To me, a large part of the negative pledging factor is already into the price… the co. doesn’t have ALM issues n is growing decently.

That’s why i am neither adding nor selling.

To me, a large part of the negative pledging factor is already into the price… the co. doesn’t have ALM issues n is growing decently.

That’s why i am neither adding nor selling.

I attended the earnings call and glad to note from some previous posts that quite a few friends from this forum were also there. Here are my notes

Notes from the discussion

My comments

Please note that there is possibility that I would have heard things incorrectly, and so points mentioned by me would be factually incorrect. I own shares of Satin and I definitely have ownership bias. This is not a buy or sell recommendation.

Cheers,

Krishna

Hi Krishna, should we communicate to Mr. Singh to finish/reduce pledging given how bad high pledging is taken by the stock market? I guess the loan should be 60-80 cr. against 115 cr. Worth of pledged shares. (We can’t be exact as my question on the concall was cut short by the other guy, not by mr.singh) . That should not a very big amount for mr. Singh, I am guessing.

Thats a good idea. Or we can even initiate to discuss this further with Mr. Singh to have a better sense of nature of borrowing against pledged shares.

You in Delhi NCR by any chance?

Yes Mayank, I am from Delhi ( currently in Delhi) but traveling to Bangalore in few days. Following is the contact page for satin -https://satincreditcare.com/contact-us/

Mayank and Vaibhav - I had reached out to Satin’s management in July 2018 regarding pledging. I also spoke to Company Secretary in length but could not reach to Mr. Singh. However the CS could not give any information on the pledging part. After my phone discussion with CS, I got this reply from their investor relations department

"In this regard, we wish to inform that the Promoters raise money for investing into the company through various sources, Loan Against Shares (LAS) being one of them. This money is utilized to infuse funds in SCNL from time to time, and this practice is in line with the industry norms. "

Frankly I was not impressed with this bookish answer. Based on my experience I would suggest that insisting on meeting Mr. Singh would be a good idea. I am in BLR and so for me personally meeting would not be possible but happy to jump on a call.

Cheers,

Krishna

Frankly speaking, if this this the case that promoters have raised money to invest in satin itself, then it is not such a bad thing at all. May be this is how they have raised funds for subscription to warrants.

Shows:

Am fairly certain that it was cut short on cue by Mr. Singh. So, I would be very surprised if you get a straight answer on this.That sais, I do like the way their overall metrics have improved which is what keeps me interested

Disc: invested from around 300 levels and watching

Couple of comments coming from the CFO of Satin

1- The liquidity situation has improved over the last ten days. Anyway there was not any problem for Satin on this front. However they were cautious because everyone was cautious.

2- The AUM growth would be 30-35% this year.

More details including broader views from the MFI industry captured here https://www.moneycontrol.com/news/business/economy/liquidity-situation-improving-in-financial-sector-rbi-has-done-enough-feel-mfi-players-3205881.html

Cheers,

Krishna

d42c8fa2-b946-4c8b-9478-c7897f24ff4d.pdf (1009.7 KB)

Satin raised 230 Crs NCDs at 11.1% for 5 years (avg maturity around 3.5 years). Great coupon rate for A- rated company. Looks like there is no liquidity issue for satin at least.

In the past few months I have been confused with what’s going on with Satin. Agree that NBFC industry has been witnessing some headwinds but not sure if funding has been an issue here. For record even in the Q2 earnings call Mr. H. P. Singh said that he has money available for lending on tap. He also said that company has more than 1000 crores available which they can lend whenever they want. And even then the company decided to to go slow on increasing the AUM. In the meantime some companies in the MFI sector focused in the same region where Satin has most of its AUM have grown at fast clip. For example Fusion has grown its AUM by 80% plus yoy while Satin slowed down its disbursements.Even the industry average lending rate in Q2 was higher than that of Satin. So I am confused that they had the money to lend and still then did not disburse, and now they are saying that with the infusion of this 213 crores they would expedite lending. Not sure what was stopping them earlier and now what changed that gives them confidence to go big. Overall I do feel that there is something that company has not been sharing openly. I expected them to be conservative in disbursement if they were indeed concerned about NBFC crisis or elections (the main election is still good six months away and not sure that they were waiting for just the assembly elections to get over). The key concerns I have are

1- Why they slowed down in Q2

2- Conversion of warrants issued at much higher price to promoters

3- Even after more than two years since Demo woes are still not over for the company with more than 100 crores of bad loans still still sitting on the book for which provisioning is not done.

4- Continuous pledging.

Cheers,

Krishna

PS: Safe to assume that I would have done transactions in the past month.

Will v see NPAs getting cropped up again with d onset of loan waiver @ state level as well as at National level?

