Just wanted to understand that over the period of 10-11 years the sales has increased by <5 times but the trade recievables has increased by > 12 times! I doubt if the bookes are clean.

3 Likes

Today I was talking with a friend from bihar, the moment I told that SIS is owned by son of a politician from bihar and because of political links it is being viewed with suspicion. He said that the politician in question is a RS MP and is known for his statesmanship. He went a bit further and said that he, at least in bihar is viewed as of the stature of Vajpayee sahab. Although it doesn’t change what’s there on ground but at least for me it has alleviated a little bit of fear of being linked to a politician. I am invested in this company at 347 rs. Others might add a bit into this.

2 Likes

It is a completely known fact that MD Rituraj Kishore Sinha and Founder & Chairman R K Sinha are active members of BJP. They are actively engaged in politics. But the company is run quite professionally. The management as well as promoter are quite interactive on earnings call and also have an in depth knowledge of the business. They are now also actively engaging with investors. A video call is taking place explaining each segment of the business in great detail.

While yes there is a concern that Board of Directors have a lot of members of family.

Attaching last two presentations and recording of call.

3 Likes

I have been looking for these videos. This company is close to 10% of my portfolio and my whole bet is on the size of the pond.

The company is run very professionally and works on volume, do go through the hierarchy of every division above. All are market veterans with more than 2 decades in the industry. One standout feature about this business is 80JJ tax exemption which is provided to them by the government. They were the first company whom I have seen were positive on the increase of the wage hikes which tells me they are true leaders.

The valuations are juicy and are at a support level, tracking position can definitely be triggered at this zone. Been an investor since COVID.

-Abhishek

5 Likes

Right Abhishek!

It looks at absolute bottom has been made…but ny reason why markets are not giving this the value it deserves?

After considering worst case scenario, was able to identify 2 reasons:

- Debt to equity of the company is 0.74! Which is a big deal as it is only a services company.

- Promoters involved in politics (Same old reason)

Disc.- 0.5% of pf(only speculative bet). No reco. Open for any constructive criticism.

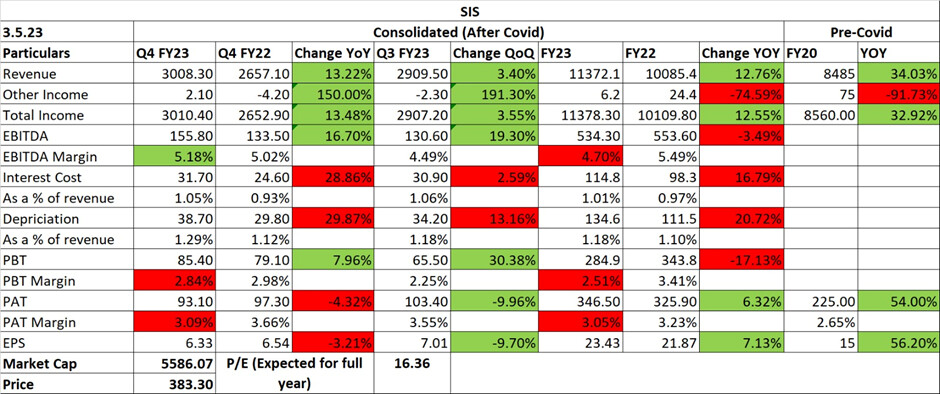

| - | The Return on Equity for FY23 was 15.7%. ROCE is at 12%. |

|---|---|

| - | Security Solutions India posted a revenue growth of 19.9% over FY22. Our technology based security solutions businesses continue to grow, with 1,088 new installations during the quarter in VProtect , our Alarm monitoring and response business, which now services more than 14,000 customer connections. Additionally, the VProtect business has a strong pipeline with confirmed orders of almost 5,000 sites of to implement in the coming quarters. |

