Thought to chime in as I felt somethings needed to be clarified.

Taking the liberty to say I have been in the payments industry so would know a little more nuances.

RBI Statistics

I track this for almost 8+ years. Please note CIF (Cards in Force) means how many cards were ever issued by an Issuer bank. It has nothing to do with average transactions made in a month. There is a concept of activation rate. Meaning say ICICI issued 100 CIFs but activation is 40%, so use 40 cards to calculate the avg spends, swipes etc. Dont use CIF as a base. This is a common misconception even amongst business media when they report. Before DeMon more than 50% of debit cards issued never saw a single txn in their lives. They were received and locked up in cupboards at home.

Unfortunately activation rates is not public info. But in my 10 years of seeing this my ballpark estimate is 40% for credit cards and less than 15% for debit cards for merchant transactions. Card networks have amazing data on such things. I believe in the US a MasterCard even sells this data to funds. Activation rates will vary drastically amongst banks. A Citibank or an Amex will have very high activation rates but a PSU will have very poor rates.

UPI

UPI payments have completely overtaken most forms of payments in the country. But the business model to profit from is iffy imho. So it is table stakes to be in it but I dont know how companies will benefit other than cross sell component.

Instant card issuance

Technically it can be done today also. Credit lines are approved in less than 1 minute (there are live examples already in our country) and one can even get a virtual card immediately if physical plastic is not available. I myself have built this product few yrs ago (for prepaid in nature at that time).

Customer Service

There is Amex and then there are the rest. Full stop.

Let me know if folks have specific queries.

Please note I am not invested in this.

Thanks for your insight! I have always wondered what could disrupt credit card and then we got UPI. Seems SBI has started taking action on this front. Do you think SBI can pull off as per the link below ?

Just one question, if CIF were not be used , but indeed let us take Cards Activated as a metric, will they average spends not increase since denominator is decreasing. If that s the case, we are looking at Rs 3.2 lacs/ user/year kind of figure. Is that accurate? Seems a little high…

See the assumptions with 40% active rate for CC and 10% on DC for April data.

The CC looks in line with the 3 txn metric I see. Though I think DC active rate should be even lower at POS than what I have assumed here.

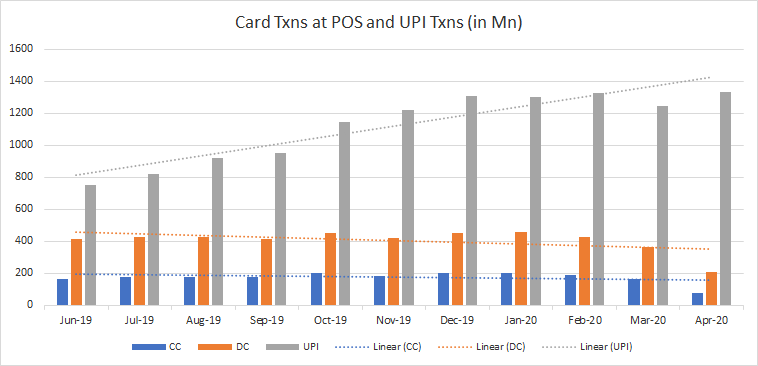

Well CC & DC in terms of number of txns have already been disrupted imho. Look at this below. I need to update till June. But I think the trend will be same. Though June will have bigger DC and CC txns as much as Jan I think (lockdown over).

I saw this notification on the competition to NPCI. I am keeping a keen eye on this. But I have seen NPCI since 2011-12 onwards they have really done well in these 9 odd years. A lot of experience they have in my opinion. Let us see. I would be only guessing if I try to make any predictions.