Traditionally NPAs haven’t arised in MFIs due to farm loan waivers because of how the demographic is different and how joint liability works. Moneylife had an article on it:

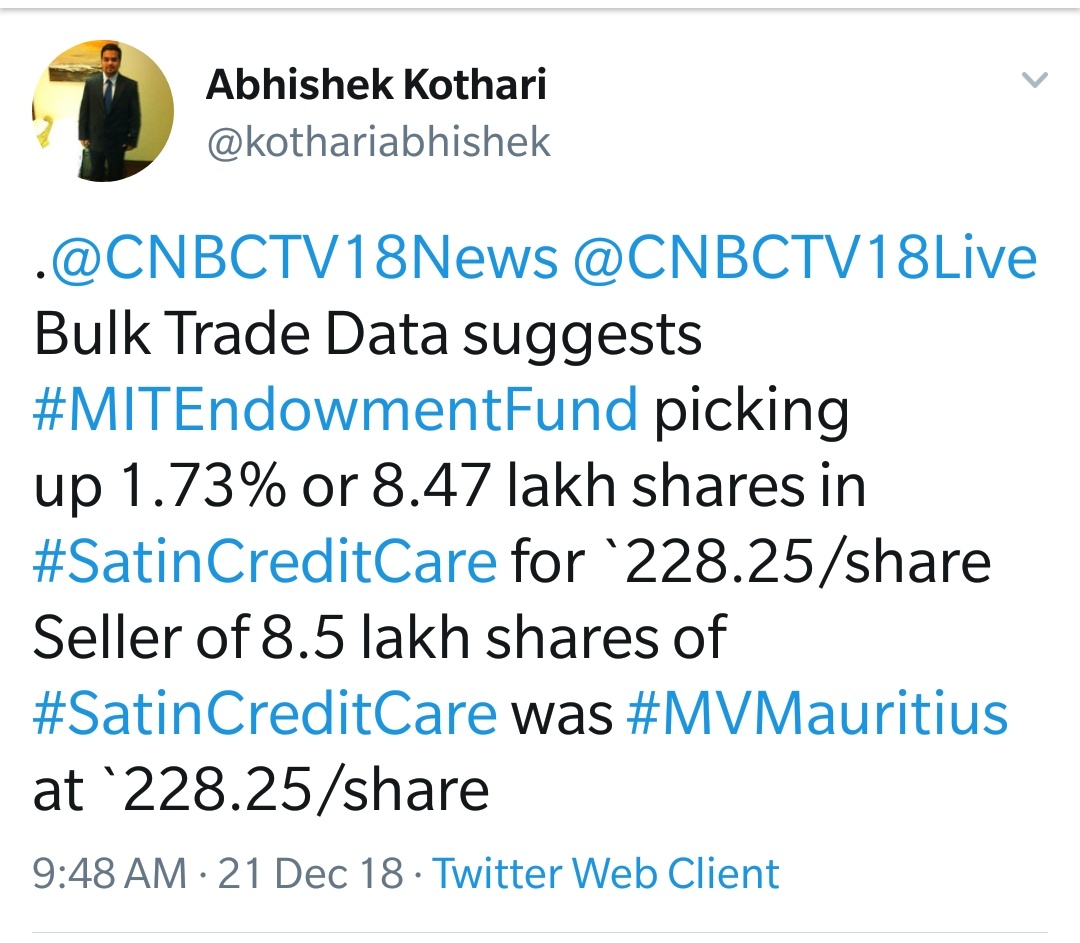

Any idea what’s up with d company, since a week promoter r either acquiring shares r releasing d pledged stakes?

