here are the results :

1 Like

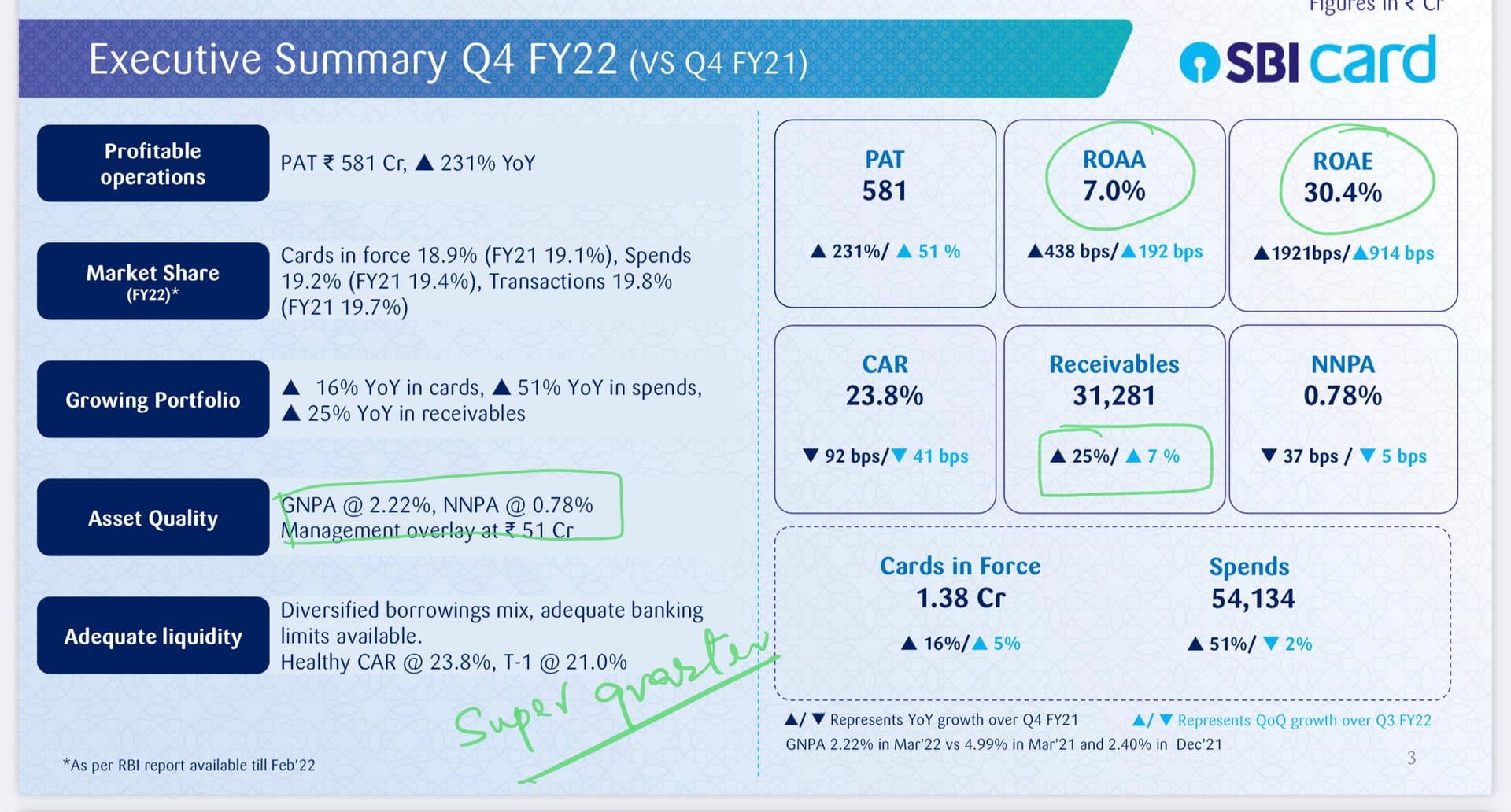

Result came after the market hours.

Investor Presentation :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3925d1d7-0be8-4f07-bced-323f345112af.pdf

Press release :

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3147b388-fc08-46b4-aded-8131cbb5512a.pdf

https://www.bseindia.com/xml-data/corpfiling/AttachLive/71a39334-a2f9-4e8d-ad78-00a189bcb44d.pdf

3 Likes

Fact - SBI Cards & Payment Services is the 2nd Largest Purely Credit Card Issuer in India with 1.18 crore cards in force enjoying a healthy market share of 19.1% as of March 31, 2021

when most NBFCs are valued at less than 5 Price to Book, Bajaj Finance and SBI are at 11. Isnt it that expectations are too much priced in this stock and few bad quarters can hammer the stock? The last quarter results was decent but the valuations are such that its priced to perfection.

Any contra views?

