Does the trading in shares of SBI Cards by SBI Life Insurance (categorised as Promoter Group) before declaration of results not come under insider trading. They informed disposal shares on 6th, 7th and 8th May. How they are getting away with this.

No they are group companies. SBI Card is not subsidiary of SBI Life. I understand that only promoter company/individuals will qualify for insider trading

1 Like

Some Thoughts On SBI Cards-

- I think that SBI cards should not be looked as a pure lending business. Think about it, what is a lending business? It’s a business wherein you give out money to people and that most of that money is actually pending collection at the end of a period, be it a quarter or a year.

- But if one looks at SBI Cards, it lends huge sums of money, but only a fraction of money is actually pending as due at any end of period. In FY20, it lent Rs130,915 crores in form of credit cards spends, but only 18% of these loans were pending due at the end of the year, about Rs24,141 crores. And this is true for any period for SBI Cards.

- It’s more like any other business wherein you have sales (spends in case of SBI Cards) and you then you have some debtors (receivables in case of SBI Cards) whom the business has offered credit period of 30-45 days. The debtor is supposed to make payment within this credit period and if he pays it, it is business as usual.

- Similarly, in case of SBI cards, if card holders make payment within the credit free period of 30-45 days, they are not charged anything.

- In case of normal business, the business earns money by selling goods and in case of SBI cards they make money from spends (which is sales for them) by earning a fixed rate of 1.5-1.8% of spends and some other fees, charges etc. And both these transactions in case of both these businesses results in 30-45 days of credit free debtors. This normal business makes up for more than 60% of SBI Cards Business (will explain how later).

- Where things turn different for SBI Cards is that, if the debtor does not pay within the credit free period it becomes a loan; wherein SBI Cards can charge enormous interest to the debtor. And this is the risky part of the business.

- For 9MFY20 (using 9MFY20 data to avoid any Covid related issues in numbers), SBI Cards, revenues were Rs6843 crores, of this 50% (Rs3241 crores) was towards MDR, Fees etc; the normal business. Remaining 50% was from interest income, which is the 2nd part of the business, however this 2nd part of the business of lending money also involves bad debts so net income from this segment is actually Rs2319 crores (Rs3421 crores – Rs1102 crores Bad debts); and this is how that 60% in point number 5 came.

- This lending part is very risky in my understanding because the leverage here is actually 100x. Yes 100x!.

- If one looks at the financials of SBI Cards, the Bad debts are actually more than or equal to company’s profits. Plus, the impairment losses are just 1% of the spends (your sales here), so if just 1 extra percent of your sales goes bad, the company actually starts making losses.

- A lot of people are also confused as to how to value the stock, whether to use Book-Value Multiple or a P/E? I think a book-value multiple is not suitable here as a good part of business is not actually lending. So all those who crib about why is it trading at 10x plus BV multiple, even though Bajaj Finance is trading at 4-6x book; P/E is a better valuation metric here.

- But one needs to be fully aware of the level of risk here; plus, the company lacks transparency in terms of their risk disclosure and is more about showing off their growth prospects.

(Just my thoughts on a different view on the company; not to be taken anything other than that)

