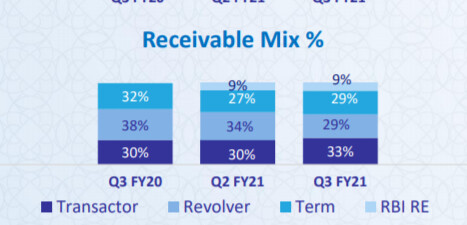

There is a difference in the RBI RE book between SBI Cards & RBL Banks CC book.

Below is RBL Banks CC book status-

Only 0.7% of the book is restructred.

Now look at SBI Cards book-

SBI Cards has been on the aggressive side while accounting for NPA’s. Also, when you are going to have 3 MD’s in 6 months its more like playing passing the parcel.

I would have expected Carlyle to put a more competent ‘private sector’ type management in place. Instead, it is full of people from SBI.

New CEO is also a career SBI man.

Mr. Rama Mohan Rao Amara is a veteran banker, with a successful career spanning over 29

years at the State Bank of India. Prior to taking charge at SBI Card, Mr. Rao was the Chief General

Manager, SBI Bhopal Circle, where he managed two key states MP & Chhattisgarh.

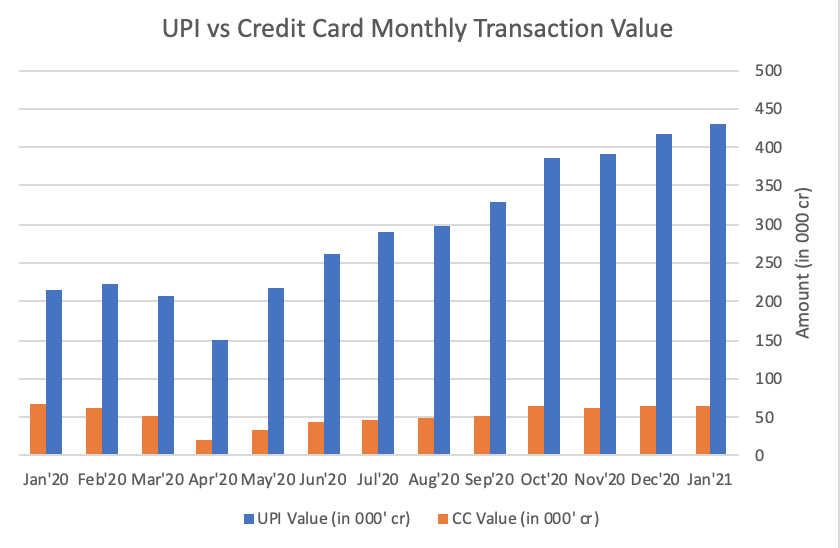

How do people think of UPI vs Credit Card data: The data is shocking. UPI is growing at 100%+ YoY even in FY21 whereas credit card spend is yet to cross its FY20 Peak. Isnt this disruption at a massive scale? How do we make a case to invest in SBI Cards at all looking at this data let alone paying 70 PE? I am not buying the argument that credit card and UPI dont compete with each other. I use credit cards and UPI both and in the last 12 months, I have gone from using UPI for <10% of my spends vs today >50% mainly led by convenience.

Those who have good credit scores will still go with credit cards. There are two benefits - accumulation of points especially if you are using premium cards like Diners Black/Infina, etc. 2nd you would maintain your credit score which could be helpful at some point in time. Continue to use UPI in case sellers don’t have a card option. Essentially forget the credit part of the credit card.

I guess high value transactions in upi are mostly peer to peer, I am not sure if above stats contains those peer to peer transactions value or is it plain consumer to merchant value, In my opinion upi has mostly replaced cash and fund transfers via imps/neft and not credit card spends. Atleast I continue to use credit card where I have used credit card before upi be it at fuel stations, e-commerce. But upi intergration in e commerce apps is very seemless and very snappy compared to credit card payments which invloves inputting credit number and waiting for OTP

My Two cents on UPI Vs CC

UPI gives me convenience. I need to have that money in my account to use it.

CC gives me flexibility (subscriptions etc). I didn’t have that money in my money, still I can use it.

If ever, UPI gives me credit facility too then… its a story !!!

Note : Invested.

Fair enough, but I think that may be more true for larger transactions rather than smaller ones. For smaller transactions, maybe the convenience of using UPI outweights the small quantity of rewards obtained?

Good point! Unsure if it is at all possible to get more granular details on UPI use cases; but I would not be surprised to see most digital spends: e-com, food delivery, etc being dominated by UPI. As these are likely to grow disproportionately and take a larger share of the customers wallet, could they be headwinds for credit card business?

Dont you think this is inevitable? If we take the example of China, Alibaba first started with payments before branching out to credit, insurance, etc. Surely, the domestic firms will do this too; especially since payments clearly seems to be a structurally non-profitable business.

Well actually, after RBI actually ends up implementing its new rules, this may not even be possible. In any case, recurring payments on credit cards are only a 2000 cr monthly spend, irrelevant in the larger scheme of things. See below article:

https://www.business-standard.com/article/current-affairs/your-automatic-debit-credit-card-payments-likely-to-fail-from-april-1-121033000550_1.html

These are my views on the above discussions, My view is for SBI Card and overall card payments future prospectus:

-

I agree UPI is rapidly increasing, but NPCI mandated to process a maximum of 30% of the transaction volumes starting Jan. 1, 2021.And this is a problem since PhonePe and Google Pay currently hold about 40% of the market, each. Meaning, they have to limit their operations soon enough or there will be consequences. Read this article for more details : (Why Google Pay and PhonePe will have to limit operations?)

