From 8th of Feb, promoters are releasing pledged shares.

Disposals are ESOP which are low in value too.

Disc: just studying.

From 8th of Feb, promoters are releasing pledged shares.

Disposals are ESOP which are low in value too.

Disc: just studying.

After all the promoters’ buying from open market and release of pledge:

Promoters’ shareholding in Dec’18: 26.73% (exc. warrants)

Pledged shares of promoters: 52.8%

Promoters’ shareholding in March’19: 27.94% (exc. warrants)

Pledged shares of promoters: 26.32%

Status: Invested (largest holding of portfolio)

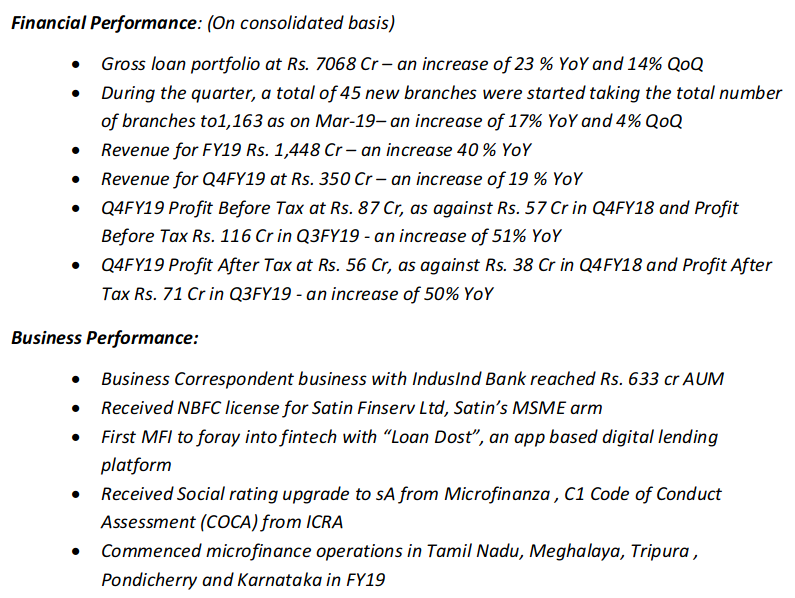

The company recorded a PBT of Rs. 316 Cr for FY19, up by 173 % YoY (Rs 116 Cr in FY18).

RoA and RoE for the year stood at 3.1 % and 19.8 % respectively.

Important to note RoA and RoE as both are negative currently on Screener.in.

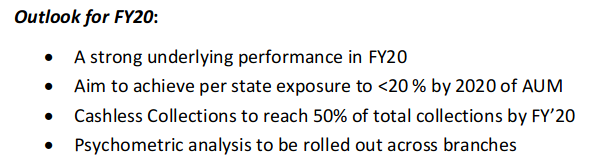

Outlook 2020 given by Satin Creditcare management:

Disc: Not invested

In December 2017 Satin had allotted 1791044 warrants on preferential basis to the promoters. These warrants have to converted to stocks within 18 months on full payment of remaining amount. The warrants were issued at 335/- which is only slightly higher than current market price. Let us see if promoters covert these. Less than three weeks are left for them to do it. The conversion would indicate promoter’s belief in the business, and not doing it would certainly show lack of confidence.

Goes without saying that continuous equity dilution and lots of pledging took a toll on this stock. Over the last few months promoter have bought some shares from open market and they have also been continuously releasing the pledge. But market would take its own time to rebuild the confidence. Conversion of warrants would help in this regard.

Cheers,

Krishna

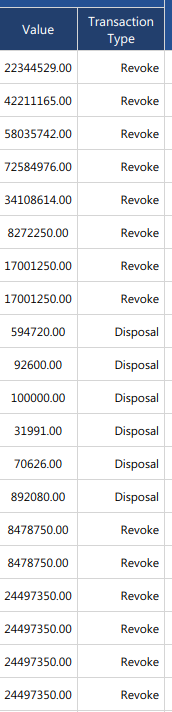

Satin Creditcare insider trade: Revoke of 264,210 equity shares worth Rs 823.01 lacs by promoter

How do you see this?

Acquisitions and Disposal of same numbers of shares and of same value?

Revoke of shares in it is a good news for Satin.

insider trade: Revoke of 758,967 equity shares worth Rs 2273.04 lacs by promoters

insider trade: Disposal of 416,123 equity shares worth Rs 1258.77 lacs by promoters

insider trade: Acquisition of 416,123 equity shares worth Rs 1258.77 lacs by promoters

Seems they have transferred shares from their ( H. P Singh , Anureet H P Singh) names to Promoter group ( Trishashna Holdings & Investments Private Limited). They are consolidating all their shares to one entity, earlier they used to have multiple entities as promoter shareholders ( You can find this in 2018 SH). I am not sure of benefits/implications of this promoter share holding consolidation. Request senior value pickers to throw some light o this.