31 Likes

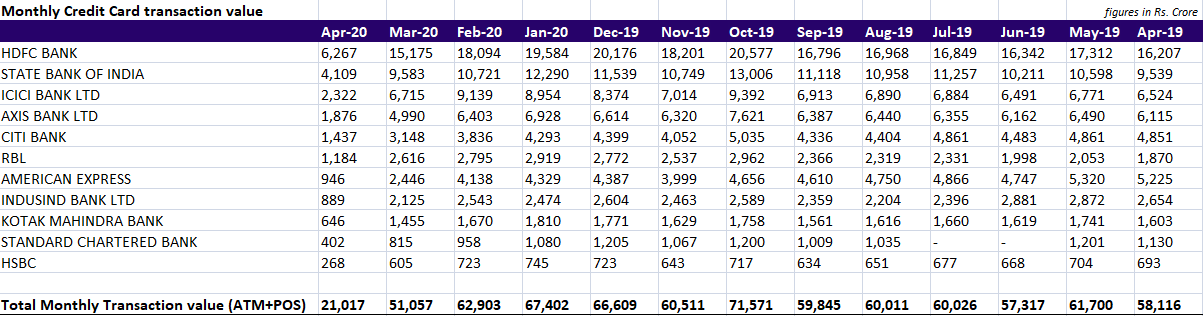

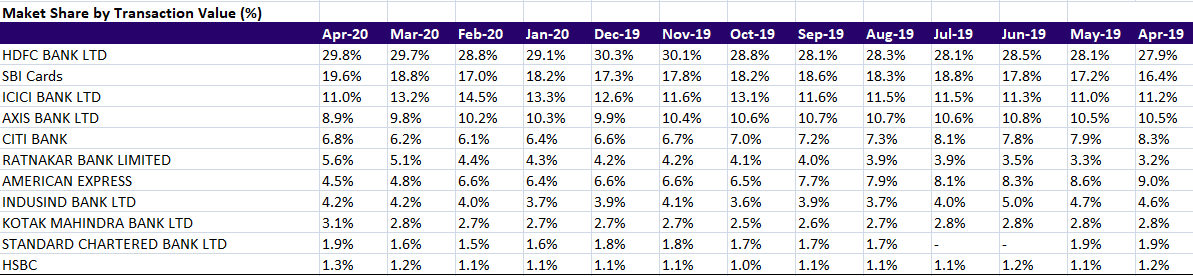

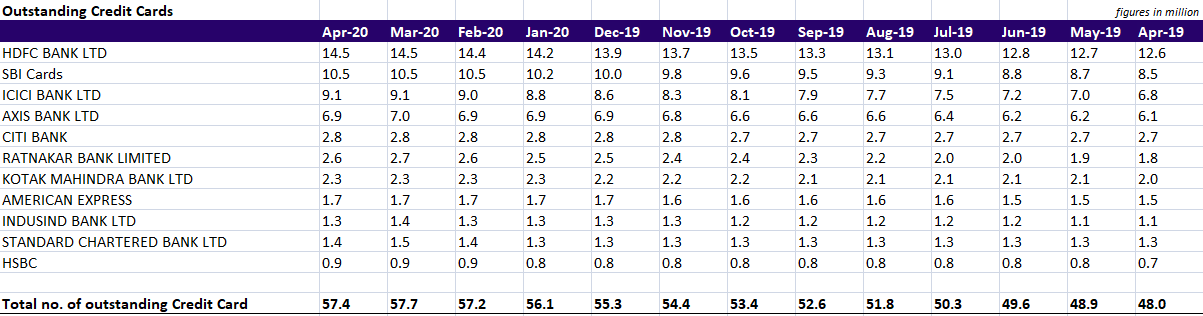

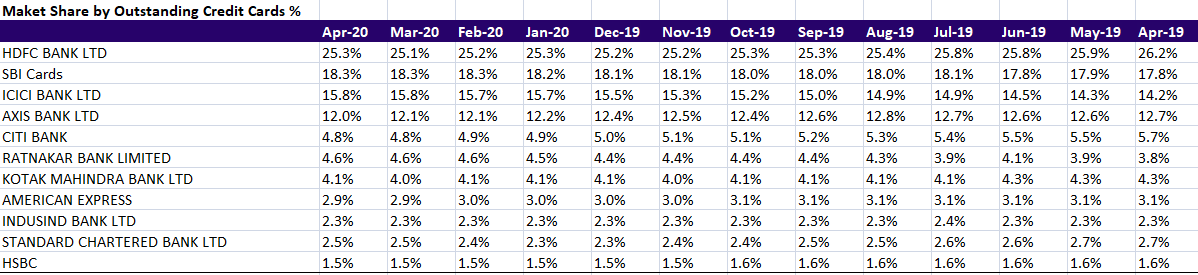

India Credit Card companies (Growth metrics across last 1 year)

-

HDFC Bank leader by a wide margin

-

ICICI & Axis stagnant/declining market share by transaction value

-

SBI Cards increasing volume as well as transaction percentage

16 Likes

Results are out. Revenue(excluding other income) and PAT for Q1 FY 21 is better than Q1 FY 20 even with almost half of the quarter in lockdown. Not gone too deep into it yet but overall the result looks fantastic. Got in around 500 and will gladly hold

what is the source of the data? can you please share?

