in AUM reflects that the new loans issued were of shorter duration ,

q3fy 24

q4fy24

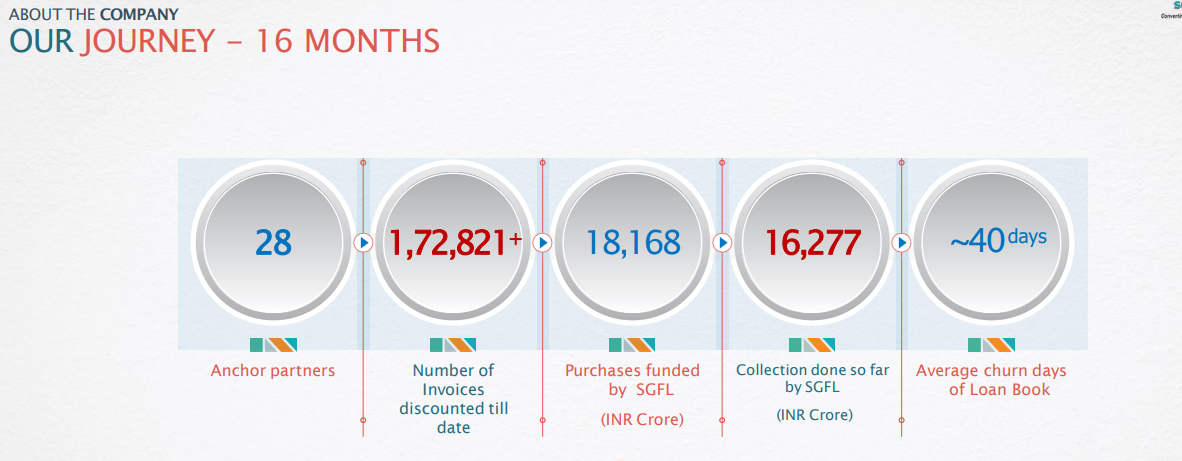

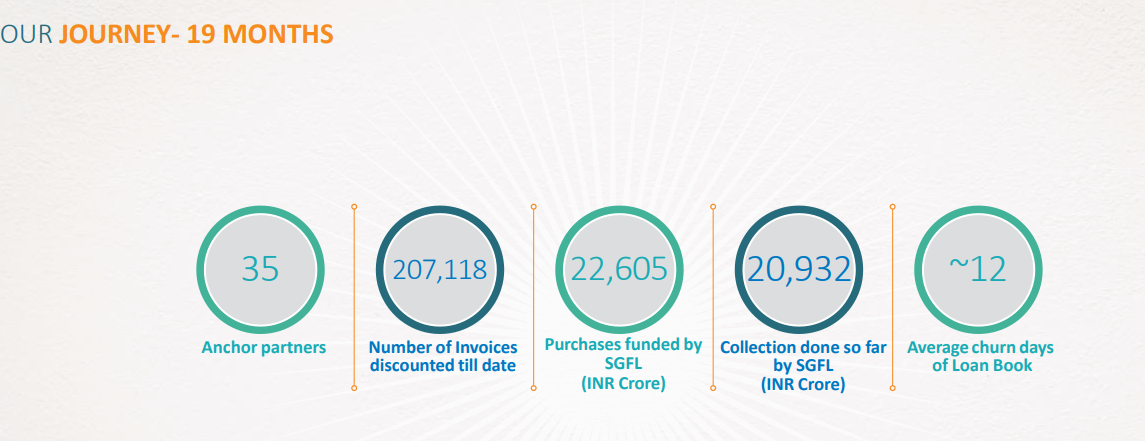

in q4fy24 result presentation 19 months journey average churn days of loan book have come down to 12 days from 40 days in q3fy24 result presentation 16 months journey

3 Likes

Ashish kacholia has reduced stake in the company, although his style of investing has been of if not completely momentum, then at least it is factored in in his investing, will have to check the results for the next quarter, then only i will take a call.

It is incorrect. Ashish kacholia got diluted but number of shares remain same as per June 2024 filings.

Disc: Invested.

3 Likes

q1fy2025 presentation shows that the company has zero bank debt, can someone help me understand why a NBFC would repay their entire bank debt of 800cr and borrow unsecured loan funds of 600 cr from promoters

also the business has performed poor in all matrix QoQ basis

The company has withdrawn its Crisil rating it seems today. Has repaid all the bank loans.

Any idea why the NBFC would give up it’s AA rating?

Company have received NBFC Type 2 certificate from RBI.

Can anybody highlight the implications of this like on the cost of funds and other details?

They have to follow more stringent regulatory controls than earlier as now the can use public money and deal with them directly.

