likes of Cred making money or not but killing money-making chances of companies like SBI cards.

2 Likes

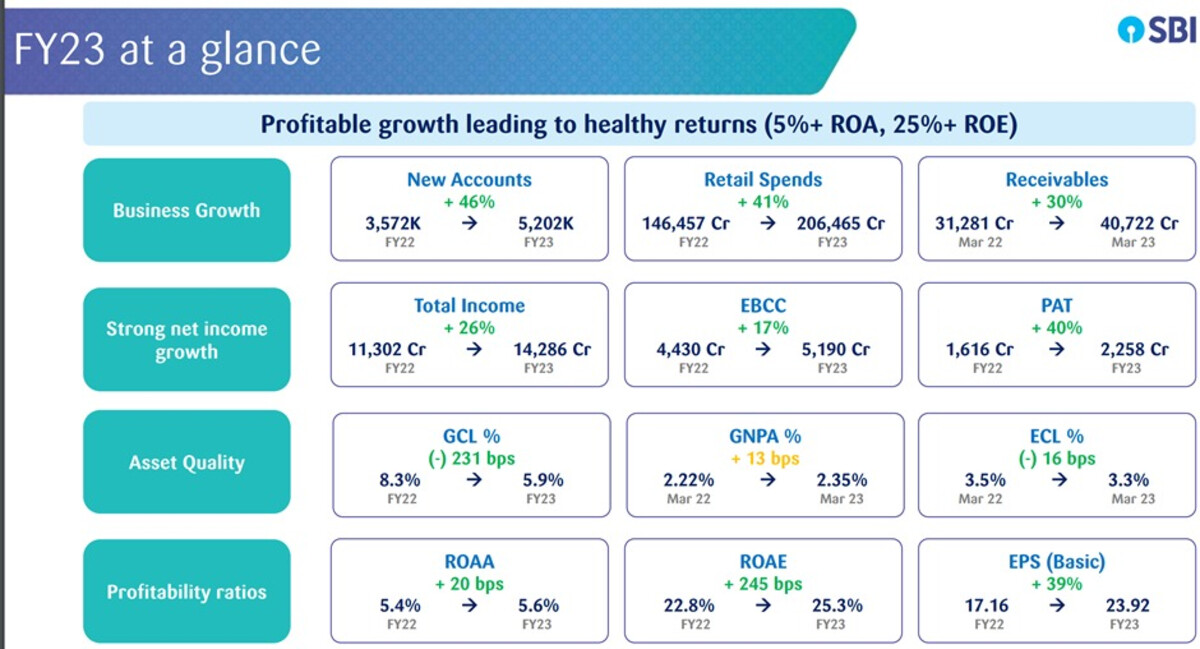

| - | No. 1 position in net card additions in FY23 |

|---|---|

| - | GNPA: 2.22%, NNPA: 0.8% |

| - | 1 million net card addition in Q3FY23. |

| - | 33% yoy growth in receivables. |

| - | 8% growth in retail card spends. Online spend increasing. |

| - | New accounts & corporate spends have also increased. |

| - | Average receivable per card has reduced. |

| - | SBI Card has partnered with Punjab & Sind Back to expand portfolio and is looking at other opportunities. |

| - | It is expected that cost of funds would increase by ~30-40 bps, in Q4 FY23. This would be largely off-set with the judicial pricing of new loan disbursals. |

| - | With the festive season behind, the company is expecting the cost to income ratio to decline, going forward. Credit cost will be below 6%. |

| - | They expect net interest margin to expand, going forward, with higher focus on the EMI lending as it yields a better margin. |

| - | Revenue growth/Earnings Growth: 20% growth in revenue for the next few quarters. |

| - | Expect revolver rate to expand. This is a good thing which means that customers will start paying more which will reduce receivables. |

| - | Want to maintain net additions of card 300,000 per month which they have maintained for the last few months and are planning to maintain for next quarters. Quarterly 1 million they want to maintain for net additions |

3 Likes

It’s result time. Being a credit card enthusiast, I had bought the second best company SBI Cards in August 2022. Had it been possible, I would have bought HDFC cards since they are the best in their category. Let’s deep dive into their business:

- Starting with basics, a credit card is a financial instrument which gives you the power to purchase upto required credit limit even if you do not have money in your bank account

- So consumers tend to use credit card to buy their latest laptops, iPhones etc. by swiping their credit cards and converting their purchase to either EMI or paying them full after bill is generated

- How do credit cards make money? Majorly through 2 ways: firstly its via interest income and secondly via interchange and membership fee

- Interest Income: Some intelligent folks pay their full month due at the onset of the billing period and hence do not incur any interest payment. They are known as transactor.

- On the other hand, some folks with tight liquidity only pay the minimum amount due. Hence these folks shell out interest payments. They are known as revolver.

