SBI Cards & Payment Services has tied up with Fabindia to launch an exclusive co-branded contactless credit card - Fabindia SBI Card.The card is designed with curated benefits and privileges to offer a rewarding shopping experience to its premium customers. The card comes in two variants - Fabindia SBI Card SELECT and Fabindia SBI Card.

SBI Cards is planning to enter the super-premium cards space with something called Aurum, a black card with a gold streak in the middle. Might just be invite-only, given some of the data points I've seen so far. (Don't @ me) pic.twitter.com/UaVF4SaGh5

— Ajay Awtaney (@LiveFromALounge) January 14, 2021

They are also launching a super premium card called Aurum. Its a black metal card targeted at people with 15lac+ spends on the card. The website is : https://aurumcreditcard.com/ . They are marketing this aggressively, had sent a free gift (https://sytara.in/) before I received a call to upgrade to this new card.

3 Likes

I am having a basic doubt here. With more UPI transaction, can the usage come down. Credit cards make most of their money only from the defaulters. How long guys can borrow at 36% and survive. Further, the trend in Microfinance is also increasing. What is USP of credit cards for guys to buy them

1 Like

I have had this debate with others too! 50 day interest free money, reward points, perks. Not everyone borrows from credit cards. 0-interest EMI offers from credit cards (I know debit cards have also started providing the same), but it is also an aspirational thing to own a credit card. Co-branded cards (I use SBI’s BPCL card) also have a huge runway because of the perks it offers.

A credit card has its purpose and place.

If I were a salaried individual and have good credit score, I could get a credit card with good credit limit. The credit stays in the card until the expiry of the card which obviously is a few years. There could be emergencies and instances where I will be in need of money which I many not have any in my bank account, and I could not ask anybody, or if I am in another city where I know nobody, I can use this card in times like these.

Not to mention the need of credit card when purchasing from websites which are located outside India, which do not accept Paypal transactions.

I could even increase the limit. The onus is on the bank which issues the card, I don’t need to have money in the account at the time of using the card. Who wouldn’t want one?

A credit card is like a reserve, it may never be used but it is a unique source of borrowing, if a specific need arises. They sure have their place, at least for the time being.

3 Likes

UPI in its current form is not a threat to Credit cards. Since banks cannot earn any money from transaction charges and the current form of UPI is debit.

But when UPI is matured enough to have a credit card like model and transaction charges are enabled, then all banks and customers can easily move to UPI. This will not affect other credit card providers. But SBI Cards is at the mercy of SBI for routing this business to SBI Cards instead of having it in its own book

1 Like

4 Likes

Quarterly results came out, just before the market close. Looks decent, at first glance

Reserve Bank of India (RBI) data showed that overall credit card outstanding remained stable at ₹1.1 lakh crore. September credit card spends surpassed ₹80,000 crore, crossing the monthly peak spends seen in March of ₹72,300 crore.

1 Like

Considering the BNPL concept picking up pace, this opens a new avenue for revenue.

1 Like

New Card Product Launch

b3ba1501-3ae7-4515-b8f1-1710f8fa4fa8.pdf (568.6 KB)

Credit cards are one of the most profitable business, say for any bank which has high interest rates.

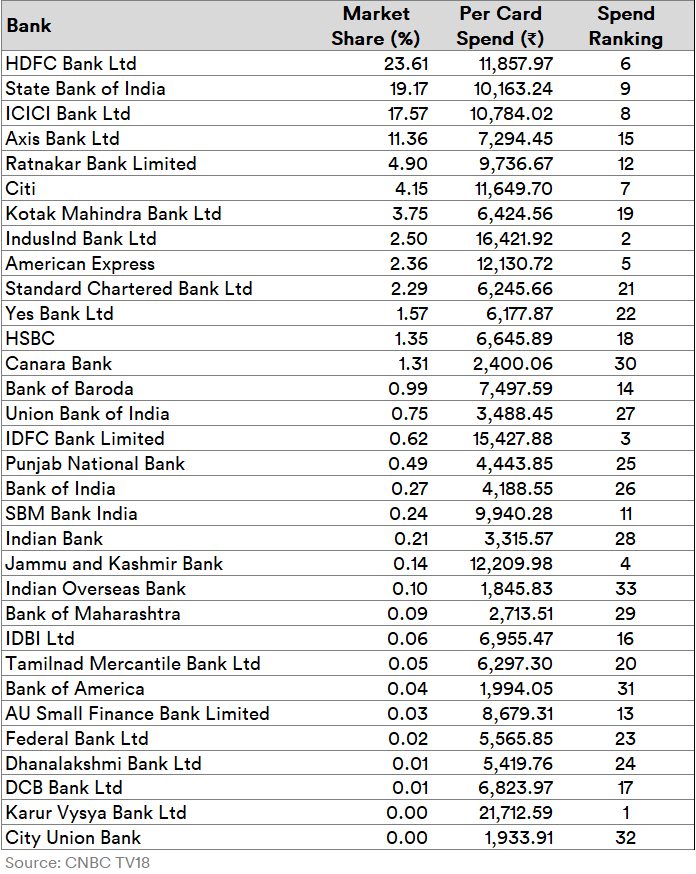

A key metric in credit cards is per card spend and what may surprise everyone is that HDFC Bank is not the market leader here. It is Karur Vysya Bank, which leads per card spend in India.

In fact, Karur Vysya Bank’s per car spend is over 2.17 times the industry average and more than 1.83 times of the market leader HDFC Bank.

From Karur’s point of view, it is the most profitable business.

Private lender IndusInd Bank also derives significant business out of its credit card segment, followed by the latest kid on the block in the banking sector i.e. IDFC First Bank!

Data As per August 25th, 2021

Source : Credit Cards In India: Hdfc Bank Leads In Market Share But This Lender Beats It In Per Card Spend

Disc : Invested in SBI Cards from lower levels

7 Likes

Can Rising buy now pay later companies be a threat for credit card industry ? Any views…

I think no, most of the people I know pay through credit card for gaining reward points and 45 days repayment period. Pay later services offer none.

The only real threat to credit card is I think UPI due to its no MDR charges (merchant loves this) and convenience for customers

1 Like

If RBI grants permission to CC industry that credit cards transaction through UPI that will be game changer.

Use BNPL and enjoy 15 days credit period. Then pay the bill using CC and enjoy another 45 days.

But its difficult i believe for BNPL to disrupt the CC industry mainly because of the low costs of funding and the balance sheets which banks have.

1 Like

Which BNPL your talking about? Isn’t it violation of RBI rules that says credit can not be cleared using other credit. I have used lazypay and it doesn’t allow clearing dues from credit card citing RBI restrictions. Also CC charges heavily on transaction and assuming that Pay later companies makes very meagre or nil profit in payment services, it can’t be sustainable for long term to accept credit card repayment. See how wallet (Paytm, mobikwik) levy heavy convenience charge on loading money by CCs

1 Like

are you sure? both lazypay and simpl allow payments through CC

they have stopped it from now on

CC uses either VISA, Master or Rupay as payment gateway, why the money will be made to flow through yet another gateway (UPI)?