Also, UPI transfer has capping limit for per day and per bank basis -

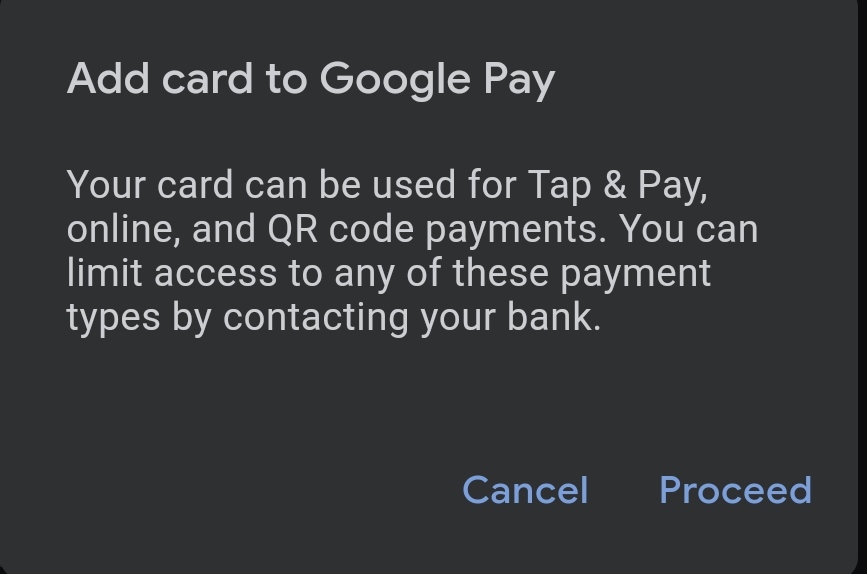

Recently few months back Google pay allows certain banks like SBI, AXIS, KOTAK, HSBC Credit and Debit card to link with their platform to pay the online and offline businesses, so that the user can pay directly with their cards. This is a win-win situation.

My assumption : In future, if they allow to transfer the money from card instead of our bank account in Gpay/Phonpe by charging some extra fees, so people can transfer the money from credit card during emergency or any urgent necessity which will also be a game changer and win-win situation. -

UPI is just a mode of payment where companies Gpay or Phonepe are mediators of banks. They are not standalone unless a bank is involved. Also they can give a minimum cashbacks and if they started giving more cashback it will affect their margins. You can already see the offers are drastically reduced when Gpay started to the current scenario. But banks on the other hand giving awesome offers and reward points and many people buy using their SBI or ICICI or AXIS or CITI credit card during Amazon or Flipkart sale. I noticed many time SBI gives 10% discount offer many times in both Flipkart and Amazon(in fact every month some offers are given), also SBI card gives exclusive cashback for the more fan following mobiles like Oneplus/Apple.

-

I jokingly used to say to my friend, in Big Bazaar there are more SBI card employees than the Big Bazaar employees. SBI Card is present almost in every big malls, Big Bazaar etc places and tremendously acquiring customers(you can see the customer base is increasing from their financial report).

-

Crypto is game changer and even VISA and other top banks issuing cards even for crypto currencies. So as the new payment evolves they(card companies) tend to make a win-win situation rather than defeating them. So even SBI Card can start supporting crypto and issue card for crypto (if our government allows).

Note : These are my thoughts and assumptions which may or may not happen.

Invested and hence biased

I hold multiple credit cards from different banks and credit is not the only thing that I find useful. These days there are various players and mode like OLA postpaid, Amazon Paylater, PayTM postpaid, debit card EMI, Lazypay, Bajaj EMI card, sezzle, etc. for the credit part i.e. spending without having funds in bank account.

Credit Cards have given me airport lounge access, airport meet and greet, overseas medical insurance, Air travel insurance, purchase protection, reward points, hotel status, airline status, additional discounts, etc. without any additional cost (apart from the annual fee, if any) or at very highly subsidized rate.

UPI offers convenience and I use only where cards are not accepted. Pecking order for me: Credit Cards > Dedit Card > UPI > cash.

There is a caveat to this. iOS doesn’t support, only B2B transactions and also the merchant should have a POS machine for it to work like charging credit card to pay UPI QRs . Please correct me if I’m wrong or things have changed now.

Disc: Not invested.

Good news for SBI cards

I did not find in my google pay account to add debit or credit card in the payment option to pay any merchant through UPI mode. There are some apps which provide credit line to pay through UPI but there is some charges which now customer has to pay upfront .

Is this big negative ? Or generally PE holding is finally suppose to come down now or sometime in future .

First thing, As per SEBI rules, promoter holding should be brought down to 75% after few years of listing. Since SBI and CA rover are promoter with more than 79% stake now, they have to bring it down. Even during IPO issue, it was CA who sold most of their shares to raise money.

Second, These Venture capitals and PE firms are not here to be the permanent promoters of any companies. They want to make huge profits and exit after some years for most of the companies.

Lastly, Nowadays I can see in many VP threads, there is much noise even if the promoter sold 0.5% or 1% also people posting and asking if it’s red flag or negative, always remember that, As long as the company Fundamentals remain intact and nothing changed, there is no need to worry. Even if the promoter holding is zero in quality companies like ITC, IEX which are regulated and professionally managed, there is no need to worry about sbicard which is country’s 2nd largest credit card company and backed by country’s biggest lender SBI.