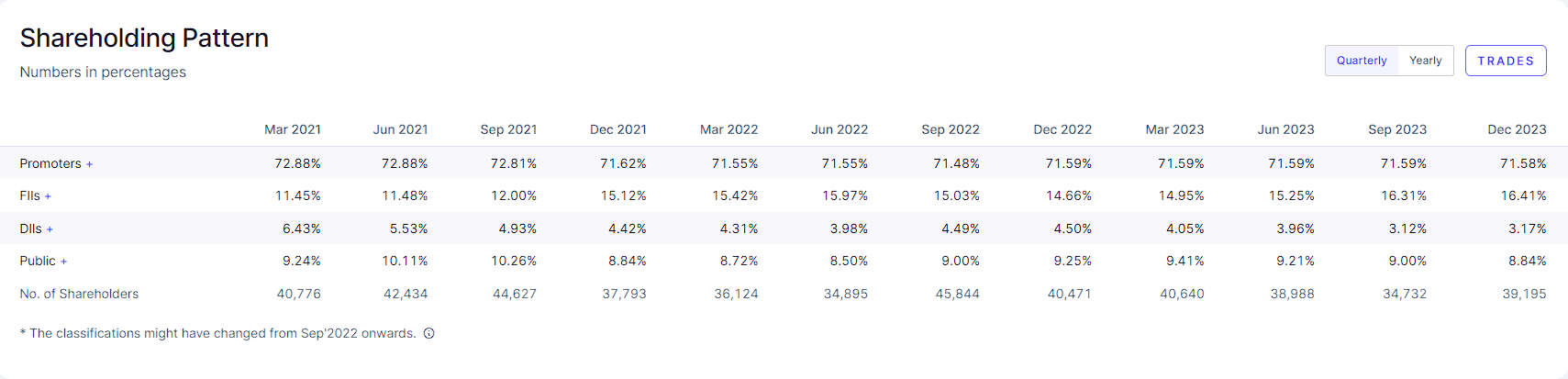

The shareholdings of FII’s is increasing rapidly… please explain?

1 Like

Investment in emoha senior is also a very good move. More investment woukd have been better (5% is too low)

1 Like

Why is the market not giving premium to the stock price, despite such good revenue growth?

1 Like

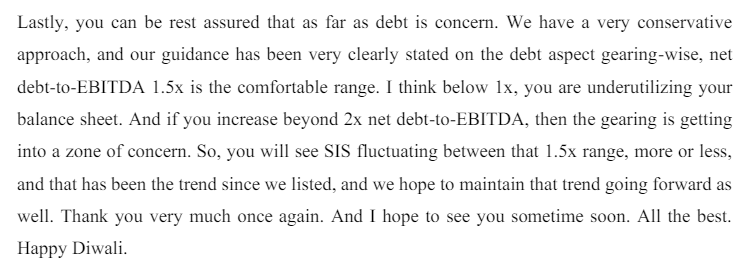

Does anyone know why management wants to use leverage in the balance sheet even when there’s no Capex as such involved?

Its hurting the bottom-line.

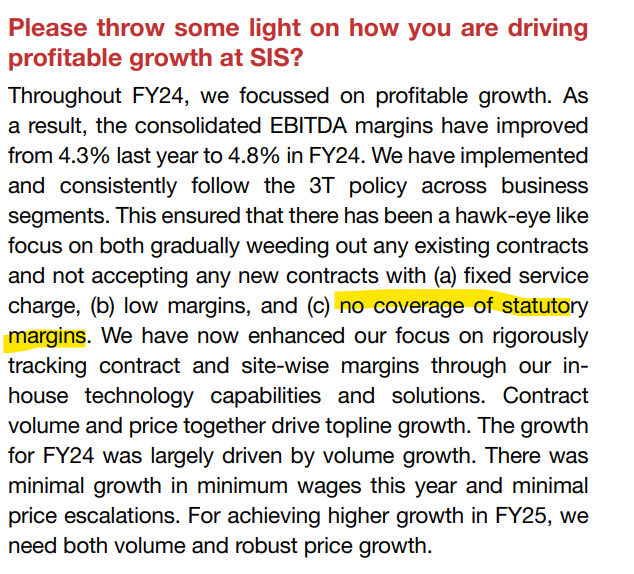

Can someone please explain what is “no coverage of statutory margins”

This is from 2024 Annual report

This is most probably related to contracts that give them a fixed margin over cost in which the wages and other technological cost gets completely passed onto the customer in case of events like minimum wage increase or installation of new equipment, etc.

1 Like

Consider it as a steady performer,

Growth will be 1.5 to 2X of GDP growth.

Will Maintain ROE of 15%.

Possible to spinoff cashlogistic business.

Interview with the Promoter, https://www.youtube.com/watch?v=Tfb9AgDi8_Q

3 Likes

Investing in Safety: How SIS India is Shaping the Future of Security Solutions

Security services have become an integral part of our daily lives, from the friendly greeting of a security guard at your office to the vigilant presence at every apartment complex. In today’s unpredictable world, companies like Security & Intelligence Services (India) play a pivotal role in enhancing safety and security.