| - | Facility Management Solutions posted a revenue growth of 36.2% over FY22. This growth was primarily driven by new wins of around INR 11 cr. of monthly revenue in Healthcare, Manufacturing, IT and Transportation segments. The role of technology in service delivery is increasing with increasing interest from customers for more mechanized and advanced facility management solutions. DSO days remained stable at 85 days during Q4 FY23. |

| - | Security Solutions International posted a revenue growth of 0.7% over FY22 (0.5% on constant currency basis); the growth was achieved despite the one time COVID related contracts falling off this year. Labour shortages in international geographies continued to affect costs. |

| - | Cash Logistics also continued its strong revenue growth with a 38.3% growth over FY22. |

| - | Margins have shown improvement due to robust management of operations. |

| - | Due to, hardening interest rates and the strong cash flow generation in FY23, post Q4 FY23, we have paid down A$15 mn . (INR 82.6 cr.) to the debt syndicate led by National Australia Bank (NAB) in Australia and reduced the outstanding amount to A$88.5 mn (INR 487.1 cr). |

| - | Net Debt/ EBITDA was 1.75 as of end of Q4 FY23, which was lower than 2.06 as of end of Q3 FY23. The decrease in Net Debt / EBITDA was driven by better working capital management during the quarter. |

| - | OCF/EBITDA on a consolidated basis was 144.2% for the quarter which is a result of the strong working capital management. DSO for the quarter reduced by 2 days. |

| - | Client concentration is very low. |

| - | Guidance: Confident of gaining medium term momentum on the backdrop of deals won. Expects improvement in margin front. Expects pickup in facility management & security business. For Facility management, the growth trend will continue but more focus on EBITDA margin rather than top line. Want to keep the D/E ratio at 1.5-2 range. The ideal ratio would be to keep a little below 1.5. Reach pre-covid level margins in India business which is 5.5-6%. Traction in FY24 is such that margins will be achieved. |

