RBI discussion paper on digital payments have wide ramifications for credit card companies. Currently the rally in price seems to be over. Better to be cautious in this counter.

will increase compition, henceforth performance will matter.

https://www.google.com/amp/s/www.financialexpress.com/money/cashback-sbi-card-launched-check-features-benefits-renewal-fee/2651924/lite/

SBI cash back card launched by the SBI cards and payment services.

SBI cards made a very aggressive move with this launch of cash back credit card. ICICI earned so many customers due to its Amazon pay cash back card now it’s the time for the SBI to show its might and acquire large number of customers to its fold with this 5% cash back. And they priced it perfectly. The annula fee from second year is 999. With this they will get huge fee income and there is only 1% cash back in offline payments which will give boost to mdr fee.

And there might not be any competition as it’s more targeted towards middle class and the class between upper and middle class with the cap of 10000 per billing cycle. The incumbent large credit card players like hdfc and ICICI might not launch a competitive card as ICICI has Amazon pay and hdfc has its own good card portfolio the ground is open for the SBI card to make a splash and issue millions of new cards.

Disclosure: holding.

2 Likes

I have one fundamental question here, how credit card companies are able to afford these higher cashback. I understand for specific cases like partner with some merchants, but in here it is vanilla cashback on all transactions right, say 1.5% on flipkart axis card on all transaction, now in SBI 5% on all online merchants. Who is really bearing this cost?

2 Likes

When I compare this card with Amazon ICICI or Flipkart Axis , only advantage is 5% cash back from all the online purchases. Disadvantage is 10 k / month limit and 999 per year annual fee , which is not there in both the cards. One must purchase approx 20 k/ year online to compensate for annual fee. I would prefer to have both Amazon ICICI and Flipkart Axis and avail unlimited 5% cash back on 3 main e-commerce portals without paying any annual fee. Also, from investment perspective , though I like credit card business , I have not invested in SBI Card as it is consistently losing market share. Management change has also been frequent and abrupt in the past.

2 Likes

Overall purchase should be 2 Lacs/annum online+offline. Happily switched to SBI. Also received highest credit approval compared to existing Axis, HDFC, IDFC cards.

1 Like

Shoddy research & some wild conjecturing in the article.

Rise of UPI, MDR changes, retail spending concerns are done to death - somehow these only seem to become factors when it comes to views on SBI Cards share prices and not on other payments and NBFC cos

On off data, due to festive sales, need to see how much can sustain

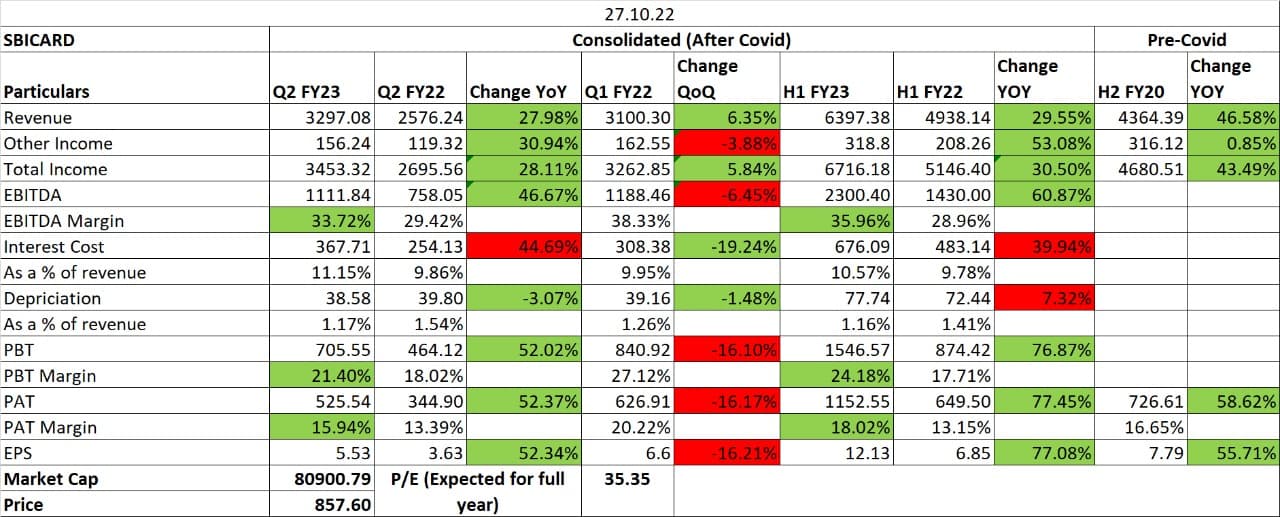

QoQ PAT dip is not good - have to hear mgmt commentary. Given the news around record breaking spends in this festival season, was this a case of people holding off spending till Oct? Or was there a general slowdown in Q2

It may be because consumers were waiting for the Diwali season for spending. Even my parents cut down on spending since August, so that they could spend more during October and November. I guess it’s a positive that the numbers aren’t so bad and we will see better results in next 2 quarters which are historically better quarters for such companies.

Personal view:

-

Raising interest rates are directly hitting the P&L with no way to passon the costs to their card holders.

-

Despite reduction in employee expenses, there is a massive spike in operating costs.

- This could be due to the launch of Cashback card and subsequent Spike in new card issuances to 13lak cards vs 9lak cards last quarter.

- There may be more long term impact as well since Cashback card comes with relatively higher rewards costs.

-

Credit costs spiking up again to 5.6% (annualized) , a bad sign.

-

This business ROA are quite volatile, yet most profitable compared to any other credit business out there.

Credit costs itself are higher than the ROA in multiple quarters. - This structure will lead to massive earnings volatility in bad times and could result in massive swings in stock price. -

HDFC bank management has said in a concall that the chronic revolvers are trending down and they don’t see it inching back.

This might be the case with SBI cards as well and reflected in the Interest income dip witness in this quarter.

- I believe this is because of fintechs like Cred, protecting the masses by educating them about the predatory charges on rollover debt. - so, this could be a longer term trend.

2 Likes

Sbi cards have also changes there changes.

More fees on emi conversion and rent payment.

Could be quite free type Cashflow according to me.

Just confirm is it true or not as these were received from one of my friend who uses sbi cards i personally recently got one this month only and no update was there.

- The management is hopeful of seeing increasing discretionary spends in the coming quarters.

- Cost of fund is likely to go up by 40-50 bps and margins to be affected +/- 10 bps

- Cost to Income will remain on an elevated level due to increased focus on new customer acquisition.

- Healthy growth in electronics, hotel, restaurant, entertainment and furnishing segment

- Credit Card base is expected to reach 750 million in 5 years.

- Lower revolver, increase in CoF and regulatory restrictions on fees and penalties to act as near term overhang

- Investments in marketing & distribution to aid improving trends in travel, hotel, leisure and entertainment spends

- Steady market share, product launches and pick up in spends to gradually convert into revolvers, thereby aiding valuation ahead.

Revolver meaning that more customers started paying off their bills in the same month rather than rolling over it to the next month. Better cash flow.

5 Likes