RBI can impose paneity or restriction on their activity if they don’t follow norms!

1 Like

Penalty by RBI !!

They had their first concall, here are my running notes from the same.

Opening remark:

- 1st investor call

- Key team- saurabh dhavan ceo, sahil sikka coo and cfo, abhishek mahajan cro, ankush agar chief experience officer

- Having worked with apl apollo and apollo pipes, lack of funding sme traders which restricts their growth

- One stock supply chain funding company

- 720 crs pure equity raise, 50% promoters and 50% other investors

- Initial target to address group channel partners, once this gets introduced here then other anchors and brands will be introduces

- Other than apollo, working with jsw, vedanta, tata group, oppo mobile, kajaria, havells etc

- Apl apollo tubes in covid started to stop credit, and instead of 1% cash discount to 2% cash discount, traders churned inventory 7-8 times, so this would give them 15-16% more v/s 9-10% of interest cost, so thats how apl apollo reduced debtor days

- Then a couple years later larger distributors stopped taking the discount as they werent able to raise cash using banks, so the group decided to tap into this

- Now 2000 cr loan book, 25-30 days repayment cycle

- 6000 cr loan book target till Fy27, ROA 4%, ROE 18-20%, NIM 6-6.5%

- 25-30% is groups own channels, and retailers associated with their own distributors, distributors 50-60k cr, retailers each do 5k cr or so, theyve also done large businesses, 12-13% interest rate for distributors but now as company is expanding to retailers this will also increase

- Infused other 450 crs in form of warrants last month

- 856 cr net worth, 720 infused initially, 1500 cr net worth by fy27, loan book at 2.2x times

- 35-40% exposure with be group and rest will be other groups

- Terms are fixed with large corporates, invoices flow from SAP of anchor to them, and direct financing happens to the large corporates only and not the distributor

- Large banks 9-11% and lower risk profiles, large nbfc aditya birla, tata capital 11-12% still lower risk profiles, new age corporates 13% , company will do at 11-13%

- Systems are aligned with income tax and gst portal

- Automated payments also done with hdfc axis

- Credit assessment model is a development ongoing for the software

- Plans to launch 24*7 banking from next year onwards

- 2500 cr loan book by end of year

- Current 1100 loan book??

- Started immediately post listing, wanted to maintain cg standards

- No CGs given by apl apollo and pipes for sg finserve

Participant discussion

- Asset quality how would it maintain, there are internal checks done, plus history, plus

- 35-40 target list of large anchor, eg tata motors itself runs 6000 cr financing

- 75 anchors by FY27

- Top down approach borrower, dealer of an anchor, MOU will be signed with an anchor with condition that based on their recommendation theyre lending to the dealer, and incase of default the anchor company will not supply to the dealer, and 5 years plus relationship of dealer and anchor and at least 50% of business from the anchor

- 30000 cr total worth of disbursements

- Minimum will be 3 years relationship, personal guarantees of promoter if incase proprietor then they take of wife and kids also, plus there are assets taken also as collateral

- On 1500 crs 13% direct, on 4500 5% spreads, ROA will be 4% and ROE 18%

- After finance cost employee and tech cost only

- Process of getting type-b/2 license from RBI hence the loan book was reduced, now that license acquired will run up again, provision is against standard asset only

- Business team responsible for collections, this is all timely, negligible overdue

- Underwriting 11 people collections 4 people total employee 64

- Future debt/equity will be 3:1, currently entire funding equity

- Previous credit rating was AA, withdrawn during license period, now will come back

- Quarterly disbursal run rate- 4000 crs per qtr, 5000 crs per qtr when 1500 crs

Disclosure- tracking not invested

11 Likes

Link to Concall

1 Like

The balance sheet of Sept 2024 shows almost no borrowing and an approx drop in the loan assets of the company. What happened?

PS : Just started tracking the company and still have to go through a lot of docs

1 Like

It was done to ensure type 2 NBFC license .

Good QoQ result but not YOY basis

https://www.bseindia.com/xml-data/corpfiling/AttachLive/380aade1-eeda-4637-ad33-fd08bee4c9b8.pdf

Q2FY25 Concall notes & highlights

-

90% loan book growth qoq

-

Equity capital is 1000 cr 340 cr to come ahead.

-

Confident of achieving target AUM.

-

Group company will contribute no more than 25% of loan book rest will come from reputed conglomerate

-

18-20% roe 4% roa target. By FY27

-

0 NPA

-

Interest cost yield spread:

-

New MOUs have been signed/new Anchor partners: 3 MOUs Whirlpool, Ingram, Polycab. 40 anchors now total.