Disruption in the business model on the horizon. Especially relevant in India as our young aspiring new to credit population in the coming decades could potentially skip the credit cards as we did with landlines. China is an example of how new different financial ecosystems have developed around e-commerce while the West is an example of how an already entrenched ecosystem makes it hard for new ecosystems to develop. We are probably somewhere in between. India 1 is well penetrated with financial services and entrenched in the current ecosystem. While India 2 has openly accepted UPI, Rupay and the volume game has shifted. I am not saying CCs will be completely wiped out, disruption is rarely so black and white when the difference in innovation is less than an order of magnitude better. New forms of credit availability in e-commerce will be mostly digital, with limited use of that credit in the outside world. That is where the CCs will continue to service the customer. But we all know e-commerce platforms are already and will form a bigger part of the customer wallet share in the future.

Crazy interest rates on defaults are potentially a weakness for CCs, one can study the business model and comment whether these are a feature of the credit product due to default rates and unsecured nature or are these a pricing power feature. If the case is latter, there is definitely room for competitors to save transaction fee and provide credit to their customers directly for their platforms.

I did base level research on klarna and afterpay when buying SBI cards. Their model is now leading to losses which will scare off future investors from investing in companies adopting the same model. How they work is : The customer chooses them as the payment option on e-commerce and chooses 4 interest free installments. Klarna/afterpay pay the full amount to the retailer and charge a transaction fee which is even higher than the usual card transaction fees. So the retailer still has to pay this and doesn’t benefit. The customer has all the power. Apart from a decrease in credit rating klarna/afterpay don’t have any sort of protection. Credit card companies charge high interest so that even if a high percentage of customers turn into npas the high interest covers for these npas overall. Klarna/afterpay just go into losses or charge late fees etc which works out similar to what credit card companies do(so it’s arguably not that beneficial to customers either). This kind of model isn’t sustainable since the npas aren’t protected and will keep rising. First half of this year klarna has gone into record losses due to npas going through the roof. Investors are now very wary of this model. Regards SBI cards, they are almost fully digital now so the use of actual physical cards isn’t an issue . Corona has made them pursue digital even more so the physical debate of credit cards isn’t really important. They charge the same transaction fee to retailers so retailers have no reason to shift to the likes of klarna etc either. SBI cards survive npa issues due to their high interest rates and in a country like India the npas are much higher compared to counties like the USA where people are used to working with credit.

Disc: invested. Biased and hence may have only seen what I wanted to see

This is my take, according to me there is nothing which fintech can do but Bank can’t (but yes, it may take banks sometime to catch up with tech). The key stumbleblock in fintech lending is access to low cost funding which is relatively easy for Banks. I do not think RBI is going to let fintech players accept deposits, they will continue to rely up on investor funding or borrow from other lenders to meeting their capital needs - this makes it difficult to make a scalable business model. Many fintech looks futuristic in their pitch but seldom grow into the size with respect to available market opportunity. Future will be decided by data & partnerships - for ex: there isn’t anything which prevent e-commerce player to have an exclusive partnership with a lender to offer credit for purchases. Another key to note will be how the UPI as a platform will evolve in future with the amount of customer behavior accumulates. This can be an extension for EMI on Debit card facility. I honestly don’t think a standalone fintech can cause massive disruption to banks or pure play card players like SBI Cards in credit space but Banks themselves can cause so much disruption to CC providers.

Agreed. Startups like klarna/afterpay got a lot of investors pumping money into them at the top of the credit cycle ie around 2015 to 2017. Everything look d Rosey due to that. Now that we have experienced a debt cycle due to Corona it’s very obvious how risky their businesses are and I don’t think we LL get similar funding for these kind of startups anytime soon. At the end of the day only banks can provide credit safely. I agree with that too. The likes of UPI etc work perfectly with debit. But there is no way the likes of Google pay etc will launch credit on their own and risk npas etc. They’ll rather just tie up with banks for the same(who already have their own interests in credit cards). What we are more likely to see is UPI etc working via strategic partnerships with credit card companies and banks( and SBI cards has recently started doing so with Google pay). This combined with them making digital a priority and them being the only listed credit card player makes SBI cards the current best fintech bet and disruptor themselves imo.

Not even close to expectation and the current valuations do not justify the earnings at all. Hoping commentary today at 5 pm will help clear the reasons why.