- On the top of it, consumers who purchase via EMI, also pay interest payments. They come under the bucket of EMI. So revolvers and EMI are interest earning receivables

- Apart from interest income, there is a subscription based income which is membership fee and annual fee. Thirdly there is interchange income

- Interchange income is basically the share which SBI cards get every time you swipe your credit card on some retail counter. This turns out to be roughly ~0.8%-1% of the swiped value. Here is how the backend looks:

- Interest payment is 46% of total income of 3656 cr in Q3 FY23. Subscription based is 26% and interchange is 28% of the total income

- Amongst the interest income, there has been a decline of 35% in revolver portfolio. Hence the management is taking two pronged approach: improving the EMI portfolio so that the loss at revolver makes up in EMI & increasing sourcing for <30 years of age and self employed who will contribute to revolver.

- Total receivables stand at 38626 crores out of which 61% is revolver and EMI and remaining 39% is transactor (which do not earn any interest)

- Spends per average card is 179000 annually which includes both retail and corporate spending. Cards in force stand at 1.59 crores up from 1.48 cr in previous quarter

- Total retail spends stand at 54000 cr and total corporate spends stand at 14000 cr. Here is how it looks:

- Regarding the health of the credit, stage 2 and stage 3 receivables are 6.1% and 2.2% of the total receivables. Out of the total stage 2 and 3 receivables, 4.9% and 64.2% are kept as provisions.

- Stage 2 used to be in 8%-9% range pre covid. Since it has been bought down to 6%, there would be lower credit costs in the coming quarter. The same has been voiced by the management in the concall

- GNPA is at 2.2% of the book and NNPA is at 0.8% which is at quite an acceptable level. Regarding the NIM profile, it is at 11.6% which is down by 0.7% due to increase in cost of funding. Similarly cost to income ratio is at 62% which is up from 59.5%

- The cost of funds has risen from 5.4% to 6.3%. This is mainly due to the fact that 65% of the funding happens via short term commercial papers. Hence the increase in repo rate is almost instantaneous in such cases

- SBI cards added the net of 1.63 million cards in Q3 FY23. Of this 1.63 million, 49% came from banking channel which is up from 37% QoQ. In terms of sourcing, more focus is given on <30 years and self employed since self employed contributes highly towards revolver category

- Given the high growth in receivables and cards in force, the credit card story is the long term consumption driven narrative which needs to be watched in greater detail to unlock the benefits. Given the huge difference between debit and credit cards, there is a lot of steam remaining to be exploited for credit cards

Here is the thread: https://twitter.com/manujindal2803/status/1622232871049240577

6 Likes

How revenue/cost model differ incase of cobranded credit cards. Do they share interchange fee with the partner?

So I recently came across this video where Nigel talks about the fact that RBI regulations prevent banks from listing their credit card business! Is it true? If yes, can someone share the link to the same. Thanks!

1 Like

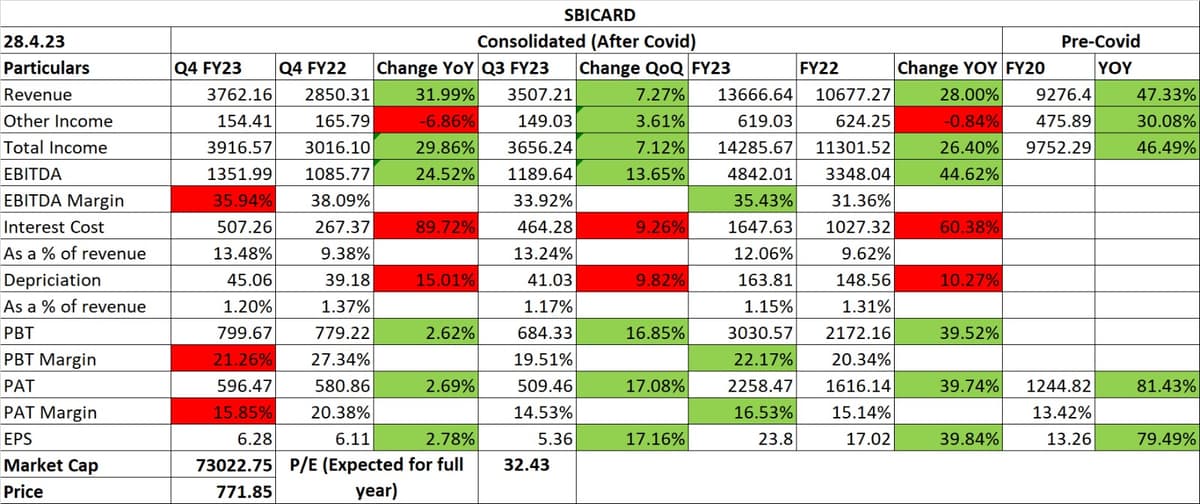

SBI CARD Q4 FY23 Result Update:

- Guidance: Cost of funds is expected to increase by 10-15 bps in H1 FY24. These are expected to reduce in H2 FY24. Margins will start getting better in H2 FY24. Credit costs will moderate gradually in the coming quarters.