-

Chances of NPA: it will be there…but it’s low. Anchors will play a role in this. Anchors will come in support. So chances are low and we have witnessed that. Our Pf at Risk are all very controlled. Our over dues and PAR are very controlled now.

-

Impact of sg mart like inventory loss: our cycle is 30-35 days. We have not seen any issue so far from any steel customers. Even the distributors didn’t face any loss due to steel price crash.

-

Current health of the supply chain market: at present there is no issue of slowdown.we churn very fast. Our cycle length is very low. Fast moving goods items’ companies/manufacturers in different sectors are our anchors. Overall health will be dependent on MSME customers and the anchors economic conditions etc

-

Retail financing NPA mitigation strategy: So, when we enter the retailers, we would we would have already considered the entire database and their run with the particular distributor because retailers would only be, the ones which are operating with the existing distributors who are our borrowers. We will have stop supply from the distributor at certain anchors. We can also get stop supply for the step down. There are certain brands which give, stop supply for the retailers as well. But otherwise, we will have to rely on the distributor and also take an underlying contingent guarantee from the distributor when financing the retailers.

-

So, it will be much higher when we reach the next quarter. This is a quarterly number. So month on month, have we reached reached a run rate of above 5,000? Answer is yes. But this will be much higher when we do the next quarter

-

NPA can come in which situation: Bankruptcy of the borrower/dealers. Getting hit from somewhere else and getting hit to the borrower that leading to bankruptcy

-

Anchor level channel penetration is very low so scope of growth is high.

-

Only lending to reccomended Distributor/ dealer from the anchor

-

Competition: No one is focussed only on supply chain financing.

-

Very confident of achieving ROE target given last quarter even more than last quarter.

-

Book value per share after receiving all the fund will be 225 rs next year.

Book value calculation:

Right now the equity base is 1,000 crores. We are expecting another 340 cr. So we will be getting another 340 crores, so it will be worth 1340 crores and flow back of the profit of next year will be worth 100 crores plus, so about 1400 crores at the end of next financial year. Number of shares will be 6.6 crores, so book value should be around 225 rupees per share. -

Entry barrier: getting entry to the tie up to the reputed large anchors will not be easy. Technology is not a big deal.

-

New to finance customer is less than 5%

-

ROE Calculation: on a loan book of 5000 cr we’ll be having an equity of 1500-1700 cr. Balance will be from bank borrowing. Today yield is 13-14% which will go up as we start retailers. Cost of borrowing is 8.5%. we are already doing minimum provisioning required for NPA as per RBI guideline. So you do simple math we’ll do pbt of 400 cr. 300 cr pat number. So ROE comes around = 300 cr pat/(1500 or 1700 cr equity) =18-20%

-

Rajratan like scenario: Big lenders don’t focus on this business. Like tata steel doesn’t focus on bead wire. Kotak Bank has just 4000 cr loan book in this business.

-

NCD we’ll raise very soon.

-

Cost of borrowing 8.5%. lending at 13% gives spread of 4 % minimum

-

Competetion:

So I can I can I can divide this that banks in supply chain finance are lending between 9% to 11%. And then it is financial institution NBFCs which include, likes of Aditya Birla, Tata Capital, Eurofin Corp. And we are directly in competition at many places with them. And 13% upwards are the smaller NBFCs and smaller players, which are into supply chain finance.

So 11% to 13%, 13.5% is a play wherein we have larger NBFCs, but no one is focused only on supply chain finance. We have an advantage that we are very clear that we will we are doing supply chain finance and that is how we are covering all the dealers’ distributors. For example, when we tie up with an anchor, we get database of the entire dealer distributor base of that anchor. So we’ve got coverage team on the ground, which is covering each and every dealer distributor and looking for conversion because we know that the number of dealers distributors now will increase drastically. So that coverage also acts as an advantage for us to, get ahead in the competition.

My take: very good result. It seems they will achieve the growth guidance given. Invested.

10 Likes

Agree with your observations and have built position at current levels as management has walked the talk till now.

For me, key takeways and reasons of investment are:

- Zero NPA NBFC and around 2.9 book value

- Preferential issue of promoters and investors at 450 gives MOS

- Book Value to increase to 225 by next year end. If current ratio of Market to BV is maintained we see a 50 percent increase in price from these levels

- Inclusion of additional clients and their channel partners reducing dependency on APL group

- Reducing interest rate cycle can help in margins

- More than 90 percent of shareholders hold more than 10 k shares

Key risk in above is below:

- Any instance of NPA

- Quality of Retailers onboarded in Q1 2025 which impact the Zero NPA story

Disclosure-Invested and adding on falls

5 Likes

I agree with the antithesis part of NPA coming from retailers