I believe the profit is down due to there being a provisioning on doubtful debts which I suppose is not a bad thing. Operationally their performance has improved actually QoQ, if I read the details correctly.

More in depth analysis welcome from senior members:

Disc : Invested from far lower levels, added more today so could be biased.

Kitchen sinking at its best after the takeover of the new CEO. Why should he carry the baggage of the past. What spooked the market is elevated GNPA despite escalated provisioning. Sure valuation is out of reality. It seems they have taken large interest reversals as moratorium is over.

SBI cards reported that its gross non-performing assets (NPAs) rose to 1.4 percent in the April-June quarter to 4.3 percent in Q2. That is a huge spike in bad loans.

That’s not the real shocker. The company has not classified any account which were not declared NPA as of August 31, 2020, as NPAs, following a Supreme Court (SC) interim stay. On September 3, the SC had said: “Accounts not declared NPAs till August 31 are not to be declared NPAs till further orders."

If that portion is accounted for, the company’s gross NPA would have risen to 7.46 percent.

Disc: No investments, just the sound of PSU management in unsecured lending doesn’t seem the brightest idea to me.

Mgmt recognised that more than 7% as NPA due to SC ruling.

Had this come in effect, this quarter may have plunged in to losses due to higher provisions.

With just 1.5% NPA in Q1, is it the mgmt failed to realise the real picture during lockdown or the real effect of it is taking now, with ppl losing their jobs and things are coming out of closet.

Would like to have opinions of others as well.

Disc : Invested.

(may buy more, if have more clarity)

Imo the main issue here is that management sounded bullish post Q1 and said that going forward things would be better and there was no hint of gnpa increasing to this level. So 1 of 2 things happened

They did not tell the shareholders the full picture on purpose

They did not estimate the full picture well enough

I’m not sure which of the two is worse tbh. I’ve lost a bit of confidence in them and I honestly don’t know what to expect anymore for the next few quarters. The good news is that they are getting higher cards in circulation and spends but if the GNPAs keep racking up then that’s all for nothing since at some point in the future everything will have to come out. Personally can see a few muted quarters and a very bad quarter post moratorium. Long term they will obviously survive and will thrive but in the short to medium term a rating of 70+ PE just doesn’t make sense to me.

Disc: invested(but trimmed a lot yesterday). Will re invest when all the cockroaches are out post moratorium which will provide a huge buying opportunity since these issues will be a thing of the past in normal times.

This is getting serious not just for SBI Cards but economically as well :

There are only 57 million credit cards in the country held by top 10% of households by income. If their defaults are increasing alarmingly, as SBI cards result show, are households into serious financial problem?

Would like to have thoughts from other investors as well.

Credit Card is a rather strange lending product unlike other type of credits. One key difference is the limit it offers, which could be 2x-5x or even higher than one’s monthly income - this is where the problem starts especially during bad times. Other side of story is about how easy it is to come back to a non-default status from default, the person will need to only pay the minimum due + penalty and still, they can carry forward the balance to next ‘n’ months. Imagine the same for Personal Loan (person will need to pay all the pending installments in full + penalty)

SBI Cards have a high share of New to Cards segment (~30%+), this looks fabulous on paper and starts we followers to think about the unlimited opportunity lying ahead for them. First time Card holders segments can become volatile during the initial months (learning curve involved in understanding the product itself takes time).

Hope that they could recover some part of the 7%+ NPA in the coming months or perhaps convert some of those bad balances into loans etc. Or in a worst case scenario, it is possible that the NPA may very well go up from here as well, the real impact of the pandemic is yet to visible!

The issues are many which did not get enough traction recently and I too missed those signals

SBI cards has been growing quite aggressively just before this pandemic or IPO. I think they were waiting to be hit hard.

I believe many are waiting for a better restructuring deal from SBI or waiting to be chased by the recovery agents.

I don’t think long term fundamentals change materially since most of credit card holders can’t afford to dent their credit history. It is matter of time folks will start paying slowly after December.

Disc: had taken small position during Q2 despite being skeptical and exited immediately after the result.