Thanks in advance

You will get all the data from RBI website

2 Likes

Participants:

- Bank of America

- Prabhudas Lilladher

- Macquarie

- HDFC Mutual Fund

- Enam

- Aditya Birla Sun Life

- HSBC

- Ambit

Business Overview:

- PAT at Rs 393 crore vs Rs 346 crore YoY

- ROAA at 6.3% vs 6.5% YoY

- ROAE at 28.3% vs 36.1% YoY

- Capital Adequacy Ratio at 24.4%; Tier 1 at 20.1%

- Card-in-force at 1.06 crore vs 88 lakh YoY, up 20%

- Receivables grew by 10% to Rs 23,330 crore

- Cost to Income ratio improved to 47.2% from 53.6% last year

- GNPA has improved to 1.35% vs 2.68% YoY

ConCall highlights:

- Spends are back to more than 75% of pre-Covid level

- SBI Card has witnessed strong rebound in new customer acquisition; recently launched video KYC

- Company has added 80,000 new account in May and 180,000 new account in June

- Market share in terms of card in force (CIF) and spend has improved. Market share in terms of CIF has improved to 18.3% from 17.8% YoY; market share in terms of spend has also improved to 19.6% from 17.2% YoY

- Accounts in moratorium has come down to 1.5 lakh in June 2020 from 12.5 lakh in May 2020

- Moratorium amount has been reduce to Rs 1,471 crore in June from Rs 7,083 crore in May

- Field collection activities have largely restored

- Company has repaid some of the high cost long-term and short-term borrowings and replaced it with low cost borrowings, Cost of fund for the quarter was 6.6%

- Overall finance cost for the quarter was lower due to Lower interest cost and lower utilization of credit limit

- SBI Card has increased its field workforce from 4,200 to over 8,000; tele workforce have gone up from 1,100 to almost 2,000

- Company has taken many steps to reduce operating cost and other expenses

- Revolver percentage has reduced to 45% in June from 49% in April and May; pre-Covid revolver was 38% of total receivables

- Weightage (in online) of Category 1 (Departmental Stores, Fuel, Health, Utilities, Education) has increased to 88-90% from 75-77% as this segment witnessed 23% growth from pre-Covid level, while Category 3 (Travel agents, Hotels, Airline & Railways) has declined sharply

- Weightage (in Point of Sales) of Category 1 has increased to 58-60% from 53-55%. Weightage of Category 3 reduced to 1-1.5% from 4-6%

- Transaction trend has been shifted from high ticket items to lower ticket high transaction

- SBI Card ran some program on Amazon and Flipkart for consumer durable goods; 80% customer purchased through EMI

- Average duration of EMI is 1 year

9 Likes

Quick question. How exposed do we feel SBI cards will be to the moratorium overhanging all financial institutions at the end of the year. My investment thesis was due to the fact credit cards are used for smaller ticket items ie not bikes/cars/houses and also since there is a high interest on late credit card payments people Moratorium wouldn’t be a huge issue. The fact Moratorium has come down from 12000 crores to 1000 or so crores in the recent result shows this too. However, do you see this being an issue over the next few quarters hence leading to a price ceiling on SBI cards in a similar manner we’ve seen with other financial companies? My thesis was that due to the aforementioned small ticket items they would be a bit immune to this and they seem to have a high enough capital adequacy ratio to deal with anything thrown at them so even issues would be temporary thus clubbing them with other nbfcs/banks etc would be wrong. Hence entered at 500 with it as one of my core portfolio stocks. Just double checking that my investment thesis was correct and if not I need to decide whether to trim a bit at present. Cheers

2 Likes

Seems a sensible investment thesis.u also entered at a great price with big MOS. all points mentioned by u for investment seems valid. views invited by others also who track it

One area that might get ignored in such discussions is the kind of support provided by credit card companies. As far as customer support goes American Express is in a different league altogether. My experience with SBI has been less than satisfactory and I get the sense they still do not understand how to run a proper business. They of course have the advantage of distribution but that is because most people who open a bank account are pushed a card. The data I would be interested in is what is the average monthly spend per card and how many of those cards are actually active.