With a wide range of offerings—such as manned guarding and cash logistics—SIS not only protects assets but also encourages confidence in investors. As the demand for robust security solutions continues to grow, SIS is well-positioned to capitalize on this trend, making it a noteworthy stock to consider.

Industry Overview- The Indian security services market is set to hit ₹1,574 billion by 2024—because who doesn’t want to pay to keep their stuff safe? With more people moving to cities and the rise of tech like data analytics, security companies are eager to offer personalized services. Now, clients want more than just a guard; they want a complete security package with one point of contact. It’s all about convenience! As we move into this tech-driven future, security is becoming less about just safety and more about high-tech solutions. Read how SIS is providing complete packages of security solutions to the client in this blog.

Business Overview- Security & Intelligence Services (India) is a premier provider of security and related services across the Asia-Pacific region and is well-equipped to meet the growing demand for security and facility management solutions. Segments consist of -

· Security Solutions- SIS is a leading provider in the Asia-Pacific region, offering a wide range of manned and technological security solutions across India, Australia, New Zealand, and Singapore. SIS Deploying AI in their services because on the client application side, AI Deploying is huge implication because as it is not just a Manpower based business it’s Manpower plus technology so if you have a CCTV which has a lot of artificial intelligence built into it that brings far more efficiency and reliability and a lot of analytics that the client appreciates.

· Facility Management- The company operates four brands—ServiceMaster Clean, Dusters Total Solutions, RARE Hospitality, and Terminix—providing services like housekeeping, integrated facility management, HVAC maintenance, and pest control. In facility management, SIS currently emphasizes soft services (Includes usage of a facility such as cleaning and catering), but the higher margins are associated with hard services (Includes managing the physical aspect of a facility such as building maintenance and plumbing). To enhance profitability, the company plans to increase its focus on securing hard service management contracts in the future. Orders in FMS are not at a steady growth rate, shredding a lot of contracts having lower margin. Expected to grow this business at 18% CAGR organically.

· Cash Logistics- In a joint venture with Prosegur, SIS offers comprehensive cash logistics services, including cash in transit, doorstep banking, cash processing, ATM replenishment, and vault solutions. It operates 3,000+ cash vans and 60+ vaults covering 300+ cities across India. The company is looking to separately list the Cash business by September next year.

Talking about the financial performance of the company-On a consolidated basis, revenue for SIS Group increased by 5.1% year-on-year basis to INR3,130 crores. While EBITDA took a small hit of 1.2%, again, on a Y-o-Y basis to INR137 crores. India business expected to grow at 15% CAGR. Doubling the Indian business to about 15000 Cr in the next 5 years. International business will grow at a much lower growth because of labor shortage issue in the continues to persist.

Future Outlook- Growing at CAGR of 15% and management expect the same growth to continue in future. In the festival season, expecting higher demand from the second half of FY25. There are few segments, especially e-commerce segment, big giants typically have requirement two three times the normal security guards that they want, and SIS is ready to provide. EBITDA margin guidance remains at 6%. The company has encountered challenges in its international business (Facing labor shortage in Australia), expected to normalize in coming 2 quarters. In securities, the working capital cycle is 84. In an ideal scenario they would like to bring it close to 70.

Technical View- SIS is showing a neutral trend on both the weekly and monthly charts, with the price consolidating in the range of 402-430 over the last few weeks. It has reversed from a strong weekly support level at 398, having found support there four times. Currently, SIS is below the 100-week moving average at 421.8 and is waiting for a breakout from a triangle pattern. Once this breakout occurs, the price may experience an upside rally, with immediate resistance at 430. If it closes above this level, can expect further aggressive movement towards 560-647. Conversely, strong weekly and monthly support levels are found at 398-346. Investors can consider accumulating at the current price (25% to 50%), and if a correction occurs in the demand zone of 398-346, they can average by adding more. The recommended holding period is 6 to 9 months.

Conclusion, Security & Intelligence Services (India) is well-positioned to grow in the expanding security market, projected to reach ₹1,574 billion. With a strong focus on both manpower and technology, SIS is ready to meet the rising demand for comprehensive security solutions. Despite facing challenges like labor shortages, the company aims for a 15% growth rate and is set to capitalize on upcoming opportunities. Investing in SIS could be a step towards a more secure future for both individuals and businesses.

1 Like

I think Krystal integrated is better placed given its growth and good relation with CM of Maharashtra

SIS Limited | Management Guidance

Says Will announce acquisition-deals in the next 1-2 months

India Security Biz EBITDA will cross 6% in next few quarters

Facility Management EBITDA will be close to 5% in next quarter

Have a kitty of 100-200 Cr for M&A

Watch here - https://youtu.be/7ewX6C44P14

Board approved buyback through tender route at Rs. 404 per share for an amount not exceeding 150 Crores. So, up to 2.57% of the total outstanding equity shares would be bought back.

2 Likes