Another action for the company is, Promoter and IndusInd bank converted their warrants issued on 28th Dec 2017 at an issue price of 335 per share ( No of equity share 31,34,327). It is a good sign for the company and shows promoter confidence in companies future.

Just a guess, they could be consolidating in preparation for making an application to become a small finance bank

Disc: invested

Though I am investor in Satin Credit since 2016 and still holding it in my portfolio.

Few Things which need more brainstorming:

Promoter has been consistently infusing money into the business, must have invested 120cr since FY08. They say promoter doesn’t have any business interest outside listed company. This bringing of huge money along with increasing promoter faith in the business also raises few doubt. Also if you see, his investment, started from 1cr in 2008 and then 8-10cr in 2010-11, some 30cr in 2014-15 and now 60cr in 2018-19. This is growing along with size of the AUM.

Always company were able to raise money when they are going for primary issue at much higher premium. Same investor are not picking stock on-market. Ímmediate after every fund raise, stock goes down.

Cost of Fund: Satin is still raising money at around 12%. Their cost of fund has been consistently high. Hence they must be giving loan to bit more risky customer. If compared to SKS or CreditGrameen, they borrow at 10% or below and hence has to lend at 20%. Though everyone in MFIN business says that at the bottom of pyramid they are not fussy about interest rate, loan should be disburse quickly. In India, everyone is cautious on finally how much is outgo from purse at the end of the month, he may not be able to calculate % and everything but sign of paying higher should be obvious.

New model of BC business. Here capital employed to give Rs100 loan is just 15% of 15% CAR, which they are doing half through cash and rest through bank gaurantee. Company RoE increases multifold in such scenario but if there is any tail event there is risk of entire capital wipe out…

Having said all this, company is trading at 1.2x book value for FY20. Once they reduce Opex ratio which they are on grinding path and AUM growth, which everyone is sounding positive as they are not affected by NBFC crisis. I think it can give 30-40% return lifting valuation to better range of 1.5 - 2.0x.

But real unlocking will happen once any bank buy them out. They have created ideal size of portfolio, which will attract bank, 7000cr and growing. Plus it is expanding branches and customer every quarter. Bank is more interested on reach and customer rather than AUM itself.

Disc Again: Already invested

Satin Creditcare insider trade: Acquisition of 1,791,044 equity shares worth Rs 5220.00 lacs by promoter group.

Disc: tracking

Its warrant conversion to stock

Hi Ravindra, these are interesting points, particularly the one about promoter infusion and source of funds. I’m not sure, but looking at MCA, promoters are directors in several other entities - including construction, food, media, trade and other financial holding companies. In this video (13 min mark), HP Singh explains how he came to start Satin - he had his own accounting practice and was an internal auditor prior to starting - if you see the directorship list, you can see several multiple entities incorporated from 1987 and in 90s. There are also moderate pledges by specialised lenders like Centrum, Reliance and Piramal in these entities, suggesting promoter is leveraging his equity holding in these entities, and through some of them their holding in Satin. The largest such pledge is from Piramal, which is for 20 cr in Nov 2018. Possibly the reason for the contribution growing with AUM is that they are pledging their holding in Satin to raise funds to invest into the business. I am unsure of the sizes of the other businesses, but the promoter group does have outside interests, and has had them for a while. HP Singh however, does not appear to be an MD in any of these besides Satin.

Any idea why was stock down by around 10% yesterday. Couldn’t get anything on the net so asked

Because of rain and floods in 5 states which it operates which could be temporary.As per management concall thing would turn around within couple of quarters as they are focusing on quality growth and diversification of geographies.They also recently re engineered their loan process and geo tagged their branches for real time data. Looks very cheap compared to its peers like Credit access and Spondana. Satin Target by centrum 410.

(http://bsmedia.business-standard.com/_media/bs/data/market-reports/equity-brokertips/2019-11/15734574040.98152300.pdf)

Private Debenture placement at 15% Yield for 7.5 years seems to indicate that company is in deep mess and finding difficult to raise funds. Looks like a signal that asset book quality may not be as good as portrayed.https://www.bseindia.com/xml-data/corpfiling/AttachLive/21771d3f-5949-49b0-a84e-5619f4c25837.pdf

They have become very active on social media. At least there will be one message on daily basis. Any reason why they are marketing themselves aggressively?