3 Likes

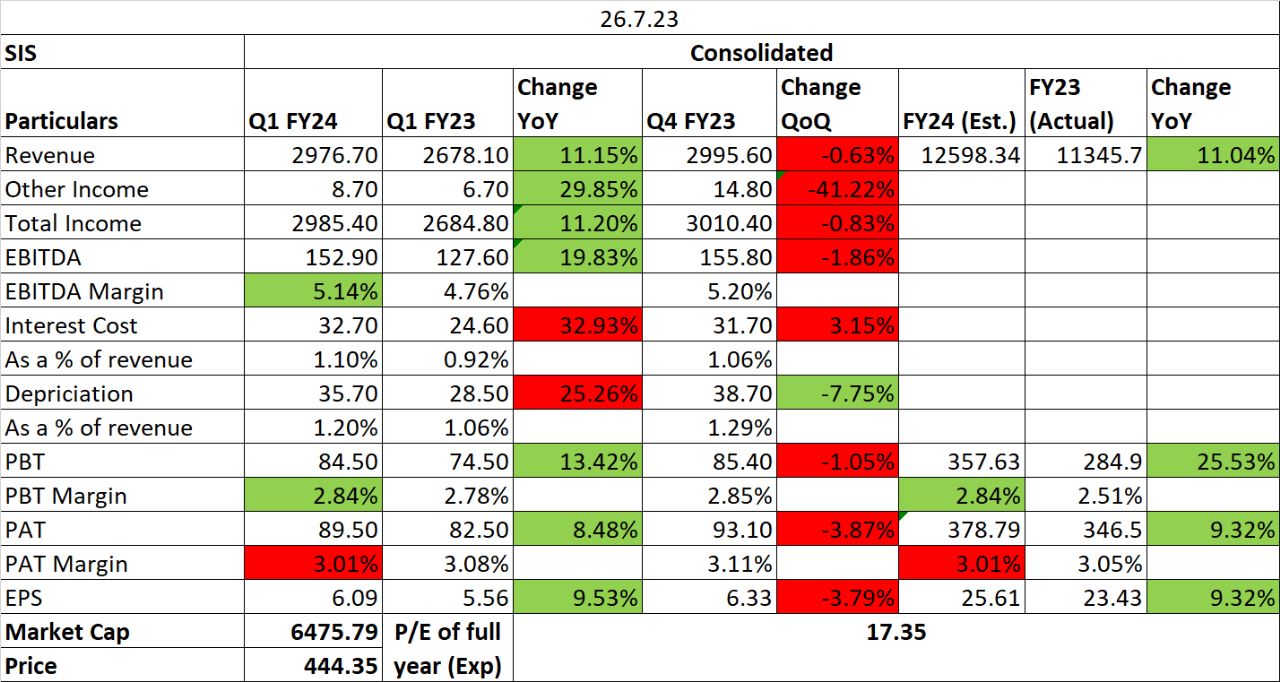

- Industry is transforming towards more organized players. Rising compliance with laws and regulations. Rising demand for superior services and quality. Rising per capita income, urbanization and Infrastructure Growth.

- Our Vision 2025, which came into effect in FY21, outlines the goal of transforming our market leadership into market share dominance and transitioning from a Services Company to a Solutions Company.

- Margins in the FM business have improved but are still below pre-COVID levels, and the company is working on further improvements. Cash management business will see further improvement in revenue and profitability.

- OCF to EBITDA conversion was negative due to increase in DSO. Historically Q1 sees weak collections since Q4 has strong collections. Usually collections improve in June itself which didn’t happen this quarter. DSO for Q1 FY24 increased by 6 days.

- Elevated SG&A costs in FY22 and FY23 impacted margins, but actions have been taken to address this and improve margin profiles.

- The VProtect alarm monitoring business has the capability to deliver double-digit EBITDA margins.

- The Australian business is showing an uptrend, and the labor supply situation is easing, which is expected to have a positive impact on performance.

- SIS aims to build all its businesses and sees itself as a platform with separate CEOs and CXOs running each segment. The company is focused on returning to pre-COVID levels of margins for all businesses and expects substantial growth and market share uptick in the post-COVID world.

- Company has maintained 6% EBITDA margins guidance and has refrained from giving topline guidance.

3 Likes

Hi, do you follow Quess and TeamLease as well? They have similar businesses among themselves.

If you compare it to Quess and TeamLease, which of the three is positioned the best for future growth? Quess has Monster which has a lot of potential and backing of FII’s whereas TeamLease has an edge on IT Staffing. SIS is a market leader in Cash management and VProtect, again has future growth prospects.

Quess has very low margins. Teamlease was a very high P/E few years ago. Plus the services are also a little different to be compared from a one-to-one basis.

This kind of business requires some political connection. The very nature of business is dealing with power and people with power.

I respect your view but I don’t think providing Security guards, cameras, and any other kind of basic security has anything to do with political power or connection.

2 Likes

I had 241 shares in Dec23, I applied 200 share in buyback, the contract note is generated for 78 shares, but I have received debit msg of 200 shares from CDSL. The money is yet to credit in bank account.

Is there any flaw in zerodha system?

1 Like

I have the same experience. Let’s wait patiently for a week

1 Like

This is standard practice though weird . By today evening you will receive back 122 shares . Further even amount will be credited in your bank account by today evening.

