This 190 crores is the total provisioning against the total bad loans as of 30th June. Since demonetization the company has provisioned following amounts- Q12019 45 crores, Q42018 25 crores, Q32018 21.41 crores, Q22018 40.81 crores, Q12018 150.28 crores, and Q4-2017 41.66 crores. Some of the bad loans for which provisioning was done is already written off from the books, and some is still left. The part that is left is 212 crores and against that 190 crores provisioning is done. You should read it as of 30th June company had 212 crores as PAR-90 and of this 190 crores is provided for. This leaves 22 crores of unprovided bad laons. However per new Accounting Standards and per ECL the company has fully provided for the bad loans.

No, there is not any such guideline in INDAS. My limited understanding is that ‘Expected Credit Loss’ is new terminology. The calculation of ECL is complex though

ECL = Exposure at Default (ED) x Probability of Default (PD) x Loss Given Default (LGD)

While ED & LGD would be readily available at the time of default for a loan, the PD would vary based on multiple macro variables.

Satin Creditcare Network is expected to file application with RBI for NBFC license of Satin Finserv and will transfer entire MSME business to new entity Satin Finserv. As per few sources company is planning this in next few months.

I was little surprised seeing the BSE notification asking Satin to explain the Business Standard article which spoke about Satin Finserv. There was a notification filed with bourses from Satin about creating this wholly owned subsidiary. Frankly it is kind of compulsion because if the MSME business would surpass 15% upper ceiling of the overall business then Satin would probably not remain classified as MFI-NBFC. And that would have its own implications.

Unrelated, but its been a one way move for Satin last few days with stock sliding to almost Demo lows (I know the absolute low was 250 kind of but stock did not spend much time there). And this has been happening when other MFIs are being (partly/fully) acquired at seemingly high premium. Satin also recently got credit rating upgrade and that should help it keep the borrowing cost a tad stable even in rising interest rate era. Overall confused about the move of stock, but then the slide has been with little volume so not reading much.

Cheers,

Krishna

Can somebody explain more about direct assignment transaction an amount of 250 crores by assigning receivables. A simple google search indicates that these kind of transactions happen at higher interest rates compare to market rates and company taking this kind of loan is hungry for liquidity.

RBI allows banks / NBFCs to sell their portfolio to other financial institutions under ‘Securitization’ guidelines. Securitization allows 2 ways for the selldown:

Direct Assignment: The underlying pool of loans are directly sold to other banks / NBFI

Pass Through Certificate (PTCs): Underlying pool is converted into tranches (aka mortgage tranches / MBS). Other banks / NBFCs / MFs can invest in these PTCs

These tools allow financial institutions to increase the velocity of their balance sheet i.e. they make margin on the pool sold down and then use the released capital / funds to finance new set of borrowers.

Effectively the new investor is taking exposure on the underlying borrowers instead of the NBFCs, but natural the pricing will be higher.

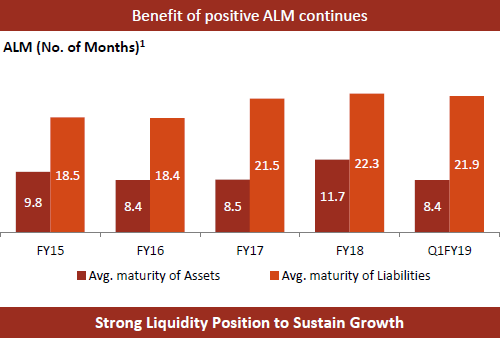

Under normal circumstances I would not have posted this message but given the time we are living in, I thought it is an important news. So Satin raised 38.7 crores at a coupon rate of 11% where interest would be paid semi-annually and the principal would be paid three years later on 26th Oct 2021. It is good to hear that the company is able to raise funds even in these times when liquidity has dried up in the market. Everyone understands the difference between MFI and HFC but both are classified as NBFC and painted with same color. Meanwhile if someone is interested in knowing the ALM situation for Satin then company provided it in the investor presentation at the end of Q1 2018-19 and it looks like

Thanks for this Krishna and I agree with painting everything with the same color even when they are not, They have maintained the lag for liability maturity compared to asset. below is their product portfolio

With such massive correction, I think mkt has overlooked thethe positive changes happening in Satin post demontisation…Positive changes in my view are as follows -

Derisking of thr portfolio by reducing concentration in UP

Tie up with Indusind is a game changer - with respect to liquidity available as they will buy assets of 100 cr per month from them , in terms of technology which will be aligned with Indusind and in terms of processes as well will be aligned with Indusind

Senior ppl of Bharat Financial like COO has joined Satin post demon… Hence i assume they would have benchmarked the operations to the best in class Bharat Financial and taken corrective steps.

Significant investment is technology which she led to cashless disbursement and also real time tracing of all branches

Overall at CMP stock trades at 4 times FY 20 earnings or 0.7 times FY20 book…seems massive undervaluation which should correct soon as fundamentals have improved dramatically

Add to that, company is not facing any liquidity issue. Raised INR NCDs at 11% last month and now raising USD 30M. In fact, liquidity was never a problem even during worst of demo crisis.

Status: holding. Largest position in PF at average price of 340 odd.

That is true Mayank…infact during demon they were raising money at 14 to 15 percent given credit quality issues…Now as no credit quality issues and rating upgrade they are raising money at 11 percent…plus ALM is massively positive and microfinance being priority sector loan will get massive demand from banks for securitisation…

Good presentation with details on ALM, collection efficiency.

Book Value at 206

RoA at 2.7% and RoE at ~19% (annualized)

Mgmt guides 165 cr PAT for FY19

Theres zero ALM issue here obviously. improving prospects after demon. One of the issues (main issue imho) is the promoter pledging. And how much is the loan against that. I was not able to get answers in today’s concall.