2 Likes

No I dont there is any restriction on making payments through credit cards. Today I paid both my Simpl and Lazy pay dues through my axis credit card.

In the case if Simpl, for transactions from 1st to 15th, the bill is generated on 15th and payment is to be made by 20th. Same way for next 15 days with due date on 5th of next month, beyond which there is a fine of Rs.10 per day. Works the same with Lazypay also.

So, assuming one makes a transaction on 1st of a month, he can get a credit period of 20 days plus 45 days on making payment through credit card. I have been using both Simpl and Lazypay for a very long now and have rarely defaulted.

Today I was surprised to receive an SMS from Lazypay asking to claim their Lazycard offering a credit limit upto 2 lakh. The card is a tieup with SBM Bank (India), which I found has received its banking license recently. It claims to have acceptance at almost all merchants (specially I could find e-commerce). So clearly, some sort of disruption is on the way

2 Likes

I think it as also good for credit cards. If credit card tie ups with paylater kind services then credit card 45, 50 days interest free period will come down to 15 to 30 days.

It could be more beneficial to credit cards rather than harm.

1 Like

Firstly we also need to understand how most investor value these credit card company as they are much less risk with a great benifit in NPA also due to very high interest rate that make them have higher price to book.

Just for example if we even see many developed market like usa and Europe there we see company like America express pure credit card play and much more slow growth opportunities and traditional a more constant compounding buisness still trades at 5-6 time there book.

This is very common with most pure credit card company to have such high pb ratio so sbi card having 1.8x to 2x of it saturated market pb ratio sound quite interesting to me.

While if we see other gold loan company in more mature and low growth market they tend to hover around 1-3 only so how these will play out is anyone’s guess.

Not all nbfc are same that need to taken in account and how they play out is also a bigger question.

As sbi cards have 2-3 growth driver

- capital consumption increase specially in mid to high income earner over a period of time.

- greater penetration over time that can make there base easily 5-10x very easily.

- New offering and move toward more cheaper loans + offering more cards that can make same customer have more then one card at a time and with more partnership can also open other income sources.

2 Likes

this impacts debit cards but similarly other credit mechanism exists for immediate loan/credit facility provided against customer profile without issuing credit cards…so can SBI CARDS be impacted ?

3 Likes

Mr. Nalin Negi, CFO Resigns

Edit: Good results + CFO resigning + finance co. makes me extremely nervous.

Any red flags?

1 Like

Headwinds for Credit card industry owing to RBI regulations.

After Apple, I expect Google play, Netflix and other tech giants to follow the same.

Disc : completely exited after Dec-21 results.

3 Likes

Interesting move by RBI

1 Like

Don’t quote me on this but I think it might be Little bad and good for company as if we see with rupay card if you do UPI atleast with Bob rupay credit card the transaction charges are zero and from both side so this might affect there direct constant source of revenue but may get them more credit dispersal capacity and also other ways they can charge it.

It may affect there net interest margin overtime but can be good in long run specially if emi etc can be there.

2 Likes

This news could be good as this will restrict the unseen credit given by BNPL and the checks that they do while credit card companies play in a more restricted space.

Finally, rbi is taking action to restrict them so they don’t issue customers in long run.

Update:- this video will help to understand in a better way that what rbi have stated.

1 Like

Sbi card is in a sweet spot as of now. With the rise in cost of living people tend to use credit cards more often and there is good chance of it being a revolving credit. And as for sbi card it has the access to the mighty sbi branch network who are very strong and especially in tier 2 and 3 cities where private banks doesn’t have any presence. The market is valuing it at par with Bajaj finance and rightly so. With the ROA of 5 and ROE of 23 it has the capability to double the profits every 3 years provided they adhere to the good credit under writing.

Now the advantage for sbi credit card is the support of its parent sbi. Sbi is pushing all its subsidiaries growth very hard be it sbi life general mutual fund and sbi card. And they have their presence across the length and breadth of India which is nearly impossible for any other bank. And from the stable of sbi it’s the sbi card business which has the Highest return metrics and has the NIM of 15 to 17%. It can do the heavy lifting for the bottom line of sbi consolidated profits. After the covid related stress issues now it’s time for the sbi card to show what they are capable off.

3 Likes

I personally have only few worried is not taking bold steps to have higher growth.

As a investor we should always need to know sbi card will rarely outperform the credit card market will loose market share at a very slow rate.

The biggest competition according to me is hdfc and axis as incase of icici the overall numbers can be huge but just talk to any credit card enthusiast other then amazon credit card other mid to premium cards are not competitive and people rarely prefer them and most just have there basic credit card that affect there average bill per card.

Just looking at sbi cards the only reason I personally Invested is that there is no better alternative for credit card stock.

We should accept around 1-2% less growth in revenue of sbi cards against credit card average that would be more realistic but it still more then 20%.

1 Like