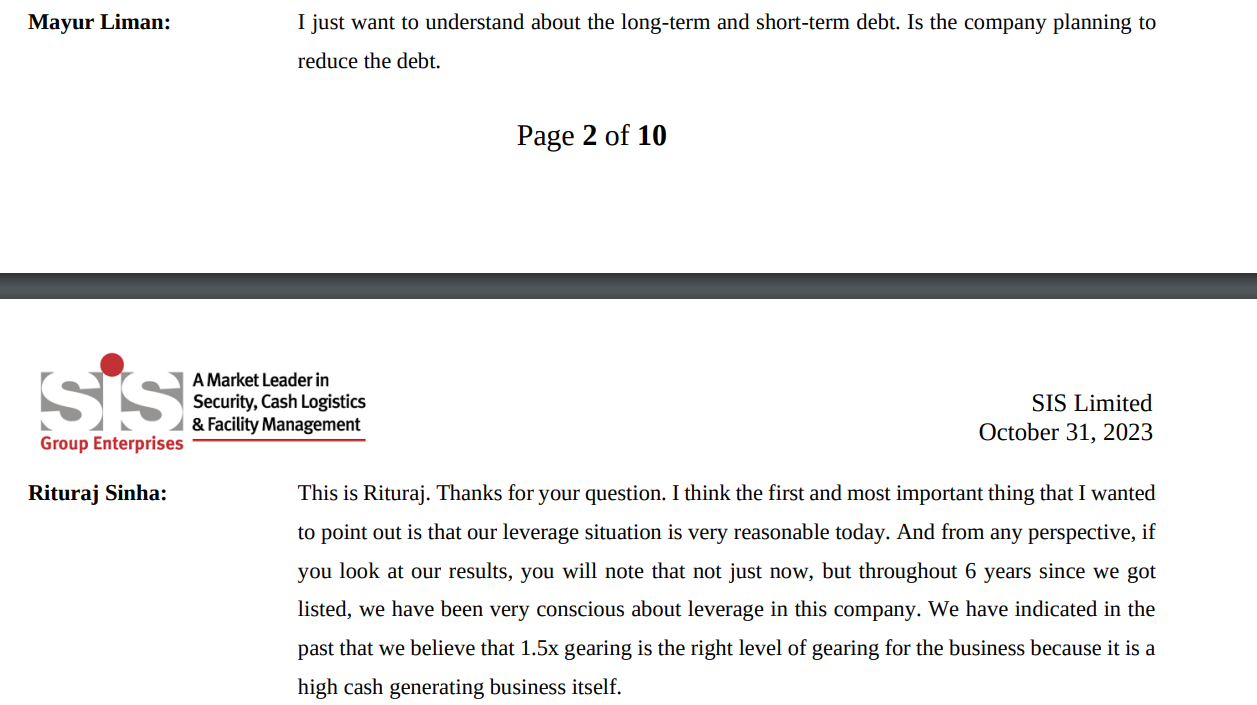

I don’t really understand why this business needs a lot of debt. Any inputs?

Adobe Scan 23 Feb 2024.pdf (877.4 KB)

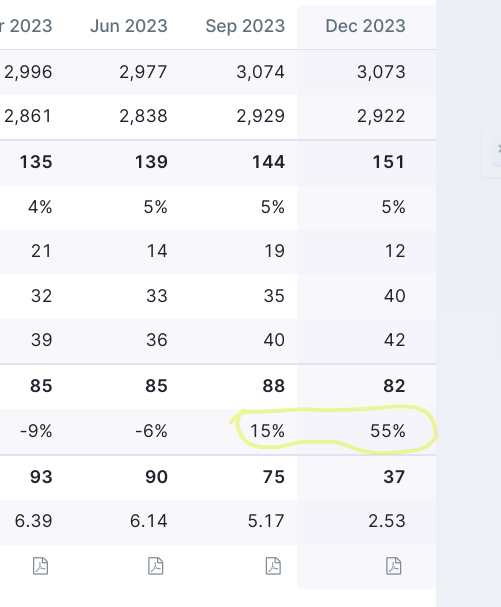

My note on Q3FY24 concall

3 Likes

The tax rates are dependent on manpower additions for that quarter, since they avail 80 JJAA benefits. I believe they were not able to add enough manpower to avail these benefits for this quarter. The company has addressed this query in the latest concall.

1 Like

Thanks for the inputs, Management seems to keep debt to reduce Tax exposure. The business does not seem to need additional debt. They are not investing or growing fast. Debt is good if there is a good capital allocation which i can not really see… what am i missing here?

I am researching this company (1) Business in good and can steadily grow. (2) Cash positive but concerns are (1) seemingly unnecessary debt (2) Slow growth (3) people Intensive - Not some of liabilities.