- Spends conversion to EMI has been higher v/s the Pre-Covid levels that is driving the higher mix of EMI book. Revolver book is expected to witness a gradual recovery.

- Overall spends grew 32% YoY/4% QoQ, with retail/corporate spends rising 33%/32% YoY. The share of online retail spends stood at 57% in FY23. Spends in the industry is likely to grow at ~22-25% and SBICARD would try to grow higher than the industry growth rate.

- Brokerages have guided PAT for 23-24 to between 2800 cr to 2850 cr.

1 Like

Article in ET wealth on SBICARD:

- Will benefit from lower card penetration in India. Only 4 cards per 100 people.

- India’s young population and higher consumption, Robust Govt. Infra with strong growth in POS and Bharat QR Terminals, Govt. pust for Digitization, a growing e-commerce market.

- Despite UPI, credit card is still preferred for large ticket expenses.

- Long interest free credit periods and reward points continue to keep credit cards attractive.

- Cross selling opportunities for customer base from SBI Bank.

- High Investment in Technology.

- Strong retail & corporate spending is expected to provide growth stability.

Brokerages are giving TP of Rs. 930-960.

2 Likes

SBI Cards’ stock is showing all signs of a good largecap multibagger in the making, with the “x” factor being “linking of credit card to UPI” which I believe is going to be a gamechanger for the company. Although the company does not earn any fee income on low ticket transactions up to Rs. 2000 through UPI, this will be more than offset by sheer volume of higher usage of credit card for regular day to day needs resulting in higher percentage of revolver credit. This is my hypothesis, insight, etc. it remains to be seen what the future holds and time will tell whether I am right or wrong, but these are exciting times for investors who invest in the Indian growth stories!!

6 Likes

As of now we can’t link Sbi rupay credit card to upi.

2 Likes

Mr. Tejas, you are right about that. They will go live only by June 2023 as per the latest news. Source: SBI Card, ICICI Bank defer RuPay credit card on UPI till June: Report

Below is an Excerpt from SBI Cards and Payments’ quarterly conference call dated April 28, 2023.

“Mr. Rama Mohan Rao Amara: We are excited with the opportunity from the linkage of Rupay cards with UPI. Access to a larger merchant and hence customer base is good for the industry players. We plan to roll out the UPI and Rupay linkage over the next few months.”

Disclaimer: I am heavily invested in this company, so my views may be biased. Please use your own discretion before investing.

2 Likes

These are just customer acquisition tactics. Every new credit card is launched with super exciting rewards, cashbacks etc. Once they have got enough customers,they quietly downgrade the benefits.

1 Like

I am credit card user and I am using it for many years , still getting all as company promised on the time of card application.

I’m not a cc user but I read various cc blogs on internet regularly. And I often come across these kind of posts there where banks start downgrading CCs after 2-3 years.

1 Like

Thanks for sharing this info.

1 Like

Why is there such a huge difference between SBI Card spot price and SBI card futures price , this difference used to be around 2 to 5 rs but today towards the end of trading session it was 25 Rs it is a very big arbitrage opportunity as there is no dividend declared. Please someone let me know what I am missing?

1 Like

Yes, does anyone have any theory here

Also SBI Cards SLBM is quoting Rs 26 now

1 Like

SBI card enables Rupay credit card on UPI.

5 Likes

Have been tracking sbi cards lately I feel credit on UPI will make it very convenient and will make credit cards useful for even small value transactions, I think the revolves book will reduce as there is some customers who are mindful about proper use of credit cards, UPI can make credit cards mainstream but I do not think they will earn on it MDR revenue, I already have two SBI credit cards, I have many other bank’s credit card but I feel SBI card is the best really like their investment in technology, recently with their SBI cashback card they have reduced MCC on which 5% cashback was applicable, also I like SBI’s customer onboarding journey, they have a good process, currently with the devaluation of majority of Axis bank credit cards and reduction of airport lounge access I am seeing players avoiding cash burn, so in all I feel revolver should reduce, credit card new users as well as spending rise, fee income should increase to in proportion, valuation is much more favourable now, India in my opinion should be very high growth also if they are able to maintain GNPA it should be a very good stock in my opinion have taken entry.

Any anti- thesis and risks someone can point.

I am a credit card user of SBI and many other banks can provide any feedback for comparision purposes if required, Happy to help.

5 Likes