Hi,

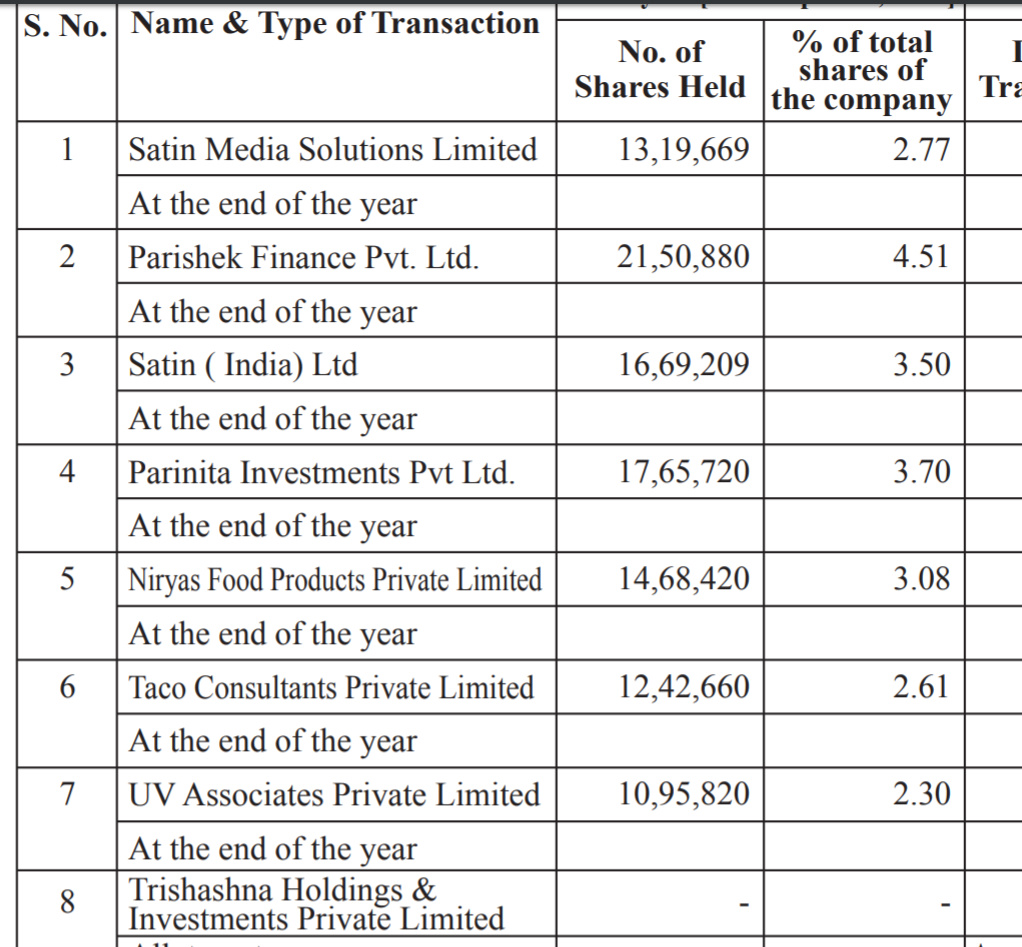

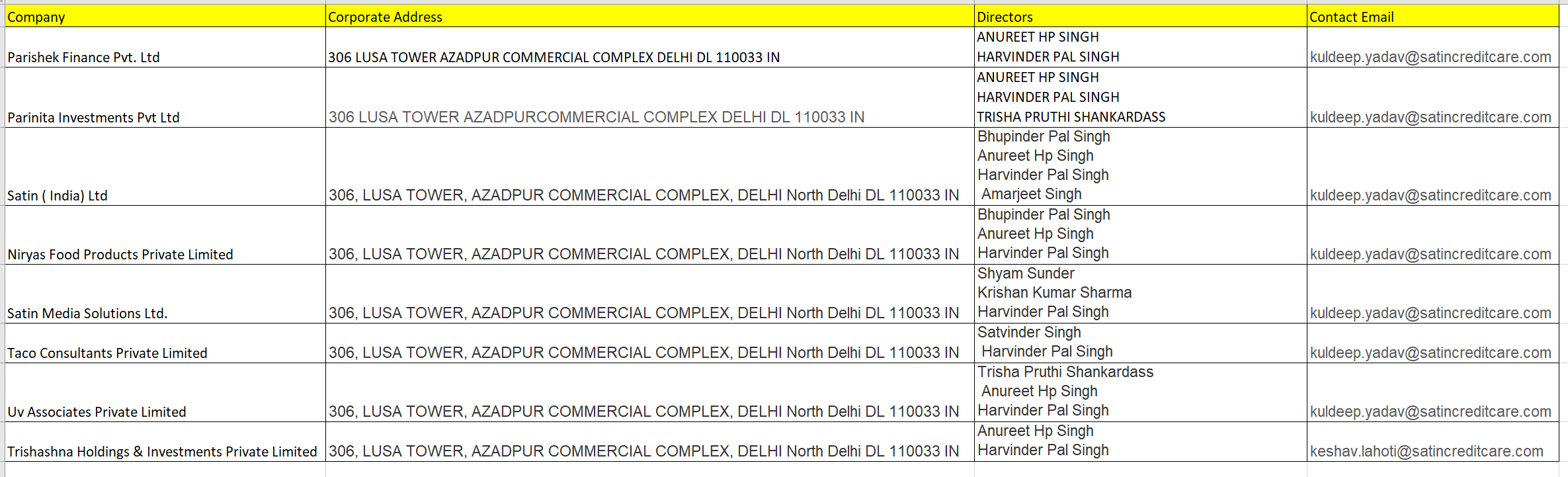

I was looking at shareholding pattern for 2018 in balance sheet, the promotor holding consists of following companies,

When I searched with Company names all companies are registered at same address and directors related to family members,

It looks like that all companies are created for purpose of share holding and there is no sizable business for these companies. Does anybody have more information on promoter quality and why had floated number of companies instead of one holding company. Is there any possibility of diverting company funds to these shell companies?

Disc: Invested in the Company.

You should read Cobrapost article on DHFL thoroughly and try to get balance sheet, profit & loss and charges documents of these companies for the website of MCA.

Good question. Maybe we should wait for Cobrapost to pick it up.

If they wanted to siphon of funds I really don’t think they would use entities which actually own shares in the company and a listed as promoter entities. Lot of companies have this.

Fundamentally the stock is trading at 1.1x book value and will do over 20% roe in FY19. On a 1200 crore market cap the pat will be over 200crores. MFI is not impacted by the NBFC crisis as banks need to focus on priority sector lending. Moreover the company is adequately capitalized with 30% CAR. Growth is expected to be between 20-30% per year. Competitors are trading at 2-3x book value

One risk is farm loan waivers but historically they have limited impact and the companies is taking adequate measures to mitigate the risk.

Sometimes market disruptions give unbelievable opportunities.