3 Likes

That could be part of the reason for making Ashwini Kumar the new MD and CEO. He has been in charge of SBIs US operations for a while now and I’m assuming they have put him in charge to replicate the way credit companies run in the USA since that is the model they should aim to replicate long term especially since all credit cards are already a part of life in the USA Vs India where they are just entering the general conscience. I liked Hardayal Prasad but I think he did the max he could. He has set up the entire growth cycle and that’s all they’ve been concentrating on and this was evident eberytime he spoke. I think Kumar will now streamline everything to ape the operations of the US but Time will tell since it’s just speculation atm but I am really looking forward to hearing him speak post Q2 results and see what direction he will head the company in

3 Likes

Apparently the Current Amazon sale surpassed the Diwali sale from last year. https://youtu.be/tQhwv_C1O2s

Sbi card was present for most products that I saw and this must have given them huge sales and visibility. Consumer spending has definitely had a huge shift towards online and it’s been fast tracked by corona and sbi cards could be in for a bumper quarter. Next quarter we have diwali too so this won’t be a one off. Overall owning this script could be a brilliant way to capture the overall consumption story in india.

2 Likes

SBI CARDS JUNE STATITICS

NUMBER OF CARDS OUTSTANDING JUNE 30 - 10602103

NUMBER OF TRANSACTIONS ATM - 68781

NUMBER OF TRANSACTIONS POS - 24651496

VALUE OF TRANSACTONS ATM - 26.90 CR.

VALUE OF TRANSACTION POS - 8670.94CR.

SOURCE - RBI

Summary

This text will be hidden

2 Likes

This is intrsting share.

So the Avg amount transacted on ATM comes out to be Rs 3910.

& on POS is Rs 3517 (I am assuming it also includes online payments using cards).

Need to understand does the POS also includes EMI payments. If this amount is including EMI, then it looks the transaction size has reduced.

Even the Avg, ATM amount is not that high. Its more like emergency cash withdrawals.

Disc : Invested in Satellite portfolio.

I’m getting a bit worried about the valuations. Current TTM at rs. 830 is 85! Even if sbi cards gets 2000 crores net profit this fiscal year their PE will be 40 at the current price. So we are basically hoping for a minimum of 500 to 600 crores profit each of the next few quarters and with the covid and moratorium overhangs no less. While I’m confident regards the company doing well I’m not sure regards the valuations and what the upside is from here this year. Is the market looking at it as a fin tech company instead of just a finance company and hence comfortable giving it high valuations similar to the likes of Affle etc or will the PE revert to mean if results aren’t extraordinary? That being said during the lockdown they did manage 393 crores so considering the various unlocks and the amazon sale maybe 500+ crores will be easy enough for them to manage even with physical POS and transactions on the lower side. Walking a valuation tightrope here though

Invested at lower levels and not booked any profit yet but the high valuations are getting me a bit worried

1 Like

597e0a2d-3569-45f2-8465-c5461b9ee015.pdf (3.8 MB)

Annual report

Overall sounds like the perfect mix of conservative yet bullish. Everything is as expected. The outlook looks good and they talk about the conversion to digital happening quicker due to covid throughout. Lots of new digital feature additions that I did not know about. While reading I totally forgot about physical cards and POS payments lol. Probably the only purely fintech play in the market due to the change in mentality post covid and hence why the high valuations. Mentions their long term growth drivers too with updated stats so overall is an interesting read. AGM on September 28th

4 Likes

The article is behind a paywall.

However, the main point is that they are looking at tie-ups with Amazon, Flipkart and even Google pay. The bet that this will become a pure tech play is working out due to them expecting a huge shift to online and slowly acting on it(first the AR and now this). Valuations may be high but they make more and more sense. Tie ups with Google pay removes a potential future threat too.

3 Likes

Exactly…SBI won’t handle sevices, support with customers just like HDFC . Just want to know how many people are really interested by using these cards.

1.“One thing is that the provision of credit bureau score into the account of the credit card holders. When the card holder logs into his account, he should be able to see the credit score. That is very, very common in the US, at no extra charge,” Tewari told PTI.

- In the US, if someone is making a purchase at a retailer and does not have a card, they will ask him to get one, Tewari said. If the person agrees, they will simply ask for his social security number and then issue a card, if the credit score is fine, within 5-10 minutes.

The card may come later, but the number is known and the person can get the benefit of the purchase there and then.

“I think we should be working towards this for getting an extra card at the point of sale at the retailer,” Tewari said.

- So far we are not on UPI, we are tying-up with Google Pay and few other players whereby we will be a partner in this space. But I think for a real value proposition in the UPI space, we have to find a proper business model. So that’s another area I think we need to go quickly and see how we can create value to our customers,” he said.

4 Likes